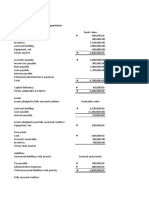

NCR Frontliners 2017 Tax

NCR Frontliners 2017 Tax

You might also like

- Post Test Regular Income Taxation For PartnershipsDocument6 pagesPost Test Regular Income Taxation For Partnershipslena cpaNo ratings yet

- Application - Regular Income Tax On Individuals and CorporationsDocument8 pagesApplication - Regular Income Tax On Individuals and CorporationsElla Marie Lopez0% (1)

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- ANSWERS Post Test Regular Income Taxation For PartnershipsDocument8 pagesANSWERS Post Test Regular Income Taxation For Partnershipslena cpa100% (1)

- Taxation Cup SeriesDocument5 pagesTaxation Cup SeriesGlaiza Atillo Batuto Orgino100% (1)

- Final and Capital Gains TaxDocument7 pagesFinal and Capital Gains TaxElla Marie LopezNo ratings yet

- Estate Tax PayableDocument8 pagesEstate Tax PayableHazel Jane Esclamada100% (2)

- Activity / Assignment: Answer and SolutionDocument3 pagesActivity / Assignment: Answer and SolutionMa. Alexandria Palma0% (1)

- Revisiting The Jalong Ambush Site (Hussars)Document41 pagesRevisiting The Jalong Ambush Site (Hussars)stmcipohNo ratings yet

- SupervisionDocument45 pagesSupervisionsunielgowda100% (5)

- Taxation Suggested SolutionsDocument3 pagesTaxation Suggested SolutionsSteven Mark MananguNo ratings yet

- Determination of The Net Taxable Estate Illustration 1: Single Resident or Citizen DecedentDocument14 pagesDetermination of The Net Taxable Estate Illustration 1: Single Resident or Citizen DecedentLea ChermarnNo ratings yet

- Estate Tax ProblemsDocument22 pagesEstate Tax ProblemsfanchasticommsNo ratings yet

- Chapter 5Document6 pagesChapter 5Briggs Navarro BaguioNo ratings yet

- Calanuga Assignment Final Period Activity - TAX 202ADocument5 pagesCalanuga Assignment Final Period Activity - TAX 202Acjmarie.cadenasNo ratings yet

- Problem 1: Net Taxable Estate 530,000 75,000 605,000Document3 pagesProblem 1: Net Taxable Estate 530,000 75,000 605,000camscamsNo ratings yet

- How To Fill Up Tax Return FormDocument19 pagesHow To Fill Up Tax Return Formmukulful2008100% (4)

- Reviewer TAXDocument3 pagesReviewer TAXAnnabel MendozaNo ratings yet

- Answer Keys For Midterm Exam PART 2Document3 pagesAnswer Keys For Midterm Exam PART 2Angel MaghuyopNo ratings yet

- Solutions To Problems: Pe On Estate TaxDocument11 pagesSolutions To Problems: Pe On Estate TaxErica NicolasuraNo ratings yet

- TAXATION 2 Chapter 5 Estate Tax Payable PDFDocument5 pagesTAXATION 2 Chapter 5 Estate Tax Payable PDFKim Cristian MaañoNo ratings yet

- BslDocument4 pagesBslŘähûł Ř Š ŚãřöjNo ratings yet

- 8.2 Assignment - Regular Income Tax For Individuals (For Discussion)Document8 pages8.2 Assignment - Regular Income Tax For Individuals (For Discussion)Roselyn LumbaoNo ratings yet

- He Is Not Subject To Basic Income Tax. However, His 13th Month Pay Exceeds 90,000. ThereforeDocument15 pagesHe Is Not Subject To Basic Income Tax. However, His 13th Month Pay Exceeds 90,000. ThereforeEarl Daniel RemorozaNo ratings yet

- Bustax Midtem Quiz 1 Answer Key Problem SolvingDocument2 pagesBustax Midtem Quiz 1 Answer Key Problem Solvingralph anthony macahiligNo ratings yet

