Download as pdf or txt

You might also like

- 6 Umlaut Benchmarking Expansion Strategy, Target Network Guidance, Competition Optimization - Huliang 00468321Document33 pages6 Umlaut Benchmarking Expansion Strategy, Target Network Guidance, Competition Optimization - Huliang 00468321Mohamed SalahNo ratings yet

- TMForum-Telco Revenue Growth BenchmarkDocument86 pagesTMForum-Telco Revenue Growth BenchmarkHasan Mukti100% (1)

- Teletech PresentationDocument18 pagesTeletech Presentationapi-402685925No ratings yet

- DL Presentation Deutsche TelekomDocument49 pagesDL Presentation Deutsche Telekomimam arifuddinNo ratings yet

- Detecon Opinion Paper FTTX Roll-Out: A Commercial Perspective Beyond TechnologyDocument11 pagesDetecon Opinion Paper FTTX Roll-Out: A Commercial Perspective Beyond TechnologyDetecon InternationalNo ratings yet

- Detecon Study Next-Generation Telco Product Lifecycle Management: How To Overcome Complexity in Product Management by Implementing Best-Practice PLMDocument66 pagesDetecon Study Next-Generation Telco Product Lifecycle Management: How To Overcome Complexity in Product Management by Implementing Best-Practice PLMDetecon International100% (2)

- Shaikha Al-Jabir - Strategic InnovationDocument12 pagesShaikha Al-Jabir - Strategic InnovationictQATARNo ratings yet

- SM Group Present TM BerhadDocument19 pagesSM Group Present TM BerhadLadiezApparelBiz50% (2)

- People & OrganizationDocument24 pagesPeople & OrganizationhiranmalukNo ratings yet

- Interim Report January-March 2011Document20 pagesInterim Report January-March 2011Jamil ArifNo ratings yet

- Investor Presentation 28 October 2021: © 2021 Nokia 1 © 2021 Nokia 1 PublicDocument22 pagesInvestor Presentation 28 October 2021: © 2021 Nokia 1 © 2021 Nokia 1 PublicDusha PeriyasamyNo ratings yet

- Summative Assessment: Financial Performance ManagementDocument24 pagesSummative Assessment: Financial Performance ManagementAshley WoodNo ratings yet

- Warid Telecom ReportDocument49 pagesWarid Telecom ReporthusnainjafriNo ratings yet

- Macedonia, FYR: Economy ProfileDocument63 pagesMacedonia, FYR: Economy ProfileArgeadNo ratings yet

- MTN PitchbookDocument21 pagesMTN PitchbookGideon Antwi Boadi100% (1)

- Globe Telecom, Incorporated I. Company ProfileDocument3 pagesGlobe Telecom, Incorporated I. Company ProfileAlyssa ArenilloNo ratings yet

- Wakounig - Organizing A New Telco - Detecon Whitepaper - NeuDocument19 pagesWakounig - Organizing A New Telco - Detecon Whitepaper - NeuM. AlimNo ratings yet

- Annual Guidance Note To The Network FINALDocument34 pagesAnnual Guidance Note To The Network FINALAdrian AndreiNo ratings yet

- Tata Communications LTD Short Term Debt Issue PR1+: Credit Analysis & Research LimitedDocument5 pagesTata Communications LTD Short Term Debt Issue PR1+: Credit Analysis & Research LimitedAnkita ChauhanNo ratings yet

- Factsheet - 0305709591 - CONG TY CO PHAN PHONG PHU SAC VIET - Company ReportDocument10 pagesFactsheet - 0305709591 - CONG TY CO PHAN PHONG PHU SAC VIET - Company ReportHung NguyenNo ratings yet

- Telecommunication 20210730 AminvestDocument5 pagesTelecommunication 20210730 AminvestaimanNo ratings yet

- Group 5-IbDocument8 pagesGroup 5-IbDayang RashidaNo ratings yet

- Telecommunications Sector Update: 2QFY10 Report Card - 03/09/2010Document8 pagesTelecommunications Sector Update: 2QFY10 Report Card - 03/09/2010Rhb InvestNo ratings yet

- Bharti 2airtel 1227851581611151 8Document49 pagesBharti 2airtel 1227851581611151 8Ramendra SinghNo ratings yet

- Integration of Products and Services PDFDocument8 pagesIntegration of Products and Services PDFvivianaNo ratings yet

