Download as docx, pdf, or txt

You might also like

- CIR V BursmeitersDocument1 pageCIR V Bursmeiterskim zeus ga-anNo ratings yet

- NPC V Sps SaludaresDocument1 pageNPC V Sps SaludaresDiane Dee YaneeNo ratings yet

- Sample Crim Law Bar Qs MCQDocument9 pagesSample Crim Law Bar Qs MCQDiane Dee YaneeNo ratings yet

- Ericsson Telecommunication vs. City of Pasig GR No. 176667, November 22. 2007Document2 pagesEricsson Telecommunication vs. City of Pasig GR No. 176667, November 22. 2007Pilyang SweetNo ratings yet

- Excise TaxesDocument5 pagesExcise TaxesJoAnne Yaptinchay Claudio100% (2)

- Philippine Bank of Communications vs. Commissioner of Internal Revenue (GR 112024. Jan. 28, 1999)Document2 pagesPhilippine Bank of Communications vs. Commissioner of Internal Revenue (GR 112024. Jan. 28, 1999)Col. McCoyNo ratings yet

- BIR vs. CA and Sps. Antonio Manly and Ruby ManlyDocument16 pagesBIR vs. CA and Sps. Antonio Manly and Ruby Manlyred gynNo ratings yet

- CIR Vs CTA and PetronDocument3 pagesCIR Vs CTA and PetronQuennieNo ratings yet

- DIGEST - FISHWEALTH CANNING CORPORATION Vs CIRDocument1 pageDIGEST - FISHWEALTH CANNING CORPORATION Vs CIRArthur Sy100% (1)

- CIR V Castaneda DigestDocument1 pageCIR V Castaneda DigestKTNo ratings yet

- CIR v. Tulio (Digest by Madz)Document3 pagesCIR v. Tulio (Digest by Madz)madzarellaNo ratings yet

- CIR Vs Commonwealth ManagementDocument3 pagesCIR Vs Commonwealth ManagementGoody100% (1)

- Basilan Estates Vs Cir (1967)Document7 pagesBasilan Estates Vs Cir (1967)RavenFoxNo ratings yet

- 04 City of San Pablo Vs ReyesDocument2 pages04 City of San Pablo Vs Reyesdos2reqjNo ratings yet

- CIR Vs SuyocDocument1 pageCIR Vs SuyocArnold JoseNo ratings yet

- IPL - Oct 20Document14 pagesIPL - Oct 20Triccie MangueraNo ratings yet

- 2017 Bar Notes in LTD PDFDocument12 pages2017 Bar Notes in LTD PDFHiroshi CarlosNo ratings yet

- Philhealth Care vs. CIR, 554 SCRA 411Document22 pagesPhilhealth Care vs. CIR, 554 SCRA 411KidMonkey2299No ratings yet

- CITY OF MANILA vs. COCA-COLA BOTTLERS PHILIPPINES, INCDocument2 pagesCITY OF MANILA vs. COCA-COLA BOTTLERS PHILIPPINES, INCEmil BautistaNo ratings yet

- 193 SCRA 132 (1991) : Ute Paterok vs. Bureau of CustomsDocument1 page193 SCRA 132 (1991) : Ute Paterok vs. Bureau of CustomsFrances BautistaNo ratings yet

- Commissioner of Internal Revenue vs. Philex Mining Corporation G.R. No. 218057 January 18, 2021Document5 pagesCommissioner of Internal Revenue vs. Philex Mining Corporation G.R. No. 218057 January 18, 2021Mae CalderonNo ratings yet

- 2 Bagunu v. Piedad, 347 Scra 571 (2000)Document2 pages2 Bagunu v. Piedad, 347 Scra 571 (2000)RICHIE SALUBRENo ratings yet

- Chua Specpro ReviewerDocument66 pagesChua Specpro Reviewereppieseverino5No ratings yet

- China Banking Corporation Vs CIRDocument3 pagesChina Banking Corporation Vs CIRMiaNo ratings yet

- City of Lapu Lapu V PEZADocument3 pagesCity of Lapu Lapu V PEZAjuan aldabaNo ratings yet

- Republic Vs AcebedoDocument2 pagesRepublic Vs AcebedoMaria Raisa Helga YsaacNo ratings yet

- Tax 1 Cases On Allowable DeductionsDocument45 pagesTax 1 Cases On Allowable DeductionsREJFREEFALLNo ratings yet