- Word Problems TaDocument15 pagesWord Problems TaMaissyNo ratings yet

- Module 1: Donor'S Taxation Lesson 1 Activities:: Name: Daniel I. Dialino Section: BSA 3-4Document21 pagesModule 1: Donor'S Taxation Lesson 1 Activities:: Name: Daniel I. Dialino Section: BSA 3-4Daniel DialinoNo ratings yet

- Midterms Sa2 FARDocument6 pagesMidterms Sa2 FAREloiNo ratings yet

- Tax QuizDocument3 pagesTax QuizLora Mae JuanitoNo ratings yet

- TaxfinDocument3 pagesTaxfinShr BnNo ratings yet

- Corporate LiquidationDocument8 pagesCorporate LiquidationKyo TieNo ratings yet

- Exercises On Estate Tax Additional ProblemsDocument8 pagesExercises On Estate Tax Additional ProblemsMidas Troy VictorNo ratings yet

- Chapter 5 - Estate Tax2013Document12 pagesChapter 5 - Estate Tax2013Anjo Ellis100% (2)

- IGNOU MCA MCS-035 Free Solved Assignments 2010Document11 pagesIGNOU MCA MCS-035 Free Solved Assignments 2010Deepti SainiNo ratings yet

- Corporate Liquidation Problem SolvingDocument21 pagesCorporate Liquidation Problem SolvingRujean Salar AltejarNo ratings yet

- Accounting Special TransactionDocument25 pagesAccounting Special TransactionMarinel Mae ChicaNo ratings yet

- Reviewer Fabm2Document3 pagesReviewer Fabm2Mark LappayNo ratings yet

- Final Income Taxation - Class Discussion (Corrected)Document21 pagesFinal Income Taxation - Class Discussion (Corrected)Christopher SantosNo ratings yet

- Frias Activity 6Document6 pagesFrias Activity 6Lars FriasNo ratings yet

- Chapter 3Document12 pagesChapter 3Briggs Navarro BaguioNo ratings yet

- Cash and Accrual BasisDocument10 pagesCash and Accrual BasisNoeme LansangNo ratings yet

- De Vera Angela Kyle G. Business Taxation Prelim Task 2.1 BSADocument11 pagesDe Vera Angela Kyle G. Business Taxation Prelim Task 2.1 BSAJohn Francis RosasNo ratings yet

- Project Taxation (Ouano)Document16 pagesProject Taxation (Ouano)GuiltyCrownNo ratings yet

- BusCom Practice SetsDocument20 pagesBusCom Practice SetsShaz NagaNo ratings yet

- CTT Answer Season 1Document4 pagesCTT Answer Season 1ucc second yearNo ratings yet

- CTT Answer Season 1Document4 pagesCTT Answer Season 1ucc second yearNo ratings yet

- Income Taxation Answer ExamDocument5 pagesIncome Taxation Answer Examyezaquera100% (1)

- Quiz 3 - CabigonDocument4 pagesQuiz 3 - CabigonRie CabigonNo ratings yet

- 8.2 Assignment - Regular Income Tax For IndividualsDocument8 pages8.2 Assignment - Regular Income Tax For Individualssam imperialNo ratings yet

- Presented by Archana Gupta 0221031 Bharat Gaikwad 0221023Document12 pagesPresented by Archana Gupta 0221031 Bharat Gaikwad 0221023Bharat GaikwadNo ratings yet

- BSMA Taxation of IndividualsDocument32 pagesBSMA Taxation of IndividualsAngela CanayaNo ratings yet

- Toaz - Info 89bf91d5 1612761367237 PRDocument7 pagesToaz - Info 89bf91d5 1612761367237 PRAEHYUN YENVYNo ratings yet

- EstateDocument8 pagesEstateLyka RoguelNo ratings yet

- CABINAS - Partnership Formation & OperationDocument16 pagesCABINAS - Partnership Formation & OperationJoshua CabinasNo ratings yet

- Assignment E & L Env 4 BusiDocument9 pagesAssignment E & L Env 4 BusiSyed Hamza RasheedNo ratings yet

- Non-Resident Foreign CorporationDocument4 pagesNon-Resident Foreign CorporationRosemarie CruzNo ratings yet

