Download as docx, pdf, or txt

You might also like

- Multiple Choice. Select The Letter That Corresponds To The Best Answer. This ExaminationDocument15 pagesMultiple Choice. Select The Letter That Corresponds To The Best Answer. This ExaminationNananananaNo ratings yet

- Individually Managed Accounts An Investor's GuideDocument272 pagesIndividually Managed Accounts An Investor's Guidebrew1cool12381No ratings yet

- Heinz Research Report JP MorganDocument9 pagesHeinz Research Report JP MorganKeshav soodNo ratings yet

- Sri Lanka Succesfully Completes Its Domestic Debt Optimization. Here'S What It MeansDocument8 pagesSri Lanka Succesfully Completes Its Domestic Debt Optimization. Here'S What It MeanstmendisNo ratings yet

- Wealth Insights Newsletter June 2021Document42 pagesWealth Insights Newsletter June 2021Ram PrasadNo ratings yet

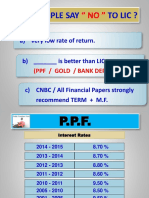

- Why People Say Tolic?: A) Very Low Rate of ReturnDocument26 pagesWhy People Say Tolic?: A) Very Low Rate of ReturnprabhathNo ratings yet

- Equity 4Q2015Document76 pagesEquity 4Q2015GrraldNo ratings yet

- Market Feedback Report: January 2020Document10 pagesMarket Feedback Report: January 2020Stevin GeorgeNo ratings yet

- Indicative Annualized Rates On Deposits W.E .F - 01 .01.2022 To 31 .03.2022Document4 pagesIndicative Annualized Rates On Deposits W.E .F - 01 .01.2022 To 31 .03.2022Afaq YousafNo ratings yet

- Views On Markets and SectorsDocument19 pagesViews On Markets and SectorskundansudNo ratings yet

- Bank Lending Rates As of 12-01-19Document1 pageBank Lending Rates As of 12-01-19Uhudhu AhmedNo ratings yet

- Banking Sector of BangladeshDocument8 pagesBanking Sector of BangladeshIftekhar Abid FahimNo ratings yet

- Banking Sector 210202Document15 pagesBanking Sector 210202Brian StanleyNo ratings yet

- MP Challenges 16 Nov 10Document18 pagesMP Challenges 16 Nov 10umairahmed83No ratings yet

- Cập Nhật Giá FI BondDocument5 pagesCập Nhật Giá FI BondNguyễn Thu ThủyNo ratings yet

- Amount (Rs. in Millions) 46,716 46,716 46,716 Annual Stated Rate (P.a.,) 10.00% 10.83% 10.83% CRR 5.0% 0.0% 0.0%Document5 pagesAmount (Rs. in Millions) 46,716 46,716 46,716 Annual Stated Rate (P.a.,) 10.00% 10.83% 10.83% CRR 5.0% 0.0% 0.0%AbidRazacaNo ratings yet

- Dabur Q3FY11 ResultDocument17 pagesDabur Q3FY11 ResultjackjariNo ratings yet

- Stock Screener002709Document2 pagesStock Screener002709Parikshit KunduNo ratings yet

- Earnings Projection of BanksDocument2 pagesEarnings Projection of Banksmahfuz69No ratings yet

- Fi MMMMMMDocument13 pagesFi MMMMMMPrabin ChaudharyNo ratings yet

- Fortnightly Banking Update: Deposit Growth Moderated But Bank Credit Growth Moderates Even MoreDocument3 pagesFortnightly Banking Update: Deposit Growth Moderated But Bank Credit Growth Moderates Even Morekumar ganeshNo ratings yet

- How Technology 20210811Document37 pagesHow Technology 20210811Line PhamNo ratings yet

- Ratio AnalysisDocument25 pagesRatio AnalysisKolaNo ratings yet

- Monthly Inflation Tracker November 2010Document8 pagesMonthly Inflation Tracker November 2010Adebayo DurodolaNo ratings yet

- LiquiLoans - LiteratureDocument28 pagesLiquiLoans - LiteratureNeetika SahNo ratings yet

- Long Term Interest RatesDocument1 pageLong Term Interest Rateshansikamedagedara179No ratings yet

- Axis Bank InvestmentDocument32 pagesAxis Bank Investment22satendraNo ratings yet

- Mercer-Capital Bank Valuation AKG PDFDocument60 pagesMercer-Capital Bank Valuation AKG PDFDesmond Dujon HenryNo ratings yet

- Daily Treasury Report0426 ENGDocument3 pagesDaily Treasury Report0426 ENGBiliguudei AmarsaikhanNo ratings yet

