Download as pdf or txt

You might also like

- Lead and Disrupt: How to Solve the Innovator's Dilemma, Second EditionFrom EverandLead and Disrupt: How to Solve the Innovator's Dilemma, Second EditionRating: 5 out of 5 stars5/5 (1)

- The Invincible Company: How to Constantly Reinvent Your Organization with Inspiration From the World's Best Business ModelsFrom EverandThe Invincible Company: How to Constantly Reinvent Your Organization with Inspiration From the World's Best Business ModelsNo ratings yet

- Case Solution Titanium DioxideDocument4 pagesCase Solution Titanium Dioxideanmolsaini01No ratings yet

- The Alchemy of Growth PDFDocument24 pagesThe Alchemy of Growth PDFpalenciaaNo ratings yet

- Financial Services: Securities Firms and Investment Banks: True / False QuestionsDocument30 pagesFinancial Services: Securities Firms and Investment Banks: True / False Questionslatifa hn100% (1)

- Mark SPitznagel - Different Black SwanDocument14 pagesMark SPitznagel - Different Black SwanVinny Sareen100% (4)

- Accenture Breaking Through Disruption Embrace The Power of The Wise PivotDocument37 pagesAccenture Breaking Through Disruption Embrace The Power of The Wise PivotLenninger von TeeseNo ratings yet

- Writing A Credible Investment Thesis - HBS Working KnowledgeDocument6 pagesWriting A Credible Investment Thesis - HBS Working KnowledgejgravisNo ratings yet

- Fortune at The Bottom of The Innovation Pyramid: The Strategic Logic of Incremental InnovationsDocument9 pagesFortune at The Bottom of The Innovation Pyramid: The Strategic Logic of Incremental Innovationsafcpa7No ratings yet

- Introduction And: Entrepreneurial Finance Leach & MelicherDocument33 pagesIntroduction And: Entrepreneurial Finance Leach & MelicherNadzirah Mohd SaidNo ratings yet

- EBSCO FullText 2023 04 22Document12 pagesEBSCO FullText 2023 04 22Ricardo RNo ratings yet

- MckinseyDocument24 pagesMckinseymoh0001No ratings yet

- 080 Strategy+business Magazine Autumn 2015Document120 pages080 Strategy+business Magazine Autumn 2015Yevhen KurilovNo ratings yet

- The Big Market Delusion Valuation and Investment ImplicationsDocument12 pagesThe Big Market Delusion Valuation and Investment ImplicationsblacksmithMGNo ratings yet

- Cohen-TOP 10 Reasons Why We Need INNOVATIONDocument4 pagesCohen-TOP 10 Reasons Why We Need INNOVATIONChristine DautNo ratings yet

- James M Higgins 101 Creative Problem Solving Techniques - RemovedDocument114 pagesJames M Higgins 101 Creative Problem Solving Techniques - RemovedNely Noer SofwatiNo ratings yet

- The Foundations of Entrepreneurship: Section IDocument40 pagesThe Foundations of Entrepreneurship: Section IAbdullahNo ratings yet

- Is Your Innovation Breaking DownDocument3 pagesIs Your Innovation Breaking Downma ChakaNo ratings yet

- Kauffman Index 2017: Growth Entrepreneurship Metropolitan Area and City TrendsDocument28 pagesKauffman Index 2017: Growth Entrepreneurship Metropolitan Area and City TrendsThe Ewing Marion Kauffman Foundation100% (1)

- Strategies For GrowthDocument8 pagesStrategies For GrowthadillawaNo ratings yet

- Capitulo 1 Innovation at The CoreDocument20 pagesCapitulo 1 Innovation at The CoreAntonio BaezNo ratings yet

- The Art of Supply Change Management: January 2009Document9 pagesThe Art of Supply Change Management: January 2009Sarmad HashimNo ratings yet

- Idea Generation and How To Read A 10KDocument12 pagesIdea Generation and How To Read A 10Kigotsomuchwin100% (1)

- Summary and Analysis of The Innovator's Dilemma: When New Technologies Cause Great Firms to Fail: Based on the Book by Clayton ChristensenFrom EverandSummary and Analysis of The Innovator's Dilemma: When New Technologies Cause Great Firms to Fail: Based on the Book by Clayton ChristensenRating: 4.5 out of 5 stars4.5/5 (5)

- Managing Organisational and Management Challenges in India: NTPC SipatDocument17 pagesManaging Organisational and Management Challenges in India: NTPC SipatVIJAYPORNo ratings yet

- BCG Creating Urgency Amid Comfort Feb 2018 Tcm9 184546Document5 pagesBCG Creating Urgency Amid Comfort Feb 2018 Tcm9 184546Timothy TuasonNo ratings yet

