Download as pdf or txt

You might also like

- Indonesia Market Outlook 2024 by NielsenIQ & MECDocument37 pagesIndonesia Market Outlook 2024 by NielsenIQ & MECdiancahayanii100% (1)

- Manual RZ5Document294 pagesManual RZ5acandrei67% (3)

- 9 Theories - Research ActivityDocument143 pages9 Theories - Research Activityapi-2978344330% (1)

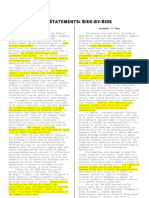

- Fed Statements Side by SideDocument1 pageFed Statements Side by SideTaylor CottamNo ratings yet

- FOMC0810Document2 pagesFOMC0810arborjimbNo ratings yet

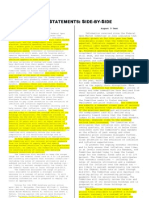

- SidebysidefedDocument1 pageSidebysidefedandrewbloggerNo ratings yet

- FOMCstatementDocument2 pagesFOMCstatementCBNo ratings yet

- Fomc S: S - S: Tatements IDE BY IDEDocument3 pagesFomc S: S - S: Tatements IDE BY IDEarborjimbNo ratings yet

- Fed Statement June 2009Document2 pagesFed Statement June 2009andrewbloggerNo ratings yet

- Fomc S: S - S: Tatements IDE BY IDEDocument3 pagesFomc S: S - S: Tatements IDE BY IDEarborjimbNo ratings yet

- Fed Side by Side 20120125Document3 pagesFed Side by Side 20120125andrewbloggerNo ratings yet

- Fomc S: S - S: Tatements IDE BY IDEDocument3 pagesFomc S: S - S: Tatements IDE BY IDEandrewbloggerNo ratings yet

- FOMC Rate Decision 04.25.12Document1 pageFOMC Rate Decision 04.25.12Pensford FinancialNo ratings yet

- Fed SideDocument1 pageFed Sideannawitkowski88No ratings yet

- Fomc Statements - Side-By-sideDocument2 pagesFomc Statements - Side-By-sideurbanovNo ratings yet

- December 17, 2014 Compared With October 29, 2014 Jeremie Cohen-SettonDocument3 pagesDecember 17, 2014 Compared With October 29, 2014 Jeremie Cohen-Settonapi-273992067No ratings yet

- January - March FOMC Statement ComparisonDocument1 pageJanuary - March FOMC Statement Comparisonshawn2207No ratings yet

- Fed TalkDocument2 pagesFed TalkTelegraphUKNo ratings yet

- FOMC Redline MarchDocument2 pagesFOMC Redline MarchZerohedgeNo ratings yet

- FOMC RedLineDocument2 pagesFOMC RedLineEduardo VinanteNo ratings yet

- Fed 09212011Document2 pagesFed 09212011andrewbloggerNo ratings yet

- FOMC Side by Side 11022011Document2 pagesFOMC Side by Side 11022011andrewbloggerNo ratings yet

- September FOMC RedlineDocument2 pagesSeptember FOMC RedlineZerohedgeNo ratings yet

- Oct FOMC RedlineDocument2 pagesOct FOMC RedlineZerohedgeNo ratings yet

- Fomc StatmentDocument1 pageFomc Statmentapi-280585983No ratings yet

- FOMC Word For Word Changes. 05.01.13Document2 pagesFOMC Word For Word Changes. 05.01.13Pensford FinancialNo ratings yet

- Sidebyside 08092011Document1 pageSidebyside 08092011andrewbloggerNo ratings yet

- Press ReleaseDocument2 pagesPress Releaseapi-26018528No ratings yet

- FedDocument4 pagesFedandre.torresNo ratings yet

- Press Release: For Release at 2:00 P.M. EDTDocument2 pagesPress Release: For Release at 2:00 P.M. EDTTREND_7425No ratings yet

