Download as docx, pdf, or txt

You might also like

- Handover NotesDocument4 pagesHandover NotesYAKUBU BABA TIJANINo ratings yet

- Bonifacio BrosDocument5 pagesBonifacio BrosRenNo ratings yet

- Bonifacio Brothers vs. Mora, G.R. No. 20853, 1967Document4 pagesBonifacio Brothers vs. Mora, G.R. No. 20853, 1967Nikko AlelojoNo ratings yet

- Bonifacio Vs MoraDocument3 pagesBonifacio Vs MoraClaudine Christine A. VicenteNo ratings yet

- BonifacioDocument4 pagesBonifaciospecialsectionNo ratings yet

- Insurance Parts Vii IxDocument28 pagesInsurance Parts Vii Ixdorothy annNo ratings yet

- Ins 0830Document31 pagesIns 0830Isa AriasNo ratings yet

- Bonifacio Brothers V MoraDocument5 pagesBonifacio Brothers V MoraJubelle AngeliNo ratings yet

- Bonifacio Bros Vs MoraDocument3 pagesBonifacio Bros Vs MoraGigiRuizTicarNo ratings yet

- BONIFACIO BROS. vs. MORADocument3 pagesBONIFACIO BROS. vs. MORArosellerbucog_437907No ratings yet

- Bonifacio Bros Vs MoraDocument2 pagesBonifacio Bros Vs MoraElerlenne LimNo ratings yet

- Plaintiffs-Appellants vs. vs. Defendants-Appellees G. Magsaysay Abad Santos & Pablo J. P. Santilla & A. D. Hidalgo, JRDocument5 pagesPlaintiffs-Appellants vs. vs. Defendants-Appellees G. Magsaysay Abad Santos & Pablo J. P. Santilla & A. D. Hidalgo, JRVictoria EscobalNo ratings yet

- 43-Bonifacio Bros. vs. Mora, 20 SCRA 261Document4 pages43-Bonifacio Bros. vs. Mora, 20 SCRA 261Jopan SJNo ratings yet

- Bonifacio Bros vs. MoraDocument2 pagesBonifacio Bros vs. MoraBryan Jay NuiqueNo ratings yet

- DOCTRINE: Mora Mortgaged His Car With H.S. Reyes With TheDocument2 pagesDOCTRINE: Mora Mortgaged His Car With H.S. Reyes With TheAnonymous ifiHUmxNo ratings yet

- Bonifacio Bro Vs MoraDocument4 pagesBonifacio Bro Vs MoraLeigh BarcelonaNo ratings yet

- Insurance Case DigestsDocument4 pagesInsurance Case DigestsBing MiloNo ratings yet

- Bro MoraDocument2 pagesBro MoraRichmon BataoilNo ratings yet

- Bonifacio Bros V MoraDocument2 pagesBonifacio Bros V MoraOwdylyn Lee100% (2)

- VOL. 20, MAY 29, 1967 261: Bonifacio Bros., Inc. vs. MoraDocument8 pagesVOL. 20, MAY 29, 1967 261: Bonifacio Bros., Inc. vs. Morabrida athenaNo ratings yet

- 243 Bonifacio Bros. V. Mora (1967) (Stipulation Pour Autrui)Document3 pages243 Bonifacio Bros. V. Mora (1967) (Stipulation Pour Autrui)Ahmed Gakusei100% (1)

- Bonifacio Vs MoraDocument2 pagesBonifacio Vs MoraMan2x SalomonNo ratings yet

- Bonifacio Brothers Inc V Mora DigestDocument2 pagesBonifacio Brothers Inc V Mora DigestAbigail TolabingNo ratings yet

- Insurance Cases Summer (Digests)Document3 pagesInsurance Cases Summer (Digests)Glyza Kaye Zorilla PatiagNo ratings yet

- 20 Scra 261Document2 pages20 Scra 261acesmaelNo ratings yet

- Digest For Bonifacio Bros V MoraDocument2 pagesDigest For Bonifacio Bros V Moracookbooks&lawbooksNo ratings yet

- Bonifacio Bros. v. Mora: 20 SCRA 262Document2 pagesBonifacio Bros. v. Mora: 20 SCRA 262Tahani Awar GurarNo ratings yet

- Bonifacio Bros Vs MoraDocument2 pagesBonifacio Bros Vs MoraOmar Nasseef BakongNo ratings yet

- Misamis Lumber Corp. v. Capital InsuranceDocument3 pagesMisamis Lumber Corp. v. Capital InsuranceLDCNo ratings yet

- Bonifacio Brothers v. Mora, 20 SCRA 261Document2 pagesBonifacio Brothers v. Mora, 20 SCRA 261Sopongco ColeenNo ratings yet