- Practically Radical: A Game Plan For Game ChangersDocument18 pagesPractically Radical: A Game Plan For Game Changersapi-20526161No ratings yet

- Creative Construction - The DNA of Sustained InnovationDocument6 pagesCreative Construction - The DNA of Sustained InnovationMoncheNo ratings yet

- How To Build A Unicorn Lessons From Venture Capitalists and Start UpsDocument7 pagesHow To Build A Unicorn Lessons From Venture Capitalists and Start UpsKheylee VegaNo ratings yet

- The Success of Persistent EntrepreneursDocument2 pagesThe Success of Persistent EntrepreneursHBSWK100% (9)

- BCG - Corporate Venture Capital (Oct - 2012)Document21 pagesBCG - Corporate Venture Capital (Oct - 2012)ddubyaNo ratings yet

- Business Model Innovation - Deloitte ConsultingDocument28 pagesBusiness Model Innovation - Deloitte Consultingamine.luuckNo ratings yet

- Chaotics: The Business of Managing and Marketing in The Age of Turbulence Sample Chapter by Philip Kotler and John A. CaslioneDocument28 pagesChaotics: The Business of Managing and Marketing in The Age of Turbulence Sample Chapter by Philip Kotler and John A. CaslioneAMACOM, Publishing Division of the American Management Association100% (1)

- Diversity Wins: How Inclusion MattersDocument56 pagesDiversity Wins: How Inclusion MattersdgNo ratings yet

- Disruptive or Discontinuos InnovationDocument5 pagesDisruptive or Discontinuos Innovationankit_rihalNo ratings yet

- Exploring The Innovation PyramidDocument3 pagesExploring The Innovation PyramidAbNo ratings yet

- L3-O'reilly, Binns - 2019 - The Three Stages of Disruptive Innovation Idea Generation, Incubation, and ScalingDocument24 pagesL3-O'reilly, Binns - 2019 - The Three Stages of Disruptive Innovation Idea Generation, Incubation, and ScalinghuangNo ratings yet

- Managing Serious ChangeDocument48 pagesManaging Serious ChangeAdrianaNo ratings yet

- After LehmanDocument3 pagesAfter LehmanSuhas JambhaleNo ratings yet

- MoF Issue 20Document24 pagesMoF Issue 20qweenNo ratings yet

- Crisis As Antecedent of InnovationDocument6 pagesCrisis As Antecedent of InnovationSrirang JhaNo ratings yet

- The Mount Vernon Report October 2001 - Vol. 1, No. 1Document4 pagesThe Mount Vernon Report October 2001 - Vol. 1, No. 1Morrissey and CompanyNo ratings yet

- Zook On The CoreDocument9 pagesZook On The CoreThu NguyenNo ratings yet

- C Baradello - SC Tech Products - 2018Document114 pagesC Baradello - SC Tech Products - 2018Johanna LopezNo ratings yet

- Session3 PDFDocument30 pagesSession3 PDFcalvin gastaudNo ratings yet

- Cite Seer XDocument15 pagesCite Seer XRajat SharmaNo ratings yet

- HBR 2011 ZookAllenDocument9 pagesHBR 2011 ZookAlleny1301401755No ratings yet

- Building A Business1Document3 pagesBuilding A Business1Oluwasegun ModupeNo ratings yet

- How To Build A Unicorn: Lessons From Venture Capitalists and Start-UpsDocument7 pagesHow To Build A Unicorn: Lessons From Venture Capitalists and Start-UpsNext GenNo ratings yet

- Dynamo: Paths of GrowthDocument10 pagesDynamo: Paths of GrowthSébastien HerrmannNo ratings yet

- The Overconfidence TrapDocument8 pagesThe Overconfidence TrapAbrahamRoshNo ratings yet

- The Founder’s Roadmap to $100 Million ARR by Bessemer Venture PartnersDocument130 pagesThe Founder’s Roadmap to $100 Million ARR by Bessemer Venture PartnersJaideepMannNo ratings yet

- #Executive SummariesDocument5 pages#Executive SummariesNgô TuấnNo ratings yet

- The Structure of Strategy - John KayDocument21 pagesThe Structure of Strategy - John Kayjoe abdullahNo ratings yet

- On The Importance of Sustainable Human Resource Management For The Adoption of Sustainable Development GoalsDocument54 pagesOn The Importance of Sustainable Human Resource Management For The Adoption of Sustainable Development GoalsparsadNo ratings yet

- 5-1 Deloitte Mastering Innovation Exploiting Ideas For Profitable GrowthDocument24 pages5-1 Deloitte Mastering Innovation Exploiting Ideas For Profitable GrowthWentian HsiehNo ratings yet

- Transcription - Org ViabilityDocument5 pagesTranscription - Org Viabilitymanoj reddyNo ratings yet