- Wealth Management Planning: The UK Tax PrinciplesFrom EverandWealth Management Planning: The UK Tax PrinciplesRating: 4.5 out of 5 stars4.5/5 (2)

- Real Estate Investing 101: Best Way to Buy a House and Save Big, Top 20 TipsFrom EverandReal Estate Investing 101: Best Way to Buy a House and Save Big, Top 20 TipsNo ratings yet

- A Stiptick for a Bleeding Nation: Or, a safe and speedy way to restore publick credit, and pay the national debtsFrom EverandA Stiptick for a Bleeding Nation: Or, a safe and speedy way to restore publick credit, and pay the national debtsNo ratings yet

- Property & Taxation: A Practical Guide to Saving Tax on Your Property InvestmentsFrom EverandProperty & Taxation: A Practical Guide to Saving Tax on Your Property InvestmentsNo ratings yet

- 19697ipcc Acc Vol2 Chapter15Document4 pages19697ipcc Acc Vol2 Chapter15jsus22No ratings yet

- Living-Limitations-And-Challenges-semi-pa-lang-talaga Drawing Near To Final Konti Na Lang Promise EditedDocument91 pagesLiving-Limitations-And-Challenges-semi-pa-lang-talaga Drawing Near To Final Konti Na Lang Promise Editedjsus220% (1)

- Issues in Partnership Accounts: Basic ConceptsDocument40 pagesIssues in Partnership Accounts: Basic Conceptsjsus22No ratings yet

- Profit or Loss Pre and Post Incorporation: Learning ObjectivesDocument20 pagesProfit or Loss Pre and Post Incorporation: Learning Objectivesjsus22No ratings yet

- Purpose of The StudyDocument8 pagesPurpose of The Studyjsus22No ratings yet

- Cat - Module 3.solutions.3.1 To3.4Document11 pagesCat - Module 3.solutions.3.1 To3.4jsus22No ratings yet

- Accounting For Bonus Issue: Learning ObjectivesDocument8 pagesAccounting For Bonus Issue: Learning Objectivesjsus22No ratings yet

- Chapter-1 HSDocument7 pagesChapter-1 HSjsus22No ratings yet

- Philippines Ifrs ProfileDocument6 pagesPhilippines Ifrs Profilejsus22No ratings yet

- Parallax Production Marketing and Sales's Company Policy: 7 Colors PartnershipDocument9 pagesParallax Production Marketing and Sales's Company Policy: 7 Colors Partnershipjsus22No ratings yet

- NOTES On PFRS 9 Financial InstrumentsDocument11 pagesNOTES On PFRS 9 Financial Instrumentsjsus22100% (1)

- Concessionary Card FormDocument2 pagesConcessionary Card Formjsus22No ratings yet

- Basic Package: Monoceros PDocument6 pagesBasic Package: Monoceros Pjsus22No ratings yet

- TAX3Document3 pagesTAX3jsus22No ratings yet

- Resa BL 1st Preboard Jul2014Document7 pagesResa BL 1st Preboard Jul2014EuniceChungNo ratings yet

- RFBT Mcqs New TopicsDocument20 pagesRFBT Mcqs New TopicsjexNo ratings yet

- Court Oft Ax Appeal: DecisionDocument18 pagesCourt Oft Ax Appeal: Decisionjsus22No ratings yet

- Major Quiz #2Document10 pagesMajor Quiz #2jsus22No ratings yet

- Adult Living Donor Liver Transplant: Questions and AnswersDocument36 pagesAdult Living Donor Liver Transplant: Questions and Answersjsus22No ratings yet

- BWR - Jul-Aug - 2016 - BMC 2015 Bottled Water Stat ArticleDocument9 pagesBWR - Jul-Aug - 2016 - BMC 2015 Bottled Water Stat Articlejsus22No ratings yet

- Chanrobles Internet Bar Review: Chanrobles Professional Review, IncDocument13 pagesChanrobles Internet Bar Review: Chanrobles Professional Review, Incjsus22No ratings yet

