Download as docx, pdf, or txt

You might also like

- Chapter 4 - Teacher's Manual - Ifa Part 1aDocument16 pagesChapter 4 - Teacher's Manual - Ifa Part 1aCharmae Agan CaroroNo ratings yet

- PDFDocument1 pagePDFKumar SamyappanNo ratings yet

- Taiwan airBnBDocument1 pageTaiwan airBnBApril IsidroNo ratings yet

- Black BookDocument55 pagesBlack Bookshubham50% (2)

- Lectures in Finance MathsDocument156 pagesLectures in Finance MathssshnsbNo ratings yet

- Case Digests On Insurance - PremiumDocument6 pagesCase Digests On Insurance - PremiumKatch RoraldoNo ratings yet

- Concealment and Rep, Insular Life v. FelicianoDocument1 pageConcealment and Rep, Insular Life v. FelicianoEman AguileraNo ratings yet

- Geagonia Vs CADocument1 pageGeagonia Vs CAmackNo ratings yet

- Phil Phoenix and UpcbDocument3 pagesPhil Phoenix and UpcbJose CabalumNo ratings yet

- Fortune Medicare, Inc. v. AmorinDocument1 pageFortune Medicare, Inc. v. AmorinperlitainocencioNo ratings yet

- Verendia Vs CADocument1 pageVerendia Vs CAkamiruhyunNo ratings yet

- Fortune Insurance Vs CA May 23 1995Document1 pageFortune Insurance Vs CA May 23 1995Alvin-Evelyn GuloyNo ratings yet

- Malayan Insurance Co. Vs ArnaldoDocument2 pagesMalayan Insurance Co. Vs ArnaldoRenz AmonNo ratings yet

- Insurance Case Digest No. 1-5Document5 pagesInsurance Case Digest No. 1-5KayeNo ratings yet

- Arce Vs Capital InsuranceDocument2 pagesArce Vs Capital InsuranceHency TanbengcoNo ratings yet

- Great Pacific Life vs. CA Case DigestDocument3 pagesGreat Pacific Life vs. CA Case DigestLiana Acuba100% (1)

- Culion Ice Fish and Electric Co Vs Phil Motors CorpDocument2 pagesCulion Ice Fish and Electric Co Vs Phil Motors CorpJerommel GabrielNo ratings yet

- Sun Life Canada Vs Ma. Daisy Et AlDocument2 pagesSun Life Canada Vs Ma. Daisy Et AlLouie SalazarNo ratings yet

- San Beda Insurance Mem AidDocument24 pagesSan Beda Insurance Mem AidchaypatotsNo ratings yet

- On February 8, 1982, Equitable Insurance Corporation Issued Fire Insurance Policy No. 39328 in The Amount of P200,000.00Document5 pagesOn February 8, 1982, Equitable Insurance Corporation Issued Fire Insurance Policy No. 39328 in The Amount of P200,000.00Rvic CivrNo ratings yet

- 129 New Life V CADocument2 pages129 New Life V CAJovelan V. EscañoNo ratings yet

- Ong Lim Sing Vs FEB LeasingDocument1 pageOng Lim Sing Vs FEB Leasingjune bayNo ratings yet

- Florendo v. Philam PlansDocument1 pageFlorendo v. Philam PlansrengieNo ratings yet

- 11 21Document34 pages11 21Anonymous fnlSh4KHIgNo ratings yet

- Carpo Vs ChuaDocument17 pagesCarpo Vs ChuaDarren Joseph del PradoNo ratings yet

- Laura Velasco and Greta AcostaDocument4 pagesLaura Velasco and Greta AcostaSor ElleNo ratings yet

- Edillon v. Manila Bankers Life Assurance, 117 SCRA 187 (1982)Document1 pageEdillon v. Manila Bankers Life Assurance, 117 SCRA 187 (1982)Sopongco Coleen100% (1)

- East Furniture vs. Globe RutgersDocument2 pagesEast Furniture vs. Globe RutgerssandrasulitNo ratings yet

- Great Pacific Life Insurance vs. CADocument1 pageGreat Pacific Life Insurance vs. CALaika CorralNo ratings yet