- Meralco Vs Savellano, 117 SCRA 804Document2 pagesMeralco Vs Savellano, 117 SCRA 804katentom-1No ratings yet

- Maceda V. Macaraig Summary: The Petition Seeks To Nullify Certain Decisions, Orders, Rulings, and ResolutionsDocument3 pagesMaceda V. Macaraig Summary: The Petition Seeks To Nullify Certain Decisions, Orders, Rulings, and ResolutionsTrixie PeraltaNo ratings yet

- Cir vs. St. LukeDocument26 pagesCir vs. St. LukeJAMNo ratings yet

- Tax2 Cases DigestedDocument16 pagesTax2 Cases DigestedCharidee LumpasNo ratings yet

- Property Compilation of Case Digests 1.Document34 pagesProperty Compilation of Case Digests 1.marc molinaNo ratings yet

- Taxation CasesDocument94 pagesTaxation CasesMichael jay sarmientoNo ratings yet

- Cyanamid Phil V CIRDocument1 pageCyanamid Phil V CIRAnonymous MikI28PkJcNo ratings yet

- 02 Manila Banking Corporation v. CIRDocument2 pages02 Manila Banking Corporation v. CIRCheska VergaraNo ratings yet

- Air Canada vs. Cir, G. R. No. 169507 (2016 J. Leonen)Document1 pageAir Canada vs. Cir, G. R. No. 169507 (2016 J. Leonen)Y P Dela PeñaNo ratings yet

- Dermaline IncDocument1 pageDermaline IncJohn Amador MalanaNo ratings yet

- AMAL Answer To Action For Rescission of Contracts Bedial PDFDocument4 pagesAMAL Answer To Action For Rescission of Contracts Bedial PDFشزغتحزع ىطشفم لشجخبهNo ratings yet

- Rules On Special ProcedureDocument107 pagesRules On Special ProcedurePaolo_00No ratings yet

- Director of Lands v. IAC, 219 SCRA 339Document4 pagesDirector of Lands v. IAC, 219 SCRA 339FranzMordenoNo ratings yet

- CIR Vs MarubeniDocument1 pageCIR Vs MarubeniMon DreykNo ratings yet

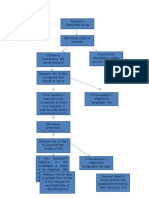

- Flowchart of Tax RemediesDocument3 pagesFlowchart of Tax RemediesJunivenReyUmadhayNo ratings yet

- CIR V CADocument2 pagesCIR V CAAlan GultiaNo ratings yet

- KHO Vs CA 2002Document2 pagesKHO Vs CA 2002Kacel CastroNo ratings yet

- CIR V United Salvage and TowageDocument1 pageCIR V United Salvage and TowageMarc VirtucioNo ratings yet

- Commissioner of Internal Revenue v. Unioil Corp., G.R. No. 204405, (August 4, 2021)Document23 pagesCommissioner of Internal Revenue v. Unioil Corp., G.R. No. 204405, (August 4, 2021)Kriszan ManiponNo ratings yet

- 027 CIR Vs BOACDocument2 pages027 CIR Vs BOACMiw CortesNo ratings yet

- Transglobe V CADocument1 pageTransglobe V CAIan AuroNo ratings yet

- CIR Vs Estate of Benigno TodaDocument18 pagesCIR Vs Estate of Benigno TodaPia Christine BungubungNo ratings yet

- TAXATION II-case DigestDocument54 pagesTAXATION II-case Digestleo.rosarioNo ratings yet

- City of Manila vs. Hon CaridadDocument2 pagesCity of Manila vs. Hon CaridadkelbingeNo ratings yet

- Phil. Home Assurance Corp vs. CADocument1 pagePhil. Home Assurance Corp vs. CACaroline A. LegaspinoNo ratings yet

- City of Manila v. Grecia CuerdoDocument1 pageCity of Manila v. Grecia CuerdoRostum AgapitoNo ratings yet

- Bedan Red Book (2020 - 21) - 04. Taxation LawDocument134 pagesBedan Red Book (2020 - 21) - 04. Taxation LawSGNo ratings yet

- City of Manila vs. Hon. Caridad Grecia-Cuerdo, RTC Pasay Et AlDocument6 pagesCity of Manila vs. Hon. Caridad Grecia-Cuerdo, RTC Pasay Et AlAP CruzNo ratings yet