- Mark-Up Price Product Size Product Cost Per Package Mark-Up Percentage Children's Flavored Drinks Sports and Adventure Drinking WaterDocument2 pagesMark-Up Price Product Size Product Cost Per Package Mark-Up Percentage Children's Flavored Drinks Sports and Adventure Drinking Waterjsus22No ratings yet

- Hci Acc Web December 31 2016-1Document52 pagesHci Acc Web December 31 2016-1Joseph FranciscoNo ratings yet

- GFFS General-Form Rev-20061Document14 pagesGFFS General-Form Rev-20061Judy Ann GacetaNo ratings yet

- Lesson 3 Module 3 Lec - Data Security AwarenessDocument16 pagesLesson 3 Module 3 Lec - Data Security AwarenessJenica Mae SaludesNo ratings yet

- Economics of PiggeryDocument3 pagesEconomics of Piggerysrujan NJNo ratings yet

- Health and Physical Education ThesisDocument35 pagesHealth and Physical Education ThesisZia IslamNo ratings yet

- Gurrea V LezamaDocument2 pagesGurrea V LezamaEdward Kenneth Kung100% (1)

- Two Versions PDFDocument70 pagesTwo Versions PDFkamilghoshalNo ratings yet

- ED Hiring GuideDocument20 pagesED Hiring Guidechokx008No ratings yet

- M B ADocument98 pagesM B AGopuNo ratings yet

- Nta (Ugc-Net) : Ask, Learn & LeadDocument18 pagesNta (Ugc-Net) : Ask, Learn & LeadprajwalbhatNo ratings yet

- Psychiatric Nursing NotesDocument13 pagesPsychiatric Nursing NotesCarlo VigoNo ratings yet

- 2023 California Model Year 1978 or Older Light-Duty Vehicle SurveyDocument10 pages2023 California Model Year 1978 or Older Light-Duty Vehicle SurveyNick PopeNo ratings yet

- Fouts Def 2nd Production of DocumentsDocument88 pagesFouts Def 2nd Production of Documentswolf woodNo ratings yet

- Ba311 - Module 5 Capacity ManagementDocument10 pagesBa311 - Module 5 Capacity ManagementShams PeloperoNo ratings yet

- Ee NewDocument1 pageEe Newhsbibahmed091No ratings yet

- Laundry and Bourbon AnalysisDocument2 pagesLaundry and Bourbon AnalysisAveryNo ratings yet

- ThesisDocument5 pagesThesisSampayan Angelica A.No ratings yet

- The FATF Recommendations On Combating Money Laundering and The Financing of Terrorism & ProliferationDocument27 pagesThe FATF Recommendations On Combating Money Laundering and The Financing of Terrorism & ProliferationAli SaeedNo ratings yet

- Weekly Report w34Document19 pagesWeekly Report w34Asep MAkmurNo ratings yet

- Rishika Dass: Growth and Importance of MSMEDocument2 pagesRishika Dass: Growth and Importance of MSMEagantook2607No ratings yet

- Week 1, Hebrews 1:1-14 HookDocument9 pagesWeek 1, Hebrews 1:1-14 HookDawit ShankoNo ratings yet

- Review of ApplicationDocument6 pagesReview of ApplicationPrabath ChinthakaNo ratings yet

- Copia de The Green Banana Lecturas I 2020Document4 pagesCopia de The Green Banana Lecturas I 2020Finn SolórzanoNo ratings yet

- 31-07-2020 - The Hindu Handwritten NotesDocument16 pages31-07-2020 - The Hindu Handwritten NotesnishuNo ratings yet

- Corpse Grinder Cult Lijst - 1.2Document4 pagesCorpse Grinder Cult Lijst - 1.2Jimmy CarterNo ratings yet

- 2 - AC Corporation (ACC) v. CIRDocument20 pages2 - AC Corporation (ACC) v. CIRCarlota VillaromanNo ratings yet

- SP 70Document75 pagesSP 70Barbie Turic100% (2)

- Equatorial Realty Vs Mayfair TheaterDocument2 pagesEquatorial Realty Vs Mayfair TheaterSaji Jimeno100% (1)

- Memorial For The Appellants-Team Code L PDFDocument44 pagesMemorial For The Appellants-Team Code L PDFAbhineet KaliaNo ratings yet