- Sun Insurance V CADocument3 pagesSun Insurance V CAChanel GarciaNo ratings yet

- 112 GREAT PACIFIC LIFE INSURANCE CORPORATION VS. COURT OF APPEALS and TEODORO CORTEZDocument1 page112 GREAT PACIFIC LIFE INSURANCE CORPORATION VS. COURT OF APPEALS and TEODORO CORTEZJovelan V. EscañoNo ratings yet

- Insurance Case Digests by LuigoDocument3 pagesInsurance Case Digests by LuigoLuigi JaroNo ratings yet

- Insurance Code My ReviewDocument13 pagesInsurance Code My ReviewPursha Monte CaraNo ratings yet

- Cases in Insurance Law (Part I)Document71 pagesCases in Insurance Law (Part I)kingofhearts006No ratings yet

- Definition of An Insurance ContractDocument7 pagesDefinition of An Insurance ContractCarmela ChuaNo ratings yet

- Geagonia vs. CADocument1 pageGeagonia vs. CAOscar E ValeroNo ratings yet

- Philamlife v. Auditor General, 22 SCRA 135 (1968)Document10 pagesPhilamlife v. Auditor General, 22 SCRA 135 (1968)KristineSherikaChyNo ratings yet

- Sps. Cha v. CADocument1 pageSps. Cha v. CAJohn Mark RevillaNo ratings yet

- INSURANCE DIGESTS INC. Atty. MigallosDocument286 pagesINSURANCE DIGESTS INC. Atty. MigallosChristine NarteaNo ratings yet

- SUM - Keppel Cebu Shipyard Inc Vs Pioneer Insurance and Surety Corporation 601 SCRA 96Document3 pagesSUM - Keppel Cebu Shipyard Inc Vs Pioneer Insurance and Surety Corporation 601 SCRA 96Gra syaNo ratings yet

- 5 Insular Life Vs PazDocument2 pages5 Insular Life Vs PazRoger Pascual CuaresmaNo ratings yet

- Insurance Case SummariesDocument31 pagesInsurance Case SummariesRaymund CallejaNo ratings yet

- UCPB vs. MasaganaDocument2 pagesUCPB vs. MasaganaQuennie Mae ZalavarriaNo ratings yet

- Insurance DigestDocument2 pagesInsurance DigestMorphuesNo ratings yet

- Yu Pang Cheng vs. CADocument1 pageYu Pang Cheng vs. CAJohn Mark RevillaNo ratings yet

- Eternal Gardens Memorial Park Corporation vs. The Philippine American Life Insurance Company G.R. No. 166245 April 9, 2008Document7 pagesEternal Gardens Memorial Park Corporation vs. The Philippine American Life Insurance Company G.R. No. 166245 April 9, 2008Claudine Christine A VicenteNo ratings yet

- 02 Country Bankers Insurance Corporation vs. Lianga Bay and Community Multi-Purpose Cooperative, Inc.Document16 pages02 Country Bankers Insurance Corporation vs. Lianga Bay and Community Multi-Purpose Cooperative, Inc.ATR100% (1)

- ANTONINA LAMPANOvDocument5 pagesANTONINA LAMPANOvYour Public ProfileNo ratings yet

- Oriental Assurance v. Court of Appeals, 200 SCRA 459 (1991)Document2 pagesOriental Assurance v. Court of Appeals, 200 SCRA 459 (1991)Sopongco ColeenNo ratings yet

- Grepalife vs. CADocument3 pagesGrepalife vs. CARenz AmonNo ratings yet

- Lorca Vs Dineros 103 Phil 122Document10 pagesLorca Vs Dineros 103 Phil 122Ashley CandiceNo ratings yet

- White Gold Marine Services Vs Pioneer (GR 154514)Document1 pageWhite Gold Marine Services Vs Pioneer (GR 154514)Marge OstanNo ratings yet

- American Home Assurance Co. v. Chua, 1999Document2 pagesAmerican Home Assurance Co. v. Chua, 1999Randy SiosonNo ratings yet

- Great Pacific Life Assurance Corp v. CADocument7 pagesGreat Pacific Life Assurance Corp v. CALea Gabrielle FariolaNo ratings yet

