Download as docx, pdf, or txt

You might also like

- Capital MarketDocument32 pagesCapital MarketAppan Kandala Vasudevachary80% (5)

- Effectiveness of Running A SariDocument32 pagesEffectiveness of Running A Sari[AP-STUDENT] April Mae PeñaflorNo ratings yet

- Oblicon Compiled CasesDocument314 pagesOblicon Compiled CasesKenn Rhyan Misoles100% (2)

- Chapter 22 Real Options: Corporate Finance, 3E (Berk/Demarzo)Document27 pagesChapter 22 Real Options: Corporate Finance, 3E (Berk/Demarzo)asdfghjkl007No ratings yet

- Indian Institute of Banking & Finance: Risk ManagementDocument53 pagesIndian Institute of Banking & Finance: Risk Managementnaseemdgr8No ratings yet

- Biitm-IFSS-Notes Module 2 - SBMDocument33 pagesBiitm-IFSS-Notes Module 2 - SBMshubham kumarNo ratings yet

- Financial Markets: Money MarketDocument13 pagesFinancial Markets: Money MarketRisha RoyNo ratings yet

- Debt Markets: Government Bonds T-Bills State Government Bonds Call Money Markets Corporate DebtDocument33 pagesDebt Markets: Government Bonds T-Bills State Government Bonds Call Money Markets Corporate DebtSwati JainNo ratings yet

- Indian Institute of Banking & FinanceDocument51 pagesIndian Institute of Banking & FinanceAnkita AgarwalNo ratings yet

- Money Market & InstrumentsDocument40 pagesMoney Market & InstrumentssujithchandrasekharaNo ratings yet

- Indian Institute of Banking & FinanceDocument53 pagesIndian Institute of Banking & FinanceDipti DalviNo ratings yet

- Basics of Indian Money MarketDocument26 pagesBasics of Indian Money MarketAmeya BhagatNo ratings yet

- Call Money Market and Money Market InstrumentsDocument7 pagesCall Money Market and Money Market Instrumentsvivekagrawal0783% (6)

- The Indian Money Market: Prime AcademyDocument5 pagesThe Indian Money Market: Prime AcademyHardik KharaNo ratings yet

- Constituents of A Financial SystemDocument4 pagesConstituents of A Financial SystemDil Shyam D KNo ratings yet

- Indian Financial System: by ChhoteDocument37 pagesIndian Financial System: by Chhotechhote999No ratings yet

- Money MarketDocument20 pagesMoney Marketmanisha guptaNo ratings yet

- Definition of Money MarketDocument17 pagesDefinition of Money MarketSmurti Rekha JamesNo ratings yet

- Caiib Risk Manage Mod CDDocument95 pagesCaiib Risk Manage Mod CDMusahib ChaudhariNo ratings yet

- Treasury BillsDocument11 pagesTreasury Billsjigna kelaNo ratings yet

- Primary Market: Prepared By: Rajesh KiriDocument30 pagesPrimary Market: Prepared By: Rajesh Kirinilampatel_mbaNo ratings yet

- Meaning of A Balance Sheet of A Bank: 2) Liabilities of The Commercial BanksDocument4 pagesMeaning of A Balance Sheet of A Bank: 2) Liabilities of The Commercial BanksShilpan ShahNo ratings yet

- The Securities and ExchangeDocument22 pagesThe Securities and ExchangeHappy AnthalNo ratings yet

- Stock MarketDocument26 pagesStock MarketBalajiNo ratings yet

- Stryker Corporation: Capital BudgetingDocument4 pagesStryker Corporation: Capital BudgetingShakthi RaghaviNo ratings yet

- Treasury & Risk Management: Post Graduate Diploma in Management (ePGDM)Document12 pagesTreasury & Risk Management: Post Graduate Diploma in Management (ePGDM)Jitendra YadavNo ratings yet

- 205FIN FMBO Unit-2 Money MarketDocument43 pages205FIN FMBO Unit-2 Money MarketTejaswini BuddhisagarNo ratings yet

- Money MktsDocument55 pagesMoney MktsKaranSinghNo ratings yet

- Listing Guidelines at BseDocument7 pagesListing Guidelines at Bseakp786No ratings yet

- Money Market Numerical ExamplesDocument14 pagesMoney Market Numerical ExamplesgauravNo ratings yet

