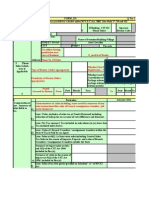

Environmental Taxes: Tax On Petroleum

Environmental Taxes: Tax On Petroleum

You might also like

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 18-19 - CT - Annual - 19dec19 - 05.35PM - SEE & Financial InstitutionDocument2 pages18-19 - CT - Annual - 19dec19 - 05.35PM - SEE & Financial InstitutionWUTYI THINNNo ratings yet

- US Internal Revenue Service: f6478 - 2004Document4 pagesUS Internal Revenue Service: f6478 - 2004IRSNo ratings yet

- Credit For Alcohol Used As Fuel: Form 4136Document4 pagesCredit For Alcohol Used As Fuel: Form 4136IRSNo ratings yet

- GSTR9 08aaafu3205h1zh 032022Document8 pagesGSTR9 08aaafu3205h1zh 032022Deepanshu AgarwalNo ratings yet

- Packet - Ii: Signature Not Verified Signature Not Verified Signature Not VerifiedDocument3 pagesPacket - Ii: Signature Not Verified Signature Not Verified Signature Not VerifiedJaimin PopatNo ratings yet

- GSTR9Document8 pagesGSTR9legendry007No ratings yet

- US Internal Revenue Service: f6478 - 2005Document4 pagesUS Internal Revenue Service: f6478 - 2005IRSNo ratings yet

- US Internal Revenue Service: F1120icd - 2000Document6 pagesUS Internal Revenue Service: F1120icd - 2000IRSNo ratings yet

- Allocation of Income and Expenses Under Section 936 (H) (5) : Schedule P (Form 5735)Document2 pagesAllocation of Income and Expenses Under Section 936 (H) (5) : Schedule P (Form 5735)IRSNo ratings yet

- Quarterly Federal Excise Tax Return: For Irs Use OnlyDocument7 pagesQuarterly Federal Excise Tax Return: For Irs Use OnlyIRSNo ratings yet

- 22-23 Annual IT 02052023 0210pmDocument8 pages22-23 Annual IT 02052023 0210pmWint PaingNo ratings yet

- Application - Form Q3Document4 pagesApplication - Form Q3Top GNo ratings yet

- US Internal Revenue Service: f8849s8Document2 pagesUS Internal Revenue Service: f8849s8IRSNo ratings yet

- CBP - Cost SubmissionDocument10 pagesCBP - Cost SubmissionGerald CrewsNo ratings yet

- Igst Itc 11112022Document18 pagesIgst Itc 11112022hrtclients1No ratings yet

- Annexure V Comparative ChartDocument4 pagesAnnexure V Comparative ChartRaju HalderNo ratings yet

- (As Defined Under Rule 2 (Ea) of The Central Excise Rules, 2002 Read With Rule 2 (1) (CCCC) of The Service Tax Rules, 1994)Document18 pages(As Defined Under Rule 2 (Ea) of The Central Excise Rules, 2002 Read With Rule 2 (1) (CCCC) of The Service Tax Rules, 1994)135276No ratings yet

- GSTR9 19GCBPS5582Q1ZH 032023Document8 pagesGSTR9 19GCBPS5582Q1ZH 032023nirmalku2061No ratings yet

- 19 CT Annual 18dec19 11.09AMDocument2 pages19 CT Annual 18dec19 11.09AMWUTYI THINNNo ratings yet

- Form VAT-R2: (See Rule 16 (2) ) DdmmyyDocument7 pagesForm VAT-R2: (See Rule 16 (2) ) Ddmmyygovind_2363No ratings yet

- US Internal Revenue Service: f1065sm3 AccessibleDocument3 pagesUS Internal Revenue Service: f1065sm3 AccessibleIRSNo ratings yet

- GSTR9 18acvpa7546a1zk 032022Document8 pagesGSTR9 18acvpa7546a1zk 032022SUBHASH MOURNo ratings yet

- US Internal Revenue Service: f8864 - 2005Document4 pagesUS Internal Revenue Service: f8864 - 2005IRSNo ratings yet

