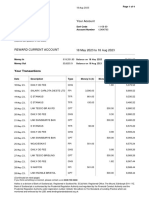

ATM Project Final

ATM Project Final

You might also like

- Your Consolidated Statement: Contact UsDocument5 pagesYour Consolidated Statement: Contact UsSAM50% (2)

- Halifax Statement 2023 08 18Document4 pagesHalifax Statement 2023 08 18VALENTIN SHABLIKANo ratings yet

- 555Document90 pages555Netflix Familia57% (7)

- Synergy (Elec)Document3 pagesSynergy (Elec)Aleksania NolanNo ratings yet

- Credit Card Fraud DetectionDocument95 pagesCredit Card Fraud DetectionMadhu Evuri0% (1)

- HOW TO BUY GOOD - LIVE CC FROM SHOP by DC PDFDocument26 pagesHOW TO BUY GOOD - LIVE CC FROM SHOP by DC PDFВиталий Мак100% (7)

- Atmdesk X: User'S ManualDocument95 pagesAtmdesk X: User'S ManualMohammed Murtala Mohammed0% (1)

- ATM Simulator: PHP ProjectDocument22 pagesATM Simulator: PHP ProjectBhushan TalwareNo ratings yet

- Blackbook Project On AtmDocument68 pagesBlackbook Project On AtmSamiksha Naik50% (6)

- Study of Atm and Deposit MachineDocument58 pagesStudy of Atm and Deposit MachineManpreetSinghRajput60% (5)

- Project On AtmDocument51 pagesProject On Atmashwin_nakman77% (53)

- A Micro-Project Report ON: "Latest ATM Security''Document19 pagesA Micro-Project Report ON: "Latest ATM Security''Kashyap PathakNo ratings yet

- Project Report: Atm Management SystemDocument47 pagesProject Report: Atm Management SystemRohit Kumar100% (1)

- Atm With An EyeDocument25 pagesAtm With An EyeKiran StridesNo ratings yet

- ATM ProjectDocument88 pagesATM ProjectRajat BansalNo ratings yet

- Finger AtmDocument74 pagesFinger Atmஸ்ரீ கண்ணன்No ratings yet

- Technical Seminar On Automatic Teller Machine by Using BiometricsDocument23 pagesTechnical Seminar On Automatic Teller Machine by Using BiometricsNAGMA SULTANANo ratings yet

- PSG College of Technology: Mohanan.D Monish ChallaDocument25 pagesPSG College of Technology: Mohanan.D Monish ChallaKumaran SgNo ratings yet

- Mobile Payments Landscape Two Years LaterDocument28 pagesMobile Payments Landscape Two Years LaterhdreifusNo ratings yet

- Credit Card Fraud Detection1Document5 pagesCredit Card Fraud Detection1Yachna DharwalNo ratings yet

- ATM Reporting System ReportDocument6 pagesATM Reporting System ReportTabish AlmasNo ratings yet

- ATM Management SystemDocument5 pagesATM Management Systemvijimudaliar100% (1)

- ON Atm SecurityDocument14 pagesON Atm SecurityShashankShekharNo ratings yet

- Cardless ATMDocument26 pagesCardless ATMWebhub Technology100% (1)

- The Popularity of Diffrent Utilities Atms CardsDocument29 pagesThe Popularity of Diffrent Utilities Atms CardsMaruti a alavandiNo ratings yet

- Customer Satisfaction With Regard To ATM ServicesDocument75 pagesCustomer Satisfaction With Regard To ATM Servicesdinesh_v_0076945100% (2)

- ATM Card OTP VerificationDocument7 pagesATM Card OTP VerificationMansoorSulaiman100% (1)

- Cyber Crime Project LawDocument5 pagesCyber Crime Project LawSrinivas PrabhuNo ratings yet

- Paytm NewDocument12 pagesPaytm NewPriya Naveen0% (1)

- 19 Smart CardsDocument48 pages19 Smart CardsZalak RakholiyaNo ratings yet

- Money PadDocument15 pagesMoney PadAnvita_Jain_2921No ratings yet

- Atm SystemDocument6 pagesAtm SystemJaydip PatelNo ratings yet

- ATM Management SystemDocument2 pagesATM Management SystemKanu Priya100% (1)