- Teleperformance Slideshow h1 2021 Va Def RsDocument60 pagesTeleperformance Slideshow h1 2021 Va Def RsJanella Marie BautistaNo ratings yet

- Integration Products ServicesDocument8 pagesIntegration Products ServicesLuis Salinas S'jNo ratings yet

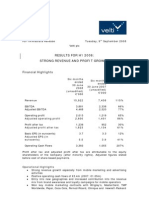

- Results For H1 2008: Strong Revenue and Profit Growth: Financial HighlightsDocument18 pagesResults For H1 2008: Strong Revenue and Profit Growth: Financial HighlightsmixedbagNo ratings yet

- TBLA Case IIM-C MjunctionDocument3 pagesTBLA Case IIM-C Mjunctionroshan64airNo ratings yet

- CCE CCEP Coca Cola European Partners CAGNY 2018Document37 pagesCCE CCEP Coca Cola European Partners CAGNY 2018Ala BasterNo ratings yet

- TPG Annual Report Accessible VersionDocument156 pagesTPG Annual Report Accessible Versiontdalisay44No ratings yet

- Modelling Multi-Mno Business For Mvnos in Their Evolution To Lte, Volte & Advanced PolicyDocument7 pagesModelling Multi-Mno Business For Mvnos in Their Evolution To Lte, Volte & Advanced Policyrdsngqb jgdhfNo ratings yet

- Library-Files-Uploaded files-TRAPresentations-Broadband in Lebanon - From An Infrastructure Perspective - US Lebanon ICT Forum - October 2010Document21 pagesLibrary-Files-Uploaded files-TRAPresentations-Broadband in Lebanon - From An Infrastructure Perspective - US Lebanon ICT Forum - October 2010Mahdi FarhatNo ratings yet

- Cellnex PitchDocument16 pagesCellnex PitchmehirdcNo ratings yet

- Icin 2011 6081092Document6 pagesIcin 2011 6081092Ari DwikiNo ratings yet

- Company Spotlight: Vodafone GroupDocument8 pagesCompany Spotlight: Vodafone Groupshabee87No ratings yet

- Marketing StretagyDocument8 pagesMarketing StretagysatbeerNo ratings yet

- Deal Drivers: EMEA FY 2021: A Spotlight On Mergers and Acquisitions Trends inDocument44 pagesDeal Drivers: EMEA FY 2021: A Spotlight On Mergers and Acquisitions Trends inBAGESNo ratings yet

- GTPL Hathway LTD.: A) About The CompanyDocument10 pagesGTPL Hathway LTD.: A) About The CompanyPayal SinghNo ratings yet

- Pakistan: Market InformationDocument11 pagesPakistan: Market InformationUsman HabibNo ratings yet

- Pakistan: Market InformationDocument11 pagesPakistan: Market InformationsilverskillsNo ratings yet

- BCT Digital - rt360 Suite OverviewDocument37 pagesBCT Digital - rt360 Suite OverviewLong VũNo ratings yet

- Vodafone Spain D-CCAP Case StudyDocument23 pagesVodafone Spain D-CCAP Case StudyNguyen Huu TruyenNo ratings yet

- Global Revenue Assurance Survey 2013 PDFDocument29 pagesGlobal Revenue Assurance Survey 2013 PDFMuhammad IslamNo ratings yet

- Atos Annual Results 2021Document28 pagesAtos Annual Results 2021Anand TajneNo ratings yet

- Bain Brief Telcos-And-InflationDocument8 pagesBain Brief Telcos-And-Inflationthb72683No ratings yet

- Case 16 Group 56 AnannaDocument44 pagesCase 16 Group 56 AnannaSM AzaharNo ratings yet

- Management AssignmentDocument4 pagesManagement AssignmentPrecious Tinashe NyakabauNo ratings yet

- Analysys Mason Sample - Digital Transformation - Financial Impact 2018Document12 pagesAnalysys Mason Sample - Digital Transformation - Financial Impact 2018Andrey PritulyukNo ratings yet

- International Business-Darko Jovanović 2014Document16 pagesInternational Business-Darko Jovanović 2014Darko JovanovicNo ratings yet

- Mirae Company Update 1Q24 TLKM 7 May 2024 Upgrade To Buy Lower TPDocument13 pagesMirae Company Update 1Q24 TLKM 7 May 2024 Upgrade To Buy Lower TPAndreas PaskalisNo ratings yet