- GST QuestionnaireDocument2 pagesGST QuestionnaireIshan MehtaNo ratings yet

- US Internal Revenue Service: F1120icd - 1992Document6 pagesUS Internal Revenue Service: F1120icd - 1992IRSNo ratings yet

- U.S. Real Estate Mortgage Investment Conduit (REMIC) Income Tax ReturnDocument4 pagesU.S. Real Estate Mortgage Investment Conduit (REMIC) Income Tax ReturnIRSNo ratings yet

- GSTR9 09aaact9363l1zq 032023Document8 pagesGSTR9 09aaact9363l1zq 032023sachinkumar.rkcjNo ratings yet

- Adm Guidelines Cov 19 LevyDocument12 pagesAdm Guidelines Cov 19 LevyFuaad DodooNo ratings yet

- US Internal Revenue Service: F1120idk - 1998Document5 pagesUS Internal Revenue Service: F1120idk - 1998IRSNo ratings yet

- GSTR9 09bwbpk7755a1zk 032021Document8 pagesGSTR9 09bwbpk7755a1zk 032021Ankit JainNo ratings yet

- US Internal Revenue Service: f1120pc - 2002Document8 pagesUS Internal Revenue Service: f1120pc - 2002IRSNo ratings yet

- Report On Petroleum Production and Revenues: January 2020Document8 pagesReport On Petroleum Production and Revenues: January 2020Rahul ChoudharyNo ratings yet

- GSTR9 29aaqfm8617b1zz 032022Document8 pagesGSTR9 29aaqfm8617b1zz 032022helloNo ratings yet

- W5 in TuteDocument5 pagesW5 in TuteBáchHợpNo ratings yet

- GSTR9 22aabcn2864p1z7 032018Document8 pagesGSTR9 22aabcn2864p1z7 032018Sumit K JhaNo ratings yet

- Multiple Choice Questions: Manan Prakashan 1Document57 pagesMultiple Choice Questions: Manan Prakashan 1Tanvi DevaleNo ratings yet

- Changes in ITC Reporting in GSTR - 3BDocument6 pagesChanges in ITC Reporting in GSTR - 3BKirtan Ramesh JethvaNo ratings yet

- US Internal Revenue Service: f1120pc - 1993Document8 pagesUS Internal Revenue Service: f1120pc - 1993IRSNo ratings yet

- US Internal Revenue Service: f8390 - 1993Document4 pagesUS Internal Revenue Service: f8390 - 1993IRSNo ratings yet

- Form IR2 4Document3 pagesForm IR2 4khaingshwe wutyiNo ratings yet

- Audit Report PART-3 Schedule-Iv: Eligibility Certificate (EC) No. Certificate of Entitlement (COE) NoDocument12 pagesAudit Report PART-3 Schedule-Iv: Eligibility Certificate (EC) No. Certificate of Entitlement (COE) NosuniljaithwarNo ratings yet

- US Internal Revenue Service: f1120sph - 1992Document2 pagesUS Internal Revenue Service: f1120sph - 1992IRSNo ratings yet

- GSTR9 23apjps3159l1zg 032022Document8 pagesGSTR9 23apjps3159l1zg 032022sales candoNo ratings yet

- US Internal Revenue Service: F1120idk - 2001Document5 pagesUS Internal Revenue Service: F1120idk - 2001IRSNo ratings yet

- FIN AL: Form GSTR-9Document8 pagesFIN AL: Form GSTR-9mani samiNo ratings yet

- US Internal Revenue Service: f6478 - 1995Document3 pagesUS Internal Revenue Service: f6478 - 1995IRSNo ratings yet

- ITR 4 Sugam Form For Assessment Year 2018 19Document9 pagesITR 4 Sugam Form For Assessment Year 2018 19sureshstipl sureshNo ratings yet

- 1120-IC-DISC: Interest Charge Domestic International Sales Corporation ReturnDocument6 pages1120-IC-DISC: Interest Charge Domestic International Sales Corporation ReturnIRSNo ratings yet

- GSTR9 27aasfp7032r1za 032020Document9 pagesGSTR9 27aasfp7032r1za 032020sharad agarwalNo ratings yet

