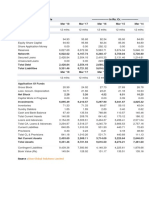

Key Financial Ratios of UCO Bank - in Rs. Cr.

Key Financial Ratios of UCO Bank - in Rs. Cr.

You might also like

- Acca AfmDocument41 pagesAcca AfmGowri Shankari100% (1)

- Fin 332 HW 3 Fall 2021Document5 pagesFin 332 HW 3 Fall 2021Alena ChauNo ratings yet

- Schaum's Outline of Basic Business Mathematics, 2edFrom EverandSchaum's Outline of Basic Business Mathematics, 2edRating: 5 out of 5 stars5/5 (2)

- Ch2 Solutions To The ExercisesDocument5 pagesCh2 Solutions To The ExercisesNishant Sharma0% (1)

- Project of Tata MotorsDocument7 pagesProject of Tata MotorsRaj KiranNo ratings yet

- in Rs. Cr.Document19 pagesin Rs. Cr.Ashish Kumar SharmaNo ratings yet

- State Bank of India: Key Financial Ratios - in Rs. Cr.Document4 pagesState Bank of India: Key Financial Ratios - in Rs. Cr.zubairkhan7No ratings yet

- ICICI Bank - Consolidated Key Financial Ratios Banks - Private Sector Consolidated Key Financial Ratios of ICICI Bank - BSE: 532174, NSE: ICICIBANKDocument2 pagesICICI Bank - Consolidated Key Financial Ratios Banks - Private Sector Consolidated Key Financial Ratios of ICICI Bank - BSE: 532174, NSE: ICICIBANKr79qwkxcfjNo ratings yet

- Balance Sheet of Axis Bank: - in Rs. Cr.Document37 pagesBalance Sheet of Axis Bank: - in Rs. Cr.rampunjaniNo ratings yet

- Balance Sheet: Sources of FundsDocument14 pagesBalance Sheet: Sources of FundsJayesh RodeNo ratings yet

- Financial Ratios of Federal BankDocument35 pagesFinancial Ratios of Federal BankVivek RanjanNo ratings yet

- Godrej IndustriesDocument5 pagesGodrej Industriesshashank sagarNo ratings yet

- Key Financial Ratios of Tata Motors: - in Rs. Cr.Document3 pagesKey Financial Ratios of Tata Motors: - in Rs. Cr.ajinkyamahajanNo ratings yet

- Atlas Copco (India) LTD Balance Sheet: Sources of FundsDocument19 pagesAtlas Copco (India) LTD Balance Sheet: Sources of FundsnehaNo ratings yet

- BaljiDocument4 pagesBaljiBalaji SuburajNo ratings yet

- Cash Flow of ICICI Bank - in Rs. Cr.Document12 pagesCash Flow of ICICI Bank - in Rs. Cr.Neethu GesanNo ratings yet

- Syndicate BankDocument5 pagesSyndicate BankpratikNo ratings yet

- Asian Paints Money ControlDocument19 pagesAsian Paints Money ControlChiranth BhoopalamNo ratings yet

- Book 1Document18 pagesBook 1Ankit PichholiyaNo ratings yet

- Eveready Industries India Balance Sheet - in Rs. Cr.Document5 pagesEveready Industries India Balance Sheet - in Rs. Cr.Jb SinghaNo ratings yet

- 2 - Aditya - Balaji TelefilmsDocument12 pages2 - Aditya - Balaji Telefilmsrajat_singlaNo ratings yet

- 12 - Ishan Aggarwal - Shreyans Industries Ltd.Document11 pages12 - Ishan Aggarwal - Shreyans Industries Ltd.rajat_singlaNo ratings yet

- FINANCIAL ANALYSIS of ONGCDocument13 pagesFINANCIAL ANALYSIS of ONGCdipshi92No ratings yet

- Ashok Leyland Limited: RatiosDocument6 pagesAshok Leyland Limited: RatiosAbhishek BhattacharjeeNo ratings yet

- Balance Sheet of TCSDocument8 pagesBalance Sheet of TCSSurbhi LodhaNo ratings yet

- Balance Sheet of TCSDocument8 pagesBalance Sheet of TCSAmit LalchandaniNo ratings yet

- Apollo TyresDocument4 pagesApollo TyresGokulKumarNo ratings yet

- Ambuja & ACC Final RatiosDocument23 pagesAmbuja & ACC Final RatiosAjay KudavNo ratings yet

