Download as pdf or txt

You might also like

- Teuer Furniture Students ExcelDocument19 pagesTeuer Furniture Students ExcelAlfonsoNo ratings yet

- Chapter 2 Solutions - Matching Supply With DemandDocument13 pagesChapter 2 Solutions - Matching Supply With Demanddonutshop100% (1)

- Analysis of Ott Platforms - Sec - HDocument25 pagesAnalysis of Ott Platforms - Sec - HChirag Laxman100% (2)

- Submitted By: Narendra Singh USN: 19MBAR0271 Bfas: Assignment-2 Module 2 Operations ManagementDocument5 pagesSubmitted By: Narendra Singh USN: 19MBAR0271 Bfas: Assignment-2 Module 2 Operations ManagementNarendra SinghNo ratings yet

- Vietnam Paint MarketDocument3 pagesVietnam Paint Marketmeocon124No ratings yet

- Flow Valuation, Case #KEL778Document31 pagesFlow Valuation, Case #KEL778javaid jamshaidNo ratings yet

- BNCM - JM L UhlnygkfDocument28 pagesBNCM - JM L UhlnygkfReckon IndepthNo ratings yet

- Teuer Furniture - Student Supplementary SheetDocument20 pagesTeuer Furniture - Student Supplementary Sheetsergio songuiNo ratings yet

- Flow Valuation, Case #KEL778Document20 pagesFlow Valuation, Case #KEL778SreeHarshaKazaNo ratings yet

- Group 13 - ME Group Assignment 2Document8 pagesGroup 13 - ME Group Assignment 2deepak krishnanNo ratings yet

- Consumer Durable Industry in India: School of Management StudiesDocument15 pagesConsumer Durable Industry in India: School of Management Studiespragnesh22No ratings yet

- Mobile Industry Overview & Average Revenue Per (Mobile) User in PakistanDocument8 pagesMobile Industry Overview & Average Revenue Per (Mobile) User in PakistanshirjeelzafarNo ratings yet

- Titan Company by Anuj GuptaDocument25 pagesTitan Company by Anuj GuptaHIMANSHU RAWATNo ratings yet

- Consumer Durable PDFDocument21 pagesConsumer Durable PDFAMIT KUMAR100% (3)

- Leec1er PDFDocument9 pagesLeec1er PDFShubham RankaNo ratings yet

- Creative Industries Economic Estimates Statistical Bulletin: September 2006Document15 pagesCreative Industries Economic Estimates Statistical Bulletin: September 2006420No ratings yet

- Eugene/Springfield Metropolitan Employment Projections by Sector, 1995 To 2020Document5 pagesEugene/Springfield Metropolitan Employment Projections by Sector, 1995 To 2020huntinxNo ratings yet

- Bottled Water IndustryDocument17 pagesBottled Water IndustrySriramVenkat100% (1)

- 2020-2029 - Tielco - Tablas Island - PSPPDocument18 pages2020-2029 - Tielco - Tablas Island - PSPPHans CunananNo ratings yet

- S.W.O.T Analysis 2015 - SouthDocument13 pagesS.W.O.T Analysis 2015 - Southpallavsharma1987No ratings yet

- Press Information Bureau Government of India New DelhiDocument10 pagesPress Information Bureau Government of India New DelhiKaushal MandaliaNo ratings yet

- Icfai National College: JaipurDocument15 pagesIcfai National College: JaipurShelly BhartiNo ratings yet

- PSD ProgrammeDocument28 pagesPSD ProgrammeedwardNo ratings yet

- Korean Dairy SectorDocument13 pagesKorean Dairy SectorVindula PussepitiyaNo ratings yet

- TT KPI Rate 1 2 3: I Ingame StatisticDocument5 pagesTT KPI Rate 1 2 3: I Ingame StatisticNguyễn Duy TùngNo ratings yet

- India Petroleum StatisticsDocument10 pagesIndia Petroleum StatisticsAjay GuptaNo ratings yet

- Lastname Firstname Initial FullnameDocument11 pagesLastname Firstname Initial Fullnamemuhammad harisNo ratings yet

- Daily Data For Ig Petro: Date Open High LOW Close ReturnDocument49 pagesDaily Data For Ig Petro: Date Open High LOW Close ReturnRinkesh K MistryNo ratings yet

- Tata Motors PresentationDocument121 pagesTata Motors PresentationSrikanth Reddy VemulaNo ratings yet