- 18 Misamis Lumber Corp. vs. Capital Ins. & Surety Co., Inc. 17 SCRA 228, May 20, 1966Document5 pages18 Misamis Lumber Corp. vs. Capital Ins. & Surety Co., Inc. 17 SCRA 228, May 20, 1966joyeduardoNo ratings yet

- Insurance 1Document17 pagesInsurance 1Monica MoranteNo ratings yet

- American Fidelity and Casualty Company v. Huston L. Simmons, 253 F.2d 634, 4th Cir. (1958)Document4 pagesAmerican Fidelity and Casualty Company v. Huston L. Simmons, 253 F.2d 634, 4th Cir. (1958)Scribd Government DocsNo ratings yet

- Insurance 2nd Exam CasesDocument12 pagesInsurance 2nd Exam CasesAmanda ButtkissNo ratings yet

- Taurus Taxi v. Capital Insurance G.R. No. L-23491Document3 pagesTaurus Taxi v. Capital Insurance G.R. No. L-23491Tin LicoNo ratings yet

- Compilation Insurance b3Document14 pagesCompilation Insurance b3Eunice SerneoNo ratings yet

- 28 - Misamis Lumber Corp. v. Capital Insurance & Surety Co., Inc PDFDocument3 pages28 - Misamis Lumber Corp. v. Capital Insurance & Surety Co., Inc PDFKaryl Eric BardelasNo ratings yet

- TAURUS TAXI CO., INC. vs. THE CAPITAL INSURANCE & SURETY CODocument2 pagesTAURUS TAXI CO., INC. vs. THE CAPITAL INSURANCE & SURETY COTin LicoNo ratings yet

- Qua Chee Gan V. Law Union and Rockinsurance Co. LTD.: Pioneer V Yap G.R. No. L-36232 December 19, 1974Document4 pagesQua Chee Gan V. Law Union and Rockinsurance Co. LTD.: Pioneer V Yap G.R. No. L-36232 December 19, 1974dianneNo ratings yet

- Stickel v. Excess Ins. CoDocument5 pagesStickel v. Excess Ins. CoEdmundo ArráizNo ratings yet

- Enrique Mora HS Reyes Inc: #32 Bonifacio Bros. v. Mora 20 SCRA 262 FactsDocument5 pagesEnrique Mora HS Reyes Inc: #32 Bonifacio Bros. v. Mora 20 SCRA 262 FactsEdward Kenneth KungNo ratings yet

- Insurance Law Cases Digests NORSUDocument21 pagesInsurance Law Cases Digests NORSUVinci Poncardas100% (1)

- Taurus Taxi Vs Capital Inusrance GR No 13491 24 Scra 454Document4 pagesTaurus Taxi Vs Capital Inusrance GR No 13491 24 Scra 454crizaldedNo ratings yet

- Case Digest InsuranceDocument11 pagesCase Digest InsuranceJoshua Talavera-TanNo ratings yet

- Taurus Taxi vs. Capital InsuranceDocument4 pagesTaurus Taxi vs. Capital InsuranceTin RamosNo ratings yet

- 5-Rizal Surety Vs Manila RailroadDocument3 pages5-Rizal Surety Vs Manila RailroadJoan Dela CruzNo ratings yet

- OneBeacon America v. Leasing Associates, 465 F.3d 38, 1st Cir. (2006)Document11 pagesOneBeacon America v. Leasing Associates, 465 F.3d 38, 1st Cir. (2006)Scribd Government DocsNo ratings yet

- (Note! Comparison Between This Case and Malayan Case-In The Malayan Case Cited by Keihin-Everett, Malayan NotDocument29 pages(Note! Comparison Between This Case and Malayan Case-In The Malayan Case Cited by Keihin-Everett, Malayan NotFerdinand PadillaNo ratings yet

- Case Digest InsuranceDocument4 pagesCase Digest InsuranceRaffy Roncales100% (1)

- Insurance Last CasesDocument6 pagesInsurance Last CasesADNo ratings yet

- Set 1 Digest PrelimsDocument8 pagesSet 1 Digest PrelimsJoni PurayNo ratings yet

- Abrogation of Its Express Terms, Terms Which The Insured Accepted or Adhered To and Which Is The Law Between The Contracting PartiesDocument19 pagesAbrogation of Its Express Terms, Terms Which The Insured Accepted or Adhered To and Which Is The Law Between The Contracting PartiesDenise GordonNo ratings yet

- Insurance Felipe Vs MGM Great Pacific V CADocument18 pagesInsurance Felipe Vs MGM Great Pacific V CAKim EstalNo ratings yet

