Download as pdf or txt

You might also like

- HR 5E 5Th Edition Angelo S Denisi Full ChapterDocument67 pagesHR 5E 5Th Edition Angelo S Denisi Full Chapterjay.landers807100% (12)

- Investing in People: Financial Impact of Human Resource InitiativesFrom EverandInvesting in People: Financial Impact of Human Resource InitiativesNo ratings yet

- The HR Scorecard (Review and Analysis of Becker, Huselid and Ulrich's Book)From EverandThe HR Scorecard (Review and Analysis of Becker, Huselid and Ulrich's Book)Rating: 5 out of 5 stars5/5 (1)

- In The Matter of Prince Rogers NelsonDocument12 pagesIn The Matter of Prince Rogers NelsonBillboard100% (2)

- Human Resource AccountingDocument15 pagesHuman Resource AccountingAbdur Rob RejveeNo ratings yet

- High-Impact Human Capital Strategy: Addressing the 12 Major Challenges Today's Organizations FaceFrom EverandHigh-Impact Human Capital Strategy: Addressing the 12 Major Challenges Today's Organizations FaceNo ratings yet

- 3 Conflict of InterestDocument3 pages3 Conflict of InterestTressa Salarza PendangNo ratings yet

- Oberlin College Black Student Union Institutional DemandsDocument14 pagesOberlin College Black Student Union Institutional DemandsLegal Insurrection14% (14)

- Krupanidhi School of Mangamentpage 1Document20 pagesKrupanidhi School of Mangamentpage 1DarshanPrimeNo ratings yet

- Human Resource AccountingDocument242 pagesHuman Resource AccountingmnjbashNo ratings yet

- Human Resource Accounting Mid Term Chapter 1 2 4Document32 pagesHuman Resource Accounting Mid Term Chapter 1 2 4HasanKhanNo ratings yet

- Human Resource AccountingDocument240 pagesHuman Resource AccountingIoana MillerNo ratings yet

- Human Resource AccountingDocument240 pagesHuman Resource AccountingSasirekha84% (19)

- HRA-Introduction and HR Costs and Financial ReportingDocument25 pagesHRA-Introduction and HR Costs and Financial ReportingCollin EdwardNo ratings yet

- Human Resource Accounting:: InvestmentsDocument4 pagesHuman Resource Accounting:: InvestmentsRuchi GargNo ratings yet

- Human Resource AccountingDocument14 pagesHuman Resource AccountingsumitruNo ratings yet

- Course Title: Accounting For Managers Course: MBA 18102 CR Session: Spring 2020 Unit IV. Human Resource Accounting and Its ApproachesDocument6 pagesCourse Title: Accounting For Managers Course: MBA 18102 CR Session: Spring 2020 Unit IV. Human Resource Accounting and Its ApproachesLeo SaimNo ratings yet

- Human Resource Accouting 260214Document175 pagesHuman Resource Accouting 260214Pradeep SinghNo ratings yet

- Human Resource AccountingDocument39 pagesHuman Resource AccountingAnkit SharmaNo ratings yet

- Hra IiDocument50 pagesHra IiShanil BohraNo ratings yet

- Role of Human Resource Accounting in TheDocument9 pagesRole of Human Resource Accounting in TheApurva SharmaNo ratings yet

- Human Resource Accounting in Indian Companies - Importance and ChallengesDocument4 pagesHuman Resource Accounting in Indian Companies - Importance and ChallengesSriNo ratings yet

- Assignment HRADocument22 pagesAssignment HRACHIRAG V VYASNo ratings yet

- Human Resource Accounting: Practical Challenges in Recognition, Measurement, Accounting Treatment Procedure and A Possible Way OutDocument6 pagesHuman Resource Accounting: Practical Challenges in Recognition, Measurement, Accounting Treatment Procedure and A Possible Way OutJkNo ratings yet

- Human Resource AccountingDocument8 pagesHuman Resource AccountingRewa BhasinNo ratings yet

- HR Accounting PDFDocument10 pagesHR Accounting PDFGaith BsharatNo ratings yet

- History of Human Resource AccountingDocument11 pagesHistory of Human Resource AccountingMd Khaled NoorNo ratings yet