- Biometrics in Secure E-TransactionDocument4 pagesBiometrics in Secure E-TransactionREx Ethics100% (1)

- Security Features of AtmDocument5 pagesSecurity Features of AtmPrasanth Naik0% (1)

- Cyber Security Measures For BanksDocument31 pagesCyber Security Measures For BanksArno CommunicationsNo ratings yet

- India Banking Fraud Survey: Edition IIDocument36 pagesIndia Banking Fraud Survey: Edition IIAkash SahuNo ratings yet

- Project Book of AtmDocument35 pagesProject Book of Atmpavan puppalaNo ratings yet

- Credit Card Fraud Detection Using Machine Learning FINALDocument8 pagesCredit Card Fraud Detection Using Machine Learning FINALSanobar khanNo ratings yet

- Unit-3 Electronic Payment SystemDocument12 pagesUnit-3 Electronic Payment SystemNezuko KamadoNo ratings yet

- Strategies and Techniques of Banking Security and ATMsDocument6 pagesStrategies and Techniques of Banking Security and ATMsVIVA-TECH IJRINo ratings yet

- Atm Switch RFPDocument77 pagesAtm Switch RFPRishi SrivastavaNo ratings yet

- Effect of Cashless Payment Methods A Case Study Perspective AnalysisDocument4 pagesEffect of Cashless Payment Methods A Case Study Perspective AnalysisAaryan Singh100% (1)

- Behavior Based Credit Card Fraud Detection Using Support VectorDocument7 pagesBehavior Based Credit Card Fraud Detection Using Support VectoryayaretyNo ratings yet

- ATM DescriptionDocument8 pagesATM DescriptionKomal SrivastavNo ratings yet

- Credit Fraud Detection in The Banking SectorDocument6 pagesCredit Fraud Detection in The Banking SectorAli MonNo ratings yet

- Atm ProjectDocument17 pagesAtm ProjectSreyoshi Shoili100% (2)

- Debit Card - Project Wark PDFDocument158 pagesDebit Card - Project Wark PDFManisha GuptaNo ratings yet

- Online Banking AbstractDocument14 pagesOnline Banking AbstractNeelanjal Singh100% (2)

- Atm ReportDocument25 pagesAtm ReportUmer AhmedNo ratings yet

- E Wallet 161115013135 PDFDocument79 pagesE Wallet 161115013135 PDFahsan habibNo ratings yet

- Atm SoftwareDocument93 pagesAtm SoftwareHemant Kumar50% (2)

- Improving Security Challeges of Atm System in Commercial Bank of Ethiopia: The Case of Wolaita Zone, Sodo CityDocument21 pagesImproving Security Challeges of Atm System in Commercial Bank of Ethiopia: The Case of Wolaita Zone, Sodo CityInternational Journal of Application or Innovation in Engineering & ManagementNo ratings yet

- Money Pad The Future WalletDocument17 pagesMoney Pad The Future WalletUsha Madanala0% (1)

- Automated Teller MachineDocument35 pagesAutomated Teller MachineDeepak SinghNo ratings yet

- Internal Guide Presented by N Nikhila Gayathri MR.S Sanjeeva Rao (Associate Professor)Document18 pagesInternal Guide Presented by N Nikhila Gayathri MR.S Sanjeeva Rao (Associate Professor)NikhilaNo ratings yet

- PPT18Document27 pagesPPT18Dev KumarNo ratings yet

- EMTM 553: E-Commerce Systems: Lecture 8: Electronic Payment SystemsDocument59 pagesEMTM 553: E-Commerce Systems: Lecture 8: Electronic Payment SystemsD Attitude KidNo ratings yet

- Sejal UpadhyayDocument55 pagesSejal UpadhyaySunita BishtNo ratings yet

- Name: Amishi Trivedi Div: A1 ROLL NO: 1111Document6 pagesName: Amishi Trivedi Div: A1 ROLL NO: 1111Amishi TrivediNo ratings yet

- ATM - Machine New 22Document13 pagesATM - Machine New 22Likhil 18No ratings yet

