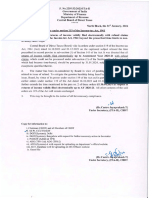

Q.V. Ramirez Vs CA - Mamugay

Q.V. Ramirez Vs CA - Mamugay

You might also like

- Affidavit of Undertaking (Line Officer Pro/Nosu) : DPRM RSD Form-01-A (Revised 2019)Document1 pageAffidavit of Undertaking (Line Officer Pro/Nosu) : DPRM RSD Form-01-A (Revised 2019)Allan Rey Daag50% (4)

- The Importance of Governance and Development and Its Interrelationship (Written Report)Document6 pagesThe Importance of Governance and Development and Its Interrelationship (Written Report)Ghudz Ernest Tambis100% (3)

- Art Acevedo LawsuitDocument52 pagesArt Acevedo LawsuitDavid SeligNo ratings yet

- JM Tuason & Co Inc Vs CADocument2 pagesJM Tuason & Co Inc Vs CASimon James Semilla50% (2)

- Concurrent DelayDocument11 pagesConcurrent DelayZinck HansenNo ratings yet

- Know All Men by These Presents:: Contract To SellDocument4 pagesKnow All Men by These Presents:: Contract To Sellarmchairphilosopher67% (3)

- 5th Weeks Cases in PropertyDocument9 pages5th Weeks Cases in PropertymarkNo ratings yet

- JM Tuason Vs CA Case Digest (Sales)Document2 pagesJM Tuason Vs CA Case Digest (Sales)Samantha ReyesNo ratings yet

- Credtrans CompilationDocument4 pagesCredtrans CompilationEditha RoxasNo ratings yet

- Involuntary Insolvency of Strochecker vs. RamirezDocument1 pageInvoluntary Insolvency of Strochecker vs. RamirezMarc Jethro Mirandilla ManipolNo ratings yet

- JM Tuazon & Co., Inc. v. Court of AppealsDocument2 pagesJM Tuazon & Co., Inc. v. Court of AppealsShella Hannah Salih100% (1)

- Consolidated Rural Bank of Cagayan Valley VDocument5 pagesConsolidated Rural Bank of Cagayan Valley VDerick TorresNo ratings yet

- Cruz and Cruz v. Bancom Finance CorporationDocument4 pagesCruz and Cruz v. Bancom Finance CorporationYvonne MallariNo ratings yet

- Nego Cases - Week 1Document26 pagesNego Cases - Week 1Shery Ann ContadoNo ratings yet

- Rayos Vs CA, Cordero Vs FS MKTGDocument2 pagesRayos Vs CA, Cordero Vs FS MKTGColeenNo ratings yet

- Involuntary Insolvence of Strochecker vs. Ramirez, 44 Phil 933Document1 pageInvoluntary Insolvence of Strochecker vs. Ramirez, 44 Phil 933FranzMordenoNo ratings yet

- Civil Law Review 2 Case DigestsDocument10 pagesCivil Law Review 2 Case DigestsBrigette DomingoNo ratings yet

- Agency and Partnership Digests #2Document8 pagesAgency and Partnership Digests #2Janz Serrano0% (1)

- Rem DigestsDocument10 pagesRem DigestsRoy DaguioNo ratings yet

- Vda. de Bautista vs. Marcos, 3 SCRA 434 Facts: Defendant Marcos Obtained A Loan in The Amount of P2,000 From PlaintiffDocument6 pagesVda. de Bautista vs. Marcos, 3 SCRA 434 Facts: Defendant Marcos Obtained A Loan in The Amount of P2,000 From PlaintiffChristian RoqueNo ratings yet

- G.R. No. 177881 October 13, 2010 Emmanuel C. Villanueva, vs. Cherdan Lending Investors CorporationDocument10 pagesG.R. No. 177881 October 13, 2010 Emmanuel C. Villanueva, vs. Cherdan Lending Investors CorporationMirzi Olga Breech SilangNo ratings yet