- FOMC Word For Word Changes 03.20.13Document2 pagesFOMC Word For Word Changes 03.20.13Pensford FinancialNo ratings yet

- Federal Reserve Issues FOMC Statement: ShareDocument2 pagesFederal Reserve Issues FOMC Statement: ShareTREND_7425No ratings yet

- Monetary 20240501 A 1Document4 pagesMonetary 20240501 A 1gustavo.kahilNo ratings yet

- Fomc Septiembre 2015Document2 pagesFomc Septiembre 2015cocoNo ratings yet

- Transcript of Chairman Bernanke's Press Conference April 25, 2012Document23 pagesTranscript of Chairman Bernanke's Press Conference April 25, 2012CoolidgeLowNo ratings yet

- Fomc Pres Conf 20141217Document23 pagesFomc Pres Conf 20141217JoseLastNo ratings yet

- Monetary 20230614 A 1Document4 pagesMonetary 20230614 A 1Jhony SmithYTNo ratings yet

- Fomc Pres Conf 20240501Document4 pagesFomc Pres Conf 20240501gustavo.kahilNo ratings yet

- FOMCpresconf 20210922Document26 pagesFOMCpresconf 20210922marcoNo ratings yet

- ChairDocument4 pagesChairandre.torresNo ratings yet

- Yellen TestimonyDocument7 pagesYellen TestimonyZerohedgeNo ratings yet

- Fed Meeting and USD Purchasing Power BlogDocument1 pageFed Meeting and USD Purchasing Power BloghweinermanNo ratings yet

- Yellen HHDocument7 pagesYellen HHZerohedgeNo ratings yet

- Unconventional Wisdom. Original Thinking.: Bulletin BoardDocument12 pagesUnconventional Wisdom. Original Thinking.: Bulletin BoardCurve123No ratings yet

- SystemDocument8 pagesSystempathanfor786No ratings yet

- Why Monetary Policy MattersDocument2 pagesWhy Monetary Policy MattersKatieYoungNo ratings yet

- 2018.01.31 FED Press ReleaseDocument2 pages2018.01.31 FED Press ReleaseTREND_7425No ratings yet

- Peso Balanced Fund: Investment ObjectiveDocument10 pagesPeso Balanced Fund: Investment ObjectiveErwin Dela CruzNo ratings yet

- US Fed FOMC Press Conference 18 September 2013 No TaperDocument26 pagesUS Fed FOMC Press Conference 18 September 2013 No TaperJhunjhunwalas Digital Finance & Business Info LibraryNo ratings yet

- Federal Reserve StatementDocument4 pagesFederal Reserve StatementTim MooreNo ratings yet

- Case 8:: Will Fed'S "Easy Money" Push Up Prices?Document19 pagesCase 8:: Will Fed'S "Easy Money" Push Up Prices?Keara MojicaNo ratings yet

- Fed Doves No Longer Rule The Roost: Economic and Financial AnalysisDocument5 pagesFed Doves No Longer Rule The Roost: Economic and Financial AnalysisOwm Close CorporationNo ratings yet

- Westpac - Fed Doves Might Have Last Word (August 2013)Document4 pagesWestpac - Fed Doves Might Have Last Word (August 2013)leithvanonselenNo ratings yet

- Ife - UsaDocument13 pagesIfe - Usagiovanni lazzeriNo ratings yet

- Interpret The Tone-FOMC Statements Answer Key: Advance Your CareerDocument3 pagesInterpret The Tone-FOMC Statements Answer Key: Advance Your CareerTarun TiwariNo ratings yet

- Q F F Q 2: 2014: Tanbic Oney Arket UNDDocument1 pageQ F F Q 2: 2014: Tanbic Oney Arket UNDOhiwei OsawemenNo ratings yet

- Monetary 20230201 A 1Document4 pagesMonetary 20230201 A 1tamhid nahianNo ratings yet

- Conduct of Monetary Policy: Tools, Goals, Strategy, and TacticsDocument30 pagesConduct of Monetary Policy: Tools, Goals, Strategy, and TacticsNaheed SakhiNo ratings yet

