Download as pdf or txt

You might also like

- LittleAcorns DWNLDDocument27 pagesLittleAcorns DWNLDGraeme Cunningham100% (3)

- Diamond DistributionDocument17 pagesDiamond DistributionMeena AggarwalNo ratings yet

- Chopra Wheel of LifeDocument2 pagesChopra Wheel of LifePooja Punjabi100% (1)

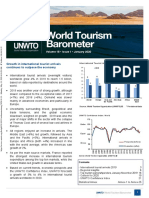

- Growth in International Tourist Arrivals Continues To Outpace The EconomyDocument48 pagesGrowth in International Tourist Arrivals Continues To Outpace The EconomyPetrosRochaNo ratings yet

- Chiquita Brands InternationalDocument6 pagesChiquita Brands InternationalKarla RodriguezNo ratings yet

- Sales of Good (Answer SC (1) (1ii) )Document4 pagesSales of Good (Answer SC (1) (1ii) )zizul86100% (4)

- Economic Outlook and Agenda BC#: Roberto Campos NetoDocument41 pagesEconomic Outlook and Agenda BC#: Roberto Campos Netoandre.torresNo ratings yet

- RCP-7.5 Drilling fluid agitator RCP-7.5 搅拌器: Parts List 9-D)Document6 pagesRCP-7.5 Drilling fluid agitator RCP-7.5 搅拌器: Parts List 9-D)waleedNo ratings yet

- Mohammed Taha Siddiqui CVDocument2 pagesMohammed Taha Siddiqui CV7ahasiddiquiNo ratings yet

- Ilovepdf MergedDocument6 pagesIlovepdf MergedJose HernandezNo ratings yet

- Introduction To The Report: Background of The StudyDocument89 pagesIntroduction To The Report: Background of The StudyMuhammad FarooqNo ratings yet

- KPI Student Satisfaction and Engagement SurveyDocument4 pagesKPI Student Satisfaction and Engagement SurveyMoataz DeiabNo ratings yet

- QT1-0-H-SAC-32-90003 - B - Central Control Building - HVAC Control Schematic DiagramDocument1 pageQT1-0-H-SAC-32-90003 - B - Central Control Building - HVAC Control Schematic DiagramVao Van Ngam VaoNo ratings yet

- 2007-01-18 Early Defaults Rise in Mortgage Securitization (Moody's Special Report)Document6 pages2007-01-18 Early Defaults Rise in Mortgage Securitization (Moody's Special Report)priak11No ratings yet

- 2007-01-18 Early Defaults Rise in Mortgage Securitization (Moody's Special Report)Document6 pages2007-01-18 Early Defaults Rise in Mortgage Securitization (Moody's Special Report)priak11No ratings yet

- MARKET DAILY For Wednesday, September 1, 2010Document1 pageMARKET DAILY For Wednesday, September 1, 2010JC CalaycayNo ratings yet

- QT1-0-H-SAC-32-90004 - B - Central Control Building - HVAC Control Schematic DiagramDocument1 pageQT1-0-H-SAC-32-90004 - B - Central Control Building - HVAC Control Schematic DiagramVao Van Ngam VaoNo ratings yet

- QT1-0-H-SAC-08-90003 - B - Central Control Building - HVAC Control Cable Schedule DrawingDocument1 pageQT1-0-H-SAC-08-90003 - B - Central Control Building - HVAC Control Cable Schedule DrawingVao Van Ngam VaoNo ratings yet

- QT1-0-H-SAC-32-90002 - B - Central Control Building - HVAC Control Schematic DiagramDocument1 pageQT1-0-H-SAC-32-90002 - B - Central Control Building - HVAC Control Schematic DiagramVao Van Ngam VaoNo ratings yet

- Intermediate Level 3b (Reharm)Document2 pagesIntermediate Level 3b (Reharm)obedientcrimeNo ratings yet

- Apple Revenue Streams by Quarter 2024Document3 pagesApple Revenue Streams by Quarter 2024kev123xuNo ratings yet

- Year 0 1 2 3 4 5 6 7 8 9 10 Net Present ValueDocument5 pagesYear 0 1 2 3 4 5 6 7 8 9 10 Net Present Valuemohitgaba19No ratings yet

- KRC BankingIndustry 20mar10Document3 pagesKRC BankingIndustry 20mar10karan36912No ratings yet

- QT1-0-H-SAC-08-90004 - B - Central Control Building - HVAC Control Cable Schedule DrawingDocument1 pageQT1-0-H-SAC-08-90004 - B - Central Control Building - HVAC Control Cable Schedule DrawingVao Van Ngam VaoNo ratings yet

- Pull, Push, Pipes: Sustainable Capital Flows For A New World OrderDocument23 pagesPull, Push, Pipes: Sustainable Capital Flows For A New World OrderHao WangNo ratings yet