- Ratio Analysis: Balance Sheet of HPCLDocument8 pagesRatio Analysis: Balance Sheet of HPCLrajat_singlaNo ratings yet

- IciciDocument9 pagesIciciChirdeep PareekNo ratings yet

- Financial Ratios of Hero Honda MotorsDocument6 pagesFinancial Ratios of Hero Honda MotorsParag MaheshwariNo ratings yet

- Capital and Liabilities:: United Western BankDocument15 pagesCapital and Liabilities:: United Western BankAbhishek KarumbaiahNo ratings yet

- Shinansh TiwariDocument11 pagesShinansh TiwariAnuj VermaNo ratings yet

- Ratio Analysis of Over The Last 5 Years: Power Grid Corporation of India LTDDocument9 pagesRatio Analysis of Over The Last 5 Years: Power Grid Corporation of India LTDKrishna NimmakuriNo ratings yet

- Balance Sheet of Indiabulls - in Rs. Cr.Document3 pagesBalance Sheet of Indiabulls - in Rs. Cr.MubeenNo ratings yet

- BajajDocument22 pagesBajajPulkit BlagganNo ratings yet

- Previous Years: Canar A Bank - in Rs. Cr.Document12 pagesPrevious Years: Canar A Bank - in Rs. Cr.kapish1014No ratings yet

- 29 - Tej Inder - Bharti AirtelDocument14 pages29 - Tej Inder - Bharti Airtelrajat_singlaNo ratings yet

- Per Share Ratios: Mar ' 09 Mar ' 08 Mar ' 07 Mar ' 06 Mar ' 05Document4 pagesPer Share Ratios: Mar ' 09 Mar ' 08 Mar ' 07 Mar ' 06 Mar ' 05alihayatNo ratings yet

- Balance Sheet of Allahabad BankDocument26 pagesBalance Sheet of Allahabad BankMemoona RizviNo ratings yet

- Icici 1Document2 pagesIcici 1AishwaryaSushantNo ratings yet

- Balance Sheet of Essar Oil: - in Rs. Cr.Document7 pagesBalance Sheet of Essar Oil: - in Rs. Cr.sonalmahidaNo ratings yet

- Balance Sheet: Hindalco IndustriesDocument20 pagesBalance Sheet: Hindalco Industriesparinay202No ratings yet

- Appl Ication Mon EyDocument14 pagesAppl Ication Mon EyDevesh PantNo ratings yet

- Key Financial Ratios of NTPC: - in Rs. Cr.Document3 pagesKey Financial Ratios of NTPC: - in Rs. Cr.Vaibhav KundalwalNo ratings yet

- HTTP WWW - MoneycontrolDocument1 pageHTTP WWW - MoneycontrolPavan PoliNo ratings yet

- Top Companies in Oil and Natural Gas SectorDocument24 pagesTop Companies in Oil and Natural Gas SectorSravanKumar IyerNo ratings yet

- Gujarat Mineral Development Corporation Standalone Balance Sheet (In Rs. CR.)Document128 pagesGujarat Mineral Development Corporation Standalone Balance Sheet (In Rs. CR.)Riya ShahNo ratings yet

- Wip Ro Key Financial Ratios - in Rs. Cr.Document4 pagesWip Ro Key Financial Ratios - in Rs. Cr.Priyanck VaisshNo ratings yet

- UTV Software Communications LTDDocument4 pagesUTV Software Communications LTDNeesha PrabhuNo ratings yet

- 15 - Manish - DLFDocument8 pages15 - Manish - DLFrajat_singlaNo ratings yet

- Balance Sheet - in Rs. Cr.Document3 pagesBalance Sheet - in Rs. Cr.jelsiya100% (1)

- Mehran Sugar Mills - Six Years Financial Review at A GlanceDocument3 pagesMehran Sugar Mills - Six Years Financial Review at A GlanceUmair ChandaNo ratings yet

- Balance Sheet of Empee DistilleriesDocument4 pagesBalance Sheet of Empee DistilleriesArun PandiyanNo ratings yet

- Balance Sheet of Larsen and Toubro: - in Rs. Cr.Document3 pagesBalance Sheet of Larsen and Toubro: - in Rs. Cr.Ashirvad MayekarNo ratings yet

- Accounts Term PaperDocument508 pagesAccounts Term Paperrohit_indiaNo ratings yet