- مشروع شرف شانعDocument10 pagesمشروع شرف شانعNiyaz AlbaseerNo ratings yet

- "A Study of Atm & Deposit Machine": Submitted by Rajput Manpreet Singh Under The Guidance of Prof. Samma NarangDocument52 pages"A Study of Atm & Deposit Machine": Submitted by Rajput Manpreet Singh Under The Guidance of Prof. Samma NarangManpreetSinghRajputNo ratings yet

- Project On AtmDocument51 pagesProject On AtmtriratnacomNo ratings yet

- BM2409I002842761Document10 pagesBM2409I002842761Abhishek SinhaNo ratings yet

- Bojo Rad Receipt, 7-12, IT Return, PDFDocument15 pagesBojo Rad Receipt, 7-12, IT Return, PDFn2ulooteraNo ratings yet

- HDFC HistoryDocument4 pagesHDFC HistoryRavi KumarNo ratings yet

- EPDQ One Page Checkout Alias GatewayDocument12 pagesEPDQ One Page Checkout Alias GatewayCarlos I. AparicioNo ratings yet

- Statement June and JulyDocument2 pagesStatement June and JulyGregory Scarpa SnrNo ratings yet

- IVeri WebAPI Developers GuideDocument18 pagesIVeri WebAPI Developers GuidedefamaNo ratings yet

- R & D Report SampleDocument49 pagesR & D Report SampleAkhil PtNo ratings yet

- Buy Bitcoin With A Credit or Debit Card Online or at An ATM - CoinFlipDocument1 pageBuy Bitcoin With A Credit or Debit Card Online or at An ATM - CoinFlipOJO Ayodeji damilolaNo ratings yet

- Sample Project - A Comparative Study of E-Banking ServicesDocument57 pagesSample Project - A Comparative Study of E-Banking ServicesAloysius BhuiyaNo ratings yet

- (Indusind Bank) : Summer Training Project Report OnDocument48 pages(Indusind Bank) : Summer Training Project Report OnAkash SrivastavaNo ratings yet

- Amway August 2014 PromotionDocument27 pagesAmway August 2014 PromotionAmbrose TaiNo ratings yet

- QVSDC IRWIN Testing ProcessDocument8 pagesQVSDC IRWIN Testing ProcessLewisMuneneNo ratings yet

- TenderDocument8 pagesTenderzaheerNo ratings yet

- Invoice No. Credit Analysis File: No. Guarantee File:: Page 5Document2 pagesInvoice No. Credit Analysis File: No. Guarantee File:: Page 5Erica EdgecombeNo ratings yet

- Consumer Protection Framework No.1-2017/BSDDocument37 pagesConsumer Protection Framework No.1-2017/BSDLucky MurindaNo ratings yet

- Undergraduate Project Report TECNO LINK FinalDocument60 pagesUndergraduate Project Report TECNO LINK FinalBontu GirmaNo ratings yet

- Online Giro Form PDFDocument3 pagesOnline Giro Form PDFDing Zheng YangNo ratings yet

- January 2023 Bank AccountDocument4 pagesJanuary 2023 Bank AccountleratokwNo ratings yet

- RandomDocument4 pagesRandomBarnendu SarkarNo ratings yet

- Details As at 01 Jun 2023, 09:54 GMTDocument3 pagesDetails As at 01 Jun 2023, 09:54 GMT19831a0484No ratings yet

- The Future of Payments: India Digital Payments ReportDocument24 pagesThe Future of Payments: India Digital Payments ReporttanmayamohanNo ratings yet

- Stripe Tax Invoice JNSYY48Q-2023-02Document2 pagesStripe Tax Invoice JNSYY48Q-2023-02ahmed abdoNo ratings yet

- Entrance Examinations For Admission To Engineering/ Medical & Allied Courses, Kerala 2016Document8 pagesEntrance Examinations For Admission To Engineering/ Medical & Allied Courses, Kerala 2016anishthNo ratings yet

- Grade Xi HOLIDAY HOMEWORK-2016-17 Commerce Stream AccountancyDocument36 pagesGrade Xi HOLIDAY HOMEWORK-2016-17 Commerce Stream AccountancysanjeevaniNo ratings yet

- NHOP - Technology Solutions Agreement For SP Hotels - 04.30.21Document10 pagesNHOP - Technology Solutions Agreement For SP Hotels - 04.30.21Jonathan MesquitaNo ratings yet