- Perez v. CA, 323 SCRA 613 (2000)Document5 pagesPerez v. CA, 323 SCRA 613 (2000)KristineSherikaChyNo ratings yet

- Digest InsuranceDocument28 pagesDigest InsuranceFayda Cariaga100% (1)

- (Insurance) Fortune vs. CADocument2 pages(Insurance) Fortune vs. CARaphael PangalanganNo ratings yet

- 2 1 InsuranceDocument6 pages2 1 InsuranceLeo GuillermoNo ratings yet

- 14 Lalican v. Insular Life Assurance Co.Document3 pages14 Lalican v. Insular Life Assurance Co.Patricia IgnacioNo ratings yet

- Musngi Vs West Coast Life Insurance Co.Document2 pagesMusngi Vs West Coast Life Insurance Co.Abhor TyrannyNo ratings yet

- Gaisano vs. Development Insurance and Surety CorporationDocument12 pagesGaisano vs. Development Insurance and Surety CorporationAaron CarinoNo ratings yet

- Case DigestDocument2 pagesCase Digestj guevarraNo ratings yet

- 48 Philippine American Life Insurance Co. v. PinedaDocument3 pages48 Philippine American Life Insurance Co. v. PinedaKaryl Eric BardelasNo ratings yet

- The Young Adult Starter Kit: 12 Steps To Being A Better Person: YA Self-HelpFrom EverandThe Young Adult Starter Kit: 12 Steps To Being A Better Person: YA Self-HelpNo ratings yet

- Insurance (Cases On Premium)Document14 pagesInsurance (Cases On Premium)nojaywalkngNo ratings yet

- Artemio Iniego V. The Honorable Judge Guillermo G. Purganan, and Fokker C. Santos G. R. No. 166876 March 24, 2006Document2 pagesArtemio Iniego V. The Honorable Judge Guillermo G. Purganan, and Fokker C. Santos G. R. No. 166876 March 24, 2006ninaNo ratings yet

- Joint Affidavit-Complaint: IN WITNESS WHEREOF, We Have Hereunto Set Our Hands This - Day ofDocument1 pageJoint Affidavit-Complaint: IN WITNESS WHEREOF, We Have Hereunto Set Our Hands This - Day ofninaNo ratings yet

- R.A. 386 The Civil Code of The Philippines: Lease of Residential HouseDocument1 pageR.A. 386 The Civil Code of The Philippines: Lease of Residential HouseninaNo ratings yet

- July 2017 Labor CasesDocument2 pagesJuly 2017 Labor CasesninaNo ratings yet

- R.A. 386 The Civil Code of The Philippines: Contract To SellDocument1 pageR.A. 386 The Civil Code of The Philippines: Contract To SellninaNo ratings yet

- Collective Bargaining AgreementDocument1 pageCollective Bargaining AgreementninaNo ratings yet

- Last Will and TestamentDocument1 pageLast Will and TestamentninaNo ratings yet

- Deed of Sale of Large CattleDocument1 pageDeed of Sale of Large CattleninaNo ratings yet

- Sale of Personal Property in Installment With MortgageDocument1 pageSale of Personal Property in Installment With MortgageninaNo ratings yet

- Deed of Sale of A Registered LandDocument1 pageDeed of Sale of A Registered LandninaNo ratings yet

- PVB V CallanganDocument2 pagesPVB V CallanganninaNo ratings yet

- Golden Sun Finance V AlbanoDocument1 pageGolden Sun Finance V AlbanoninaNo ratings yet

- Demand LetterDocument2 pagesDemand Letternina100% (1)

- Macalalag V OmbudsmanDocument2 pagesMacalalag V OmbudsmanninaNo ratings yet

- Maglana V ConsolacionDocument1 pageMaglana V ConsolacionninaNo ratings yet

- Canon 3Document1 pageCanon 3ninaNo ratings yet

- La Sallete College V PilotinDocument2 pagesLa Sallete College V PilotinninaNo ratings yet