- Anup May 2024Document16 pagesAnup May 2024g_sivakumarNo ratings yet

- Chapter IDocument15 pagesChapter Imohsin.usafzai932No ratings yet

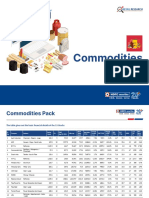

- HSL - Commodities Pack Report - 2021-202108182348310059173Document16 pagesHSL - Commodities Pack Report - 2021-202108182348310059173SHAIK AHMEDNo ratings yet

- Growth and Development of Telecom Sector in India - An: J.Jasmine Bhastina, Dr. (MRS) .J.MahamayiDocument3 pagesGrowth and Development of Telecom Sector in India - An: J.Jasmine Bhastina, Dr. (MRS) .J.Mahamayispmalla31No ratings yet

- Economic Instability in PakistanDocument35 pagesEconomic Instability in PakistanJunaid NaseemNo ratings yet

- 01 Growth and InvestmentDocument24 pages01 Growth and Investmentbugti1986No ratings yet

- Long Term SIP Picks Jan 23Document15 pagesLong Term SIP Picks Jan 23sbvaNo ratings yet

- 39023000Document5 pages39023000shawon azamNo ratings yet

- CTC CNAA 06162015 TeaserDocument3 pagesCTC CNAA 06162015 TeaserJean-Louis ThiemeleNo ratings yet

- Pdfanddoc 538625 PDFDocument76 pagesPdfanddoc 538625 PDFsoumyarm942No ratings yet

- Annex2 - Population ForecastDocument4 pagesAnnex2 - Population ForecastfeasprerNo ratings yet

- Global 500 2010Document15 pagesGlobal 500 2010Ravindra ReddyNo ratings yet

- Stock Market Trading Analysis by Mansukh Investment and Trading Solutions 3/4/2010Document5 pagesStock Market Trading Analysis by Mansukh Investment and Trading Solutions 3/4/2010MansukhNo ratings yet

- Last 15 Price Stock Bangladesh LTD 4Document1 pageLast 15 Price Stock Bangladesh LTD 4chinmoysaha17No ratings yet

- Last 15 Price Stock Bangladesh LTD 3Document1 pageLast 15 Price Stock Bangladesh LTD 3chinmoysaha17No ratings yet

- Weekly Foreign Holding & Block Trade - Update - 10 10 2014 PDFDocument4 pagesWeekly Foreign Holding & Block Trade - Update - 10 10 2014 PDFRandora LkNo ratings yet

- And Investment Holdings 32015Document10 pagesAnd Investment Holdings 32015Milan PetrikNo ratings yet

- Adb JapanDocument62 pagesAdb JapanHoang Giang NguyenNo ratings yet

- Dividend Yield StocksDocument2 pagesDividend Yield Stocksunu_uncNo ratings yet

- Beer IndustryDocument26 pagesBeer IndustryNathaniel GonzalesNo ratings yet

- Scheme DetailsDocument132 pagesScheme DetailsAman JainNo ratings yet

- Inositolic MarketDocument7 pagesInositolic Markethassan shahidNo ratings yet

- Group4 Project2-2Document19 pagesGroup4 Project2-2John Brian Asi AlmazanNo ratings yet

- India'Sindustrial SectorDocument51 pagesIndia'Sindustrial SectorParthrajNo ratings yet

- Iip June 2010Document9 pagesIip June 2010kdasNo ratings yet

- Mountain Man Brewing Co Bringing The Brand To Light-EXHIBITSDocument15 pagesMountain Man Brewing Co Bringing The Brand To Light-EXHIBITSVenkyNo ratings yet

- Business Plan For Establishment of Liquid Detergent PlantDocument22 pagesBusiness Plan For Establishment of Liquid Detergent PlantĐạt Diệp0% (1)

- SACM Exhibits TemplateDocument11 pagesSACM Exhibits TemplateJustin RuffingNo ratings yet

- Tales from the Development Frontier: How China and Other Countries Harness Light Manufacturing to Create Jobs and ProsperityFrom EverandTales from the Development Frontier: How China and Other Countries Harness Light Manufacturing to Create Jobs and ProsperityNo ratings yet

- Using Economic Indicators to Improve Investment AnalysisFrom EverandUsing Economic Indicators to Improve Investment AnalysisRating: 3.5 out of 5 stars3.5/5 (1)

- Clay Refractory Products World Summary: Market Sector Values & Financials by CountryFrom EverandClay Refractory Products World Summary: Market Sector Values & Financials by CountryNo ratings yet

