Status of Implementation of Prior Years' Unimplemented Audit Recommendations

Status of Implementation of Prior Years' Unimplemented Audit Recommendations

You might also like

- The New Four Ps of DTC MarketingDocument22 pagesThe New Four Ps of DTC MarketingTimNo ratings yet

- Case Analysis LenhaageDocument3 pagesCase Analysis Lenhaage11108109No ratings yet

- OCR GCSE 9-1 Business: My Revision GuideDocument113 pagesOCR GCSE 9-1 Business: My Revision GuideAnya Johal100% (1)

- 01 - Technical Notes For SGLG LGPMS Field TestDocument58 pages01 - Technical Notes For SGLG LGPMS Field Testnorman100% (1)

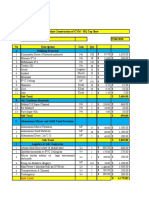

- Estimation Coffeteria & Gym - Fooqa SareDocument9 pagesEstimation Coffeteria & Gym - Fooqa SareEng Abdi Shakur Yusuf100% (1)

- Part Iii-Status of Implementation of Prior Years' Audit RecommendationsDocument7 pagesPart Iii-Status of Implementation of Prior Years' Audit RecommendationsAlicia NhsNo ratings yet

- Malimono SDN ES2013Document10 pagesMalimono SDN ES2013J JaNo ratings yet

- Status of Implementation of Prior Years' Audit RecommendationsDocument20 pagesStatus of Implementation of Prior Years' Audit Recommendationssandra bolokNo ratings yet

- Improper Handling of Collections: Observations and RecommendationsDocument22 pagesImproper Handling of Collections: Observations and Recommendationsdemos reaNo ratings yet

- Alegria Executive Summary 2019Document6 pagesAlegria Executive Summary 2019Ronel CadelinoNo ratings yet

- Maramag Water District Bukidnon Executive Summary 2020Document6 pagesMaramag Water District Bukidnon Executive Summary 2020cpa126235No ratings yet

- San Luis - Matrix of Audit Observations For CY 2017Document7 pagesSan Luis - Matrix of Audit Observations For CY 2017Kei PaceñoNo ratings yet

- SurigaoDelNorte ES2010Document5 pagesSurigaoDelNorte ES2010J JaNo ratings yet

- Status of Implementation of Prior Year'S Audit RecommendationsDocument15 pagesStatus of Implementation of Prior Year'S Audit RecommendationsGloria AlamilNo ratings yet

- Status of Implementation of Prior Years' Unimplemented Audit RecommendationsDocument35 pagesStatus of Implementation of Prior Years' Unimplemented Audit Recommendationssandra bolokNo ratings yet

- Guimba Executive Summary 2014Document5 pagesGuimba Executive Summary 2014Winter KimNo ratings yet

- Executive Summary: Highlights of Financial OperationsDocument12 pagesExecutive Summary: Highlights of Financial OperationsJaniceNo ratings yet

- Kabasalan ZS ES2013Document9 pagesKabasalan ZS ES2013ArdenNo ratings yet

- Thirteen (13) Twelve (12) Eleven (11) Ten (10) : Status of Implementation of Prior Years' Audit RecommendationsDocument5 pagesThirteen (13) Twelve (12) Eleven (11) Ten (10) : Status of Implementation of Prior Years' Audit RecommendationsVal Escobar MagumunNo ratings yet

- 2013 inDocument3 pages2013 inRahul KumarNo ratings yet

- Pakil Laguna ES2014Document8 pagesPakil Laguna ES2014Jeffrey RiveraNo ratings yet

- 8 COA Actions Taken FinalDocument4 pages8 COA Actions Taken FinalDOLE West Leyte Field OfficeNo ratings yet

- Part Ii - Audit Findings and RecommendationsDocument13 pagesPart Ii - Audit Findings and Recommendationssandra bolokNo ratings yet

- Executive SummaryDocument9 pagesExecutive SummaryjonquintanoNo ratings yet

- SAOR 2015 Additional AOM DO ZDNDocument9 pagesSAOR 2015 Additional AOM DO ZDNrussel1435No ratings yet

- Status of Implementation of Prior Year's Recommendations CY 2016Document8 pagesStatus of Implementation of Prior Year's Recommendations CY 2016Mary Jane Katipunan CalumbaNo ratings yet