- CASE #19 Consolacion P. Chavez, Et - Al. Vs Maybank Philippines, Inc. G.R. No. 242852, July 29, 2019 FactsDocument1 pageCASE #19 Consolacion P. Chavez, Et - Al. Vs Maybank Philippines, Inc. G.R. No. 242852, July 29, 2019 FactsHarlene HemorNo ratings yet

- Atp Case Digests 29 38Document7 pagesAtp Case Digests 29 38Maria RumusudNo ratings yet

- Last 3 Sale DigestDocument5 pagesLast 3 Sale DigestSui Ge NerisNo ratings yet

- Property Law 1-23Document2 pagesProperty Law 1-23Marione John SetoNo ratings yet

- Luzon Brokerage v. Maritime and MyersDocument1 pageLuzon Brokerage v. Maritime and MyersBinkee VillaramaNo ratings yet

- Digest Sales 2Document4 pagesDigest Sales 2Christian ParadoNo ratings yet

- SALES, 1st Bacth, Rayos Vs CADocument2 pagesSALES, 1st Bacth, Rayos Vs CAReina HabijanNo ratings yet

- Sps CO Vs CA & Sps MemijeDocument12 pagesSps CO Vs CA & Sps MemijeAljay DAHANNo ratings yet

- Case Digests in Civil Law Review 2Document74 pagesCase Digests in Civil Law Review 2krystel engcoyNo ratings yet

- 11.strochecker V Ramirez, 44 Phil 933Document2 pages11.strochecker V Ramirez, 44 Phil 933H100% (1)

- Case Digests 2Document5 pagesCase Digests 2arnaldpaguioNo ratings yet

- Pledge Case DigestDocument18 pagesPledge Case DigestAnjela Ching100% (1)

- Case Digest Civil Law 2Document74 pagesCase Digest Civil Law 2Johaima C. DitucalanNo ratings yet

- Afan Vs de GuzmanDocument24 pagesAfan Vs de GuzmanRap PatajoNo ratings yet

- Ballesteros V AbionDocument3 pagesBallesteros V AbionMarion Yves Mosones100% (1)

- Quijada vs. Court of Appeals, Agro V Court of Appeals and Equatorial V Mayfair Case DigestsDocument7 pagesQuijada vs. Court of Appeals, Agro V Court of Appeals and Equatorial V Mayfair Case DigestsGarsha HaleNo ratings yet

- Sam Henderson O. Lofranco PropertyDocument40 pagesSam Henderson O. Lofranco PropertySam Henderson LOFRANCONo ratings yet

- Case Digest SaleDocument11 pagesCase Digest SaleLexa L. DotyalNo ratings yet

- I. Dignos vs. CA FactsDocument5 pagesI. Dignos vs. CA FactsckqashNo ratings yet

- Go Ong vs. Ca G.R. No. 75884 September 24, 1987 FACTS: 2 Parcels of Land Under 1 TCT Are Owned by Alfredo and When He Died, His WifeDocument10 pagesGo Ong vs. Ca G.R. No. 75884 September 24, 1987 FACTS: 2 Parcels of Land Under 1 TCT Are Owned by Alfredo and When He Died, His WifeKrishna AdduruNo ratings yet

- Digest Jam2Document5 pagesDigest Jam2Jam CastilloNo ratings yet

- Guzman DIGESTDocument5 pagesGuzman DIGESTCarmela SalazarNo ratings yet

- Velarde Vs Court of Appeals G.R. No. 108346. July 11, 2001Document2 pagesVelarde Vs Court of Appeals G.R. No. 108346. July 11, 2001Joshua Ouano100% (1)

- Republic of The PhilippinesDocument3 pagesRepublic of The PhilippinesSal PanditaNo ratings yet

- Plaintiffs Avelina and Mariano Velarde (Herein Petitioners) For The Sale of Said Property, Which Was, However, Under LeaseDocument22 pagesPlaintiffs Avelina and Mariano Velarde (Herein Petitioners) For The Sale of Said Property, Which Was, However, Under LeaseThalia SalvadorNo ratings yet

