Download as pdf or txt

You might also like

- Tally ERP 9 (Power Of Simplicity): Software for business & accountsFrom EverandTally ERP 9 (Power Of Simplicity): Software for business & accountsRating: 5 out of 5 stars5/5 (3)

- Itinerary J4W9XF PDFDocument2 pagesItinerary J4W9XF PDFWahyu Bin Djalal100% (4)

- A Complete Practice Book Tally 9Document19 pagesA Complete Practice Book Tally 9bagsourav100% (5)

- Tally ERP 9 Notes + Practical Assignment - Free Download PDFDocument19 pagesTally ERP 9 Notes + Practical Assignment - Free Download PDFHimanshu Saha67% (3)

- Tally Erp.9: M.S.N.Durga PrasadDocument91 pagesTally Erp.9: M.S.N.Durga PrasadMsme-tdc Meerut100% (1)

- VAT ReviewerDocument11 pagesVAT ReviewerMarianne Agunoy100% (1)

- Tally GURU Syllabus PDFDocument2 pagesTally GURU Syllabus PDFWedsa Kumari50% (2)

- Tally AssignmentDocument90 pagesTally AssignmentM Keerthana100% (1)

- Tally Erp 9 Coplete TheoryDocument94 pagesTally Erp 9 Coplete Theorytuntun yadavNo ratings yet

- Tally - ERP9 Book With GSTDocument1,843 pagesTally - ERP9 Book With GSThatim100% (1)

- All Semesters Pages 47 65Document19 pagesAll Semesters Pages 47 65rpraveenkumarreddyNo ratings yet

- YCI Tally NotesDocument85 pagesYCI Tally NoteshxjdyufjNo ratings yet

- Tally ERP 2017-18 - Basic LevelDocument44 pagesTally ERP 2017-18 - Basic LevelAnonymous 3yqNzCxtTz100% (1)

- Tally Assignment AfrozDocument17 pagesTally Assignment AfrozAfrozNo ratings yet

- Personal Loan EMI Accounting Entry in Tally PrimeDocument17 pagesPersonal Loan EMI Accounting Entry in Tally PrimeVansh Gusai0% (1)

- Tally AssignmentDocument90 pagesTally AssignmentASHOK RAJ100% (2)

- Interest Calculation in Tally Erp9Document9 pagesInterest Calculation in Tally Erp9Michael Wells0% (1)

- Tally PDFDocument185 pagesTally PDFArunNo ratings yet

- Tally Exercise 5Document1 pageTally Exercise 5ArunNo ratings yet

- Tally Test Paper 1Document16 pagesTally Test Paper 1lalwaniashok77% (39)

- Tally - Erp 9 Complete CourseDocument12 pagesTally - Erp 9 Complete CourseMeghaNo ratings yet

- Tally Erp9 EnglisheditionDocument31 pagesTally Erp9 Englisheditionapi-262072056No ratings yet

- Accounting Question: (Tally)Document9 pagesAccounting Question: (Tally)prempankaj7788% (17)

- Tally ExerciseDocument16 pagesTally ExercisePavanSyamsundarNo ratings yet

- Tally 9 AssignmentDocument49 pagesTally 9 AssignmentmayankNo ratings yet

- Tally Exercise 3Document1 pageTally Exercise 3Arun0% (1)

- Tally AssignmentDocument22 pagesTally AssignmentRahul Aggarwal64% (11)

- Practice Questions of TallyDocument18 pagesPractice Questions of TallyVISHAL100% (2)

- Tally Coaching FileDocument7 pagesTally Coaching FileG Subramaniam92% (26)

- TallyDocument172 pagesTallyEzhil Kumar100% (1)

- Multi Currency in TallyDocument10 pagesMulti Currency in TallyMahendra50% (2)

- Tally ExerciseDocument16 pagesTally Exercisesbnikte73% (11)

- Tally New NotesDocument308 pagesTally New NotesAMIN BUHARI ABDUL KHADER79% (14)