Download as docx, pdf, or txt

You might also like

- Your Consolidated Statement: Contact UsDocument5 pagesYour Consolidated Statement: Contact UsSAM50% (2)

- Halifax Statement 2023 08 18Document4 pagesHalifax Statement 2023 08 18VALENTIN SHABLIKANo ratings yet

- 555Document90 pages555Netflix Familia57% (7)

- Synergy (Elec)Document3 pagesSynergy (Elec)Aleksania NolanNo ratings yet

- Credit Card Fraud DetectionDocument95 pagesCredit Card Fraud DetectionMadhu Evuri0% (1)

- HOW TO BUY GOOD - LIVE CC FROM SHOP by DC PDFDocument26 pagesHOW TO BUY GOOD - LIVE CC FROM SHOP by DC PDFВиталий Мак100% (7)

- Atmdesk X: User'S ManualDocument95 pagesAtmdesk X: User'S ManualMohammed Murtala Mohammed0% (1)

- ATM Simulator: PHP ProjectDocument22 pagesATM Simulator: PHP ProjectBhushan TalwareNo ratings yet

- Blackbook Project On AtmDocument68 pagesBlackbook Project On AtmSamiksha Naik50% (6)

- Study of Atm and Deposit MachineDocument58 pagesStudy of Atm and Deposit MachineManpreetSinghRajput60% (5)

- Project On AtmDocument51 pagesProject On Atmashwin_nakman77% (53)

- A Micro-Project Report ON: "Latest ATM Security''Document19 pagesA Micro-Project Report ON: "Latest ATM Security''Kashyap PathakNo ratings yet

- Project Report: Atm Management SystemDocument47 pagesProject Report: Atm Management SystemRohit Kumar100% (1)

- Atm With An EyeDocument25 pagesAtm With An EyeKiran StridesNo ratings yet

- ATM ProjectDocument88 pagesATM ProjectRajat BansalNo ratings yet

- Finger AtmDocument74 pagesFinger Atmஸ்ரீ கண்ணன்No ratings yet

- Technical Seminar On Automatic Teller Machine by Using BiometricsDocument23 pagesTechnical Seminar On Automatic Teller Machine by Using BiometricsNAGMA SULTANANo ratings yet

- PSG College of Technology: Mohanan.D Monish ChallaDocument25 pagesPSG College of Technology: Mohanan.D Monish ChallaKumaran SgNo ratings yet

- Mobile Payments Landscape Two Years LaterDocument28 pagesMobile Payments Landscape Two Years LaterhdreifusNo ratings yet

- Credit Card Fraud Detection1Document5 pagesCredit Card Fraud Detection1Yachna DharwalNo ratings yet

- ATM Reporting System ReportDocument6 pagesATM Reporting System ReportTabish AlmasNo ratings yet

- ATM Management SystemDocument5 pagesATM Management Systemvijimudaliar100% (1)

- ON Atm SecurityDocument14 pagesON Atm SecurityShashankShekharNo ratings yet

- Cardless ATMDocument26 pagesCardless ATMWebhub Technology100% (1)

- The Popularity of Diffrent Utilities Atms CardsDocument29 pagesThe Popularity of Diffrent Utilities Atms CardsMaruti a alavandiNo ratings yet

- Customer Satisfaction With Regard To ATM ServicesDocument75 pagesCustomer Satisfaction With Regard To ATM Servicesdinesh_v_0076945100% (2)

- ATM Card OTP VerificationDocument7 pagesATM Card OTP VerificationMansoorSulaiman100% (1)

- Cyber Crime Project LawDocument5 pagesCyber Crime Project LawSrinivas PrabhuNo ratings yet

- Paytm NewDocument12 pagesPaytm NewPriya Naveen0% (1)

- 19 Smart CardsDocument48 pages19 Smart CardsZalak RakholiyaNo ratings yet

- Money PadDocument15 pagesMoney PadAnvita_Jain_2921No ratings yet

- Atm SystemDocument6 pagesAtm SystemJaydip PatelNo ratings yet

- ATM Management SystemDocument2 pagesATM Management SystemKanu Priya100% (1)