- Sunlife V CADocument1 pageSunlife V CAninaNo ratings yet

- Canon 3Document1 pageCanon 3ninaNo ratings yet

- Amendment of Application SLOCPIDocument1 pageAmendment of Application SLOCPIChristine Joy PrestozaNo ratings yet

- PACRA Rating Transition CriteriaDocument14 pagesPACRA Rating Transition Criteriarizwanahmed350No ratings yet

- Thesis On Good GovernanceDocument25 pagesThesis On Good GovernanceJoshua Eric Velasco DandalNo ratings yet

- Gerard Amedio Chapter 13 BankruptcyDocument67 pagesGerard Amedio Chapter 13 BankruptcyWendy LiberatoreNo ratings yet

- Cost Allocation, Customer-Profitability Analysis, and Sales-Variance AnalysisDocument59 pagesCost Allocation, Customer-Profitability Analysis, and Sales-Variance AnalysisHarold Dela Fuente100% (1)

- Bajaj Allianz Summer TrainingDocument46 pagesBajaj Allianz Summer TrainingAman BajajNo ratings yet

- Amal Andraos ResumeDocument4 pagesAmal Andraos Resumeapi-275860073No ratings yet

- THE Insurance Code of The Philippines (Pres. Decree No. 1460, As Amended.) General ProvisionsDocument13 pagesTHE Insurance Code of The Philippines (Pres. Decree No. 1460, As Amended.) General ProvisionsDonna TreceñeNo ratings yet

- IT Contract SampleDocument46 pagesIT Contract SamplebalmazanNo ratings yet

- YBM GST Invoice FormatDocument4 pagesYBM GST Invoice FormatMl AgarwalNo ratings yet

- 9AKK102951 ABB Supplier Qualification QuestionnaireDocument6 pages9AKK102951 ABB Supplier Qualification Questionnairesudar1477No ratings yet

- Issuance of Certificate of Irrigation CoverageDocument1 pageIssuance of Certificate of Irrigation CoverageLenie Ricardo Dela CruzNo ratings yet

- Balance Sheet of Bandhan BankDocument4 pagesBalance Sheet of Bandhan BankAditya Kumar SahNo ratings yet

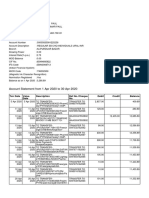

- Account Statement From 1 Apr 2020 To 30 Apr 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceDocument2 pagesAccount Statement From 1 Apr 2020 To 30 Apr 2020: TXN Date Value Date Description Ref No./Cheque No. Debit Credit BalanceSubham PaulNo ratings yet

- Current Trends and Challenges of Micro Finance in IndiaDocument10 pagesCurrent Trends and Challenges of Micro Finance in IndiaAkila TharunNo ratings yet

- Deletion of Account Holders PDFDocument1 pageDeletion of Account Holders PDFSophia ShafiNo ratings yet

- Itisthe2 Steps in The Accounting Cycle. It Is Also Called As The Book of Final Entries?Document11 pagesItisthe2 Steps in The Accounting Cycle. It Is Also Called As The Book of Final Entries?Noel BuctotNo ratings yet

- Electronics Projects VolDocument1 pageElectronics Projects Volmuthurajan_hNo ratings yet

- Anshu Bba5th SemDocument85 pagesAnshu Bba5th Semanshu jainNo ratings yet

- Case Moss and Mcadams Accounting FirmDocument3 pagesCase Moss and Mcadams Accounting FirmNiranjan PatelNo ratings yet

- PDFDocument2 pagesPDFRagini AshokNo ratings yet

- Invest Hedge September 2010 - Billion Dollar ClubDocument6 pagesInvest Hedge September 2010 - Billion Dollar ClubEden Rock Capital ManagementNo ratings yet

- VguardfinalDocument324 pagesVguardfinalmuthoot2009No ratings yet

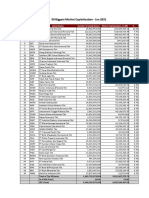

- 50 Biggest Market Capitalization - Jan 2021Document1 page50 Biggest Market Capitalization - Jan 2021Aditya WidiyadiNo ratings yet

- India Infoline Company ProfileDocument12 pagesIndia Infoline Company ProfileGowri MbaNo ratings yet