- Money Market InstrumentsDocument9 pagesMoney Market InstrumentsJaanish JanNo ratings yet

- Money MarketsDocument30 pagesMoney MarketsAshwin JacobNo ratings yet

- Listing RequirementsDocument5 pagesListing Requirementsnidhiash1989No ratings yet

- Financial Markets and ServicesDocument71 pagesFinancial Markets and ServicesMohammed ImranNo ratings yet

- Guidelines For Listing: ChecklistDocument6 pagesGuidelines For Listing: ChecklistParag MogarkarNo ratings yet

- Commercial Paper MKTDocument29 pagesCommercial Paper MKTmohamedsafwan0480No ratings yet

- Ans 1) The Reserve Bank of India (RBI) Uses Credit Control As A Monetary Policy Tool ToDocument9 pagesAns 1) The Reserve Bank of India (RBI) Uses Credit Control As A Monetary Policy Tool ToSHAILLY SHARMANo ratings yet

- Law NotesDocument19 pagesLaw NotesPranavNo ratings yet

- Introduction To Financial Markets 2022Document17 pagesIntroduction To Financial Markets 2022djroytatanNo ratings yet

- Unit 1Document64 pagesUnit 1Suneel KumarNo ratings yet

- What Are The Money Market Instruments in PakistanDocument2 pagesWhat Are The Money Market Instruments in PakistanWajiah Rahat100% (2)

- Scheduled Banks in India:: Market Segments of Money Market in India AreDocument4 pagesScheduled Banks in India:: Market Segments of Money Market in India AreTaltson SunnyNo ratings yet

- Draft Debt SecuritiesDocument21 pagesDraft Debt SecuritiesFaisal AliNo ratings yet

- Kousali Institute of Management Studies: MBA Assignment 2020-2022Document7 pagesKousali Institute of Management Studies: MBA Assignment 2020-2022Bhavani BhajantriNo ratings yet

- Financial Institution and MarketsDocument6 pagesFinancial Institution and MarketsSolve AssignmentNo ratings yet

- Chapter 19 - Money MarketDocument7 pagesChapter 19 - Money MarketDammar JoshiNo ratings yet

- Money Market Instruments Project ReportDocument17 pagesMoney Market Instruments Project ReportPratik Walve0% (1)

- Commercial PaperDocument12 pagesCommercial Paperjaideep92naikNo ratings yet

- Merchant Banking and Financial Services Two Marks Questions and AnswersDocument8 pagesMerchant Banking and Financial Services Two Marks Questions and AnswersadammurugeshNo ratings yet

- Ge AssignmentDocument9 pagesGe AssignmentNidhuNo ratings yet

- Understanding - Money MarketDocument39 pagesUnderstanding - Money MarketaartipujariNo ratings yet

- Capital Markets OverviewDocument32 pagesCapital Markets OverviewVamsi Krishna YNNo ratings yet

- Money Market and Types of Money Market InstrumentsDocument6 pagesMoney Market and Types of Money Market InstrumentsWasimAkramNo ratings yet

- MF0016 B1814 SLM Unit 02 PDFDocument18 pagesMF0016 B1814 SLM Unit 02 PDFBinnatPatelNo ratings yet

- B&I Unit 3Document14 pagesB&I Unit 3saisri nagamallaNo ratings yet

- Presented By: Divya Sharma M.B.A. Iv-Sem JietsomgDocument30 pagesPresented By: Divya Sharma M.B.A. Iv-Sem Jietsomglakshmimadhu2005No ratings yet

- Research Assignment of FmiDocument11 pagesResearch Assignment of FmiAnshita GargNo ratings yet

- A Practical Approach to the Study of Indian Capital MarketsFrom EverandA Practical Approach to the Study of Indian Capital MarketsNo ratings yet

- Summary of Philip J. Romero & Tucker Balch's What Hedge Funds Really DoFrom EverandSummary of Philip J. Romero & Tucker Balch's What Hedge Funds Really DoNo ratings yet

- Equity Investment for CFA level 1: CFA level 1, #2From EverandEquity Investment for CFA level 1: CFA level 1, #2Rating: 5 out of 5 stars5/5 (1)

- Bank Fundamentals: An Introduction to the World of Finance and BankingFrom EverandBank Fundamentals: An Introduction to the World of Finance and BankingRating: 4.5 out of 5 stars4.5/5 (4)