- Digested CasesDocument36 pagesDigested CasesJepoy Nisperos ReyesNo ratings yet

- 24 Marubeni v. CIRDocument2 pages24 Marubeni v. CIRRem SerranoNo ratings yet

- CIR Vs Sony PhilDocument1 pageCIR Vs Sony PhilJazem Ansama100% (3)

- Commissioner of Internal Revenue Vs Tours SpecialistsDocument10 pagesCommissioner of Internal Revenue Vs Tours SpecialistsVincent OngNo ratings yet

- Power Sector v. CIR GR No. 198146 Dated August 08, 2017Document4 pagesPower Sector v. CIR GR No. 198146 Dated August 08, 2017Vel JuneNo ratings yet

- Part D - Focus CasesDocument22 pagesPart D - Focus CasesShalom MangalindanNo ratings yet

- Blank 8Document11 pagesBlank 8Stephen Celoso EscartinNo ratings yet

- Affidavit of LossDocument1 pageAffidavit of LossDiane Dee YaneeNo ratings yet

- Lite Refuses or Fails To Do So, Any Third Person WhoDocument7 pagesLite Refuses or Fails To Do So, Any Third Person WhoDiane Dee YaneeNo ratings yet

- RCBC vs. SERRA2Document3 pagesRCBC vs. SERRA2Diane Dee YaneeNo ratings yet

- Re Letter of The Up Law Faculty Entitled Restoring IntegrityDocument4 pagesRe Letter of The Up Law Faculty Entitled Restoring IntegrityDiane Dee YaneeNo ratings yet

- Adoption ResearchDocument1 pageAdoption ResearchDiane Dee YaneeNo ratings yet

- RCBC vs. SerraDocument2 pagesRCBC vs. SerraDiane Dee YaneeNo ratings yet

- Rizal Commercial Banking Corporation vs. Federico A. SerraDocument2 pagesRizal Commercial Banking Corporation vs. Federico A. SerraDiane Dee YaneeNo ratings yet

- Rizal Commercial Banking Corporation vs. Federico A. SerraDocument2 pagesRizal Commercial Banking Corporation vs. Federico A. SerraDiane Dee YaneeNo ratings yet

- Municipality of Biñan vs. GarciaDocument1 pageMunicipality of Biñan vs. GarciaDiane Dee Yanee100% (2)

- Crim Rev Cases FulltextDocument74 pagesCrim Rev Cases FulltextDiane Dee YaneeNo ratings yet

- WackDocument1 pageWackDiane Dee YaneeNo ratings yet

- REPUBLIC V Heirs of BorbonDocument2 pagesREPUBLIC V Heirs of BorbonDiane Dee YaneeNo ratings yet

- RuleDocument4 pagesRuleDiane Dee YaneeNo ratings yet

- Crim Law Bar Qs EssayDocument130 pagesCrim Law Bar Qs EssayDiane Dee YaneeNo ratings yet

- Mercantile Law 2016 Bar Examinations No AnswersDocument4 pagesMercantile Law 2016 Bar Examinations No AnswersDiane Dee YaneeNo ratings yet

- Affidavit of QuitclaimDocument3 pagesAffidavit of QuitclaimDiane Dee YaneeNo ratings yet

- Quitclaim SampleDocument1 pageQuitclaim SampleDiane Dee YaneeNo ratings yet

- No Answers Legal Ethics Bar Questions 2006-2014Document88 pagesNo Answers Legal Ethics Bar Questions 2006-2014Diane Dee YaneeNo ratings yet

- Trinidad Gamboa-Roces vs. Judge Ranhel PerezDocument2 pagesTrinidad Gamboa-Roces vs. Judge Ranhel PerezDiane Dee YaneeNo ratings yet

- PALE Judicial DisciplineDocument6 pagesPALE Judicial DisciplineDiane Dee YaneeNo ratings yet

- Gamboa-Roces vs. Judge Ranhel A. PerezDocument1 pageGamboa-Roces vs. Judge Ranhel A. PerezDiane Dee YaneeNo ratings yet

- A.M. No. MTJ-16-1887Document1 pageA.M. No. MTJ-16-1887Diane Dee YaneeNo ratings yet

- Gamboa-Roces vs. Judge PerezDocument1 pageGamboa-Roces vs. Judge PerezDiane Dee YaneeNo ratings yet