- Strategy Update November 2010Document41 pagesStrategy Update November 2010Jonathan GablerNo ratings yet

- Etisalat Group Annual Report English 2019Document88 pagesEtisalat Group Annual Report English 2019RamiNo ratings yet

- WP 193Document45 pagesWP 193Ashraful AlamNo ratings yet

- ECS Holdings 2011 Annual ReportDocument112 pagesECS Holdings 2011 Annual ReportWeR1 Consultants Pte LtdNo ratings yet

- Presented By:: Subhankar Rath (09kb036) Sayan Mukherjee (09kb040) Dhruppad Bhattacharya (09kb054) Bikash Jena (09kb056)Document15 pagesPresented By:: Subhankar Rath (09kb036) Sayan Mukherjee (09kb040) Dhruppad Bhattacharya (09kb054) Bikash Jena (09kb056)jenabikashNo ratings yet

- Benchmark Report Telco GrowthDocument78 pagesBenchmark Report Telco Growthdaba1987No ratings yet

- Research Report Prepared By: Rishiraj SinghDocument7 pagesResearch Report Prepared By: Rishiraj Singhshraddha anandNo ratings yet

- Econet AR 2011Document75 pagesEconet AR 2011Kristi Duran100% (1)

- V G PLC C R: A Transforming IndustryDocument53 pagesV G PLC C R: A Transforming Industryamar jotNo ratings yet

- Generali 1H22 Results PresentationDocument46 pagesGenerali 1H22 Results PresentationAmal SebastianNo ratings yet

- DMR Article: A Generals TacticsDocument11 pagesDMR Article: A Generals TacticsDetecon InternationalNo ratings yet

- DMR Article: From King To King Maker - Mobile Service Strategies For The Telecom OperatorsDocument7 pagesDMR Article: From King To King Maker - Mobile Service Strategies For The Telecom OperatorsDetecon InternationalNo ratings yet

- Detecon Opinion Paper Next-Generation Mobile Application Management: Strategies For Leveraging Mobile Applications Within The EnterpriseDocument18 pagesDetecon Opinion Paper Next-Generation Mobile Application Management: Strategies For Leveraging Mobile Applications Within The EnterpriseDetecon InternationalNo ratings yet

- Detecon Study How Mature Is Your Sales Performance Management? Results of Detecon's Sales Performance Management StudyDocument20 pagesDetecon Study How Mature Is Your Sales Performance Management? Results of Detecon's Sales Performance Management StudyDetecon InternationalNo ratings yet

- Detecon Opinion Paper When Giants Flex Their Muscles: Green Activities of Silicon Valley ICT Industry LeadersDocument33 pagesDetecon Opinion Paper When Giants Flex Their Muscles: Green Activities of Silicon Valley ICT Industry LeadersDetecon InternationalNo ratings yet

- Procurement Process & Application Strategy: IT-savvy CPOs Are More Successful (Detecon Executive Briefing)Document7 pagesProcurement Process & Application Strategy: IT-savvy CPOs Are More Successful (Detecon Executive Briefing)Detecon InternationalNo ratings yet

- Detecon Opinion Paper Big Deal or Bad Deal. Advertising in The NewTV AgeDocument20 pagesDetecon Opinion Paper Big Deal or Bad Deal. Advertising in The NewTV AgeDetecon InternationalNo ratings yet

- Detecon Opinion Paper Next-Generation PLM - Strengthen Competitiveness in The Telco Business: An Introduction To The 4-Pillars Approach of Integrated Product Lifecycle ManagementDocument33 pagesDetecon Opinion Paper Next-Generation PLM - Strengthen Competitiveness in The Telco Business: An Introduction To The 4-Pillars Approach of Integrated Product Lifecycle ManagementDetecon InternationalNo ratings yet

- Detecon Opinion Paper Technical Cost Modelling: A Practical GuideDocument27 pagesDetecon Opinion Paper Technical Cost Modelling: A Practical GuideDetecon InternationalNo ratings yet

- Regulating NGN Access Networks in Germany (Detecon Executive Briefing)Document6 pagesRegulating NGN Access Networks in Germany (Detecon Executive Briefing)Detecon InternationalNo ratings yet