- Financial Markets Fundamentals: Why, how and what Products are traded on Financial Markets. Understand the Emotions that drive TradingFrom EverandFinancial Markets Fundamentals: Why, how and what Products are traded on Financial Markets. Understand the Emotions that drive TradingNo ratings yet

- Saldana vs. Phil. GuarantyDocument1 pageSaldana vs. Phil. GuarantyKeilah ArguellesNo ratings yet

- Divorce Deals Webinar - HandoutDocument18 pagesDivorce Deals Webinar - HandoutlonghornsteveNo ratings yet

- Chapter Exam - Partnership Formation - 1Document12 pagesChapter Exam - Partnership Formation - 1NarikoNo ratings yet

- Topic 5: International Lending and Portfolio ManagementDocument29 pagesTopic 5: International Lending and Portfolio ManagementSanthiya MogenNo ratings yet

- Lobrigas Unit5 Topic4 AssessmentDocument5 pagesLobrigas Unit5 Topic4 AssessmentClaudine LobrigasNo ratings yet

- 2023 Industry ReportDocument72 pages2023 Industry ReportJeremy Burns100% (1)

- Characteristic Features of Financial InstrumentsDocument17 pagesCharacteristic Features of Financial Instrumentsmanoranjanpatra93% (15)

- Debt ManagementDocument55 pagesDebt ManagementAh MhiNo ratings yet

- NCR Negosale Batch 15138 100322 CompressedDocument37 pagesNCR Negosale Batch 15138 100322 CompressedNica ReyesNo ratings yet

- Credit PolicyDocument10 pagesCredit PolicyAyesha KhanNo ratings yet

- Maceda and Condo ActDocument4 pagesMaceda and Condo ActAngel Chane OstrazNo ratings yet

- Unit 4Document24 pagesUnit 4Prashan PatilNo ratings yet

- Characteristics of Floating ChargeDocument4 pagesCharacteristics of Floating ChargeNg GraceNo ratings yet

- Financial Statements AnalysisDocument58 pagesFinancial Statements AnalysisenkeltvrelseNo ratings yet

- Cavite Development Bank v. Spouses Lim Et. Al.Document8 pagesCavite Development Bank v. Spouses Lim Et. Al.jagabriel616No ratings yet

- Fmi CH4Document10 pagesFmi CH4Khalid MuhammadNo ratings yet

- The Oxford Handbook of Banking 3nbsped 0198824637 9780198824633Document1,309 pagesThe Oxford Handbook of Banking 3nbsped 0198824637 9780198824633cyvhjbNo ratings yet

- Saunders 8e PPT Chapter05Document33 pagesSaunders 8e PPT Chapter05sdgdfs sdfsfNo ratings yet

- Cagayan Fishing Devt Vs SandikoDocument2 pagesCagayan Fishing Devt Vs SandikoAmanda ButtkissNo ratings yet

- Chapter 12 The Bond MarketDocument7 pagesChapter 12 The Bond Marketlasha KachkachishviliNo ratings yet

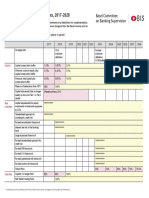

- Basel III Transitional Arrangements, 2017-2028: Basel Committee On Banking SupervisionDocument1 pageBasel III Transitional Arrangements, 2017-2028: Basel Committee On Banking SupervisiongoonNo ratings yet

- Portfolio TutoDocument50 pagesPortfolio TutoLim XiaopeiNo ratings yet

- FinQuiz - Curriculum Note, Study Session 4, Reading 11Document16 pagesFinQuiz - Curriculum Note, Study Session 4, Reading 11Jacek KowalskiNo ratings yet

- MGT604 Mega File For Quizes Finalterm PapersDocument34 pagesMGT604 Mega File For Quizes Finalterm PapersAbdul JabbarNo ratings yet

- A Study On Credit Risk Management at HDFC BankDocument58 pagesA Study On Credit Risk Management at HDFC BankRajesh BathulaNo ratings yet

- M06 Brooks266675 01 FM C06Document63 pagesM06 Brooks266675 01 FM C06Mubashar NawazNo ratings yet

- Anahuac University Mexico: Finance For Economists 10373 Professor Gilberto Escobedo AragonesDocument13 pagesAnahuac University Mexico: Finance For Economists 10373 Professor Gilberto Escobedo AragonesIngrid ReyesNo ratings yet