- Balance Sheet - in Rs. Cr.Document72 pagesBalance Sheet - in Rs. Cr.sukesh_sanghi100% (1)

- Surajit SahaDocument30 pagesSurajit SahaAgneesh DuttaNo ratings yet

- Ratios FinDocument30 pagesRatios Fingaurav sahuNo ratings yet

- Ratios FinDocument16 pagesRatios Fingaurav sahuNo ratings yet

- Ratios FinancialDocument16 pagesRatios Financialgaurav sahuNo ratings yet

- Ratios FinancialDocument16 pagesRatios Financialgaurav sahuNo ratings yet

- Annual Accounts 2021Document11 pagesAnnual Accounts 2021Shehzad QureshiNo ratings yet

- How GSK Boosts HUL in An All Equity Merger - Case Analysis - IpleadersDocument5 pagesHow GSK Boosts HUL in An All Equity Merger - Case Analysis - IpleadersArchisman SahaNo ratings yet

- Vaneck Etfs Distributions Schedule 2023Document2 pagesVaneck Etfs Distributions Schedule 2023Jéferson AlegreNo ratings yet

- The 5 Most Powerful Candlestick PatternsDocument13 pagesThe 5 Most Powerful Candlestick PatternsnandhalaalaaNo ratings yet

- Relative Value Models (Feb04)Document18 pagesRelative Value Models (Feb04)api-3763138No ratings yet

- International Financial Management: Resume Chapter 6Document6 pagesInternational Financial Management: Resume Chapter 6Wida KusmayanaNo ratings yet

- The Yukii Community Token (YCT)Document15 pagesThe Yukii Community Token (YCT)Sopso TkoNo ratings yet

- Prospectus 080920201601Document403 pagesProspectus 080920201601SubscriptionNo ratings yet

- The Innovative Pharma Marketeer's Toolkit - Your Prescription For Digital Content Marketing SuccessDocument34 pagesThe Innovative Pharma Marketeer's Toolkit - Your Prescription For Digital Content Marketing SuccessSunil K.BNo ratings yet

- Moving AverageDocument3 pagesMoving AveragedorpianabsaNo ratings yet

- MFIN6003 - Group Project 1Document2 pagesMFIN6003 - Group Project 1cccNo ratings yet

- Reliance Monthly Income PlanDocument3 pagesReliance Monthly Income PlanPaul RamoneNo ratings yet

- Debt InstrumentDocument6 pagesDebt InstrumentTin PangilinanNo ratings yet

- Chapter 15 ProblemsDocument2 pagesChapter 15 ProblemsBombitaNo ratings yet

- International Equity Investing: Investing in Emerging MarketsDocument20 pagesInternational Equity Investing: Investing in Emerging MarketsPhuoc DangNo ratings yet

- MarcomInvest English 1Document14 pagesMarcomInvest English 1piranikaweakrNo ratings yet

- FZ5000 Solución Tarea 1 AJ2020Document3 pagesFZ5000 Solución Tarea 1 AJ2020gerardoNo ratings yet

- Arbitrage Pricing TheoryDocument15 pagesArbitrage Pricing TheoryYixing ZhangNo ratings yet

- Capital Market DevelopmentDocument12 pagesCapital Market DevelopmentFaiz1000No ratings yet

- Options Strat9 enDocument2 pagesOptions Strat9 enCorey WuNo ratings yet

- 2018 Re Nationality Requirement of Third Telco20211217 12Document12 pages2018 Re Nationality Requirement of Third Telco20211217 12Jadel Kaye ALJ TrainingNo ratings yet

- 19bbl110 FINAL RESEARCH PAPERDocument20 pages19bbl110 FINAL RESEARCH PAPERShubham TejasNo ratings yet

- Marketable Securities + Receivable: Increase. IncreaseDocument4 pagesMarketable Securities + Receivable: Increase. IncreaseVergel MartinezNo ratings yet

- Solved Lindy A Calendar Year U S Corporation Bought Inventory Items From ADocument1 pageSolved Lindy A Calendar Year U S Corporation Bought Inventory Items From AAnbu jaromia100% (1)

- Materi Rumus Uts MKDocument10 pagesMateri Rumus Uts MKMarsa ArrahmanNo ratings yet

- Reverse MergerDocument30 pagesReverse MergerAmrita SinghNo ratings yet

- Presentation On Option StrategiesDocument11 pagesPresentation On Option Strategies26amitNo ratings yet