- Full Development of Annex A Exercise-J CardenasDocument17 pagesFull Development of Annex A Exercise-J CardenasBruno SamosNo ratings yet

- Introduction To Computer NetworkingDocument28 pagesIntroduction To Computer NetworkingKendrewNo ratings yet

- Dr. N. Kumarappan IE (I) Council Candidate - Electrical DivisionDocument1 pageDr. N. Kumarappan IE (I) Council Candidate - Electrical Divisionshanmugasundaram32No ratings yet

- اسئلة بروتوكولات الفصل الاولDocument21 pagesاسئلة بروتوكولات الفصل الاولرسول ابراهيم عبد علي رويعيNo ratings yet

- Astro-Logics Pub PDFDocument7 pagesAstro-Logics Pub PDFlbedar100% (1)

- CAT Test Series 2015Document2 pagesCAT Test Series 2015Nikhil SiddharthNo ratings yet

- Black Ops CheatsDocument108 pagesBlack Ops CheatsVincent NewsonNo ratings yet

- Production ManagementDocument26 pagesProduction Managementkevin punzalan100% (5)

- Pe 3 Worksheet 5Document5 pagesPe 3 Worksheet 5Zaimin Yaz Del ValleNo ratings yet

- A Stingless Bee Hive Design For A Broader ClimateDocument4 pagesA Stingless Bee Hive Design For A Broader ClimateMarlon Manaya Garrigues100% (1)

- Aquagen: Recombination System For Stationary BatteriesDocument2 pagesAquagen: Recombination System For Stationary BatteriestaahaNo ratings yet

- Reflective Paper - SoundDocument3 pagesReflective Paper - Soundkashan HaiderNo ratings yet

- Sma Negeri 1 Kotabaru: I. Answer The Following Question!Document6 pagesSma Negeri 1 Kotabaru: I. Answer The Following Question!Dian MardhikaNo ratings yet

- PT English-6 Q2Document7 pagesPT English-6 Q2Elona Jane CapangpanganNo ratings yet

- Overhead Conductors Trefinasa 2016webDocument52 pagesOverhead Conductors Trefinasa 2016weboaktree2010No ratings yet

- 3storeyresidence Final ModelDocument1 page3storeyresidence Final ModelRheafel LimNo ratings yet

- Waste Heat Boiler Deskbook PDFDocument423 pagesWaste Heat Boiler Deskbook PDFwei zhou100% (1)

- Paint Data Sheet - National Synthetic Enamel Gloss IDocument3 pagesPaint Data Sheet - National Synthetic Enamel Gloss Iaakh0% (1)

- Coldplay - Higher Power (Uke Cifras)Document2 pagesColdplay - Higher Power (Uke Cifras)Jamille MesquitaNo ratings yet

- Organised By: Dr. Poonam S. TiwariDocument2 pagesOrganised By: Dr. Poonam S. Tiwarisayed kundumon100% (1)

- Illustrated Spare Part List FOR: Kirloskar Oil Engines LimitedDocument61 pagesIllustrated Spare Part List FOR: Kirloskar Oil Engines LimitedDarshan MakwanaNo ratings yet

- Sikkim ENVIS-REPORT ON WED 2021Document25 pagesSikkim ENVIS-REPORT ON WED 2021CHANDER KUMAR MNo ratings yet

- Guidotti Timothy E1980Document164 pagesGuidotti Timothy E1980Samuel GarciaNo ratings yet

- T5 B68 Craig Unger FDR - 5-21-04 Stull Email - Unger Saudi Flight Docs 616Document6 pagesT5 B68 Craig Unger FDR - 5-21-04 Stull Email - Unger Saudi Flight Docs 6169/11 Document ArchiveNo ratings yet

- Ex Parte Petition 734100 7Document19 pagesEx Parte Petition 734100 7WXMINo ratings yet

- History of UniverseDocument1 pageHistory of UniversemajdaNo ratings yet

- Envi Cases - La VinaDocument100 pagesEnvi Cases - La VinaChristine Gel MadrilejoNo ratings yet

- Indian Weekender Issue#96Document32 pagesIndian Weekender Issue#96Indian WeekenderNo ratings yet

- Intro To WW1 - Lesson 1Document24 pagesIntro To WW1 - Lesson 1Mrs_PPNo ratings yet

- Judi Online Di MedsosDocument11 pagesJudi Online Di MedsosHabibah HabibahNo ratings yet