- Case DigestDocument6 pagesCase DigestFlorencio Saministrado Jr.No ratings yet

- (Type Here) Dav3 Digests (Type Here)Document9 pages(Type Here) Dav3 Digests (Type Here)Gusty Ong VañoNo ratings yet

- Hermosa Vs Longara 49 OG 4287Document1 pageHermosa Vs Longara 49 OG 4287Dominic BenjaminNo ratings yet

- Credit CasesDocument6 pagesCredit CasesKFNo ratings yet

- T11.1 Bernardino Ramos Vs CA GR# 111027Document2 pagesT11.1 Bernardino Ramos Vs CA GR# 111027Midzmar KulaniNo ratings yet

- Oblicon - Cases 1-12Document8 pagesOblicon - Cases 1-12ace lagurinNo ratings yet

- MYSALESDocument7 pagesMYSALESjimart10No ratings yet

- Rayos V CADocument1 pageRayos V CArafael.louise.roca2244No ratings yet

- Oblicon 3Document152 pagesOblicon 3Karl Anthony Tence DionisioNo ratings yet

- 51-Paranaque Kings Enterprises vs. CADocument3 pages51-Paranaque Kings Enterprises vs. CAMaribel Nicole Lopez100% (1)

- ToleranceDocument2 pagesToleranceswityioraxNo ratings yet

- Velarde V CA 31 SCRA 56Document1 pageVelarde V CA 31 SCRA 56Eileen Eika Dela Cruz-Lee100% (1)

- BA Finance Corporation vs. Court of AppealsDocument1 pageBA Finance Corporation vs. Court of AppealsTon Ton CananeaNo ratings yet

- Digest CivproDocument69 pagesDigest CivproRay PiñocoNo ratings yet

- ATP CasesDocument24 pagesATP CasesPrince Jheremias Ravina AbrencilloNo ratings yet

- Real Estate and Chattel MortgageDocument9 pagesReal Estate and Chattel MortgageMAASIN CPSNo ratings yet

- AF Realty V DieselmanDocument2 pagesAF Realty V DieselmandmcfloresNo ratings yet

- Dagupan Trading Vs MacamDocument4 pagesDagupan Trading Vs MacamPaolo Antonio EscalonaNo ratings yet

- Summary Votes GovDocument52 pagesSummary Votes GovIan Van MamugayNo ratings yet

- Summary VotesDocument52 pagesSummary VotesIan Van MamugayNo ratings yet

- ACKNOWLEDGMENTForm 1Document1 pageACKNOWLEDGMENTForm 1Ian Van MamugayNo ratings yet

- Fifth Pillar of Cjs - CommunityDocument7 pagesFifth Pillar of Cjs - CommunityIan Van MamugayNo ratings yet

- Updated Payment Instructions 2019NLEDocument12 pagesUpdated Payment Instructions 2019NLEIan Van MamugayNo ratings yet

- Delivery LogDocument2 pagesDelivery LogIan Van MamugayNo ratings yet

- Car PassDocument1 pageCar PassIan Van MamugayNo ratings yet

- Com Res 10741Document13 pagesCom Res 10741Ian Van MamugayNo ratings yet

- Read First Before OpeningDocument1 pageRead First Before OpeningIan Van MamugayNo ratings yet

- Mutuum and Usury Case Digests CompleteDocument16 pagesMutuum and Usury Case Digests CompleteIan Van MamugayNo ratings yet

- Republic of The PhilippinesDocument3 pagesRepublic of The PhilippinesIan Van MamugayNo ratings yet

- CRIMINAL LAW AdDU Bar NotesDocument6 pagesCRIMINAL LAW AdDU Bar NotesIan Van MamugayNo ratings yet

- Republic of The PhilippinesDocument3 pagesRepublic of The PhilippinesIan Van MamugayNo ratings yet

- Bungcaras and Mendoza MRDocument2 pagesBungcaras and Mendoza MRIan Van MamugayNo ratings yet