- Form 231Document14 pagesForm 231Jignesh Dinesh MewadaNo ratings yet

- Basic Act & CenvatDocument24 pagesBasic Act & CenvatrameshNo ratings yet

- April 2020 PTE 2 PathfinderDocument54 pagesApril 2020 PTE 2 PathfinderBadmus AyomideNo ratings yet

- Itctp 2022Document4 pagesItctp 2022Muskaan ShawNo ratings yet

- GSTR9 29aahcv2115k1z5 032021Document8 pagesGSTR9 29aahcv2115k1z5 032021MICO EMPLOYEES CO OPERATIVE SOCIETY LTDNo ratings yet

- 2021-09-09 Morrisons Interim AnnouncementDocument48 pages2021-09-09 Morrisons Interim AnnouncementBassel HagagNo ratings yet

- US Internal Revenue Service: f4562 - 1992Document2 pagesUS Internal Revenue Service: f4562 - 1992IRSNo ratings yet

- Form Vat - IiiDocument4 pagesForm Vat - IiihrsolutionNo ratings yet

- Imp Questions Eco Part 1Document28 pagesImp Questions Eco Part 1sansarnathNo ratings yet

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSNo ratings yet

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSNo ratings yet

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSNo ratings yet

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSNo ratings yet

- 2 ADocument8 pages2 AMayur PatelNo ratings yet

- Basic Welding TheoryDocument15 pagesBasic Welding TheoryCarina MostralesNo ratings yet

- Fem DamageDocument13 pagesFem DamageGerard VelicariaNo ratings yet

- Classical Theory of DetonationDocument20 pagesClassical Theory of Detonationalexander.lhoistNo ratings yet

- Boiler Steam To ProcessDocument9 pagesBoiler Steam To ProcessMDR PRAPHUNo ratings yet

- HTLP-80 Application ProcedureDocument9 pagesHTLP-80 Application ProceduremaheshNo ratings yet

- RNAprotect Cell Reagent HandbookDocument40 pagesRNAprotect Cell Reagent HandbookSergio MugnaiNo ratings yet

- BS 6683 (1985) Installation and Use of ValvesDocument18 pagesBS 6683 (1985) Installation and Use of Valves김창배No ratings yet

- Standart Cina Untuk WeldingDocument52 pagesStandart Cina Untuk Weldingandristy90No ratings yet

- Prep. BUROW'S SOLUTIONDocument1 pagePrep. BUROW'S SOLUTIONJoanna Carla Marmonejo Estorninos-Walker100% (1)

- Toxicology - Lesson Plan - KnightonDocument7 pagesToxicology - Lesson Plan - Knightonapi-257588494100% (1)

- ExerciseDocument4 pagesExerciseariefnur19No ratings yet

- How To Eliminatdadde Outgassing, The Powder Coating Faux PasDocument2 pagesHow To Eliminatdadde Outgassing, The Powder Coating Faux PasSandra ArianaNo ratings yet

- Flexural Behavior of RC Beam Strengthened With Carbon Fiber Sheets in Shear and Flexure ZoneDocument38 pagesFlexural Behavior of RC Beam Strengthened With Carbon Fiber Sheets in Shear and Flexure ZoneFrances Sol TumulakNo ratings yet

- ASTM DIN Equivalent MaterialsDocument6 pagesASTM DIN Equivalent MaterialsCandra Saja63% (8)

- Research Article: Determination of Ranitidine in Human Plasma by SPE and ESI-LC-MS/MS For Use in Bioequivalence StudiesDocument8 pagesResearch Article: Determination of Ranitidine in Human Plasma by SPE and ESI-LC-MS/MS For Use in Bioequivalence StudiesSrujana BudheNo ratings yet

- BIOplastics Catalog2010Document129 pagesBIOplastics Catalog2010Enrico SchicchiNo ratings yet

- Ophthalmics Brochure 1015 Lay2Document36 pagesOphthalmics Brochure 1015 Lay2nadjib62100% (2)

- Thermo Dynamics Question BankDocument3 pagesThermo Dynamics Question Banknisar_ulNo ratings yet