- The Feds New Monetary Policy Tools - SEDocument11 pagesThe Feds New Monetary Policy Tools - SEAndré M. TrottaNo ratings yet

- Felicia Irene - Week 5Document27 pagesFelicia Irene - Week 5felicia ireneNo ratings yet

- Monetary 20230726 A 1Document4 pagesMonetary 20230726 A 1Verónica SilveriNo ratings yet

- The Escape from Balance Sheet Recession and the QE Trap: A Hazardous Road for the World EconomyFrom EverandThe Escape from Balance Sheet Recession and the QE Trap: A Hazardous Road for the World EconomyRating: 5 out of 5 stars5/5 (1)

- Rydex Report For 5.3.11Document11 pagesRydex Report For 5.3.11glerner133926No ratings yet

- Morning News Notes:2011-07-21Document1 pageMorning News Notes:2011-07-21glerner133926No ratings yet

- Rydex Report For 4.5.11Document9 pagesRydex Report For 4.5.11glerner133926No ratings yet

- Rydex Report For 4.5.11Document9 pagesRydex Report For 4.5.11glerner133926No ratings yet

- Morning News Notes:2011-07-13Document1 pageMorning News Notes:2011-07-13glerner133926No ratings yet

- Morning News Notes: 2011-07-11Document1 pageMorning News Notes: 2011-07-11glerner133926No ratings yet

- Morning News Notes:2011-06-15Document1 pageMorning News Notes:2011-06-15glerner133926No ratings yet

- Morning News Notes:2011-07-19Document1 pageMorning News Notes:2011-07-19glerner133926No ratings yet

- Morning News Notes: 2011-06-16Document2 pagesMorning News Notes: 2011-06-16glerner133926No ratings yet

- Morning News Notes:2011-06-29Document1 pageMorning News Notes:2011-06-29glerner133926No ratings yet

- Morning News Notes:2011-06-14Document1 pageMorning News Notes:2011-06-14glerner133926No ratings yet

- Morning News Notes: 2011-03-31Document2 pagesMorning News Notes: 2011-03-31glerner133926No ratings yet

- Morning News Notes: 2011-04-21Document2 pagesMorning News Notes: 2011-04-21glerner133926No ratings yet

- Morning News Notes: 2011-06-09Document1 pageMorning News Notes: 2011-06-09glerner133926No ratings yet

- Morning News Notes: 2011-05-06Document1 pageMorning News Notes: 2011-05-06glerner133926No ratings yet

- Morning News Notes: 2011-06-13Document1 pageMorning News Notes: 2011-06-13glerner133926No ratings yet

- Web Layout v1 Slide 1-2Document1 pageWeb Layout v1 Slide 1-2glerner133926No ratings yet

- Morning News Notes: 2011-04-18Document1 pageMorning News Notes: 2011-04-18glerner133926No ratings yet

- Morning News Notes: 2011-05-04Document1 pageMorning News Notes: 2011-05-04glerner133926No ratings yet

- Morning News Notes: 2011-04-13Document1 pageMorning News Notes: 2011-04-13glerner133926No ratings yet

- London TelegraphDocument1 pageLondon Telegraphglerner133926No ratings yet

- Morning News Notes: 2011-03-29Document1 pageMorning News Notes: 2011-03-29glerner133926No ratings yet

- Achievements:: 'The Spirit of Wipro' Is Best Represented Through The Following Three StatementsDocument3 pagesAchievements:: 'The Spirit of Wipro' Is Best Represented Through The Following Three StatementsNitesh R ShahaniNo ratings yet

- Early AdulthoodDocument1 pageEarly AdulthoodCherry BobierNo ratings yet

- Classification of FolkdanceDocument2 pagesClassification of FolkdanceMica CasimeroNo ratings yet

- Fundamentals of Buddhist Psychotherapy (A Critical....Document65 pagesFundamentals of Buddhist Psychotherapy (A Critical....Rev NandacaraNo ratings yet