Download as rtf, pdf, or txt

You might also like

- Post Test Regular Income Taxation For PartnershipsDocument6 pagesPost Test Regular Income Taxation For Partnershipslena cpaNo ratings yet

- Application - Regular Income Tax On Individuals and CorporationsDocument8 pagesApplication - Regular Income Tax On Individuals and CorporationsElla Marie Lopez0% (1)

- The Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeFrom EverandThe Gone Fishin' Portfolio: Get Wise, Get Wealthy...and Get on With Your LifeNo ratings yet

- ANSWERS Post Test Regular Income Taxation For PartnershipsDocument8 pagesANSWERS Post Test Regular Income Taxation For Partnershipslena cpa100% (1)

- Taxation Cup SeriesDocument5 pagesTaxation Cup SeriesGlaiza Atillo Batuto Orgino100% (1)

- Final and Capital Gains TaxDocument7 pagesFinal and Capital Gains TaxElla Marie LopezNo ratings yet

- Estate Tax PayableDocument8 pagesEstate Tax PayableHazel Jane Esclamada100% (2)

- Activity / Assignment: Answer and SolutionDocument3 pagesActivity / Assignment: Answer and SolutionMa. Alexandria Palma0% (1)

- Revisiting The Jalong Ambush Site (Hussars)Document41 pagesRevisiting The Jalong Ambush Site (Hussars)stmcipohNo ratings yet

- SupervisionDocument45 pagesSupervisionsunielgowda100% (5)

- Taxation Suggested SolutionsDocument3 pagesTaxation Suggested SolutionsSteven Mark MananguNo ratings yet

- Determination of The Net Taxable Estate Illustration 1: Single Resident or Citizen DecedentDocument14 pagesDetermination of The Net Taxable Estate Illustration 1: Single Resident or Citizen DecedentLea ChermarnNo ratings yet

- Estate Tax ProblemsDocument22 pagesEstate Tax ProblemsfanchasticommsNo ratings yet

- Chapter 5Document6 pagesChapter 5Briggs Navarro BaguioNo ratings yet

- Calanuga Assignment Final Period Activity - TAX 202ADocument5 pagesCalanuga Assignment Final Period Activity - TAX 202Acjmarie.cadenasNo ratings yet

- Problem 1: Net Taxable Estate 530,000 75,000 605,000Document3 pagesProblem 1: Net Taxable Estate 530,000 75,000 605,000camscamsNo ratings yet

- How To Fill Up Tax Return FormDocument19 pagesHow To Fill Up Tax Return Formmukulful2008100% (4)

- Reviewer TAXDocument3 pagesReviewer TAXAnnabel MendozaNo ratings yet

- Answer Keys For Midterm Exam PART 2Document3 pagesAnswer Keys For Midterm Exam PART 2Angel MaghuyopNo ratings yet

- Solutions To Problems: Pe On Estate TaxDocument11 pagesSolutions To Problems: Pe On Estate TaxErica NicolasuraNo ratings yet

- TAXATION 2 Chapter 5 Estate Tax Payable PDFDocument5 pagesTAXATION 2 Chapter 5 Estate Tax Payable PDFKim Cristian MaañoNo ratings yet

- BslDocument4 pagesBslŘähûł Ř Š ŚãřöjNo ratings yet

- 8.2 Assignment - Regular Income Tax For Individuals (For Discussion)Document8 pages8.2 Assignment - Regular Income Tax For Individuals (For Discussion)Roselyn LumbaoNo ratings yet

- He Is Not Subject To Basic Income Tax. However, His 13th Month Pay Exceeds 90,000. ThereforeDocument15 pagesHe Is Not Subject To Basic Income Tax. However, His 13th Month Pay Exceeds 90,000. ThereforeEarl Daniel RemorozaNo ratings yet

- Bustax Midtem Quiz 1 Answer Key Problem SolvingDocument2 pagesBustax Midtem Quiz 1 Answer Key Problem Solvingralph anthony macahiligNo ratings yet