- Water Quality Analysis of Nairobi DamDocument43 pagesWater Quality Analysis of Nairobi DamOrwe Elly100% (1)

- Ethylene Glycol CAS No 107-21-1: Material Safety Data Sheet Sds/MsdsDocument7 pagesEthylene Glycol CAS No 107-21-1: Material Safety Data Sheet Sds/MsdsRyanNo ratings yet

- Advanced Finishing ProcessesDocument23 pagesAdvanced Finishing ProcessesADWAITH G SNo ratings yet

- 202 TA 202A Introduction To Manufacturing ProcessesDocument20 pages202 TA 202A Introduction To Manufacturing ProcessesshubhamNo ratings yet

- Presentasi Sesi 2 Webinar Bromat AMDKDocument46 pagesPresentasi Sesi 2 Webinar Bromat AMDKAOC BPOM Jambi 2022No ratings yet

- Thermal Properties of MaterialsDocument6 pagesThermal Properties of Materialsdhanya1995No ratings yet

- 100 All Greatest Popular Science BooksDocument9 pages100 All Greatest Popular Science BooksJaime Messía100% (2)

- SW13494 - Heat-Flex - 3500. Loai Thay The Bao On PDFDocument2 pagesSW13494 - Heat-Flex - 3500. Loai Thay The Bao On PDFtienNo ratings yet

- Pupuk PT SSA PDFDocument2 pagesPupuk PT SSA PDFNurul HardiyantiNo ratings yet

- Stoichiometry and Process Calculations - K. V. Narayanan and B. Lakshmikutty PDFDocument167 pagesStoichiometry and Process Calculations - K. V. Narayanan and B. Lakshmikutty PDFSarah SanchezNo ratings yet

- ShilajitDocument13 pagesShilajitpseudo3No ratings yet

Download as pdf or txt

You might also like

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- 6th Central Pay Commission Salary CalculatorDocument15 pages6th Central Pay Commission Salary Calculatorrakhonde100% (436)

- Tratamentul Total Al CanceruluiDocument71 pagesTratamentul Total Al CanceruluiAntal98% (98)

- 18-19 - CT - Annual - 19dec19 - 05.35PM - SEE & Financial InstitutionDocument2 pages18-19 - CT - Annual - 19dec19 - 05.35PM - SEE & Financial InstitutionWUTYI THINNNo ratings yet

- US Internal Revenue Service: f6478 - 2004Document4 pagesUS Internal Revenue Service: f6478 - 2004IRSNo ratings yet

- Credit For Alcohol Used As Fuel: Form 4136Document4 pagesCredit For Alcohol Used As Fuel: Form 4136IRSNo ratings yet

- GSTR9 08aaafu3205h1zh 032022Document8 pagesGSTR9 08aaafu3205h1zh 032022Deepanshu AgarwalNo ratings yet

- Packet - Ii: Signature Not Verified Signature Not Verified Signature Not VerifiedDocument3 pagesPacket - Ii: Signature Not Verified Signature Not Verified Signature Not VerifiedJaimin PopatNo ratings yet

- GSTR9Document8 pagesGSTR9legendry007No ratings yet

- US Internal Revenue Service: f6478 - 2005Document4 pagesUS Internal Revenue Service: f6478 - 2005IRSNo ratings yet

- US Internal Revenue Service: F1120icd - 2000Document6 pagesUS Internal Revenue Service: F1120icd - 2000IRSNo ratings yet

- Allocation of Income and Expenses Under Section 936 (H) (5) : Schedule P (Form 5735)Document2 pagesAllocation of Income and Expenses Under Section 936 (H) (5) : Schedule P (Form 5735)IRSNo ratings yet

- Quarterly Federal Excise Tax Return: For Irs Use OnlyDocument7 pagesQuarterly Federal Excise Tax Return: For Irs Use OnlyIRSNo ratings yet

- 22-23 Annual IT 02052023 0210pmDocument8 pages22-23 Annual IT 02052023 0210pmWint PaingNo ratings yet