- Biometrics in Secure E-TransactionDocument4 pagesBiometrics in Secure E-TransactionREx Ethics100% (1)

- Security Features of AtmDocument5 pagesSecurity Features of AtmPrasanth Naik0% (1)

- Cyber Security Measures For BanksDocument31 pagesCyber Security Measures For BanksArno CommunicationsNo ratings yet

- India Banking Fraud Survey: Edition IIDocument36 pagesIndia Banking Fraud Survey: Edition IIAkash SahuNo ratings yet

- Project Book of AtmDocument35 pagesProject Book of Atmpavan puppalaNo ratings yet

- Credit Card Fraud Detection Using Machine Learning FINALDocument8 pagesCredit Card Fraud Detection Using Machine Learning FINALSanobar khanNo ratings yet

- Unit-3 Electronic Payment SystemDocument12 pagesUnit-3 Electronic Payment SystemNezuko KamadoNo ratings yet

- Strategies and Techniques of Banking Security and ATMsDocument6 pagesStrategies and Techniques of Banking Security and ATMsVIVA-TECH IJRINo ratings yet

- Atm Switch RFPDocument77 pagesAtm Switch RFPRishi SrivastavaNo ratings yet

- Effect of Cashless Payment Methods A Case Study Perspective AnalysisDocument4 pagesEffect of Cashless Payment Methods A Case Study Perspective AnalysisAaryan Singh100% (1)

- Behavior Based Credit Card Fraud Detection Using Support VectorDocument7 pagesBehavior Based Credit Card Fraud Detection Using Support VectoryayaretyNo ratings yet

- ATM DescriptionDocument8 pagesATM DescriptionKomal SrivastavNo ratings yet

- Credit Fraud Detection in The Banking SectorDocument6 pagesCredit Fraud Detection in The Banking SectorAli MonNo ratings yet

- Atm ProjectDocument17 pagesAtm ProjectSreyoshi Shoili100% (2)

- Debit Card - Project Wark PDFDocument158 pagesDebit Card - Project Wark PDFManisha GuptaNo ratings yet

- Online Banking AbstractDocument14 pagesOnline Banking AbstractNeelanjal Singh100% (2)

- Atm ReportDocument25 pagesAtm ReportUmer AhmedNo ratings yet

- E Wallet 161115013135 PDFDocument79 pagesE Wallet 161115013135 PDFahsan habibNo ratings yet

- Atm SoftwareDocument93 pagesAtm SoftwareHemant Kumar50% (2)

- Improving Security Challeges of Atm System in Commercial Bank of Ethiopia: The Case of Wolaita Zone, Sodo CityDocument21 pagesImproving Security Challeges of Atm System in Commercial Bank of Ethiopia: The Case of Wolaita Zone, Sodo CityInternational Journal of Application or Innovation in Engineering & ManagementNo ratings yet

- Money Pad The Future WalletDocument17 pagesMoney Pad The Future WalletUsha Madanala0% (1)

- Automated Teller MachineDocument35 pagesAutomated Teller MachineDeepak SinghNo ratings yet

- Internal Guide Presented by N Nikhila Gayathri MR.S Sanjeeva Rao (Associate Professor)Document18 pagesInternal Guide Presented by N Nikhila Gayathri MR.S Sanjeeva Rao (Associate Professor)NikhilaNo ratings yet

- PPT18Document27 pagesPPT18Dev KumarNo ratings yet

- EMTM 553: E-Commerce Systems: Lecture 8: Electronic Payment SystemsDocument59 pagesEMTM 553: E-Commerce Systems: Lecture 8: Electronic Payment SystemsD Attitude KidNo ratings yet

- Sejal UpadhyayDocument55 pagesSejal UpadhyaySunita BishtNo ratings yet

- Name: Amishi Trivedi Div: A1 ROLL NO: 1111Document6 pagesName: Amishi Trivedi Div: A1 ROLL NO: 1111Amishi TrivediNo ratings yet

- ATM - Machine New 22Document13 pagesATM - Machine New 22Likhil 18No ratings yet