- Overview of Credit RatingsDocument13 pagesOverview of Credit RatingsFragancias Europeas CTNo ratings yet

Download as docx, pdf, or txt

You might also like

- Acca AfmDocument41 pagesAcca AfmGowri Shankari100% (1)

- Fin 332 HW 3 Fall 2021Document5 pagesFin 332 HW 3 Fall 2021Alena ChauNo ratings yet

- Schaum's Outline of Basic Business Mathematics, 2edFrom EverandSchaum's Outline of Basic Business Mathematics, 2edRating: 5 out of 5 stars5/5 (2)

- Ch2 Solutions To The ExercisesDocument5 pagesCh2 Solutions To The ExercisesNishant Sharma0% (1)

- Project of Tata MotorsDocument7 pagesProject of Tata MotorsRaj KiranNo ratings yet

- in Rs. Cr.Document19 pagesin Rs. Cr.Ashish Kumar SharmaNo ratings yet

- State Bank of India: Key Financial Ratios - in Rs. Cr.Document4 pagesState Bank of India: Key Financial Ratios - in Rs. Cr.zubairkhan7No ratings yet

- ICICI Bank - Consolidated Key Financial Ratios Banks - Private Sector Consolidated Key Financial Ratios of ICICI Bank - BSE: 532174, NSE: ICICIBANKDocument2 pagesICICI Bank - Consolidated Key Financial Ratios Banks - Private Sector Consolidated Key Financial Ratios of ICICI Bank - BSE: 532174, NSE: ICICIBANKr79qwkxcfjNo ratings yet

- Balance Sheet of Axis Bank: - in Rs. Cr.Document37 pagesBalance Sheet of Axis Bank: - in Rs. Cr.rampunjaniNo ratings yet

- Balance Sheet: Sources of FundsDocument14 pagesBalance Sheet: Sources of FundsJayesh RodeNo ratings yet

- Financial Ratios of Federal BankDocument35 pagesFinancial Ratios of Federal BankVivek RanjanNo ratings yet

- Godrej IndustriesDocument5 pagesGodrej Industriesshashank sagarNo ratings yet

- Key Financial Ratios of Tata Motors: - in Rs. Cr.Document3 pagesKey Financial Ratios of Tata Motors: - in Rs. Cr.ajinkyamahajanNo ratings yet

- Atlas Copco (India) LTD Balance Sheet: Sources of FundsDocument19 pagesAtlas Copco (India) LTD Balance Sheet: Sources of FundsnehaNo ratings yet

- BaljiDocument4 pagesBaljiBalaji SuburajNo ratings yet

- Cash Flow of ICICI Bank - in Rs. Cr.Document12 pagesCash Flow of ICICI Bank - in Rs. Cr.Neethu GesanNo ratings yet

- Syndicate BankDocument5 pagesSyndicate BankpratikNo ratings yet

- Asian Paints Money ControlDocument19 pagesAsian Paints Money ControlChiranth BhoopalamNo ratings yet

- Book 1Document18 pagesBook 1Ankit PichholiyaNo ratings yet

- Eveready Industries India Balance Sheet - in Rs. Cr.Document5 pagesEveready Industries India Balance Sheet - in Rs. Cr.Jb SinghaNo ratings yet

- 2 - Aditya - Balaji TelefilmsDocument12 pages2 - Aditya - Balaji Telefilmsrajat_singlaNo ratings yet

- 12 - Ishan Aggarwal - Shreyans Industries Ltd.Document11 pages12 - Ishan Aggarwal - Shreyans Industries Ltd.rajat_singlaNo ratings yet

- FINANCIAL ANALYSIS of ONGCDocument13 pagesFINANCIAL ANALYSIS of ONGCdipshi92No ratings yet

- Ashok Leyland Limited: RatiosDocument6 pagesAshok Leyland Limited: RatiosAbhishek BhattacharjeeNo ratings yet

- Balance Sheet of TCSDocument8 pagesBalance Sheet of TCSSurbhi LodhaNo ratings yet

- Balance Sheet of TCSDocument8 pagesBalance Sheet of TCSAmit LalchandaniNo ratings yet

- Apollo TyresDocument4 pagesApollo TyresGokulKumarNo ratings yet

- Ambuja & ACC Final RatiosDocument23 pagesAmbuja & ACC Final RatiosAjay KudavNo ratings yet