- Application - Form Q3Document4 pagesApplication - Form Q3Top GNo ratings yet

- US Internal Revenue Service: f8849s8Document2 pagesUS Internal Revenue Service: f8849s8IRSNo ratings yet

- CBP - Cost SubmissionDocument10 pagesCBP - Cost SubmissionGerald CrewsNo ratings yet

- Igst Itc 11112022Document18 pagesIgst Itc 11112022hrtclients1No ratings yet

- Annexure V Comparative ChartDocument4 pagesAnnexure V Comparative ChartRaju HalderNo ratings yet

- (As Defined Under Rule 2 (Ea) of The Central Excise Rules, 2002 Read With Rule 2 (1) (CCCC) of The Service Tax Rules, 1994)Document18 pages(As Defined Under Rule 2 (Ea) of The Central Excise Rules, 2002 Read With Rule 2 (1) (CCCC) of The Service Tax Rules, 1994)135276No ratings yet

- GSTR9 19GCBPS5582Q1ZH 032023Document8 pagesGSTR9 19GCBPS5582Q1ZH 032023nirmalku2061No ratings yet

- 19 CT Annual 18dec19 11.09AMDocument2 pages19 CT Annual 18dec19 11.09AMWUTYI THINNNo ratings yet

- Form VAT-R2: (See Rule 16 (2) ) DdmmyyDocument7 pagesForm VAT-R2: (See Rule 16 (2) ) Ddmmyygovind_2363No ratings yet

- US Internal Revenue Service: f1065sm3 AccessibleDocument3 pagesUS Internal Revenue Service: f1065sm3 AccessibleIRSNo ratings yet

- GSTR9 18acvpa7546a1zk 032022Document8 pagesGSTR9 18acvpa7546a1zk 032022SUBHASH MOURNo ratings yet

- US Internal Revenue Service: f8864 - 2005Document4 pagesUS Internal Revenue Service: f8864 - 2005IRSNo ratings yet

- GST QuestionnaireDocument2 pagesGST QuestionnaireIshan MehtaNo ratings yet

- US Internal Revenue Service: F1120icd - 1992Document6 pagesUS Internal Revenue Service: F1120icd - 1992IRSNo ratings yet

- U.S. Real Estate Mortgage Investment Conduit (REMIC) Income Tax ReturnDocument4 pagesU.S. Real Estate Mortgage Investment Conduit (REMIC) Income Tax ReturnIRSNo ratings yet

- GSTR9 09aaact9363l1zq 032023Document8 pagesGSTR9 09aaact9363l1zq 032023sachinkumar.rkcjNo ratings yet

- Adm Guidelines Cov 19 LevyDocument12 pagesAdm Guidelines Cov 19 LevyFuaad DodooNo ratings yet

- US Internal Revenue Service: F1120idk - 1998Document5 pagesUS Internal Revenue Service: F1120idk - 1998IRSNo ratings yet

- GSTR9 09bwbpk7755a1zk 032021Document8 pagesGSTR9 09bwbpk7755a1zk 032021Ankit JainNo ratings yet

- US Internal Revenue Service: f1120pc - 2002Document8 pagesUS Internal Revenue Service: f1120pc - 2002IRSNo ratings yet

- Report On Petroleum Production and Revenues: January 2020Document8 pagesReport On Petroleum Production and Revenues: January 2020Rahul ChoudharyNo ratings yet

- GSTR9 29aaqfm8617b1zz 032022Document8 pagesGSTR9 29aaqfm8617b1zz 032022helloNo ratings yet

- W5 in TuteDocument5 pagesW5 in TuteBáchHợpNo ratings yet

- GSTR9 22aabcn2864p1z7 032018Document8 pagesGSTR9 22aabcn2864p1z7 032018Sumit K JhaNo ratings yet

- Multiple Choice Questions: Manan Prakashan 1Document57 pagesMultiple Choice Questions: Manan Prakashan 1Tanvi DevaleNo ratings yet

- Changes in ITC Reporting in GSTR - 3BDocument6 pagesChanges in ITC Reporting in GSTR - 3BKirtan Ramesh JethvaNo ratings yet

- US Internal Revenue Service: f1120pc - 1993Document8 pagesUS Internal Revenue Service: f1120pc - 1993IRSNo ratings yet