- Misamis Lumber Corp v. Capital Dev. Surety Co.Document2 pagesMisamis Lumber Corp v. Capital Dev. Surety Co.Roland OliquinoNo ratings yet

- Bonifacio V MoraDocument1 pageBonifacio V MoraPraisah Marjorey PicotNo ratings yet

- Coquia vs. Fieldmen's Insurance Co., Inc.: 178 Supreme Court Reports AnnotatedDocument6 pagesCoquia vs. Fieldmen's Insurance Co., Inc.: 178 Supreme Court Reports AnnotatedHalin GayNo ratings yet

- Case 14Document3 pagesCase 14William DC RiveraNo ratings yet

- Taurus Taxi Co Inc v. The Capital Insurance Surety Co IncDocument3 pagesTaurus Taxi Co Inc v. The Capital Insurance Surety Co IncShiela PilarNo ratings yet

- 10) Rizal Surety & Insurance Co. vs. Manila Railroad Company, 23 SCRA 205, No. L-24043 April 25, 1968Document4 pages10) Rizal Surety & Insurance Co. vs. Manila Railroad Company, 23 SCRA 205, No. L-24043 April 25, 1968Alexiss Mace JuradoNo ratings yet

- Insurance #4 Travellers V CA GR 82036 May 22 1997Document1 pageInsurance #4 Travellers V CA GR 82036 May 22 1997RoseNo ratings yet

- Understanding Named, Automatic and Additional Insureds in the CGL PolicyFrom EverandUnderstanding Named, Automatic and Additional Insureds in the CGL PolicyNo ratings yet

- Baculi Vs BattungDocument2 pagesBaculi Vs BattungGabe BedanaNo ratings yet

- Legal Research As A Fundamental Skill PDFDocument55 pagesLegal Research As A Fundamental Skill PDFGabe BedanaNo ratings yet

- Categorical Logic: BEDANA, Joy Gabrielle A. 1C - 2010-019022Document11 pagesCategorical Logic: BEDANA, Joy Gabrielle A. 1C - 2010-019022Gabe BedanaNo ratings yet

- Bayani V. PeopleDocument2 pagesBayani V. PeopleGabe BedanaNo ratings yet

- Right To Vote and Attend Meetings G.R. No. L-37281 November 10, 1933 W. S. Price & The Sulu Development Company vs. H. MartinDocument15 pagesRight To Vote and Attend Meetings G.R. No. L-37281 November 10, 1933 W. S. Price & The Sulu Development Company vs. H. MartinGabe BedanaNo ratings yet

- Meryll Lynch V CaDocument7 pagesMeryll Lynch V CaGabe BedanaNo ratings yet

- Corpo 13Document3 pagesCorpo 13Gabe BedanaNo ratings yet

- REPUBLIC ACT NO. 10883, July 17, 2016 An Act Providing For A New Anti-Carnapping Law of The PhilippinesDocument16 pagesREPUBLIC ACT NO. 10883, July 17, 2016 An Act Providing For A New Anti-Carnapping Law of The PhilippinesGabe BedanaNo ratings yet

- People vs. Rapeza: IssueDocument1 pagePeople vs. Rapeza: IssueGabe BedanaNo ratings yet

- Judicial Admissions G.R. No. 181459 June 9, 2014 Commissioner of Internal Revenue, Petitioner, vs. Manila ELECTRIC COMPANY (MERALCO), RespondentDocument21 pagesJudicial Admissions G.R. No. 181459 June 9, 2014 Commissioner of Internal Revenue, Petitioner, vs. Manila ELECTRIC COMPANY (MERALCO), RespondentGabe BedanaNo ratings yet

- Corpo5 FinalDocument10 pagesCorpo5 FinalGabe BedanaNo ratings yet

- Paraffin Test Pp. vs. Tomas Sr. Ilisan vs. PeopleDocument2 pagesParaffin Test Pp. vs. Tomas Sr. Ilisan vs. PeopleGabe BedanaNo ratings yet

- Subscription Contracts G.R. No. L-5003 June 27, 1953 NAZARIO TRILLANA, Administrator-Appellee, Vs - QUEZON COLLEGE, INC., Claimant-AppellantDocument26 pagesSubscription Contracts G.R. No. L-5003 June 27, 1953 NAZARIO TRILLANA, Administrator-Appellee, Vs - QUEZON COLLEGE, INC., Claimant-AppellantGabe BedanaNo ratings yet

- Corpo 12Document17 pagesCorpo 12Gabe BedanaNo ratings yet

- Types of Dividends and Other Distributions Nielson & Co. Inc. vs. Lepanto Consolidated Mining Co. (GR. No. L-21601 December 28, 1968)Document17 pagesTypes of Dividends and Other Distributions Nielson & Co. Inc. vs. Lepanto Consolidated Mining Co. (GR. No. L-21601 December 28, 1968)Gabe BedanaNo ratings yet