- Del Monte vs. CA and Sushine Sauce GR L78325, January 25, 1990 FactsDocument2 pagesDel Monte vs. CA and Sushine Sauce GR L78325, January 25, 1990 FactsIan Van MamugayNo ratings yet

- Consti July 11Document2 pagesConsti July 11Ian Van MamugayNo ratings yet

- LEGAL RESEARCH On A Case Involving The Alleged Commission byDocument3 pagesLEGAL RESEARCH On A Case Involving The Alleged Commission byIan Van MamugayNo ratings yet

- Order 119 MiscComm 31 1 24Document6 pagesOrder 119 MiscComm 31 1 24Mmkpss Sriram Sista MmkpssNo ratings yet

- Barangay Captain - Complaint PDFDocument4 pagesBarangay Captain - Complaint PDFrobina56No ratings yet

- Sylvia Walby Eu Gender PDFDocument26 pagesSylvia Walby Eu Gender PDFAdrian StefanNo ratings yet

- SEMINAR Legislative DraftingDocument32 pagesSEMINAR Legislative DraftingYoYoAviNo ratings yet

- Security Training: Intercept Group Pty LTDDocument5 pagesSecurity Training: Intercept Group Pty LTDourpatchNo ratings yet

- Syntel Private Limited: Mumbai Maharashtra IndiaDocument1 pageSyntel Private Limited: Mumbai Maharashtra IndiagssNo ratings yet

- Sanctioning Authorities - Sanctioning Process - Statutory Rules and Regulations - Guideline Value - Property CostDocument22 pagesSanctioning Authorities - Sanctioning Process - Statutory Rules and Regulations - Guideline Value - Property Costvishnu_2008No ratings yet

- ParakramPadak-1112 0Document17 pagesParakramPadak-1112 0AJAY KUMAR DASNo ratings yet

- Philippine ConstitutionDocument7 pagesPhilippine ConstitutionBajado Princes Lenalyn LykaNo ratings yet

- 1905 Aboriginies Act OfficialDocument9 pages1905 Aboriginies Act Officialapi-250562430No ratings yet

- Case Digest PropertyDocument2 pagesCase Digest PropertyJanine Prelle DacanayNo ratings yet

- Local Government Units: Title One. - The BarangayDocument84 pagesLocal Government Units: Title One. - The BarangayNikki GNo ratings yet

- Syllabus - Final PDFDocument14 pagesSyllabus - Final PDFERICANo ratings yet

- Introduction To LawDocument242 pagesIntroduction To Lawderda derdaNo ratings yet

- Contract of Agency MainDocument17 pagesContract of Agency MainAnjali BalanNo ratings yet

- San Beda Bar ReviewDocument2 pagesSan Beda Bar Reviewbearangel10% (3)

- Detail Note On 12-2 - and Judgment ReferencersDocument7 pagesDetail Note On 12-2 - and Judgment ReferencersAbc 123No ratings yet

- Aakash Singh - CVDocument2 pagesAakash Singh - CVAakash Singh BhadwariyaNo ratings yet

- Vicarious Liability JustificationDocument8 pagesVicarious Liability JustificationAryanNo ratings yet

- HeaderDocument40 pagesHeaderFloramae Celine Bosque100% (1)

- Alma LoodDocument1 pageAlma LoodVERA FilesNo ratings yet

- Union County, North Carolina - Request To Join ICE 287 (G) ProgramDocument4 pagesUnion County, North Carolina - Request To Join ICE 287 (G) ProgramJ CoxNo ratings yet

- The Constitution of The United Republic of Tanzania, 1977Document142 pagesThe Constitution of The United Republic of Tanzania, 1977Kessy JumaNo ratings yet

- Essential Elements of A Valid ContractDocument14 pagesEssential Elements of A Valid ContractdevilzniteinNo ratings yet