- Part 3 - CanantongDocument5 pagesPart 3 - CanantongJonson PalmaresNo ratings yet

- Esperanza Executive Summary 2011Document5 pagesEsperanza Executive Summary 2011Rowena MahusayNo ratings yet

- Part Iii - Status of Implementation of Prior Years' Audit RecommendationsDocument37 pagesPart Iii - Status of Implementation of Prior Years' Audit RecommendationsAlicia NhsNo ratings yet

- ATL-Reviewed BrgyAOM2022-01 KC Saravia CashDeficitDocument4 pagesATL-Reviewed BrgyAOM2022-01 KC Saravia CashDeficitkipar_16No ratings yet

- 12-Casiguran Aurora 2010 Part3-Status of PY's RecommendationsDocument7 pages12-Casiguran Aurora 2010 Part3-Status of PY's RecommendationsKasiguruhan AuroraNo ratings yet

- Luna Executive Summary 2012Document4 pagesLuna Executive Summary 2012The ApprenticeNo ratings yet

- AUDIT REPORT-GB RevenuesDocument27 pagesAUDIT REPORT-GB RevenuesAbid KhawajaNo ratings yet

- 10-TaclobanCity2018 Part3-Status of PY's RecommDocument13 pages10-TaclobanCity2018 Part3-Status of PY's Recommrobert lachicaNo ratings yet

- Commission On Audit Regional Office No. IV-A NGS Cluster 8-A, B, G, Audit Team R4A-42Document5 pagesCommission On Audit Regional Office No. IV-A NGS Cluster 8-A, B, G, Audit Team R4A-42oabeljeanmoniqueNo ratings yet

- Commission On Audit Office of The Regional Director Regional Office No. IDocument6 pagesCommission On Audit Office of The Regional Director Regional Office No. IEG ReyesNo ratings yet

- San Miguel Executive Summary 2012Document4 pagesSan Miguel Executive Summary 2012imnikki.gonzalesNo ratings yet

- Taytay Water District Executive Summary 2018Document6 pagesTaytay Water District Executive Summary 2018Allan SobrepeñaNo ratings yet

- COA & COMELEC R4A - APMT 2017 ML SAOR With DetailsDocument8 pagesCOA & COMELEC R4A - APMT 2017 ML SAOR With DetailsVicky Danila AlbanoNo ratings yet

- Malabang Executive Summary 2018Document5 pagesMalabang Executive Summary 2018Evan LoirtNo ratings yet

- San Miguel Executive Summary 2013Document7 pagesSan Miguel Executive Summary 2013SharaJaenDinorogBagundolNo ratings yet

- Ne BarabggayDocument100 pagesNe BarabggayTheresa MacasiebNo ratings yet

- Dasmariñas2020 Audit ReportDocument228 pagesDasmariñas2020 Audit ReportJuswa DanyelNo ratings yet

- 10-Loboc2012 Status of PY's RecommendationsDocument19 pages10-Loboc2012 Status of PY's RecommendationsMiss_AccountantNo ratings yet

- 08-SarProv2021 Part IIDocument28 pages08-SarProv2021 Part IIReyna YlenaNo ratings yet

- Lugait Executive Summary 2018Document4 pagesLugait Executive Summary 2018OZ La NB AnamiNo ratings yet

- Bureau of Fire Protection Executive Summary 2011Document6 pagesBureau of Fire Protection Executive Summary 2011Vin CentNo ratings yet

- 11-CebuCity2017 Part3-Status of PYs RecommDocument64 pages11-CebuCity2017 Part3-Status of PYs RecommKen AbabaNo ratings yet

- 09-EARIST2021 Part2-Observations and RecommDocument44 pages09-EARIST2021 Part2-Observations and RecommMiss_AccountantNo ratings yet

- 10-Bacolor2017 Part2-Observations and RecommDocument47 pages10-Bacolor2017 Part2-Observations and RecommKatherine PacenoNo ratings yet

- Common Ltoe Findings & RecomDocument4 pagesCommon Ltoe Findings & RecomYanee T-ChanNo ratings yet

- Cagwait Executive Summary 2022Document5 pagesCagwait Executive Summary 2022renelynarbisNo ratings yet

- Mga Tao Sa KapehanDocument4 pagesMga Tao Sa KapehanJoshua Lavega AbrinaNo ratings yet