- US Internal Revenue Service: f8390 - 1993Document4 pagesUS Internal Revenue Service: f8390 - 1993IRSNo ratings yet

- Form IR2 4Document3 pagesForm IR2 4khaingshwe wutyiNo ratings yet

- Audit Report PART-3 Schedule-Iv: Eligibility Certificate (EC) No. Certificate of Entitlement (COE) NoDocument12 pagesAudit Report PART-3 Schedule-Iv: Eligibility Certificate (EC) No. Certificate of Entitlement (COE) NosuniljaithwarNo ratings yet

- US Internal Revenue Service: f1120sph - 1992Document2 pagesUS Internal Revenue Service: f1120sph - 1992IRSNo ratings yet

- GSTR9 23apjps3159l1zg 032022Document8 pagesGSTR9 23apjps3159l1zg 032022sales candoNo ratings yet

- US Internal Revenue Service: F1120idk - 2001Document5 pagesUS Internal Revenue Service: F1120idk - 2001IRSNo ratings yet

- FIN AL: Form GSTR-9Document8 pagesFIN AL: Form GSTR-9mani samiNo ratings yet

- US Internal Revenue Service: f6478 - 1995Document3 pagesUS Internal Revenue Service: f6478 - 1995IRSNo ratings yet

- ITR 4 Sugam Form For Assessment Year 2018 19Document9 pagesITR 4 Sugam Form For Assessment Year 2018 19sureshstipl sureshNo ratings yet

- 1120-IC-DISC: Interest Charge Domestic International Sales Corporation ReturnDocument6 pages1120-IC-DISC: Interest Charge Domestic International Sales Corporation ReturnIRSNo ratings yet

- GSTR9 27aasfp7032r1za 032020Document9 pagesGSTR9 27aasfp7032r1za 032020sharad agarwalNo ratings yet

- Form 231Document14 pagesForm 231Jignesh Dinesh MewadaNo ratings yet

- Basic Act & CenvatDocument24 pagesBasic Act & CenvatrameshNo ratings yet

- April 2020 PTE 2 PathfinderDocument54 pagesApril 2020 PTE 2 PathfinderBadmus AyomideNo ratings yet

- Itctp 2022Document4 pagesItctp 2022Muskaan ShawNo ratings yet

- GSTR9 29aahcv2115k1z5 032021Document8 pagesGSTR9 29aahcv2115k1z5 032021MICO EMPLOYEES CO OPERATIVE SOCIETY LTDNo ratings yet

- 2021-09-09 Morrisons Interim AnnouncementDocument48 pages2021-09-09 Morrisons Interim AnnouncementBassel HagagNo ratings yet

- US Internal Revenue Service: f4562 - 1992Document2 pagesUS Internal Revenue Service: f4562 - 1992IRSNo ratings yet

- Form Vat - IiiDocument4 pagesForm Vat - IiihrsolutionNo ratings yet

- Imp Questions Eco Part 1Document28 pagesImp Questions Eco Part 1sansarnathNo ratings yet

- 2008 Objectives Report To Congress v2Document153 pages2008 Objectives Report To Congress v2IRSNo ratings yet

- US Internal Revenue Service: 2290rulesty2007v4 0Document6 pagesUS Internal Revenue Service: 2290rulesty2007v4 0IRSNo ratings yet

- 2008 Credit Card Bulk Provider RequirementsDocument112 pages2008 Credit Card Bulk Provider RequirementsIRSNo ratings yet

- 2008 Data DictionaryDocument260 pages2008 Data DictionaryIRSNo ratings yet

- 2 ADocument8 pages2 AMayur PatelNo ratings yet

- Basic Welding TheoryDocument15 pagesBasic Welding TheoryCarina MostralesNo ratings yet

- Fem DamageDocument13 pagesFem DamageGerard VelicariaNo ratings yet

- Classical Theory of DetonationDocument20 pagesClassical Theory of Detonationalexander.lhoistNo ratings yet

- Boiler Steam To ProcessDocument9 pagesBoiler Steam To ProcessMDR PRAPHUNo ratings yet