- Ratio Analysis: Balance Sheet of HPCLDocument8 pagesRatio Analysis: Balance Sheet of HPCLrajat_singlaNo ratings yet

- IciciDocument9 pagesIciciChirdeep PareekNo ratings yet

- Financial Ratios of Hero Honda MotorsDocument6 pagesFinancial Ratios of Hero Honda MotorsParag MaheshwariNo ratings yet

- Capital and Liabilities:: United Western BankDocument15 pagesCapital and Liabilities:: United Western BankAbhishek KarumbaiahNo ratings yet

- Shinansh TiwariDocument11 pagesShinansh TiwariAnuj VermaNo ratings yet

- Ratio Analysis of Over The Last 5 Years: Power Grid Corporation of India LTDDocument9 pagesRatio Analysis of Over The Last 5 Years: Power Grid Corporation of India LTDKrishna NimmakuriNo ratings yet

- Balance Sheet of Indiabulls - in Rs. Cr.Document3 pagesBalance Sheet of Indiabulls - in Rs. Cr.MubeenNo ratings yet

- BajajDocument22 pagesBajajPulkit BlagganNo ratings yet

- Previous Years: Canar A Bank - in Rs. Cr.Document12 pagesPrevious Years: Canar A Bank - in Rs. Cr.kapish1014No ratings yet

- 29 - Tej Inder - Bharti AirtelDocument14 pages29 - Tej Inder - Bharti Airtelrajat_singlaNo ratings yet

- Per Share Ratios: Mar ' 09 Mar ' 08 Mar ' 07 Mar ' 06 Mar ' 05Document4 pagesPer Share Ratios: Mar ' 09 Mar ' 08 Mar ' 07 Mar ' 06 Mar ' 05alihayatNo ratings yet

- Balance Sheet of Allahabad BankDocument26 pagesBalance Sheet of Allahabad BankMemoona RizviNo ratings yet

- Icici 1Document2 pagesIcici 1AishwaryaSushantNo ratings yet

- Balance Sheet of Essar Oil: - in Rs. Cr.Document7 pagesBalance Sheet of Essar Oil: - in Rs. Cr.sonalmahidaNo ratings yet

- Balance Sheet: Hindalco IndustriesDocument20 pagesBalance Sheet: Hindalco Industriesparinay202No ratings yet

- Appl Ication Mon EyDocument14 pagesAppl Ication Mon EyDevesh PantNo ratings yet

- Key Financial Ratios of NTPC: - in Rs. Cr.Document3 pagesKey Financial Ratios of NTPC: - in Rs. Cr.Vaibhav KundalwalNo ratings yet

- HTTP WWW - MoneycontrolDocument1 pageHTTP WWW - MoneycontrolPavan PoliNo ratings yet

- Top Companies in Oil and Natural Gas SectorDocument24 pagesTop Companies in Oil and Natural Gas SectorSravanKumar IyerNo ratings yet

- Gujarat Mineral Development Corporation Standalone Balance Sheet (In Rs. CR.)Document128 pagesGujarat Mineral Development Corporation Standalone Balance Sheet (In Rs. CR.)Riya ShahNo ratings yet

- Wip Ro Key Financial Ratios - in Rs. Cr.Document4 pagesWip Ro Key Financial Ratios - in Rs. Cr.Priyanck VaisshNo ratings yet

- UTV Software Communications LTDDocument4 pagesUTV Software Communications LTDNeesha PrabhuNo ratings yet

- 15 - Manish - DLFDocument8 pages15 - Manish - DLFrajat_singlaNo ratings yet

- Balance Sheet - in Rs. Cr.Document3 pagesBalance Sheet - in Rs. Cr.jelsiya100% (1)

- Mehran Sugar Mills - Six Years Financial Review at A GlanceDocument3 pagesMehran Sugar Mills - Six Years Financial Review at A GlanceUmair ChandaNo ratings yet

- Balance Sheet of Empee DistilleriesDocument4 pagesBalance Sheet of Empee DistilleriesArun PandiyanNo ratings yet

- Balance Sheet of Larsen and Toubro: - in Rs. Cr.Document3 pagesBalance Sheet of Larsen and Toubro: - in Rs. Cr.Ashirvad MayekarNo ratings yet

- Accounts Term PaperDocument508 pagesAccounts Term Paperrohit_indiaNo ratings yet

- Balance Sheet - in Rs. Cr.Document72 pagesBalance Sheet - in Rs. Cr.sukesh_sanghi100% (1)