- Basud Executive Summary 2011Document6 pagesBasud Executive Summary 2011Maria CharessaNo ratings yet

- 08 BLGUMAGSAYSAYHILL 2022 AAR Part2 Findings and RecommendationsDocument22 pages08 BLGUMAGSAYSAYHILL 2022 AAR Part2 Findings and RecommendationsGil DavinNo ratings yet

- 10-WVSU2021 Part2-Observations and RecommDocument39 pages10-WVSU2021 Part2-Observations and RecommMiss_AccountantNo ratings yet

- 2024 SGLG Technical Notes - For Orientation Purposes OnlyDocument124 pages2024 SGLG Technical Notes - For Orientation Purposes OnlyDILG BAYAMBANG100% (1)

- Masantol Executive Summary 2019Document5 pagesMasantol Executive Summary 2019Juan Miguel NavarroNo ratings yet

- Ne BarabggayDocument100 pagesNe BarabggayTheresa MacasiebNo ratings yet

- Moalboal Executive Summary 2014Document6 pagesMoalboal Executive Summary 2014Horace CimafrancaNo ratings yet

- 11 - NYC 2020 COA Report Part3 - Status of PY's RecommDocument13 pages11 - NYC 2020 COA Report Part3 - Status of PY's RecommVERA FilesNo ratings yet

- Aparri Water District Cagayan Executive Summary 2020Document5 pagesAparri Water District Cagayan Executive Summary 2020Franciz NasisNo ratings yet

- AAPSIDocument30 pagesAAPSICG EusebioNo ratings yet

- Ched Es2015Document11 pagesChed Es2015demos reaNo ratings yet

- 01-Abucay2014 Transmittal LetterDocument8 pages01-Abucay2014 Transmittal Letterdemos reaNo ratings yet

- Independent Auditor'S Report The Honorable Mayor: Management's Responsibility For The Consolidated Financial StatementsDocument2 pagesIndependent Auditor'S Report The Honorable Mayor: Management's Responsibility For The Consolidated Financial Statementsdemos reaNo ratings yet

- Notes To Financial StatementsDocument11 pagesNotes To Financial Statementsdemos reaNo ratings yet

- Part I - Audited Financial StatementsDocument4 pagesPart I - Audited Financial Statementsdemos reaNo ratings yet

- Improper Handling of Collections: Observations and RecommendationsDocument22 pagesImproper Handling of Collections: Observations and Recommendationsdemos reaNo ratings yet

- 02-Abucay2014 CoverDocument1 page02-Abucay2014 Coverdemos reaNo ratings yet

- Statement of Management'S Responsibility For Financial StatementsDocument1 pageStatement of Management'S Responsibility For Financial Statementsdemos reaNo ratings yet

- 08-Abucay2014 Part1-Financial StatementsDocument5 pages08-Abucay2014 Part1-Financial Statementsdemos reaNo ratings yet

- AssignDocument18 pagesAssignRalph Adrian MielNo ratings yet

- Finance Submission 02Document58 pagesFinance Submission 02prathamgharat019No ratings yet

- About Rtgs & NeftDocument5 pagesAbout Rtgs & NeftAbdulhussain JariwalaNo ratings yet

- Agriclinics and Agribusiness CentersDocument47 pagesAgriclinics and Agribusiness CentersMadhavilathaNo ratings yet

- Cooperative MarketingDocument2 pagesCooperative MarketinggnmadaviNo ratings yet

- Capacity Planning For Products and ServicesDocument27 pagesCapacity Planning For Products and ServicesJose Mario PagsanjanNo ratings yet

- The Role of Microbusinesses in The Economy: by Brian Headd, EconomistDocument1 pageThe Role of Microbusinesses in The Economy: by Brian Headd, Economist--No ratings yet

- Sanjay Kanojiya-ElectricalDocument1 pageSanjay Kanojiya-ElectricalAMANNo ratings yet

- Capital & Class 1993 Naples 119 37Document20 pagesCapital & Class 1993 Naples 119 37D. Silva EscobarNo ratings yet

- Floor Plan Lending PrimerDocument73 pagesFloor Plan Lending PrimerCari Mangalindan MacaalayNo ratings yet

- Upto 1000 Solved MCQs of MKT501 Marketing Management WWW - VustudentsDocument228 pagesUpto 1000 Solved MCQs of MKT501 Marketing Management WWW - VustudentsLyla Abbas Khan100% (24)