- Before The Court of Sessions at Jagatpura, State of KingsthanDocument18 pagesBefore The Court of Sessions at Jagatpura, State of KingsthanHarshit Singh Rawat100% (1)

Download as docx, pdf, or txt

You might also like

- Affidavit of Undertaking (Line Officer Pro/Nosu) : DPRM RSD Form-01-A (Revised 2019)Document1 pageAffidavit of Undertaking (Line Officer Pro/Nosu) : DPRM RSD Form-01-A (Revised 2019)Allan Rey Daag50% (4)

- The Importance of Governance and Development and Its Interrelationship (Written Report)Document6 pagesThe Importance of Governance and Development and Its Interrelationship (Written Report)Ghudz Ernest Tambis100% (3)

- Art Acevedo LawsuitDocument52 pagesArt Acevedo LawsuitDavid SeligNo ratings yet

- JM Tuason & Co Inc Vs CADocument2 pagesJM Tuason & Co Inc Vs CASimon James Semilla50% (2)

- Concurrent DelayDocument11 pagesConcurrent DelayZinck HansenNo ratings yet

- Know All Men by These Presents:: Contract To SellDocument4 pagesKnow All Men by These Presents:: Contract To Sellarmchairphilosopher67% (3)

- 5th Weeks Cases in PropertyDocument9 pages5th Weeks Cases in PropertymarkNo ratings yet

- JM Tuason Vs CA Case Digest (Sales)Document2 pagesJM Tuason Vs CA Case Digest (Sales)Samantha ReyesNo ratings yet

- Credtrans CompilationDocument4 pagesCredtrans CompilationEditha RoxasNo ratings yet

- Involuntary Insolvency of Strochecker vs. RamirezDocument1 pageInvoluntary Insolvency of Strochecker vs. RamirezMarc Jethro Mirandilla ManipolNo ratings yet

- JM Tuazon & Co., Inc. v. Court of AppealsDocument2 pagesJM Tuazon & Co., Inc. v. Court of AppealsShella Hannah Salih100% (1)

- Consolidated Rural Bank of Cagayan Valley VDocument5 pagesConsolidated Rural Bank of Cagayan Valley VDerick TorresNo ratings yet

- Cruz and Cruz v. Bancom Finance CorporationDocument4 pagesCruz and Cruz v. Bancom Finance CorporationYvonne MallariNo ratings yet

- Nego Cases - Week 1Document26 pagesNego Cases - Week 1Shery Ann ContadoNo ratings yet

- Rayos Vs CA, Cordero Vs FS MKTGDocument2 pagesRayos Vs CA, Cordero Vs FS MKTGColeenNo ratings yet

- Involuntary Insolvence of Strochecker vs. Ramirez, 44 Phil 933Document1 pageInvoluntary Insolvence of Strochecker vs. Ramirez, 44 Phil 933FranzMordenoNo ratings yet

- Civil Law Review 2 Case DigestsDocument10 pagesCivil Law Review 2 Case DigestsBrigette DomingoNo ratings yet

- Agency and Partnership Digests #2Document8 pagesAgency and Partnership Digests #2Janz Serrano0% (1)

- Rem DigestsDocument10 pagesRem DigestsRoy DaguioNo ratings yet

- Vda. de Bautista vs. Marcos, 3 SCRA 434 Facts: Defendant Marcos Obtained A Loan in The Amount of P2,000 From PlaintiffDocument6 pagesVda. de Bautista vs. Marcos, 3 SCRA 434 Facts: Defendant Marcos Obtained A Loan in The Amount of P2,000 From PlaintiffChristian RoqueNo ratings yet

- G.R. No. 177881 October 13, 2010 Emmanuel C. Villanueva, vs. Cherdan Lending Investors CorporationDocument10 pagesG.R. No. 177881 October 13, 2010 Emmanuel C. Villanueva, vs. Cherdan Lending Investors CorporationMirzi Olga Breech SilangNo ratings yet