- Main Structure - ST-01Document1 pageMain Structure - ST-01engr. abet hilarioNo ratings yet

- En Principal Islamic Asia Pacific Dynamic Equity Fund MYR FFSDocument2 pagesEn Principal Islamic Asia Pacific Dynamic Equity Fund MYR FFSsantiyrhNo ratings yet

- El Noi de La Mare (Sky Guitar #93) L3 (TAB) PDFDocument2 pagesEl Noi de La Mare (Sky Guitar #93) L3 (TAB) PDFAntonio CoronadoNo ratings yet

- Cost ReductionDocument1 pageCost Reductionashokkumar3363No ratings yet

- Jan Feb Mar Eapr Emei Juni Juli: Template by SeptyanidhikaDocument1 pageJan Feb Mar Eapr Emei Juni Juli: Template by SeptyanidhikadhikaNo ratings yet

- Practice Sums - Sessions - 3-4Document58 pagesPractice Sums - Sessions - 3-4Vibhuti AnandNo ratings yet

- STM Unit4 DecisionTablesDocument24 pagesSTM Unit4 DecisionTablesGuna SekaranNo ratings yet

- MicrosoftWord ReportDebtDocument4 pagesMicrosoftWord ReportDebtCommittee For a Responsible Federal BudgetNo ratings yet

- Getting Started As A Translator Learning Activity 5 Evidence 5Document8 pagesGetting Started As A Translator Learning Activity 5 Evidence 5Elizabeth SotomayorNo ratings yet

- SchematicDocument1 pageSchematicsimaabrahmanNo ratings yet

- Proprietary Information: Project NameDocument1 pageProprietary Information: Project NameManuel RevillaNo ratings yet

- Motilal Oswal Value Strategy FundDocument27 pagesMotilal Oswal Value Strategy FundFountainheadNo ratings yet

- L4 Lab 08 Timer Capture AssemblyDocument6 pagesL4 Lab 08 Timer Capture AssemblyIssam BalaNo ratings yet

- P2S Brief Review Dec22Document17 pagesP2S Brief Review Dec22diansyah wahyuNo ratings yet

- v1 Panbio COVID-19 IgG IgM QRG OUSDocument1 pagev1 Panbio COVID-19 IgG IgM QRG OUSAchmad NurNo ratings yet

- Subtraction - Middle AbilityDocument2 pagesSubtraction - Middle AbilitySomala KarthigeshNo ratings yet

- Addition - Same Denom2Document2 pagesAddition - Same Denom2aye quijanoNo ratings yet

- DB-1 1Document6 pagesDB-1 1Julio Alberto EspinozaNo ratings yet

- Clichês Harmônicos Alvo MenorDocument1 pageClichês Harmônicos Alvo MenorManoel Vitorino JuniorNo ratings yet

- Tresanje Tutorial WaltzDocument1 pageTresanje Tutorial Waltzjkranjc34No ratings yet

- SO DO KIT TN Nguyen Ly V3.0Document40 pagesSO DO KIT TN Nguyen Ly V3.0Bảo HoàngNo ratings yet

- Wtobarometereng 2020 18 1 1 PDFDocument48 pagesWtobarometereng 2020 18 1 1 PDFjohnNo ratings yet

- Nbacha QuadDocument2 pagesNbacha Quadapi-361246102No ratings yet

- Detail of Nozzle AbsorbentDocument1 pageDetail of Nozzle AbsorbentAlbet MulyonoNo ratings yet

- Something's Gotten Hold of My HeartDocument2 pagesSomething's Gotten Hold of My HeartZaina HmidaNo ratings yet

- Bartolome, Rohan Siegfried B. Ac 007 Plate No. (Municipal Government Center)Document14 pagesBartolome, Rohan Siegfried B. Ac 007 Plate No. (Municipal Government Center)Bartolome, Rohan Siegfried B.No ratings yet

- QT1-0-H-SAC-32-90001 - B - Central Control Building - HVAC Control Schematic DiagramDocument1 pageQT1-0-H-SAC-32-90001 - B - Central Control Building - HVAC Control Schematic DiagramVao Van Ngam VaoNo ratings yet

- Kris Lane, The Color of Paradise (Intro) PDFDocument27 pagesKris Lane, The Color of Paradise (Intro) PDFBllNo ratings yet

- Digital Logic Design Lab: Experiment #5 NAND / NOR Logic Circuit ImplementationDocument9 pagesDigital Logic Design Lab: Experiment #5 NAND / NOR Logic Circuit ImplementationMohamad MonerNo ratings yet

- CW & Aux - Boilers Water Analysis Nov 2022Document6 pagesCW & Aux - Boilers Water Analysis Nov 2022bulatovdaniil73No ratings yet