- Chapter - 12 - Inventory Accounting For Consumable SuppliesDocument10 pagesChapter - 12 - Inventory Accounting For Consumable SuppliesJa Mi LahNo ratings yet

- Classification of Reserves and ResourcesDocument27 pagesClassification of Reserves and Resourcesnina chentsovaNo ratings yet

- General Banking Activities of Jamuna BankDocument52 pagesGeneral Banking Activities of Jamuna BankFatin Arefin0% (1)

- Pilipinas Shell Petroleum Corporation: SHLPHDocument17 pagesPilipinas Shell Petroleum Corporation: SHLPHIsis Normagne PascualNo ratings yet

- Cfo AgendaDocument7 pagesCfo AgendaMOORTHY.KENo ratings yet

- Part 1 CapstoneDocument14 pagesPart 1 Capstonenica abellanaNo ratings yet

- Xcel CFA® Series: Financial Reporting and Analysis Reading 25Document6 pagesXcel CFA® Series: Financial Reporting and Analysis Reading 25Naseer AhmedNo ratings yet

- Ti TechDocument4 pagesTi Techmadddy_hyd100% (3)

- By Hamed Armesh 1082200034Document22 pagesBy Hamed Armesh 1082200034Roozbeh HojabriNo ratings yet

- Consumer Behavior Buying Having and Being 11th Edition Solomon Test Bank 1Document25 pagesConsumer Behavior Buying Having and Being 11th Edition Solomon Test Bank 1elizabeth100% (44)

- The Is Greater Than The Sum of Its Parts.: WholeDocument18 pagesThe Is Greater Than The Sum of Its Parts.: WholeAkshata MalhotraNo ratings yet

- A Study On The Challenges HR Managers Face TodayDocument10 pagesA Study On The Challenges HR Managers Face TodayJAY MARK TANONo ratings yet

- Theory Madison Proposal LowresDocument68 pagesTheory Madison Proposal Lowresinfo.giantholdingsNo ratings yet

- Ismt LTD (2019-2020)Document150 pagesIsmt LTD (2019-2020)Nimit BhimjiyaniNo ratings yet

- Financial Forecasting For Strategic GrowthDocument3 pagesFinancial Forecasting For Strategic GrowthVergel MartinezNo ratings yet

Download as docx, pdf, or txt

You might also like

- The New Four Ps of DTC MarketingDocument22 pagesThe New Four Ps of DTC MarketingTimNo ratings yet

- Case Analysis LenhaageDocument3 pagesCase Analysis Lenhaage11108109No ratings yet

- OCR GCSE 9-1 Business: My Revision GuideDocument113 pagesOCR GCSE 9-1 Business: My Revision GuideAnya Johal100% (1)

- 01 - Technical Notes For SGLG LGPMS Field TestDocument58 pages01 - Technical Notes For SGLG LGPMS Field Testnorman100% (1)

- Estimation Coffeteria & Gym - Fooqa SareDocument9 pagesEstimation Coffeteria & Gym - Fooqa SareEng Abdi Shakur Yusuf100% (1)

- Part Iii-Status of Implementation of Prior Years' Audit RecommendationsDocument7 pagesPart Iii-Status of Implementation of Prior Years' Audit RecommendationsAlicia NhsNo ratings yet

- Malimono SDN ES2013Document10 pagesMalimono SDN ES2013J JaNo ratings yet

- Status of Implementation of Prior Years' Audit RecommendationsDocument20 pagesStatus of Implementation of Prior Years' Audit Recommendationssandra bolokNo ratings yet

- Improper Handling of Collections: Observations and RecommendationsDocument22 pagesImproper Handling of Collections: Observations and Recommendationsdemos reaNo ratings yet

- Alegria Executive Summary 2019Document6 pagesAlegria Executive Summary 2019Ronel CadelinoNo ratings yet

- Maramag Water District Bukidnon Executive Summary 2020Document6 pagesMaramag Water District Bukidnon Executive Summary 2020cpa126235No ratings yet

- San Luis - Matrix of Audit Observations For CY 2017Document7 pagesSan Luis - Matrix of Audit Observations For CY 2017Kei PaceñoNo ratings yet