- Word Problems TaDocument15 pagesWord Problems TaMaissyNo ratings yet

- Module 1: Donor'S Taxation Lesson 1 Activities:: Name: Daniel I. Dialino Section: BSA 3-4Document21 pagesModule 1: Donor'S Taxation Lesson 1 Activities:: Name: Daniel I. Dialino Section: BSA 3-4Daniel DialinoNo ratings yet

- Midterms Sa2 FARDocument6 pagesMidterms Sa2 FAREloiNo ratings yet

- Tax QuizDocument3 pagesTax QuizLora Mae JuanitoNo ratings yet

- TaxfinDocument3 pagesTaxfinShr BnNo ratings yet

- Corporate LiquidationDocument8 pagesCorporate LiquidationKyo TieNo ratings yet

- Exercises On Estate Tax Additional ProblemsDocument8 pagesExercises On Estate Tax Additional ProblemsMidas Troy VictorNo ratings yet

- Chapter 5 - Estate Tax2013Document12 pagesChapter 5 - Estate Tax2013Anjo Ellis100% (2)

- IGNOU MCA MCS-035 Free Solved Assignments 2010Document11 pagesIGNOU MCA MCS-035 Free Solved Assignments 2010Deepti SainiNo ratings yet

- Corporate Liquidation Problem SolvingDocument21 pagesCorporate Liquidation Problem SolvingRujean Salar AltejarNo ratings yet

- Accounting Special TransactionDocument25 pagesAccounting Special TransactionMarinel Mae ChicaNo ratings yet

- Reviewer Fabm2Document3 pagesReviewer Fabm2Mark LappayNo ratings yet

- Final Income Taxation - Class Discussion (Corrected)Document21 pagesFinal Income Taxation - Class Discussion (Corrected)Christopher SantosNo ratings yet

- Frias Activity 6Document6 pagesFrias Activity 6Lars FriasNo ratings yet

- Chapter 3Document12 pagesChapter 3Briggs Navarro BaguioNo ratings yet

- Cash and Accrual BasisDocument10 pagesCash and Accrual BasisNoeme LansangNo ratings yet

- De Vera Angela Kyle G. Business Taxation Prelim Task 2.1 BSADocument11 pagesDe Vera Angela Kyle G. Business Taxation Prelim Task 2.1 BSAJohn Francis RosasNo ratings yet

- Project Taxation (Ouano)Document16 pagesProject Taxation (Ouano)GuiltyCrownNo ratings yet

- BusCom Practice SetsDocument20 pagesBusCom Practice SetsShaz NagaNo ratings yet

- CTT Answer Season 1Document4 pagesCTT Answer Season 1ucc second yearNo ratings yet

- CTT Answer Season 1Document4 pagesCTT Answer Season 1ucc second yearNo ratings yet

- Income Taxation Answer ExamDocument5 pagesIncome Taxation Answer Examyezaquera100% (1)

- Quiz 3 - CabigonDocument4 pagesQuiz 3 - CabigonRie CabigonNo ratings yet

- 8.2 Assignment - Regular Income Tax For IndividualsDocument8 pages8.2 Assignment - Regular Income Tax For Individualssam imperialNo ratings yet

- Presented by Archana Gupta 0221031 Bharat Gaikwad 0221023Document12 pagesPresented by Archana Gupta 0221031 Bharat Gaikwad 0221023Bharat GaikwadNo ratings yet

- BSMA Taxation of IndividualsDocument32 pagesBSMA Taxation of IndividualsAngela CanayaNo ratings yet

- Toaz - Info 89bf91d5 1612761367237 PRDocument7 pagesToaz - Info 89bf91d5 1612761367237 PRAEHYUN YENVYNo ratings yet

- EstateDocument8 pagesEstateLyka RoguelNo ratings yet

- CABINAS - Partnership Formation & OperationDocument16 pagesCABINAS - Partnership Formation & OperationJoshua CabinasNo ratings yet

- Assignment E & L Env 4 BusiDocument9 pagesAssignment E & L Env 4 BusiSyed Hamza RasheedNo ratings yet

- Non-Resident Foreign CorporationDocument4 pagesNon-Resident Foreign CorporationRosemarie CruzNo ratings yet