- Bank of AmericaDocument21 pagesBank of AmericaRavish SrivastavaNo ratings yet

- Tourism Performance 2Document30 pagesTourism Performance 2Reymond BodiaoNo ratings yet

- Cost of Fund: HabibmetroDocument16 pagesCost of Fund: HabibmetroAsad MuhammadNo ratings yet

- Kestrel Weekly Commentary 26 April 2024Document7 pagesKestrel Weekly Commentary 26 April 2024otis2ke9588No ratings yet

- South Central Africa Top CompaniesDocument16 pagesSouth Central Africa Top CompaniesaddyNo ratings yet

- Portfolio Report 2010Document13 pagesPortfolio Report 2010ASP420No ratings yet

- Recent Challenges in Monetary Policy Design in India: Mridul SaggarDocument38 pagesRecent Challenges in Monetary Policy Design in India: Mridul SaggarbafnajayeshNo ratings yet

- US Restaurant 2015 ForecastDocument4 pagesUS Restaurant 2015 ForecastshichifukuroNo ratings yet

- Pool Rates March 2023Document4 pagesPool Rates March 2023Born To LooseNo ratings yet

- Sanitation Management SystemsDocument19 pagesSanitation Management SystemsIshfaq HussainNo ratings yet

- Company Name Exchange:Ticker Price To Book Return On EquityDocument6 pagesCompany Name Exchange:Ticker Price To Book Return On EquitygigiNo ratings yet

- Slabs Profit Rate: Deposit and Prematurity RatesDocument1 pageSlabs Profit Rate: Deposit and Prematurity RatesJay KhanNo ratings yet

- Interest Rate RangeDocument1 pageInterest Rate RangeAnaghaNo ratings yet

- Financial Projections Template 08Document26 pagesFinancial Projections Template 08Clyde SakuradaNo ratings yet

- Portfolio For CAPM: Asset Distribution According To Stocks and FundsDocument5 pagesPortfolio For CAPM: Asset Distribution According To Stocks and FundsJyotishman SahaNo ratings yet

- Update Harga: Real-Time: QualityDocument44 pagesUpdate Harga: Real-Time: QualityNul AsashiNo ratings yet

- Deposit Rate WEF 01-04-2019Document1 pageDeposit Rate WEF 01-04-2019Thomas HarveyNo ratings yet

- Mini Assignment 1Document4 pagesMini Assignment 1Pratik AgrawalNo ratings yet

- Sir MubeenDocument5 pagesSir MubeenA. Bilal SaleemNo ratings yet

- Interim Union Budget 2024-25 Note - 0Document3 pagesInterim Union Budget 2024-25 Note - 030091998skumarNo ratings yet

- Hemas Holdings PLC: Investor Presentation Q3 2012/13Document14 pagesHemas Holdings PLC: Investor Presentation Q3 2012/13haffaNo ratings yet

- Tasas de Interés BANECUADOR BP - ENERO 2024 Signed Signed 1Document2 pagesTasas de Interés BANECUADOR BP - ENERO 2024 Signed Signed 1pepevicho1973No ratings yet

- BOLT DCF ValuationDocument1 pageBOLT DCF ValuationOld School ValueNo ratings yet

- ValuationDocument4 pagesValuationRhea Mae CarantoNo ratings yet

- Interest Rate Comparison of BanksDocument15 pagesInterest Rate Comparison of Bankspune projectNo ratings yet

- FY2009 Financial ResultsDocument17 pagesFY2009 Financial ResultstinkrboxNo ratings yet

- CNPF Ratio AnalysisDocument8 pagesCNPF Ratio AnalysisSheena Ann Keh LorenzoNo ratings yet

- Giguere hw4Document4 pagesGiguere hw4api-554525839No ratings yet

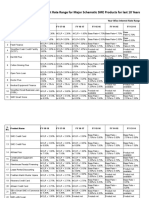

- Interest Rates For Last 10 Yr For Major SME ProductsDocument6 pagesInterest Rates For Last 10 Yr For Major SME Productssharad1996No ratings yet

- HBFC PrivitizationDocument6 pagesHBFC PrivitizationMomin IqbalNo ratings yet

- Weekly Wrap For The Week Ended 270919Document1 pageWeekly Wrap For The Week Ended 270919Dilkaran SinghNo ratings yet

- Financial Soundness Indicators for Financial Sector Stability in BangladeshFrom EverandFinancial Soundness Indicators for Financial Sector Stability in BangladeshNo ratings yet