- SurigaoDelNorte ES2010Document5 pagesSurigaoDelNorte ES2010J JaNo ratings yet

- Status of Implementation of Prior Year'S Audit RecommendationsDocument15 pagesStatus of Implementation of Prior Year'S Audit RecommendationsGloria AlamilNo ratings yet

- Status of Implementation of Prior Years' Unimplemented Audit RecommendationsDocument35 pagesStatus of Implementation of Prior Years' Unimplemented Audit Recommendationssandra bolokNo ratings yet

- Guimba Executive Summary 2014Document5 pagesGuimba Executive Summary 2014Winter KimNo ratings yet

- Executive Summary: Highlights of Financial OperationsDocument12 pagesExecutive Summary: Highlights of Financial OperationsJaniceNo ratings yet

- Kabasalan ZS ES2013Document9 pagesKabasalan ZS ES2013ArdenNo ratings yet

- Thirteen (13) Twelve (12) Eleven (11) Ten (10) : Status of Implementation of Prior Years' Audit RecommendationsDocument5 pagesThirteen (13) Twelve (12) Eleven (11) Ten (10) : Status of Implementation of Prior Years' Audit RecommendationsVal Escobar MagumunNo ratings yet

- 2013 inDocument3 pages2013 inRahul KumarNo ratings yet

- Pakil Laguna ES2014Document8 pagesPakil Laguna ES2014Jeffrey RiveraNo ratings yet

- 8 COA Actions Taken FinalDocument4 pages8 COA Actions Taken FinalDOLE West Leyte Field OfficeNo ratings yet

- Part Ii - Audit Findings and RecommendationsDocument13 pagesPart Ii - Audit Findings and Recommendationssandra bolokNo ratings yet

- Executive SummaryDocument9 pagesExecutive SummaryjonquintanoNo ratings yet

- SAOR 2015 Additional AOM DO ZDNDocument9 pagesSAOR 2015 Additional AOM DO ZDNrussel1435No ratings yet

- Status of Implementation of Prior Year's Recommendations CY 2016Document8 pagesStatus of Implementation of Prior Year's Recommendations CY 2016Mary Jane Katipunan CalumbaNo ratings yet

- Part 3 - CanantongDocument5 pagesPart 3 - CanantongJonson PalmaresNo ratings yet

- Esperanza Executive Summary 2011Document5 pagesEsperanza Executive Summary 2011Rowena MahusayNo ratings yet

- Part Iii - Status of Implementation of Prior Years' Audit RecommendationsDocument37 pagesPart Iii - Status of Implementation of Prior Years' Audit RecommendationsAlicia NhsNo ratings yet

- ATL-Reviewed BrgyAOM2022-01 KC Saravia CashDeficitDocument4 pagesATL-Reviewed BrgyAOM2022-01 KC Saravia CashDeficitkipar_16No ratings yet

- 12-Casiguran Aurora 2010 Part3-Status of PY's RecommendationsDocument7 pages12-Casiguran Aurora 2010 Part3-Status of PY's RecommendationsKasiguruhan AuroraNo ratings yet

- Luna Executive Summary 2012Document4 pagesLuna Executive Summary 2012The ApprenticeNo ratings yet

- AUDIT REPORT-GB RevenuesDocument27 pagesAUDIT REPORT-GB RevenuesAbid KhawajaNo ratings yet

- 10-TaclobanCity2018 Part3-Status of PY's RecommDocument13 pages10-TaclobanCity2018 Part3-Status of PY's Recommrobert lachicaNo ratings yet

- Commission On Audit Regional Office No. IV-A NGS Cluster 8-A, B, G, Audit Team R4A-42Document5 pagesCommission On Audit Regional Office No. IV-A NGS Cluster 8-A, B, G, Audit Team R4A-42oabeljeanmoniqueNo ratings yet

- Commission On Audit Office of The Regional Director Regional Office No. IDocument6 pagesCommission On Audit Office of The Regional Director Regional Office No. IEG ReyesNo ratings yet

- San Miguel Executive Summary 2012Document4 pagesSan Miguel Executive Summary 2012imnikki.gonzalesNo ratings yet

- Taytay Water District Executive Summary 2018Document6 pagesTaytay Water District Executive Summary 2018Allan SobrepeñaNo ratings yet

- COA & COMELEC R4A - APMT 2017 ML SAOR With DetailsDocument8 pagesCOA & COMELEC R4A - APMT 2017 ML SAOR With DetailsVicky Danila AlbanoNo ratings yet