- CASE #19 Consolacion P. Chavez, Et - Al. Vs Maybank Philippines, Inc. G.R. No. 242852, July 29, 2019 FactsDocument1 pageCASE #19 Consolacion P. Chavez, Et - Al. Vs Maybank Philippines, Inc. G.R. No. 242852, July 29, 2019 FactsHarlene HemorNo ratings yet

- Atp Case Digests 29 38Document7 pagesAtp Case Digests 29 38Maria RumusudNo ratings yet

- Last 3 Sale DigestDocument5 pagesLast 3 Sale DigestSui Ge NerisNo ratings yet

- Property Law 1-23Document2 pagesProperty Law 1-23Marione John SetoNo ratings yet

- Luzon Brokerage v. Maritime and MyersDocument1 pageLuzon Brokerage v. Maritime and MyersBinkee VillaramaNo ratings yet

- Digest Sales 2Document4 pagesDigest Sales 2Christian ParadoNo ratings yet

- SALES, 1st Bacth, Rayos Vs CADocument2 pagesSALES, 1st Bacth, Rayos Vs CAReina HabijanNo ratings yet

- Sps CO Vs CA & Sps MemijeDocument12 pagesSps CO Vs CA & Sps MemijeAljay DAHANNo ratings yet

- Case Digests in Civil Law Review 2Document74 pagesCase Digests in Civil Law Review 2krystel engcoyNo ratings yet

- 11.strochecker V Ramirez, 44 Phil 933Document2 pages11.strochecker V Ramirez, 44 Phil 933H100% (1)

- Case Digests 2Document5 pagesCase Digests 2arnaldpaguioNo ratings yet

- Pledge Case DigestDocument18 pagesPledge Case DigestAnjela Ching100% (1)

- Case Digest Civil Law 2Document74 pagesCase Digest Civil Law 2Johaima C. DitucalanNo ratings yet

- Afan Vs de GuzmanDocument24 pagesAfan Vs de GuzmanRap PatajoNo ratings yet

- Ballesteros V AbionDocument3 pagesBallesteros V AbionMarion Yves Mosones100% (1)

- Quijada vs. Court of Appeals, Agro V Court of Appeals and Equatorial V Mayfair Case DigestsDocument7 pagesQuijada vs. Court of Appeals, Agro V Court of Appeals and Equatorial V Mayfair Case DigestsGarsha HaleNo ratings yet

- Sam Henderson O. Lofranco PropertyDocument40 pagesSam Henderson O. Lofranco PropertySam Henderson LOFRANCONo ratings yet

- Case Digest SaleDocument11 pagesCase Digest SaleLexa L. DotyalNo ratings yet

- I. Dignos vs. CA FactsDocument5 pagesI. Dignos vs. CA FactsckqashNo ratings yet

- Go Ong vs. Ca G.R. No. 75884 September 24, 1987 FACTS: 2 Parcels of Land Under 1 TCT Are Owned by Alfredo and When He Died, His WifeDocument10 pagesGo Ong vs. Ca G.R. No. 75884 September 24, 1987 FACTS: 2 Parcels of Land Under 1 TCT Are Owned by Alfredo and When He Died, His WifeKrishna AdduruNo ratings yet

- Digest Jam2Document5 pagesDigest Jam2Jam CastilloNo ratings yet

- Guzman DIGESTDocument5 pagesGuzman DIGESTCarmela SalazarNo ratings yet

- Velarde Vs Court of Appeals G.R. No. 108346. July 11, 2001Document2 pagesVelarde Vs Court of Appeals G.R. No. 108346. July 11, 2001Joshua Ouano100% (1)

- Republic of The PhilippinesDocument3 pagesRepublic of The PhilippinesSal PanditaNo ratings yet

- Plaintiffs Avelina and Mariano Velarde (Herein Petitioners) For The Sale of Said Property, Which Was, However, Under LeaseDocument22 pagesPlaintiffs Avelina and Mariano Velarde (Herein Petitioners) For The Sale of Said Property, Which Was, However, Under LeaseThalia SalvadorNo ratings yet