- Tally TestDocument2 pagesTally TestHK DuggalNo ratings yet

- Tally Prime Budget Management For BusinessesDocument12 pagesTally Prime Budget Management For BusinessesVansh GusaiNo ratings yet

- Tally - Erp 9 NotesDocument340 pagesTally - Erp 9 NotesSaishankar Vemuri100% (3)

- Tally Business Entry ExericiseDocument1 pageTally Business Entry ExericiseVinay Kumar82% (28)

- Tally NotesDocument5 pagesTally NotesAMIN BUHARI ABDUL KHADER100% (1)

- Tally 9 NotesDocument17 pagesTally 9 NotesAnjali HemadeNo ratings yet

- Tally Prime NotesDocument54 pagesTally Prime Notesroshandhamankar0100% (3)

- Tally Assignment BookDocument30 pagesTally Assignment BookArun Babu100% (14)

- Tally NotesDocument33 pagesTally NotesShilpi RaiNo ratings yet

- Tally Questions Zero Value, Billed and Actual Quantity PDFDocument4 pagesTally Questions Zero Value, Billed and Actual Quantity PDFAjitesh anandNo ratings yet

- Tally With GST Workshop Jan 2023 QuestionDocument3 pagesTally With GST Workshop Jan 2023 QuestionAryan GuptaNo ratings yet

- Case Study 3 Tally Prime ExerciseDocument10 pagesCase Study 3 Tally Prime ExerciseBishal Saha100% (1)

- T.D.S. Assignment: Match The Following:-CASH .. 1,01,950 SBI 37,550Document2 pagesT.D.S. Assignment: Match The Following:-CASH .. 1,01,950 SBI 37,550Reema Kumari67% (3)

- Order Processing Exercise 1Document2 pagesOrder Processing Exercise 1AnbarasanNo ratings yet

- Tally Exercise 6Document1 pageTally Exercise 6Arun100% (1)

- Universal Tally Note 2074&m18Document56 pagesUniversal Tally Note 2074&m18universal academy100% (6)

- Tally Prime Question Paper TP001Document1 pageTally Prime Question Paper TP001AnuragNo ratings yet

- Official Guide to Financial Accounting using TallyPrime: Managing your Business Just Got SimplerFrom EverandOfficial Guide to Financial Accounting using TallyPrime: Managing your Business Just Got SimplerNo ratings yet

- CAS Tally TRAINING MaterialDocument39 pagesCAS Tally TRAINING MaterialTesfa HunderaNo ratings yet

- Audit of Financial StatementDocument23 pagesAudit of Financial StatementGurpreet KaurNo ratings yet

- Fundamentals 02 Accounting Interview QuestionsDocument37 pagesFundamentals 02 Accounting Interview Questionsnatalia.velianoskiNo ratings yet

- Guidelines For Conducting Revenue Audit of PSPCLDocument48 pagesGuidelines For Conducting Revenue Audit of PSPCLsahil rohitNo ratings yet

- Notes On Chapter 7: 7.1 Purposes of The Trading and Profit and Loss AccountDocument3 pagesNotes On Chapter 7: 7.1 Purposes of The Trading and Profit and Loss AccountPriya SunderNo ratings yet

- Profit and Loss (P&L) : Definition - What Does Mean?Document2 pagesProfit and Loss (P&L) : Definition - What Does Mean?Divyang BhattNo ratings yet

- IE132 Financial AccountingDocument8 pagesIE132 Financial AccountingAndrea Padilla MoralesNo ratings yet

- Bookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursFrom EverandBookkeeping And Accountancy Made Simple: For Owner Managed Businesses, Students And Young EntrepreneursNo ratings yet

- Rec 3Document12 pagesRec 3Ahmed AltohamyNo ratings yet

- Project TallyDocument12 pagesProject Tallygau2910No ratings yet

- Practice2 PDFDocument8 pagesPractice2 PDFKingg2009No ratings yet

- VoucherDocument38 pagesVoucherKingg2009No ratings yet

- Dealer Dealerlist - Do Mapimage.x 170Document1 pageDealer Dealerlist - Do Mapimage.x 170Kingg2009No ratings yet