- Surajit SahaDocument30 pagesSurajit SahaAgneesh DuttaNo ratings yet

- Ratios FinDocument30 pagesRatios Fingaurav sahuNo ratings yet

- Ratios FinDocument16 pagesRatios Fingaurav sahuNo ratings yet

- Ratios FinancialDocument16 pagesRatios Financialgaurav sahuNo ratings yet

- Ratios FinancialDocument16 pagesRatios Financialgaurav sahuNo ratings yet

- Annual Accounts 2021Document11 pagesAnnual Accounts 2021Shehzad QureshiNo ratings yet

- How GSK Boosts HUL in An All Equity Merger - Case Analysis - IpleadersDocument5 pagesHow GSK Boosts HUL in An All Equity Merger - Case Analysis - IpleadersArchisman SahaNo ratings yet

- Vaneck Etfs Distributions Schedule 2023Document2 pagesVaneck Etfs Distributions Schedule 2023Jéferson AlegreNo ratings yet

- The 5 Most Powerful Candlestick PatternsDocument13 pagesThe 5 Most Powerful Candlestick PatternsnandhalaalaaNo ratings yet

- Relative Value Models (Feb04)Document18 pagesRelative Value Models (Feb04)api-3763138No ratings yet

- International Financial Management: Resume Chapter 6Document6 pagesInternational Financial Management: Resume Chapter 6Wida KusmayanaNo ratings yet

- The Yukii Community Token (YCT)Document15 pagesThe Yukii Community Token (YCT)Sopso TkoNo ratings yet

- Prospectus 080920201601Document403 pagesProspectus 080920201601SubscriptionNo ratings yet

- The Innovative Pharma Marketeer's Toolkit - Your Prescription For Digital Content Marketing SuccessDocument34 pagesThe Innovative Pharma Marketeer's Toolkit - Your Prescription For Digital Content Marketing SuccessSunil K.BNo ratings yet

- Moving AverageDocument3 pagesMoving AveragedorpianabsaNo ratings yet

- MFIN6003 - Group Project 1Document2 pagesMFIN6003 - Group Project 1cccNo ratings yet

- Reliance Monthly Income PlanDocument3 pagesReliance Monthly Income PlanPaul RamoneNo ratings yet

- Debt InstrumentDocument6 pagesDebt InstrumentTin PangilinanNo ratings yet

- Chapter 15 ProblemsDocument2 pagesChapter 15 ProblemsBombitaNo ratings yet

- International Equity Investing: Investing in Emerging MarketsDocument20 pagesInternational Equity Investing: Investing in Emerging MarketsPhuoc DangNo ratings yet

- MarcomInvest English 1Document14 pagesMarcomInvest English 1piranikaweakrNo ratings yet

- FZ5000 Solución Tarea 1 AJ2020Document3 pagesFZ5000 Solución Tarea 1 AJ2020gerardoNo ratings yet

- Arbitrage Pricing TheoryDocument15 pagesArbitrage Pricing TheoryYixing ZhangNo ratings yet

- Capital Market DevelopmentDocument12 pagesCapital Market DevelopmentFaiz1000No ratings yet

- Options Strat9 enDocument2 pagesOptions Strat9 enCorey WuNo ratings yet

- 2018 Re Nationality Requirement of Third Telco20211217 12Document12 pages2018 Re Nationality Requirement of Third Telco20211217 12Jadel Kaye ALJ TrainingNo ratings yet

- 19bbl110 FINAL RESEARCH PAPERDocument20 pages19bbl110 FINAL RESEARCH PAPERShubham TejasNo ratings yet

- Marketable Securities + Receivable: Increase. IncreaseDocument4 pagesMarketable Securities + Receivable: Increase. IncreaseVergel MartinezNo ratings yet

- Solved Lindy A Calendar Year U S Corporation Bought Inventory Items From ADocument1 pageSolved Lindy A Calendar Year U S Corporation Bought Inventory Items From AAnbu jaromia100% (1)

- Materi Rumus Uts MKDocument10 pagesMateri Rumus Uts MKMarsa ArrahmanNo ratings yet

- Reverse MergerDocument30 pagesReverse MergerAmrita SinghNo ratings yet

- Presentation On Option StrategiesDocument11 pagesPresentation On Option Strategies26amitNo ratings yet

- Overview of Credit RatingsDocument13 pagesOverview of Credit RatingsFragancias Europeas CTNo ratings yet