- Unit 6Document44 pagesUnit 6EYOB AHMEDNo ratings yet

- Assignment: Resource Management-Valuation of Human Resources - Methodologies and PracticesDocument7 pagesAssignment: Resource Management-Valuation of Human Resources - Methodologies and PracticespriyankaNo ratings yet

- Human Resource Accounting-A New DimensionDocument18 pagesHuman Resource Accounting-A New Dimensionhossein100% (2)

- Evidence - Based Human ResourcesDocument23 pagesEvidence - Based Human ResourcesJassiel100% (1)

- Human Resource AccountingDocument47 pagesHuman Resource AccountingYash VoraNo ratings yet

- Chapter 1: IntroductionDocument31 pagesChapter 1: IntroductionManoj KrishnanNo ratings yet

- HCM Unit-IiDocument23 pagesHCM Unit-IiPrasadarao YenugulaNo ratings yet

- Human Resources Accounting Unit 1Document14 pagesHuman Resources Accounting Unit 1World is GoldNo ratings yet

- Hra For Managing Human Resources: Decision MakingDocument11 pagesHra For Managing Human Resources: Decision MakinglovleshrubyNo ratings yet

- HRADocument11 pagesHRAMd. Shamim HossainNo ratings yet

- PP. Human Resource Accounting Last EdtidDocument21 pagesPP. Human Resource Accounting Last EdtidHope KnockNo ratings yet

- Research Paper On Human Resource AccountingDocument4 pagesResearch Paper On Human Resource Accountingsvfziasif100% (1)

- Dbim HraDocument3 pagesDbim HraAlif ShaikhNo ratings yet

- Human Resources Accounting Concepts Objectives Models and CriticismDocument10 pagesHuman Resources Accounting Concepts Objectives Models and Criticismpavan kumarNo ratings yet

- Human Resource AccountingDocument5 pagesHuman Resource AccountingChowdhury NishatNo ratings yet

- HR Valuation and AccountingDocument10 pagesHR Valuation and AccountingSanskar YadavNo ratings yet

- Culture AdvancementDocument24 pagesCulture AdvancementSilver TricksNo ratings yet

- Thesis On Human Resource Accounting PDFDocument5 pagesThesis On Human Resource Accounting PDFashleycornettneworleans100% (2)

- Human Resource Accounting: BY K. Venkata Ramana Lecturer, Mba Dept.,Giacr RayagadaDocument11 pagesHuman Resource Accounting: BY K. Venkata Ramana Lecturer, Mba Dept.,Giacr RayagadasaiprasannamudirajNo ratings yet

- Assignment: Resource Management-Valuation of Human Resources - Methodologies and PracticesDocument11 pagesAssignment: Resource Management-Valuation of Human Resources - Methodologies and PracticespriyankaNo ratings yet

- Human Resource Accounting: Meaning, Definition, Objectives and LimitationsDocument3 pagesHuman Resource Accounting: Meaning, Definition, Objectives and LimitationsSanaullah M SultanpurNo ratings yet

- Human Resource AccountingDocument31 pagesHuman Resource AccountingmnjbashNo ratings yet

- Talent ManagementDocument8 pagesTalent Managementricha sharma291No ratings yet

- Term Paper On HraDocument30 pagesTerm Paper On HraDeidre StuartNo ratings yet

- Unit 5 Human Resource Accounting: StructureDocument20 pagesUnit 5 Human Resource Accounting: StructureArun SankarNo ratings yet

- Running Head: Human Resource Accounting 1Document6 pagesRunning Head: Human Resource Accounting 1Irynn RynnNo ratings yet

- Thomas Arkan: Introduction To Human Resources AccountingDocument1 pageThomas Arkan: Introduction To Human Resources AccountingWelcome 1995No ratings yet

- Asian Journal of Management ResearchDocument8 pagesAsian Journal of Management Researcharun1974No ratings yet

- What Is HraDocument19 pagesWhat Is Hradagar0071No ratings yet

- HRA - Definition, Objectives, Advantages & DisadvantagesDocument4 pagesHRA - Definition, Objectives, Advantages & DisadvantagesArghya D Punk100% (1)