- Wealth Management Planning: The UK Tax PrinciplesFrom EverandWealth Management Planning: The UK Tax PrinciplesRating: 4.5 out of 5 stars4.5/5 (2)

- Real Estate Investing 101: Best Way to Buy a House and Save Big, Top 20 TipsFrom EverandReal Estate Investing 101: Best Way to Buy a House and Save Big, Top 20 TipsNo ratings yet

- A Stiptick for a Bleeding Nation: Or, a safe and speedy way to restore publick credit, and pay the national debtsFrom EverandA Stiptick for a Bleeding Nation: Or, a safe and speedy way to restore publick credit, and pay the national debtsNo ratings yet

- Property & Taxation: A Practical Guide to Saving Tax on Your Property InvestmentsFrom EverandProperty & Taxation: A Practical Guide to Saving Tax on Your Property InvestmentsNo ratings yet

- 19697ipcc Acc Vol2 Chapter15Document4 pages19697ipcc Acc Vol2 Chapter15jsus22No ratings yet

- Living-Limitations-And-Challenges-semi-pa-lang-talaga Drawing Near To Final Konti Na Lang Promise EditedDocument91 pagesLiving-Limitations-And-Challenges-semi-pa-lang-talaga Drawing Near To Final Konti Na Lang Promise Editedjsus220% (1)

- Issues in Partnership Accounts: Basic ConceptsDocument40 pagesIssues in Partnership Accounts: Basic Conceptsjsus22No ratings yet

- Profit or Loss Pre and Post Incorporation: Learning ObjectivesDocument20 pagesProfit or Loss Pre and Post Incorporation: Learning Objectivesjsus22No ratings yet

- Purpose of The StudyDocument8 pagesPurpose of The Studyjsus22No ratings yet

- Cat - Module 3.solutions.3.1 To3.4Document11 pagesCat - Module 3.solutions.3.1 To3.4jsus22No ratings yet

- Accounting For Bonus Issue: Learning ObjectivesDocument8 pagesAccounting For Bonus Issue: Learning Objectivesjsus22No ratings yet

- Chapter-1 HSDocument7 pagesChapter-1 HSjsus22No ratings yet

- Philippines Ifrs ProfileDocument6 pagesPhilippines Ifrs Profilejsus22No ratings yet

- Parallax Production Marketing and Sales's Company Policy: 7 Colors PartnershipDocument9 pagesParallax Production Marketing and Sales's Company Policy: 7 Colors Partnershipjsus22No ratings yet

- NOTES On PFRS 9 Financial InstrumentsDocument11 pagesNOTES On PFRS 9 Financial Instrumentsjsus22100% (1)

- Concessionary Card FormDocument2 pagesConcessionary Card Formjsus22No ratings yet

- Basic Package: Monoceros PDocument6 pagesBasic Package: Monoceros Pjsus22No ratings yet

- TAX3Document3 pagesTAX3jsus22No ratings yet

- Resa BL 1st Preboard Jul2014Document7 pagesResa BL 1st Preboard Jul2014EuniceChungNo ratings yet

- RFBT Mcqs New TopicsDocument20 pagesRFBT Mcqs New TopicsjexNo ratings yet

- Court Oft Ax Appeal: DecisionDocument18 pagesCourt Oft Ax Appeal: Decisionjsus22No ratings yet

- Major Quiz #2Document10 pagesMajor Quiz #2jsus22No ratings yet

- Adult Living Donor Liver Transplant: Questions and AnswersDocument36 pagesAdult Living Donor Liver Transplant: Questions and Answersjsus22No ratings yet

- BWR - Jul-Aug - 2016 - BMC 2015 Bottled Water Stat ArticleDocument9 pagesBWR - Jul-Aug - 2016 - BMC 2015 Bottled Water Stat Articlejsus22No ratings yet

- Chanrobles Internet Bar Review: Chanrobles Professional Review, IncDocument13 pagesChanrobles Internet Bar Review: Chanrobles Professional Review, Incjsus22No ratings yet