- Malabang Executive Summary 2018Document5 pagesMalabang Executive Summary 2018Evan LoirtNo ratings yet

- San Miguel Executive Summary 2013Document7 pagesSan Miguel Executive Summary 2013SharaJaenDinorogBagundolNo ratings yet

- Ne BarabggayDocument100 pagesNe BarabggayTheresa MacasiebNo ratings yet

- Dasmariñas2020 Audit ReportDocument228 pagesDasmariñas2020 Audit ReportJuswa DanyelNo ratings yet

- 10-Loboc2012 Status of PY's RecommendationsDocument19 pages10-Loboc2012 Status of PY's RecommendationsMiss_AccountantNo ratings yet

- 08-SarProv2021 Part IIDocument28 pages08-SarProv2021 Part IIReyna YlenaNo ratings yet

- Lugait Executive Summary 2018Document4 pagesLugait Executive Summary 2018OZ La NB AnamiNo ratings yet

- Bureau of Fire Protection Executive Summary 2011Document6 pagesBureau of Fire Protection Executive Summary 2011Vin CentNo ratings yet

- 11-CebuCity2017 Part3-Status of PYs RecommDocument64 pages11-CebuCity2017 Part3-Status of PYs RecommKen AbabaNo ratings yet

- 09-EARIST2021 Part2-Observations and RecommDocument44 pages09-EARIST2021 Part2-Observations and RecommMiss_AccountantNo ratings yet

- 10-Bacolor2017 Part2-Observations and RecommDocument47 pages10-Bacolor2017 Part2-Observations and RecommKatherine PacenoNo ratings yet

- Common Ltoe Findings & RecomDocument4 pagesCommon Ltoe Findings & RecomYanee T-ChanNo ratings yet

- Cagwait Executive Summary 2022Document5 pagesCagwait Executive Summary 2022renelynarbisNo ratings yet

- Mga Tao Sa KapehanDocument4 pagesMga Tao Sa KapehanJoshua Lavega AbrinaNo ratings yet

- Basud Executive Summary 2011Document6 pagesBasud Executive Summary 2011Maria CharessaNo ratings yet

- 08 BLGUMAGSAYSAYHILL 2022 AAR Part2 Findings and RecommendationsDocument22 pages08 BLGUMAGSAYSAYHILL 2022 AAR Part2 Findings and RecommendationsGil DavinNo ratings yet

- 10-WVSU2021 Part2-Observations and RecommDocument39 pages10-WVSU2021 Part2-Observations and RecommMiss_AccountantNo ratings yet

- 2024 SGLG Technical Notes - For Orientation Purposes OnlyDocument124 pages2024 SGLG Technical Notes - For Orientation Purposes OnlyDILG BAYAMBANG100% (1)

- Masantol Executive Summary 2019Document5 pagesMasantol Executive Summary 2019Juan Miguel NavarroNo ratings yet

- Ne BarabggayDocument100 pagesNe BarabggayTheresa MacasiebNo ratings yet

- Moalboal Executive Summary 2014Document6 pagesMoalboal Executive Summary 2014Horace CimafrancaNo ratings yet

- 11 - NYC 2020 COA Report Part3 - Status of PY's RecommDocument13 pages11 - NYC 2020 COA Report Part3 - Status of PY's RecommVERA FilesNo ratings yet

- Aparri Water District Cagayan Executive Summary 2020Document5 pagesAparri Water District Cagayan Executive Summary 2020Franciz NasisNo ratings yet

- AAPSIDocument30 pagesAAPSICG EusebioNo ratings yet

- Ched Es2015Document11 pagesChed Es2015demos reaNo ratings yet

- 01-Abucay2014 Transmittal LetterDocument8 pages01-Abucay2014 Transmittal Letterdemos reaNo ratings yet

- Independent Auditor'S Report The Honorable Mayor: Management's Responsibility For The Consolidated Financial StatementsDocument2 pagesIndependent Auditor'S Report The Honorable Mayor: Management's Responsibility For The Consolidated Financial Statementsdemos reaNo ratings yet

- Notes To Financial StatementsDocument11 pagesNotes To Financial Statementsdemos reaNo ratings yet

- Part I - Audited Financial StatementsDocument4 pagesPart I - Audited Financial Statementsdemos reaNo ratings yet