- Study of Human Resource Accounting Practices: April 2018Document4 pagesStudy of Human Resource Accounting Practices: April 2018Priyanka YadavNo ratings yet

- Human Resource Management in the Knowledge Economy: New Challenges, New Roles, New CapabilitiesFrom EverandHuman Resource Management in the Knowledge Economy: New Challenges, New Roles, New CapabilitiesRating: 3 out of 5 stars3/5 (5)

- Human Capital Management: What Really Works in GovernmentFrom EverandHuman Capital Management: What Really Works in GovernmentNo ratings yet

- Achieving Excellence in Human Resources Management: An Assessment of Human Resource FunctionsFrom EverandAchieving Excellence in Human Resources Management: An Assessment of Human Resource FunctionsRating: 3 out of 5 stars3/5 (1)

- The ACE Advantage: How Smart Companies Unleash Talent for Optimal PerformanceFrom EverandThe ACE Advantage: How Smart Companies Unleash Talent for Optimal PerformanceNo ratings yet

- Business Environment AnalysisDocument29 pagesBusiness Environment AnalysisISHFAQ ASHRAFNo ratings yet

- Evolution of International BusinessDocument6 pagesEvolution of International BusinessISHFAQ ASHRAFNo ratings yet

- Factsheet of SEZsDocument1 pageFactsheet of SEZsISHFAQ ASHRAFNo ratings yet

- Presentation On World Bank and Its Role in IndiaDocument32 pagesPresentation On World Bank and Its Role in IndiaISHFAQ ASHRAFNo ratings yet

- World Trade Organisation (WTO)Document22 pagesWorld Trade Organisation (WTO)ISHFAQ ASHRAFNo ratings yet

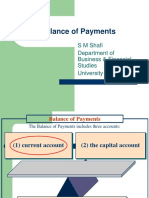

- Balance of Payments: S M Shafi Department of Business & Financial Studies University of KashmirDocument9 pagesBalance of Payments: S M Shafi Department of Business & Financial Studies University of KashmirISHFAQ ASHRAFNo ratings yet

- EXIM Bank: Dr. S M Shafi Department of Business & Financial Studies, KUDocument12 pagesEXIM Bank: Dr. S M Shafi Department of Business & Financial Studies, KUISHFAQ ASHRAFNo ratings yet

- Bretton Woods System: The Collapse of Fixed Exchange Rate SystemDocument34 pagesBretton Woods System: The Collapse of Fixed Exchange Rate SystemISHFAQ ASHRAFNo ratings yet

- Asian Development Bank (Asia)Document19 pagesAsian Development Bank (Asia)ISHFAQ ASHRAFNo ratings yet

- Responsibility AccountingDocument7 pagesResponsibility AccountingISHFAQ ASHRAFNo ratings yet

- Advantages of International Business: Dr. S M Shafi Department of Business & Financial Studies, KUDocument4 pagesAdvantages of International Business: Dr. S M Shafi Department of Business & Financial Studies, KUISHFAQ ASHRAFNo ratings yet

- Accounting Unit 3Document19 pagesAccounting Unit 3ISHFAQ ASHRAFNo ratings yet

- Inflation AccountingDocument18 pagesInflation AccountingISHFAQ ASHRAFNo ratings yet

- Accounting Unit 2Document19 pagesAccounting Unit 2ISHFAQ ASHRAFNo ratings yet

- Packaging N Labelling of Packaged Drinking WaterDocument10 pagesPackaging N Labelling of Packaged Drinking WaterISHFAQ ASHRAFNo ratings yet

- How Is Bottled Water Different From Tap Water?Document4 pagesHow Is Bottled Water Different From Tap Water?ISHFAQ ASHRAFNo ratings yet

- PDW IntroDocument6 pagesPDW IntroISHFAQ ASHRAFNo ratings yet

- 033-Philippine Appliance Corp v. CA, G.R. No. 149434, June 3, 2004Document4 pages033-Philippine Appliance Corp v. CA, G.R. No. 149434, June 3, 2004Jopan SJNo ratings yet