- The Well-Timed Strategy (Review and Analysis of Navarro's Book)From EverandThe Well-Timed Strategy (Review and Analysis of Navarro's Book)No ratings yet

- Designing Corporate Venturing Capital Successfully Startup Intellect Featured Insight Report FinalDocument24 pagesDesigning Corporate Venturing Capital Successfully Startup Intellect Featured Insight Report Finalali sharifzadehNo ratings yet

- Buku PDFDocument9 pagesBuku PDFradianNo ratings yet

- Do Innovating FirmsDocument17 pagesDo Innovating FirmsMAGALY ALBANNY BUSTAMANTE HIGINIONo ratings yet

- Harvard Business ReviewDocument3 pagesHarvard Business Reviewcorradopassera100% (1)

- L18 Persuade Change HBR 2022EnFebDocument7 pagesL18 Persuade Change HBR 2022EnFebMarcelo PosadasNo ratings yet

- Bain - Corporate VenturingDocument12 pagesBain - Corporate VenturingddubyaNo ratings yet

- Big Picture in Focus: Ulob. Differentiate The Types of Financial MarketsDocument10 pagesBig Picture in Focus: Ulob. Differentiate The Types of Financial MarketsJohn Stephen PendonNo ratings yet

- Exam 1 PDFDocument4 pagesExam 1 PDFFiraa'ool YusufNo ratings yet

- Dividend Policy, Business Economics & Finance B Com NotesDocument4 pagesDividend Policy, Business Economics & Finance B Com NotesMr. Rain ManNo ratings yet

- Lecture 7-Risk & ReturnDocument58 pagesLecture 7-Risk & ReturnSour CandyNo ratings yet

- Traders QuotesDocument53 pagesTraders QuotesTaresaNo ratings yet

- MicroCap Review Summer/Fall 2014Document96 pagesMicroCap Review Summer/Fall 2014Planet MicroCap Review MagazineNo ratings yet

- NZX Ecoya Media ReleaseDocument4 pagesNZX Ecoya Media ReleaseAlphatrader.co.nzNo ratings yet

- Project (Axis Mutul Fund)Document128 pagesProject (Axis Mutul Fund)nandish30No ratings yet

- Ar PDFDocument255 pagesAr PDFPRAVEEENGODARANo ratings yet

- Risk and Return Thuyết TrìnhDocument16 pagesRisk and Return Thuyết Trìnhdinhduongle2004No ratings yet

- IB Session 1Document34 pagesIB Session 1Pulokesh GhoshNo ratings yet

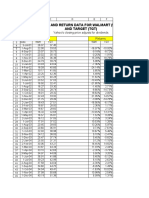

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument19 pagesPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsSyed Ameer Ali ShahNo ratings yet

- Harnish Inc Acquired 25 of The Outstanding Common Shares ofDocument1 pageHarnish Inc Acquired 25 of The Outstanding Common Shares ofFreelance WorkerNo ratings yet

- Quiz 2 - Linear ProgrammingDocument2 pagesQuiz 2 - Linear ProgrammingSandra AndradeNo ratings yet

- Cost of CapitalDocument56 pagesCost of CapitalAndayani SalisNo ratings yet

- The Role of Pension Funds in Financing Green Growth InitiativesDocument70 pagesThe Role of Pension Funds in Financing Green Growth InitiativesJorkosNo ratings yet

- ELEC 101-Behavioral FinanceDocument12 pagesELEC 101-Behavioral FinanceKier Arven SallyNo ratings yet

- Dividend Policy - Traditional PositionDocument7 pagesDividend Policy - Traditional PositionVaidyanathan Ravichandran67% (3)

- IFCDocument2 pagesIFCaltemurcan kursunluNo ratings yet

- Rakesh JhunjhunwalaDocument11 pagesRakesh Jhunjhunwalachinmay 1001No ratings yet

- FSA IFRS Test QuestionsDocument51 pagesFSA IFRS Test QuestionsArmand Hajdaraj33% (3)

- Basics of Share and DebentureDocument14 pagesBasics of Share and DebentureChaman SinghNo ratings yet

- Objectives & Scope of Portfolio ManagementDocument4 pagesObjectives & Scope of Portfolio ManagementGourav BaidNo ratings yet

- Microsoft PowerPoint - Finance FunctionDocument13 pagesMicrosoft PowerPoint - Finance FunctionBatenda FelixNo ratings yet

- Ca Ipcc - FM: - Covered in This File - Click Here - Click HereDocument63 pagesCa Ipcc - FM: - Covered in This File - Click Here - Click HereVarun MurthyNo ratings yet

- Akm 2 Week 11Document3 pagesAkm 2 Week 11Ahsan FirdausNo ratings yet