- Key Imperatives of Life Insurance Industry in The Current Market EnvironmentDocument11 pagesKey Imperatives of Life Insurance Industry in The Current Market EnvironmentvsparmarNo ratings yet

- IT Initiatives PortfolioDocument9 pagesIT Initiatives Portfoliomahmoud.nouhNo ratings yet

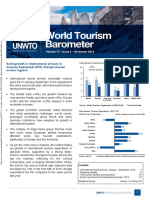

- Solid Growth in International Arrivals in January-September 2019, Though Uneven Across RegionsDocument44 pagesSolid Growth in International Arrivals in January-September 2019, Though Uneven Across RegionsJennifer LaraNo ratings yet

- BAV Assignment WalmartDocument3 pagesBAV Assignment WalmartVidushi ThapliyalNo ratings yet

- MDY LAN Ops DIA Weekly Report MN Biz 19 Jul 25 JulDocument6 pagesMDY LAN Ops DIA Weekly Report MN Biz 19 Jul 25 Julei monphyoNo ratings yet

- CN385 - 2 SSP Smart Hopper User Interface Cable AssemblyDocument2 pagesCN385 - 2 SSP Smart Hopper User Interface Cable AssemblyAymen CheffiNo ratings yet

- PBC45 25CDocument1 pagePBC45 25CZeeshan Byfuglien GrudzielanekNo ratings yet

- Fill Your Glass With Gold-When It's Half-Full or Even Completely ShatteredFrom EverandFill Your Glass With Gold-When It's Half-Full or Even Completely ShatteredNo ratings yet

- Weekly Xxviii - July 11 To 15, 2011Document2 pagesWeekly Xxviii - July 11 To 15, 2011JC CalaycayNo ratings yet

- Weekly Xxvix - July 18 To 22, 2011Document2 pagesWeekly Xxvix - July 18 To 22, 2011JC CalaycayNo ratings yet

- Market Balance - Daily For August 11, 2011Document3 pagesMarket Balance - Daily For August 11, 2011JC CalaycayNo ratings yet

- Weekly Xxxi - August 1 To 5, 2011Document2 pagesWeekly Xxxi - August 1 To 5, 2011JC CalaycayNo ratings yet

- Market Balance - Daily For August 10, 2011Document2 pagesMarket Balance - Daily For August 10, 2011JC CalaycayNo ratings yet

- Market Notes July 22 FridayDocument1 pageMarket Notes July 22 FridayJC CalaycayNo ratings yet

- DAILY - July 22-25, 2011Document1 pageDAILY - July 22-25, 2011JC CalaycayNo ratings yet

- DAILY - June 21-22, 2011Document1 pageDAILY - June 21-22, 2011JC CalaycayNo ratings yet

- Market Notes Mining atDocument2 pagesMarket Notes Mining atJC CalaycayNo ratings yet

- DAILY - June 22-23, 2011Document1 pageDAILY - June 22-23, 2011JC CalaycayNo ratings yet

- Market Notes June 22 WednesdayDocument2 pagesMarket Notes June 22 WednesdayJC CalaycayNo ratings yet

- Market Notes MwideDocument2 pagesMarket Notes MwideJC CalaycayNo ratings yet

- DAILY - June 16-17, 2011Document1 pageDAILY - June 16-17, 2011JC CalaycayNo ratings yet

- Daily - June 7-8, 2011Document3 pagesDaily - June 7-8, 2011JC CalaycayNo ratings yet

- Accord Capital Equities Corporation: Outlook For Week XXV - June 21 To 24 - TD 119-122Document3 pagesAccord Capital Equities Corporation: Outlook For Week XXV - June 21 To 24 - TD 119-122JC CalaycayNo ratings yet

- DAILY - June 14-15, 2011Document2 pagesDAILY - June 14-15, 2011JC CalaycayNo ratings yet

- Market Notes June 17 FridayDocument1 pageMarket Notes June 17 FridayJC CalaycayNo ratings yet

- Market Notes - Food SroDocument2 pagesMarket Notes - Food SroJC CalaycayNo ratings yet

- Accord Capital Equities Corporation: Outlook For Week XXIV - June 13 To 17 - TD 114-118Document2 pagesAccord Capital Equities Corporation: Outlook For Week XXIV - June 13 To 17 - TD 114-118JC CalaycayNo ratings yet

- Market Notes - June 6, 2011 - MondayDocument2 pagesMarket Notes - June 6, 2011 - MondayJC CalaycayNo ratings yet

- Weekly Report - June 6-10, 2011Document2 pagesWeekly Report - June 6-10, 2011JC CalaycayNo ratings yet

- Weekly Report - Xxi - May 23 To 27, 2011Document3 pagesWeekly Report - Xxi - May 23 To 27, 2011JC CalaycayNo ratings yet