- Case DigestDocument6 pagesCase DigestFlorencio Saministrado Jr.No ratings yet

- (Type Here) Dav3 Digests (Type Here)Document9 pages(Type Here) Dav3 Digests (Type Here)Gusty Ong VañoNo ratings yet

- Hermosa Vs Longara 49 OG 4287Document1 pageHermosa Vs Longara 49 OG 4287Dominic BenjaminNo ratings yet

- Credit CasesDocument6 pagesCredit CasesKFNo ratings yet

- T11.1 Bernardino Ramos Vs CA GR# 111027Document2 pagesT11.1 Bernardino Ramos Vs CA GR# 111027Midzmar KulaniNo ratings yet

- Oblicon - Cases 1-12Document8 pagesOblicon - Cases 1-12ace lagurinNo ratings yet

- MYSALESDocument7 pagesMYSALESjimart10No ratings yet

- Rayos V CADocument1 pageRayos V CArafael.louise.roca2244No ratings yet

- Oblicon 3Document152 pagesOblicon 3Karl Anthony Tence DionisioNo ratings yet

- 51-Paranaque Kings Enterprises vs. CADocument3 pages51-Paranaque Kings Enterprises vs. CAMaribel Nicole Lopez100% (1)

- ToleranceDocument2 pagesToleranceswityioraxNo ratings yet

- Velarde V CA 31 SCRA 56Document1 pageVelarde V CA 31 SCRA 56Eileen Eika Dela Cruz-Lee100% (1)

- BA Finance Corporation vs. Court of AppealsDocument1 pageBA Finance Corporation vs. Court of AppealsTon Ton CananeaNo ratings yet

- Digest CivproDocument69 pagesDigest CivproRay PiñocoNo ratings yet

- ATP CasesDocument24 pagesATP CasesPrince Jheremias Ravina AbrencilloNo ratings yet

- Real Estate and Chattel MortgageDocument9 pagesReal Estate and Chattel MortgageMAASIN CPSNo ratings yet

- AF Realty V DieselmanDocument2 pagesAF Realty V DieselmandmcfloresNo ratings yet

- Dagupan Trading Vs MacamDocument4 pagesDagupan Trading Vs MacamPaolo Antonio EscalonaNo ratings yet

- Summary Votes GovDocument52 pagesSummary Votes GovIan Van MamugayNo ratings yet

- Summary VotesDocument52 pagesSummary VotesIan Van MamugayNo ratings yet

- ACKNOWLEDGMENTForm 1Document1 pageACKNOWLEDGMENTForm 1Ian Van MamugayNo ratings yet

- Fifth Pillar of Cjs - CommunityDocument7 pagesFifth Pillar of Cjs - CommunityIan Van MamugayNo ratings yet

- Updated Payment Instructions 2019NLEDocument12 pagesUpdated Payment Instructions 2019NLEIan Van MamugayNo ratings yet

- Delivery LogDocument2 pagesDelivery LogIan Van MamugayNo ratings yet

- Car PassDocument1 pageCar PassIan Van MamugayNo ratings yet

- Com Res 10741Document13 pagesCom Res 10741Ian Van MamugayNo ratings yet

- Read First Before OpeningDocument1 pageRead First Before OpeningIan Van MamugayNo ratings yet

- Mutuum and Usury Case Digests CompleteDocument16 pagesMutuum and Usury Case Digests CompleteIan Van MamugayNo ratings yet

- Republic of The PhilippinesDocument3 pagesRepublic of The PhilippinesIan Van MamugayNo ratings yet

- CRIMINAL LAW AdDU Bar NotesDocument6 pagesCRIMINAL LAW AdDU Bar NotesIan Van MamugayNo ratings yet

- Republic of The PhilippinesDocument3 pagesRepublic of The PhilippinesIan Van MamugayNo ratings yet

- Bungcaras and Mendoza MRDocument2 pagesBungcaras and Mendoza MRIan Van MamugayNo ratings yet