- Device Settings - South Zone: 1. Portal SettingDocument4 pagesDevice Settings - South Zone: 1. Portal SettingKingg2009No ratings yet

- 02Document1 page02Rozina TabassumNo ratings yet

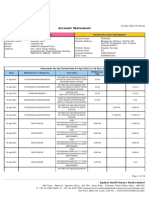

- Account StatementDocument77 pagesAccount StatementBASHA SHAFIQNo ratings yet

- UAB Aug 24-Oct 02,2011Document2 pagesUAB Aug 24-Oct 02,2011Danngee XeyNo ratings yet

- Transfer ConfirmationDocument3 pagesTransfer Confirmationme NaderNo ratings yet

- 2020-04-23 0012724719 590.00 PDFDocument1 page2020-04-23 0012724719 590.00 PDFAnjan MondalNo ratings yet

- Week1 - Electronic CommerceDocument3 pagesWeek1 - Electronic CommerceMary Joy Emjhay BanalNo ratings yet

- American ExpressDocument2 pagesAmerican Expressshankesh singhNo ratings yet

- 2024 03 29 12 28 15dec 23 - 201102Document6 pages2024 03 29 12 28 15dec 23 - 201102zamirsaifi613No ratings yet

- Statement 1690874707502Document10 pagesStatement 1690874707502Tarang ShandilyaNo ratings yet

- UE Online Registration 2Document2 pagesUE Online Registration 2Jovcel ObcenaNo ratings yet

- Proceeding IMOPH 2016Document8 pagesProceeding IMOPH 2016drgrizahNo ratings yet

- Austin Goh Jun de - 1358Document2 pagesAustin Goh Jun de - 1358Austin GohNo ratings yet

- Export Financing BBLC IFDBC PCDocument22 pagesExport Financing BBLC IFDBC PCrajmirakshan100% (1)

- TM HDMF June 2019Document620 pagesTM HDMF June 2019Wendelle Mayo DomingcilNo ratings yet

- 20180523153227XXXXXXX3302 PDFDocument1 page20180523153227XXXXXXX3302 PDFUMESH KUMAR YadavNo ratings yet

- Jaipur District Development Plan Transportation: Aashka ShahDocument9 pagesJaipur District Development Plan Transportation: Aashka ShahAashka ShahNo ratings yet

- Revised CA Product PDFDocument3 pagesRevised CA Product PDFm.khurana093425No ratings yet

- Report On Fintech: in Context of NepalDocument9 pagesReport On Fintech: in Context of Nepalankur wagleNo ratings yet

- 1621 Jan 2019 FinalDocument2 pages1621 Jan 2019 FinaljomarNo ratings yet

- FintechDocument95 pagesFintechSagar KansalNo ratings yet

- Test Reconciliation Grade 11Document6 pagesTest Reconciliation Grade 11Stars2323100% (2)

- Stop Payment RequestDocument5 pagesStop Payment RequestNaveed AliNo ratings yet

- ACC-305 Week 3 - P7-10 P7-14Document7 pagesACC-305 Week 3 - P7-10 P7-14Shaikh GufranNo ratings yet

- Tax Invoice: Advance Receipt Voucher NoDocument1 pageTax Invoice: Advance Receipt Voucher NoNikhilNo ratings yet

- Finnish TaxationDocument217 pagesFinnish TaxationTobi MemoryNo ratings yet

- The Air Cargo Agents Association of India: AcaaiDocument8 pagesThe Air Cargo Agents Association of India: AcaaiDevasyruc0% (1)

- Indian Income Tax Return Acknowledgement 2021-22: Assessment YearDocument1 pageIndian Income Tax Return Acknowledgement 2021-22: Assessment YearImtiaz SkNo ratings yet

- Account Statement: Customer Information Branch/Account InformationDocument12 pagesAccount Statement: Customer Information Branch/Account InformationRohit kumarNo ratings yet