- Middle East and North Africa Quarterly Economic Brief, January 2014: Growth Slowdown Heightens the Need for ReformsFrom EverandMiddle East and North Africa Quarterly Economic Brief, January 2014: Growth Slowdown Heightens the Need for ReformsNo ratings yet

- Banking on Growth Models: China's Troubled Pursuit of Financial Reform and Economic RebalancingFrom EverandBanking on Growth Models: China's Troubled Pursuit of Financial Reform and Economic RebalancingNo ratings yet

- SPCapitalIQEquityResearch ConchoResourcesInc Feb 28 2016Document11 pagesSPCapitalIQEquityResearch ConchoResourcesInc Feb 28 2016VeryclearwaterNo ratings yet

- Chapter# 5 of Investments Principles & Concepts International Student Version 11th EditionDocument5 pagesChapter# 5 of Investments Principles & Concepts International Student Version 11th Editionmavimalik89% (9)

- Final Exam Web 1Document10 pagesFinal Exam Web 1Karina LeakesNo ratings yet

- Ashok Leyland LTD: ESG Disclosure ScoreDocument8 pagesAshok Leyland LTD: ESG Disclosure ScoreRomelu MartialNo ratings yet

- Security Analysis and Portfolio ManagementDocument26 pagesSecurity Analysis and Portfolio ManagementXandarnova corpsNo ratings yet

- Illustration 1: Trial Balance As On 31' March 2015 Rs. Credit RsDocument3 pagesIllustration 1: Trial Balance As On 31' March 2015 Rs. Credit RsDrpranav SaraswatNo ratings yet

- SEC Opinion - Mr. Fernando C. Santico - 178279-1991-Mr. - Fernando - C. - Santico20210623-11-9s3w53Document2 pagesSEC Opinion - Mr. Fernando C. Santico - 178279-1991-Mr. - Fernando - C. - Santico20210623-11-9s3w53Loren SanapoNo ratings yet

- Commart V SECDocument4 pagesCommart V SECJan Mark WongNo ratings yet

- USA v. Speight Doc 5 Filed 23 Jul 14Document8 pagesUSA v. Speight Doc 5 Filed 23 Jul 14scion.scionNo ratings yet

- ETF Newsletter - February - 23Document20 pagesETF Newsletter - February - 23Chuck CookNo ratings yet

- Newell Brands: Google Search Info Shows Decline in Key BrandDocument2 pagesNewell Brands: Google Search Info Shows Decline in Key BrandAnonymous Ecd8rCNo ratings yet

- TB Ch03Document67 pagesTB Ch03CG100% (1)

- Definition of Terms-TAXDocument5 pagesDefinition of Terms-TAXAnonymous iOYkz0wNo ratings yet

- Brazilian Broadband MarketDocument6 pagesBrazilian Broadband Marketbenjah2No ratings yet

- Sharekhan - Fundamental AnalysisDocument72 pagesSharekhan - Fundamental Analysissomeshol9355100% (8)

- Entrepreneurship & Sources of Business FinanceDocument14 pagesEntrepreneurship & Sources of Business FinancePETER OTIENONo ratings yet

- Chap 6 Dividend Decision RevisedDocument49 pagesChap 6 Dividend Decision RevisedGizachew AlazarNo ratings yet

- SEx 13Document36 pagesSEx 13Amir MadaniNo ratings yet

- Eco - Finance SyllabiDocument18 pagesEco - Finance SyllabiKJ VillNo ratings yet

- E-Books - AS 13 Accounting For InvestmentsDocument32 pagesE-Books - AS 13 Accounting For InvestmentssmartshivenduNo ratings yet

- Finance Theory: Introduction To Risk and ReturnDocument34 pagesFinance Theory: Introduction To Risk and ReturnAiqa AliNo ratings yet

- INVESTMENTSDocument9 pagesINVESTMENTSKrisan RiveraNo ratings yet

- Best Earning AppDocument3 pagesBest Earning AppSree ProsantoNo ratings yet

- Value Investing - Aswath DamodaranDocument43 pagesValue Investing - Aswath Damodaranapi-3821333100% (1)

- Examination: Subject SA3 - General Insurance Specialist ApplicationsDocument5 pagesExamination: Subject SA3 - General Insurance Specialist Applicationsdickson phiriNo ratings yet

- Cost Accounting Unit 2Document12 pagesCost Accounting Unit 2anon_45870178No ratings yet

- MK - ch12 - Cost of CapitalDocument13 pagesMK - ch12 - Cost of CapitalDwi Slamet RiyadiNo ratings yet