- Aneesh.K.Saju Aneesh.K.Saju Roll No:5 Roll No:5 Seventh Semester Seventh Semester Electrical &electronics Engg.. Electrical &electronics Engg.Document15 pagesAneesh.K.Saju Aneesh.K.Saju Roll No:5 Roll No:5 Seventh Semester Seventh Semester Electrical &electronics Engg.. Electrical &electronics Engg.Prabhavathi KNo ratings yet

- Flexem'S User'S Manual of The Fbox DevicesDocument143 pagesFlexem'S User'S Manual of The Fbox Devicesbassit82No ratings yet

- SSRN Id38085421Document21 pagesSSRN Id38085421Jay Ram JadavNo ratings yet

- Country Overview: Philippines Growth Through Innovation: AnalysisDocument35 pagesCountry Overview: Philippines Growth Through Innovation: AnalysisJasmine YlayaNo ratings yet

- Network Device and FunctionsDocument33 pagesNetwork Device and FunctionsNandhiniNo ratings yet

- UG 4-1 R19 CSE SyllabusDocument33 pagesUG 4-1 R19 CSE SyllabusBrahmaiah ThanniruNo ratings yet

- Helios SignalTouch Series Digital ICS Home RelayDocument16 pagesHelios SignalTouch Series Digital ICS Home Relayrochdi9991No ratings yet

- 5G ReadyDocument6 pages5G ReadyRoshan JamesNo ratings yet

- Telecom Industry Case StudyDocument12 pagesTelecom Industry Case Studysarat_maNo ratings yet

- Sony Ericsson C705 A Multi-Purposed Handset On Which Every WidgetDocument1 pageSony Ericsson C705 A Multi-Purposed Handset On Which Every WidgetandrewoliviaNo ratings yet

- Robin Joseph Thomas (FK-2055)Document18 pagesRobin Joseph Thomas (FK-2055)Robin Joseph ThomasNo ratings yet

- Ciena: Delivering Carrier Grade Ethernet Transport InfrastructuresDocument36 pagesCiena: Delivering Carrier Grade Ethernet Transport InfrastructuresSahil ChandraNo ratings yet

- Battery Life Optimization in Mobile Devices With Internet UsageDocument6 pagesBattery Life Optimization in Mobile Devices With Internet UsageKishan GondiNo ratings yet

- Thesis Topic On Mobile CommunicationDocument7 pagesThesis Topic On Mobile Communicationbsq39zpf100% (2)

- 5G TechnologyDocument23 pages5G TechnologyAkshay Phadke67% (3)

- Analyzing Marketing Environment of Viettel Telecom: Individual AssignmentDocument4 pagesAnalyzing Marketing Environment of Viettel Telecom: Individual AssignmentHoàng TriềuNo ratings yet

- Project Report On Market Potential AnalysisDocument92 pagesProject Report On Market Potential AnalysisJames Bond100% (1)

- 2G, 3G and LTE Co-Transmission (ERAN15.1 - Draft A)Document30 pages2G, 3G and LTE Co-Transmission (ERAN15.1 - Draft A)Waqas AhmedNo ratings yet

- What Is APNDocument20 pagesWhat Is APNmgk609No ratings yet

- Generations of Mobile TechDocument12 pagesGenerations of Mobile Techseema fatimaNo ratings yet

- Global Internet Report 2014Document146 pagesGlobal Internet Report 2014InternetSocietyNo ratings yet

- Asia Mobile Data Wireless Broadband Market and ForecastsDocument250 pagesAsia Mobile Data Wireless Broadband Market and ForecastsMithunRafsanNo ratings yet

- LTE UMTS GSM Network OptimizationDocument44 pagesLTE UMTS GSM Network OptimizationAvi Shetty100% (1)

- ABEM Terrameter LS 2: GeneralDocument2 pagesABEM Terrameter LS 2: GeneralFlash WingNo ratings yet

- PCS265LTE Installation and Programming GuideDocument2 pagesPCS265LTE Installation and Programming GuideHector LinaresNo ratings yet

- Part-B Unit-4 Web Applications & SecurityDocument5 pagesPart-B Unit-4 Web Applications & SecurityAgastya SinghNo ratings yet

- Cdma IS-95, IMT-2000: Technology, ANDDocument29 pagesCdma IS-95, IMT-2000: Technology, ANDrajasekarNo ratings yet

- SSP Profile1Document7 pagesSSP Profile1Asad KhanNo ratings yet

- Lte3316-M604 2Document4 pagesLte3316-M604 2Ali KılıçkayaNo ratings yet