- مشروع شرف شانعDocument10 pagesمشروع شرف شانعNiyaz AlbaseerNo ratings yet

- "A Study of Atm & Deposit Machine": Submitted by Rajput Manpreet Singh Under The Guidance of Prof. Samma NarangDocument52 pages"A Study of Atm & Deposit Machine": Submitted by Rajput Manpreet Singh Under The Guidance of Prof. Samma NarangManpreetSinghRajputNo ratings yet

- Project On AtmDocument51 pagesProject On AtmtriratnacomNo ratings yet

- BM2409I002842761Document10 pagesBM2409I002842761Abhishek SinhaNo ratings yet

- Bojo Rad Receipt, 7-12, IT Return, PDFDocument15 pagesBojo Rad Receipt, 7-12, IT Return, PDFn2ulooteraNo ratings yet

- HDFC HistoryDocument4 pagesHDFC HistoryRavi KumarNo ratings yet

- EPDQ One Page Checkout Alias GatewayDocument12 pagesEPDQ One Page Checkout Alias GatewayCarlos I. AparicioNo ratings yet

- Statement June and JulyDocument2 pagesStatement June and JulyGregory Scarpa SnrNo ratings yet

- IVeri WebAPI Developers GuideDocument18 pagesIVeri WebAPI Developers GuidedefamaNo ratings yet

- R & D Report SampleDocument49 pagesR & D Report SampleAkhil PtNo ratings yet

- Buy Bitcoin With A Credit or Debit Card Online or at An ATM - CoinFlipDocument1 pageBuy Bitcoin With A Credit or Debit Card Online or at An ATM - CoinFlipOJO Ayodeji damilolaNo ratings yet

- Sample Project - A Comparative Study of E-Banking ServicesDocument57 pagesSample Project - A Comparative Study of E-Banking ServicesAloysius BhuiyaNo ratings yet

- (Indusind Bank) : Summer Training Project Report OnDocument48 pages(Indusind Bank) : Summer Training Project Report OnAkash SrivastavaNo ratings yet

- Amway August 2014 PromotionDocument27 pagesAmway August 2014 PromotionAmbrose TaiNo ratings yet

- QVSDC IRWIN Testing ProcessDocument8 pagesQVSDC IRWIN Testing ProcessLewisMuneneNo ratings yet

- TenderDocument8 pagesTenderzaheerNo ratings yet

- Invoice No. Credit Analysis File: No. Guarantee File:: Page 5Document2 pagesInvoice No. Credit Analysis File: No. Guarantee File:: Page 5Erica EdgecombeNo ratings yet

- Consumer Protection Framework No.1-2017/BSDDocument37 pagesConsumer Protection Framework No.1-2017/BSDLucky MurindaNo ratings yet

- Undergraduate Project Report TECNO LINK FinalDocument60 pagesUndergraduate Project Report TECNO LINK FinalBontu GirmaNo ratings yet

- Online Giro Form PDFDocument3 pagesOnline Giro Form PDFDing Zheng YangNo ratings yet

- January 2023 Bank AccountDocument4 pagesJanuary 2023 Bank AccountleratokwNo ratings yet

- RandomDocument4 pagesRandomBarnendu SarkarNo ratings yet

- Details As at 01 Jun 2023, 09:54 GMTDocument3 pagesDetails As at 01 Jun 2023, 09:54 GMT19831a0484No ratings yet

- The Future of Payments: India Digital Payments ReportDocument24 pagesThe Future of Payments: India Digital Payments ReporttanmayamohanNo ratings yet

- Stripe Tax Invoice JNSYY48Q-2023-02Document2 pagesStripe Tax Invoice JNSYY48Q-2023-02ahmed abdoNo ratings yet

- Entrance Examinations For Admission To Engineering/ Medical & Allied Courses, Kerala 2016Document8 pagesEntrance Examinations For Admission To Engineering/ Medical & Allied Courses, Kerala 2016anishthNo ratings yet

- Grade Xi HOLIDAY HOMEWORK-2016-17 Commerce Stream AccountancyDocument36 pagesGrade Xi HOLIDAY HOMEWORK-2016-17 Commerce Stream AccountancysanjeevaniNo ratings yet

- NHOP - Technology Solutions Agreement For SP Hotels - 04.30.21Document10 pagesNHOP - Technology Solutions Agreement For SP Hotels - 04.30.21Jonathan MesquitaNo ratings yet