- HTLP-80 Application ProcedureDocument9 pagesHTLP-80 Application ProceduremaheshNo ratings yet

- RNAprotect Cell Reagent HandbookDocument40 pagesRNAprotect Cell Reagent HandbookSergio MugnaiNo ratings yet

- BS 6683 (1985) Installation and Use of ValvesDocument18 pagesBS 6683 (1985) Installation and Use of Valves김창배No ratings yet

- Standart Cina Untuk WeldingDocument52 pagesStandart Cina Untuk Weldingandristy90No ratings yet

- Prep. BUROW'S SOLUTIONDocument1 pagePrep. BUROW'S SOLUTIONJoanna Carla Marmonejo Estorninos-Walker100% (1)

- Toxicology - Lesson Plan - KnightonDocument7 pagesToxicology - Lesson Plan - Knightonapi-257588494100% (1)

- ExerciseDocument4 pagesExerciseariefnur19No ratings yet

- How To Eliminatdadde Outgassing, The Powder Coating Faux PasDocument2 pagesHow To Eliminatdadde Outgassing, The Powder Coating Faux PasSandra ArianaNo ratings yet

- Flexural Behavior of RC Beam Strengthened With Carbon Fiber Sheets in Shear and Flexure ZoneDocument38 pagesFlexural Behavior of RC Beam Strengthened With Carbon Fiber Sheets in Shear and Flexure ZoneFrances Sol TumulakNo ratings yet

- ASTM DIN Equivalent MaterialsDocument6 pagesASTM DIN Equivalent MaterialsCandra Saja63% (8)

- Research Article: Determination of Ranitidine in Human Plasma by SPE and ESI-LC-MS/MS For Use in Bioequivalence StudiesDocument8 pagesResearch Article: Determination of Ranitidine in Human Plasma by SPE and ESI-LC-MS/MS For Use in Bioequivalence StudiesSrujana BudheNo ratings yet

- BIOplastics Catalog2010Document129 pagesBIOplastics Catalog2010Enrico SchicchiNo ratings yet

- Ophthalmics Brochure 1015 Lay2Document36 pagesOphthalmics Brochure 1015 Lay2nadjib62100% (2)

- Thermo Dynamics Question BankDocument3 pagesThermo Dynamics Question Banknisar_ulNo ratings yet

- Water Quality Analysis of Nairobi DamDocument43 pagesWater Quality Analysis of Nairobi DamOrwe Elly100% (1)

- Ethylene Glycol CAS No 107-21-1: Material Safety Data Sheet Sds/MsdsDocument7 pagesEthylene Glycol CAS No 107-21-1: Material Safety Data Sheet Sds/MsdsRyanNo ratings yet

- Advanced Finishing ProcessesDocument23 pagesAdvanced Finishing ProcessesADWAITH G SNo ratings yet

- 202 TA 202A Introduction To Manufacturing ProcessesDocument20 pages202 TA 202A Introduction To Manufacturing ProcessesshubhamNo ratings yet

- Presentasi Sesi 2 Webinar Bromat AMDKDocument46 pagesPresentasi Sesi 2 Webinar Bromat AMDKAOC BPOM Jambi 2022No ratings yet

- Thermal Properties of MaterialsDocument6 pagesThermal Properties of Materialsdhanya1995No ratings yet

- 100 All Greatest Popular Science BooksDocument9 pages100 All Greatest Popular Science BooksJaime Messía100% (2)

- SW13494 - Heat-Flex - 3500. Loai Thay The Bao On PDFDocument2 pagesSW13494 - Heat-Flex - 3500. Loai Thay The Bao On PDFtienNo ratings yet

- Pupuk PT SSA PDFDocument2 pagesPupuk PT SSA PDFNurul HardiyantiNo ratings yet

- Stoichiometry and Process Calculations - K. V. Narayanan and B. Lakshmikutty PDFDocument167 pagesStoichiometry and Process Calculations - K. V. Narayanan and B. Lakshmikutty PDFSarah SanchezNo ratings yet

- ShilajitDocument13 pagesShilajitpseudo3No ratings yet