- Worker's Participation in Management in India by Nishat Mba 3 SEMDocument20 pagesWorker's Participation in Management in India by Nishat Mba 3 SEMNishat AhmadNo ratings yet

- Starbucks Corporation-Case StudyDocument3 pagesStarbucks Corporation-Case StudyAyesha AnsNo ratings yet

- 2023 - 07 - Tension Is Rising Around Remote WorkDocument10 pages2023 - 07 - Tension Is Rising Around Remote WorkRitvik SinghNo ratings yet

- Islam and Business EthicsDocument27 pagesIslam and Business EthicsSyed Oon Haider ZaidiNo ratings yet

- IBIS FabricCraftSewingSuppliesStoresintheUSDocument41 pagesIBIS FabricCraftSewingSuppliesStoresintheUSmaily24No ratings yet

- Retail Impact Assessment WhitePaper 20 Sep 2020 v2Document24 pagesRetail Impact Assessment WhitePaper 20 Sep 2020 v2Narottam SharmaNo ratings yet

- 27 - Hotel Specialist Tagaytay Inc. v..20210505-11-1fg6pgfDocument23 pages27 - Hotel Specialist Tagaytay Inc. v..20210505-11-1fg6pgfPio Vincent BuencaminoNo ratings yet

- Guide Certificate: Banking Employees" Under My Supervision in Partial Fulfilment of The Master of BusinessDocument55 pagesGuide Certificate: Banking Employees" Under My Supervision in Partial Fulfilment of The Master of BusinessHomi NathNo ratings yet

- "If I Negotiate, Will My Severance Be Taken Off The Table?": Alan L. SkloverDocument2 pages"If I Negotiate, Will My Severance Be Taken Off The Table?": Alan L. Sklovere4mak9230100% (1)

- FULL Download Ebook PDF International and Comparative Employment Relations National Regulation Global Changes Sixth Edition PDF EbookDocument42 pagesFULL Download Ebook PDF International and Comparative Employment Relations National Regulation Global Changes Sixth Edition PDF Ebookquiana.dobiesz290100% (41)

- Indian Facilities Management Services Report-FinalDocument51 pagesIndian Facilities Management Services Report-FinalTarun Soni50% (2)

- Diversity Case PDFDocument14 pagesDiversity Case PDFALI AKHTARNo ratings yet

- Data Final 10th Jan 19Document15 pagesData Final 10th Jan 19Sumiran GiriNo ratings yet

- Teachers'/Trainers' Industrial Attachment Individual ReportDocument18 pagesTeachers'/Trainers' Industrial Attachment Individual ReportBezawit MekonnenNo ratings yet

- Eco Dynamics Eba 2Document33 pagesEco Dynamics Eba 2Beau HumeNo ratings yet

- Labor Relations: Assistant Ombudsman Leilanie Bernadette C. CabrasDocument9 pagesLabor Relations: Assistant Ombudsman Leilanie Bernadette C. CabrasRonaldo ValladoresNo ratings yet

- 1041 Interview PacketDocument15 pages1041 Interview PacketLalaina RAKOTONIRIANANo ratings yet

- A - Course Outline - BUPDocument9 pagesA - Course Outline - BUPZubayer AhmmedNo ratings yet

- LaborDocument12 pagesLaborAnonymous tlQd2LINo ratings yet

- Cases Digest Labor 1114Document97 pagesCases Digest Labor 1114DenardConwiBesaNo ratings yet

- 7 PsDocument3 pages7 PsAdriana CarinanNo ratings yet

- CASE STUDY All TyresDocument9 pagesCASE STUDY All Tyresمصطفى محمدNo ratings yet

- ALS Annual Report 2019Document98 pagesALS Annual Report 2019Scott SchonbergerNo ratings yet

- Michigan Legislature - Summary During Lame-Duck Session 2012Document63 pagesMichigan Legislature - Summary During Lame-Duck Session 2012Stephen BoyleNo ratings yet

- Official Thesis Sept 4 13Document67 pagesOfficial Thesis Sept 4 13Eve DC100% (1)