- DAILY - May 17-18, 2011Document2 pagesDAILY - May 17-18, 2011JC CalaycayNo ratings yet

- DAILY - May 11-12, 2011Document1 pageDAILY - May 11-12, 2011JC CalaycayNo ratings yet

- Market Notes May 16 MondayDocument1 pageMarket Notes May 16 MondayJC CalaycayNo ratings yet

- Market Notes May 17 TuesdayDocument2 pagesMarket Notes May 17 TuesdayJC CalaycayNo ratings yet

- Market Notes May 13 FridayDocument3 pagesMarket Notes May 13 FridayJC CalaycayNo ratings yet

- DAILY - May 12-13, 2011Document2 pagesDAILY - May 12-13, 2011JC CalaycayNo ratings yet

- DAILY - May 16-17, 2011Document1 pageDAILY - May 16-17, 2011JC CalaycayNo ratings yet

- Daily - May 13, 2011 - End of WeekDocument2 pagesDaily - May 13, 2011 - End of WeekJC CalaycayNo ratings yet

- Chap 005Document40 pagesChap 005Erica JurkowskiNo ratings yet

- Managerial Economics - Q1Document6 pagesManagerial Economics - Q1wivadaNo ratings yet

- 37 Wyckoff TimeDocument4 pages37 Wyckoff TimeACasey101100% (1)

- Project Controls Manual 2013-11-01 Issued Rev 3Document206 pagesProject Controls Manual 2013-11-01 Issued Rev 3ankitch123No ratings yet

- Walt Disney Strategy SSSDocument31 pagesWalt Disney Strategy SSSRao P Satyanarayana100% (2)

- Business and Management Standard Level Paper 2: 2214-5014 7 Pages © International Baccalaureate Organization 2014Document7 pagesBusiness and Management Standard Level Paper 2: 2214-5014 7 Pages © International Baccalaureate Organization 2014Leyla HmiNo ratings yet

- ISINGA PRIVATE ESTATE Investment ProposalDocument14 pagesISINGA PRIVATE ESTATE Investment ProposalEffortNo ratings yet

- 201 Final Fall 2011 V1aDocument11 pages201 Final Fall 2011 V1aJonathan RuizNo ratings yet

- Macroeconomic Determinants of Stock Market Development: Evidence From Borsa IstanbulDocument21 pagesMacroeconomic Determinants of Stock Market Development: Evidence From Borsa IstanbulMaria KulawikNo ratings yet

- 2006.zingwiro Protase Tichafa Sanangurai 2006Document80 pages2006.zingwiro Protase Tichafa Sanangurai 2006sixto tovarNo ratings yet

- Triptico NIC 16Document3 pagesTriptico NIC 16Brayan HM0% (1)

- QuestionPaperDec 2010Document50 pagesQuestionPaperDec 2010Md.Reza HussainNo ratings yet

- Amjad Hammad 1165230: Porter Six Forces For Aluminum Industry in PalestineDocument6 pagesAmjad Hammad 1165230: Porter Six Forces For Aluminum Industry in PalestineEng Eman HannounNo ratings yet

- Customer Ordering Guide and Price List: Transit Chassis CabDocument18 pagesCustomer Ordering Guide and Price List: Transit Chassis CabZoraydaNo ratings yet

- Power of Eminent Domain - 7. Republic v. Vda. de CastellviDocument1 pagePower of Eminent Domain - 7. Republic v. Vda. de CastellviPaul Joshua Torda Suba100% (1)

- Cost ManagementDocument3 pagesCost ManagementAccenture AustraNo ratings yet

- Asda Stores TerminologyDocument4 pagesAsda Stores TerminologyShesmene ScheissekopfNo ratings yet

- Formation Lean ManufacturingDocument167 pagesFormation Lean ManufacturingYoussefNo ratings yet

- Unit Plan On Consumer Arithmetic For Form 4Document16 pagesUnit Plan On Consumer Arithmetic For Form 4api-537308426No ratings yet

- Case Presentation PART 2+PART 3Document3 pagesCase Presentation PART 2+PART 3jackywen1024No ratings yet

- Fixed Income Assignment 1Document3 pagesFixed Income Assignment 1Rattan Preet SinghNo ratings yet

- Financial Modeling With Excel and VBADocument113 pagesFinancial Modeling With Excel and VBAakash_sugumaran100% (11)

- Arlington Value Combined FilesDocument48 pagesArlington Value Combined FilesBruno Pinto RibeiroNo ratings yet

- AB Back Tester BasicsDocument27 pagesAB Back Tester BasicstungkanguruNo ratings yet

- Intro To Health EconomicsDocument34 pagesIntro To Health EconomicsRasha ElzenyNo ratings yet

- Tutorial 4 - SolutionDocument16 pagesTutorial 4 - SolutionNg Chun SenfNo ratings yet