- Del Monte vs. CA and Sushine Sauce GR L78325, January 25, 1990 FactsDocument2 pagesDel Monte vs. CA and Sushine Sauce GR L78325, January 25, 1990 FactsIan Van MamugayNo ratings yet

- Consti July 11Document2 pagesConsti July 11Ian Van MamugayNo ratings yet

- LEGAL RESEARCH On A Case Involving The Alleged Commission byDocument3 pagesLEGAL RESEARCH On A Case Involving The Alleged Commission byIan Van MamugayNo ratings yet

- Order 119 MiscComm 31 1 24Document6 pagesOrder 119 MiscComm 31 1 24Mmkpss Sriram Sista MmkpssNo ratings yet

- Barangay Captain - Complaint PDFDocument4 pagesBarangay Captain - Complaint PDFrobina56No ratings yet

- Sylvia Walby Eu Gender PDFDocument26 pagesSylvia Walby Eu Gender PDFAdrian StefanNo ratings yet

- SEMINAR Legislative DraftingDocument32 pagesSEMINAR Legislative DraftingYoYoAviNo ratings yet

- Security Training: Intercept Group Pty LTDDocument5 pagesSecurity Training: Intercept Group Pty LTDourpatchNo ratings yet

- Syntel Private Limited: Mumbai Maharashtra IndiaDocument1 pageSyntel Private Limited: Mumbai Maharashtra IndiagssNo ratings yet

- Sanctioning Authorities - Sanctioning Process - Statutory Rules and Regulations - Guideline Value - Property CostDocument22 pagesSanctioning Authorities - Sanctioning Process - Statutory Rules and Regulations - Guideline Value - Property Costvishnu_2008No ratings yet

- ParakramPadak-1112 0Document17 pagesParakramPadak-1112 0AJAY KUMAR DASNo ratings yet

- Philippine ConstitutionDocument7 pagesPhilippine ConstitutionBajado Princes Lenalyn LykaNo ratings yet

- 1905 Aboriginies Act OfficialDocument9 pages1905 Aboriginies Act Officialapi-250562430No ratings yet

- Case Digest PropertyDocument2 pagesCase Digest PropertyJanine Prelle DacanayNo ratings yet

- Local Government Units: Title One. - The BarangayDocument84 pagesLocal Government Units: Title One. - The BarangayNikki GNo ratings yet

- Syllabus - Final PDFDocument14 pagesSyllabus - Final PDFERICANo ratings yet

- Introduction To LawDocument242 pagesIntroduction To Lawderda derdaNo ratings yet

- Contract of Agency MainDocument17 pagesContract of Agency MainAnjali BalanNo ratings yet

- San Beda Bar ReviewDocument2 pagesSan Beda Bar Reviewbearangel10% (3)

- Detail Note On 12-2 - and Judgment ReferencersDocument7 pagesDetail Note On 12-2 - and Judgment ReferencersAbc 123No ratings yet

- Aakash Singh - CVDocument2 pagesAakash Singh - CVAakash Singh BhadwariyaNo ratings yet

- Vicarious Liability JustificationDocument8 pagesVicarious Liability JustificationAryanNo ratings yet

- HeaderDocument40 pagesHeaderFloramae Celine Bosque100% (1)

- Alma LoodDocument1 pageAlma LoodVERA FilesNo ratings yet

- Union County, North Carolina - Request To Join ICE 287 (G) ProgramDocument4 pagesUnion County, North Carolina - Request To Join ICE 287 (G) ProgramJ CoxNo ratings yet

- The Constitution of The United Republic of Tanzania, 1977Document142 pagesThe Constitution of The United Republic of Tanzania, 1977Kessy JumaNo ratings yet

- Essential Elements of A Valid ContractDocument14 pagesEssential Elements of A Valid ContractdevilzniteinNo ratings yet

- Before The Court of Sessions at Jagatpura, State of KingsthanDocument18 pagesBefore The Court of Sessions at Jagatpura, State of KingsthanHarshit Singh Rawat100% (1)