- Mark-Up Price Product Size Product Cost Per Package Mark-Up Percentage Children's Flavored Drinks Sports and Adventure Drinking WaterDocument2 pagesMark-Up Price Product Size Product Cost Per Package Mark-Up Percentage Children's Flavored Drinks Sports and Adventure Drinking Waterjsus22No ratings yet

- Hci Acc Web December 31 2016-1Document52 pagesHci Acc Web December 31 2016-1Joseph FranciscoNo ratings yet

- GFFS General-Form Rev-20061Document14 pagesGFFS General-Form Rev-20061Judy Ann GacetaNo ratings yet

- Lesson 3 Module 3 Lec - Data Security AwarenessDocument16 pagesLesson 3 Module 3 Lec - Data Security AwarenessJenica Mae SaludesNo ratings yet

- Economics of PiggeryDocument3 pagesEconomics of Piggerysrujan NJNo ratings yet

- Health and Physical Education ThesisDocument35 pagesHealth and Physical Education ThesisZia IslamNo ratings yet

- Gurrea V LezamaDocument2 pagesGurrea V LezamaEdward Kenneth Kung100% (1)

- Two Versions PDFDocument70 pagesTwo Versions PDFkamilghoshalNo ratings yet

- ED Hiring GuideDocument20 pagesED Hiring Guidechokx008No ratings yet

- M B ADocument98 pagesM B AGopuNo ratings yet

- Nta (Ugc-Net) : Ask, Learn & LeadDocument18 pagesNta (Ugc-Net) : Ask, Learn & LeadprajwalbhatNo ratings yet

- Psychiatric Nursing NotesDocument13 pagesPsychiatric Nursing NotesCarlo VigoNo ratings yet

- 2023 California Model Year 1978 or Older Light-Duty Vehicle SurveyDocument10 pages2023 California Model Year 1978 or Older Light-Duty Vehicle SurveyNick PopeNo ratings yet

- Fouts Def 2nd Production of DocumentsDocument88 pagesFouts Def 2nd Production of Documentswolf woodNo ratings yet

- Ba311 - Module 5 Capacity ManagementDocument10 pagesBa311 - Module 5 Capacity ManagementShams PeloperoNo ratings yet

- Ee NewDocument1 pageEe Newhsbibahmed091No ratings yet

- Laundry and Bourbon AnalysisDocument2 pagesLaundry and Bourbon AnalysisAveryNo ratings yet

- ThesisDocument5 pagesThesisSampayan Angelica A.No ratings yet

- The FATF Recommendations On Combating Money Laundering and The Financing of Terrorism & ProliferationDocument27 pagesThe FATF Recommendations On Combating Money Laundering and The Financing of Terrorism & ProliferationAli SaeedNo ratings yet

- Weekly Report w34Document19 pagesWeekly Report w34Asep MAkmurNo ratings yet

- Rishika Dass: Growth and Importance of MSMEDocument2 pagesRishika Dass: Growth and Importance of MSMEagantook2607No ratings yet

- Week 1, Hebrews 1:1-14 HookDocument9 pagesWeek 1, Hebrews 1:1-14 HookDawit ShankoNo ratings yet

- Review of ApplicationDocument6 pagesReview of ApplicationPrabath ChinthakaNo ratings yet

- Copia de The Green Banana Lecturas I 2020Document4 pagesCopia de The Green Banana Lecturas I 2020Finn SolórzanoNo ratings yet

- 31-07-2020 - The Hindu Handwritten NotesDocument16 pages31-07-2020 - The Hindu Handwritten NotesnishuNo ratings yet

- Corpse Grinder Cult Lijst - 1.2Document4 pagesCorpse Grinder Cult Lijst - 1.2Jimmy CarterNo ratings yet

- 2 - AC Corporation (ACC) v. CIRDocument20 pages2 - AC Corporation (ACC) v. CIRCarlota VillaromanNo ratings yet

- SP 70Document75 pagesSP 70Barbie Turic100% (2)

- Equatorial Realty Vs Mayfair TheaterDocument2 pagesEquatorial Realty Vs Mayfair TheaterSaji Jimeno100% (1)

- Memorial For The Appellants-Team Code L PDFDocument44 pagesMemorial For The Appellants-Team Code L PDFAbhineet KaliaNo ratings yet