- Corpo3 and 4Document35 pagesCorpo3 and 4Gabe BedanaNo ratings yet

- Corpo6 For PrintDocument22 pagesCorpo6 For PrintGabe Bedana100% (1)

- Chapter 9Document17 pagesChapter 9Emrah CanNo ratings yet

- Attach File Bbs BBS 4 3-2 ProjectLoan N EquipmentLoanDocument4 pagesAttach File Bbs BBS 4 3-2 ProjectLoan N EquipmentLoanRovita TriyambudiNo ratings yet

- Variable Construction Guarantee MW 3Document2 pagesVariable Construction Guarantee MW 3Michael BenhuraNo ratings yet

- Cavendish University Uganda: Mba715 Finance For Managers SATURDAY at 2:30-5:30PMDocument53 pagesCavendish University Uganda: Mba715 Finance For Managers SATURDAY at 2:30-5:30PMFaith AmbNo ratings yet

- Function and Role of Financial SystemsDocument33 pagesFunction and Role of Financial Systemsaamirjewani100% (1)

- Trust FunctionDocument9 pagesTrust FunctionKarina Blanco100% (2)

- Beds R Us June CatalogueDocument6 pagesBeds R Us June CataloguevandyksNo ratings yet

- HUD-HECM Complaint Notice of Default-Intent To ForecloseDocument29 pagesHUD-HECM Complaint Notice of Default-Intent To ForecloseNeil Gillespie100% (1)

- Pep Research: How Rich Are The Mayors?: The Guests at The WeddingDocument4 pagesPep Research: How Rich Are The Mayors?: The Guests at The WeddingJelena Vranic-UgrinovskaNo ratings yet

- Finals Business TaxationDocument5 pagesFinals Business TaxationSherwin DueNo ratings yet

- GK Tornado Sbi Po Main Exam 2019-68Document119 pagesGK Tornado Sbi Po Main Exam 2019-68sasNo ratings yet

- Corp Finance Chapter 30Document2 pagesCorp Finance Chapter 30discreetmike50No ratings yet

- 32 Nature and Scope of BankingDocument20 pages32 Nature and Scope of Bankingpatilamol019100% (1)

- Basic Banking Awareness Questions AnswersDocument7 pagesBasic Banking Awareness Questions AnswersSoumyaprakash PaniNo ratings yet

- Law Commission Report-Land RegistrationDocument308 pagesLaw Commission Report-Land RegistrationIngrid TarlageanuNo ratings yet

- Indian Banking and EconomyDocument51 pagesIndian Banking and Economysantosh.pw423097% (33)

- Wild Carrot Proposal For 3901 Shaw Boulevard - St. Louis, MODocument30 pagesWild Carrot Proposal For 3901 Shaw Boulevard - St. Louis, MOnextSTL.comNo ratings yet

- Marketing Approach For Rural AreasDocument2 pagesMarketing Approach For Rural AreasBhuvanvignesh VengurlekarNo ratings yet

- Percentage Taxes UstDocument5 pagesPercentage Taxes UstGabriel PonceNo ratings yet

- Credit Management For CooperativesDocument141 pagesCredit Management For CooperativesAndres Lorenzo III75% (16)

- Time Value of MoneyDocument61 pagesTime Value of Moneyfatin atiqahNo ratings yet

- 15 Torbela V Spouses RosarioDocument3 pages15 Torbela V Spouses RosarioCheska Vergara100% (1)

- 25) Union Bank of The PH v. SantibanezDocument1 page25) Union Bank of The PH v. SantibanezPio Guieb AguilarNo ratings yet

- Portfolios of The PoorDocument4 pagesPortfolios of The PoorjamieNo ratings yet

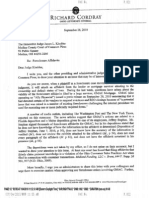

- Cordray Foreclosure LetterDocument2 pagesCordray Foreclosure LetterOAITANo ratings yet

- 156 - Asian Cathay Finance and Leasing Corporation VS SPS Gravador - 2PDocument2 pages156 - Asian Cathay Finance and Leasing Corporation VS SPS Gravador - 2PJomar TenezaNo ratings yet

- Civ Pro Conso Cases - Rules 57-70Document181 pagesCiv Pro Conso Cases - Rules 57-70Butch MaatNo ratings yet

- 23 Spouses Andal v. Philippine National BankDocument9 pages23 Spouses Andal v. Philippine National BankOke HarunoNo ratings yet

- SHG ProjectDocument116 pagesSHG ProjectYog KhopkarNo ratings yet