- Affirmations To Balance Meridians and EmotionsDocument2 pagesAffirmations To Balance Meridians and EmotionsMario L M Ramos100% (1)

- Cutting Opera Tion Takes Onl Y 24HRS: User ListDocument2 pagesCutting Opera Tion Takes Onl Y 24HRS: User ListNurSarahNo ratings yet

- 2011 Equipment Flyer 05272011updatedDocument24 pages2011 Equipment Flyer 05272011updatedChecho BuenaventuraNo ratings yet

- Link of Support Material Link 2020-21CLASSES 9 1 - 11 12Document2 pagesLink of Support Material Link 2020-21CLASSES 9 1 - 11 12naman mahawerNo ratings yet

- Activitiesclasswork Unit 2 Lesson 3 Great Civilizations Emerge Maya Religion Ans Social HierarchyDocument25 pagesActivitiesclasswork Unit 2 Lesson 3 Great Civilizations Emerge Maya Religion Ans Social Hierarchyapi-240724606No ratings yet

- s19 Secundaria 3 Recurso Ingles A2 Transcripciondeaudio PDFDocument2 pagess19 Secundaria 3 Recurso Ingles A2 Transcripciondeaudio PDFCristian Valencia Segundo0% (1)

- Basic ECG Interpretation Practice Test: DIRECTIONS: The Following Test Consists of 20 QuestionsDocument10 pagesBasic ECG Interpretation Practice Test: DIRECTIONS: The Following Test Consists of 20 Questionsmihaela_bondocNo ratings yet

- Personal Statement EdmundoDocument4 pagesPersonal Statement EdmundoAnca UngureanuNo ratings yet

- 21 Rev Der PR51Document7 pages21 Rev Der PR51takoNo ratings yet

- Roplasto English Presentation of The 7001 5 Chambers ProfileDocument4 pagesRoplasto English Presentation of The 7001 5 Chambers ProfileHIDROPLASTONo ratings yet

- A Film Review General Luna and Macario SDocument5 pagesA Film Review General Luna and Macario SjasminjajarefeNo ratings yet

- Kusama Artist Presentation 1Document9 pagesKusama Artist Presentation 1api-592346261No ratings yet

- Skills Framework For Design Technical Skills and Competencies (TSC) Reference DocumentDocument2 pagesSkills Framework For Design Technical Skills and Competencies (TSC) Reference DocumentdianNo ratings yet

- Teutonic Mythology v1 1000023511 PDFDocument452 pagesTeutonic Mythology v1 1000023511 PDFOlga SultanNo ratings yet

- Zeffere Ketema Paym FinalDocument186 pagesZeffere Ketema Paym FinalEphremHailuNo ratings yet

- TSB 2000010 Technical Overview of The STERILIZABLEBAGDocument4 pagesTSB 2000010 Technical Overview of The STERILIZABLEBAGdatinjacabNo ratings yet

- Comentary On Nostra AetateDocument11 pagesComentary On Nostra AetateJude nnawuiheNo ratings yet

- Mca MaterialDocument30 pagesMca MaterialsharmilaNo ratings yet

- Proc Q and A - 2022updated V1Document47 pagesProc Q and A - 2022updated V1dreamsky702243No ratings yet

- Ramanuja Srivaishnavism VisistaadvaitaDocument32 pagesRamanuja Srivaishnavism VisistaadvaitarajNo ratings yet

- Depression in Neurodegenerative Diseases - Common Mechanisms and Current Treatment OptionsDocument103 pagesDepression in Neurodegenerative Diseases - Common Mechanisms and Current Treatment OptionsAna Paula LopesNo ratings yet

- MTICDocument5 pagesMTICSonali TanejaNo ratings yet

- Die and Mould 2016 Exhibitors ListDocument19 pagesDie and Mould 2016 Exhibitors Listsentamil vigneshwaranNo ratings yet