- Improper Handling of Collections: Observations and RecommendationsDocument22 pagesImproper Handling of Collections: Observations and Recommendationsdemos reaNo ratings yet

- 02-Abucay2014 CoverDocument1 page02-Abucay2014 Coverdemos reaNo ratings yet

- Statement of Management'S Responsibility For Financial StatementsDocument1 pageStatement of Management'S Responsibility For Financial Statementsdemos reaNo ratings yet

- 08-Abucay2014 Part1-Financial StatementsDocument5 pages08-Abucay2014 Part1-Financial Statementsdemos reaNo ratings yet

- AssignDocument18 pagesAssignRalph Adrian MielNo ratings yet

- Finance Submission 02Document58 pagesFinance Submission 02prathamgharat019No ratings yet

- About Rtgs & NeftDocument5 pagesAbout Rtgs & NeftAbdulhussain JariwalaNo ratings yet

- Agriclinics and Agribusiness CentersDocument47 pagesAgriclinics and Agribusiness CentersMadhavilathaNo ratings yet

- Cooperative MarketingDocument2 pagesCooperative MarketinggnmadaviNo ratings yet

- Capacity Planning For Products and ServicesDocument27 pagesCapacity Planning For Products and ServicesJose Mario PagsanjanNo ratings yet

- The Role of Microbusinesses in The Economy: by Brian Headd, EconomistDocument1 pageThe Role of Microbusinesses in The Economy: by Brian Headd, Economist--No ratings yet

- Sanjay Kanojiya-ElectricalDocument1 pageSanjay Kanojiya-ElectricalAMANNo ratings yet

- Capital & Class 1993 Naples 119 37Document20 pagesCapital & Class 1993 Naples 119 37D. Silva EscobarNo ratings yet

- Floor Plan Lending PrimerDocument73 pagesFloor Plan Lending PrimerCari Mangalindan MacaalayNo ratings yet

- Upto 1000 Solved MCQs of MKT501 Marketing Management WWW - VustudentsDocument228 pagesUpto 1000 Solved MCQs of MKT501 Marketing Management WWW - VustudentsLyla Abbas Khan100% (24)

- Chapter - 12 - Inventory Accounting For Consumable SuppliesDocument10 pagesChapter - 12 - Inventory Accounting For Consumable SuppliesJa Mi LahNo ratings yet

- Classification of Reserves and ResourcesDocument27 pagesClassification of Reserves and Resourcesnina chentsovaNo ratings yet

- General Banking Activities of Jamuna BankDocument52 pagesGeneral Banking Activities of Jamuna BankFatin Arefin0% (1)

- Pilipinas Shell Petroleum Corporation: SHLPHDocument17 pagesPilipinas Shell Petroleum Corporation: SHLPHIsis Normagne PascualNo ratings yet

- Cfo AgendaDocument7 pagesCfo AgendaMOORTHY.KENo ratings yet

- Part 1 CapstoneDocument14 pagesPart 1 Capstonenica abellanaNo ratings yet

- Xcel CFA® Series: Financial Reporting and Analysis Reading 25Document6 pagesXcel CFA® Series: Financial Reporting and Analysis Reading 25Naseer AhmedNo ratings yet

- Ti TechDocument4 pagesTi Techmadddy_hyd100% (3)

- By Hamed Armesh 1082200034Document22 pagesBy Hamed Armesh 1082200034Roozbeh HojabriNo ratings yet

- Consumer Behavior Buying Having and Being 11th Edition Solomon Test Bank 1Document25 pagesConsumer Behavior Buying Having and Being 11th Edition Solomon Test Bank 1elizabeth100% (44)

- The Is Greater Than The Sum of Its Parts.: WholeDocument18 pagesThe Is Greater Than The Sum of Its Parts.: WholeAkshata MalhotraNo ratings yet

- A Study On The Challenges HR Managers Face TodayDocument10 pagesA Study On The Challenges HR Managers Face TodayJAY MARK TANONo ratings yet

- Theory Madison Proposal LowresDocument68 pagesTheory Madison Proposal Lowresinfo.giantholdingsNo ratings yet

- Ismt LTD (2019-2020)Document150 pagesIsmt LTD (2019-2020)Nimit BhimjiyaniNo ratings yet

- Financial Forecasting For Strategic GrowthDocument3 pagesFinancial Forecasting For Strategic GrowthVergel MartinezNo ratings yet