Presentation On Kenyan Capital Gains Tax

Presentation On Kenyan Capital Gains Tax

You might also like

- Buckwold20e Solutions Ch06Document93 pagesBuckwold20e Solutions Ch06Aman Lottay100% (1)

- BIR Ruling (DA-005-07) (Travel Agencies) PDFDocument4 pagesBIR Ruling (DA-005-07) (Travel Agencies) PDFAl Marvin0% (2)

- Fiscal and Monetary Policy of GermanyDocument125 pagesFiscal and Monetary Policy of Germanyarpit vora100% (2)

- Tugasan Berkumpulan Valuation Methodology (DDWF 1423) : Nama Pensyarah: Puan DR Noraini Binti RejabDocument27 pagesTugasan Berkumpulan Valuation Methodology (DDWF 1423) : Nama Pensyarah: Puan DR Noraini Binti Rejabhilman afiq100% (1)

- 7capital Gain TaxationDocument23 pages7capital Gain TaxationWINSTON YATICHNo ratings yet

- Proposed Tax Changes Under The Finance Bill 2023 Snapshot - ALN Kenya Legal AlertDocument20 pagesProposed Tax Changes Under The Finance Bill 2023 Snapshot - ALN Kenya Legal AlertKafonyi JohnNo ratings yet

- Canadian Income Taxation 2014 2015 Planning and Decision Making Canadian 17th Edition Buckwold Solutions Manual 1Document36 pagesCanadian Income Taxation 2014 2015 Planning and Decision Making Canadian 17th Edition Buckwold Solutions Manual 1aliciahollandygimjrqotk100% (29)

- Canadian Income Taxation 2014 2015 Planning and Decision Making Canadian 17Th Edition Buckwold Solutions Manual Full Chapter PDFDocument36 pagesCanadian Income Taxation 2014 2015 Planning and Decision Making Canadian 17Th Edition Buckwold Solutions Manual Full Chapter PDFkenneth.cappello861100% (21)

- CGT Presentation - LSK CLE October 2016Document25 pagesCGT Presentation - LSK CLE October 2016Mulindi KhayesiNo ratings yet

- Guide To CW QnsDocument12 pagesGuide To CW QnsMwebembezi Mark EricNo ratings yet

- Taxation Q&ADocument18 pagesTaxation Q&AZsazsaNo ratings yet

- Chapter 11 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Document20 pagesChapter 11 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din SheryarNo ratings yet

- Question As Emailed To Us On 24 Oct 2020 by Safique SardarDocument4 pagesQuestion As Emailed To Us On 24 Oct 2020 by Safique SardarSk Asif AliNo ratings yet

- Kenya Revenue Authority: Domestic Taxes DepartmentDocument19 pagesKenya Revenue Authority: Domestic Taxes DepartmentEmeka NkemNo ratings yet

- Corporate Reporting Assignment 1 - GroupDocument18 pagesCorporate Reporting Assignment 1 - GroupangelaNo ratings yet

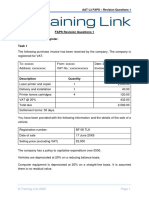

- AAT L3 FAPS Revision Questions 1Document7 pagesAAT L3 FAPS Revision Questions 1uzytkownik2207No ratings yet

- Uganda Issues Tax Amendment Bills 2020Document6 pagesUganda Issues Tax Amendment Bills 2020harryNo ratings yet

- Other Income Tax AccountingDocument19 pagesOther Income Tax AccountingHabtamu Hailemariam AsfawNo ratings yet

- Asia Counsel Insights August 2017Document2 pagesAsia Counsel Insights August 2017C_schaeferNo ratings yet

- Capital Cost Allowances and Cumulative Eligible Capital: How Tax Addresses Depreciable PropertyDocument31 pagesCapital Cost Allowances and Cumulative Eligible Capital: How Tax Addresses Depreciable PropertyJamalNo ratings yet

- HO 3 - Journal Entries - Revenue and Other ReceiptsDocument9 pagesHO 3 - Journal Entries - Revenue and Other ReceiptsMELBERT JOHN M. BRILLANTESNo ratings yet

- Taxation of CompaniesDocument3 pagesTaxation of CompaniesJEBET RUTH KIPLAGATNo ratings yet

- Capital Gain and Rent Income TaxDocument40 pagesCapital Gain and Rent Income TaxObeng CliffNo ratings yet

- December 2010 TC10BQDocument11 pagesDecember 2010 TC10BQkalowekamoNo ratings yet

- 1) JSK Has To Determine With Tax Method That It Wishes To Adopt Prior To We Being Able To Go Forward With The Tax SimulationsDocument2 pages1) JSK Has To Determine With Tax Method That It Wishes To Adopt Prior To We Being Able To Go Forward With The Tax SimulationsJSK1 JSK11No ratings yet

- Tax Assignment Question 3Document5 pagesTax Assignment Question 3Rick WaveyNo ratings yet

- CG Digital Assets 2022 - 0Document18 pagesCG Digital Assets 2022 - 0sami ullahNo ratings yet

- Ril Pe Price Dt. 01.11.2016Document29 pagesRil Pe Price Dt. 01.11.2016Akshat Engineers Private LimitedNo ratings yet

- Buckwold 21e - CH 6 Selected SolutionsDocument25 pagesBuckwold 21e - CH 6 Selected SolutionsLucy100% (1)

- Bir Ruling Da (Vat 050) 282 09Document3 pagesBir Ruling Da (Vat 050) 282 09doraemoanNo ratings yet

- Tax Digests VATDocument27 pagesTax Digests VATBer Sib JosNo ratings yet

- Value Added Tax Lecture Summary 2020Document72 pagesValue Added Tax Lecture Summary 2020Tatenda RamsNo ratings yet

- AFF's Tax Memorandum - Changes in Finance Bill, 2023 (Pakistan)Document14 pagesAFF's Tax Memorandum - Changes in Finance Bill, 2023 (Pakistan)salahuddin ahmedNo ratings yet

- Taxation Management and PlanningDocument10 pagesTaxation Management and PlanningJoel EdauNo ratings yet

- Ril Pe Price Dt. 01.01.2017Document29 pagesRil Pe Price Dt. 01.01.2017Akshat Engineers Private LimitedNo ratings yet

- Practical Illustrations On Indirect TaxationDocument9 pagesPractical Illustrations On Indirect Taxationsridharan1969No ratings yet

- Taxation Bar QuestionsDocument32 pagesTaxation Bar QuestionsthebeautyinsideNo ratings yet

- Checklist For Post Merger - CompliancesDocument4 pagesChecklist For Post Merger - CompliancesgautamNo ratings yet

- MTF Tax Journal July 2021Document27 pagesMTF Tax Journal July 2021Earle EdraNo ratings yet

- RR 05-09 (Sale of RP)Document7 pagesRR 05-09 (Sale of RP)joefieNo ratings yet

- Newsletter V10 Oct 2023Document47 pagesNewsletter V10 Oct 2023mohinlaskar123No ratings yet

- Rental IncomeDocument3 pagesRental IncomeZhen WeiNo ratings yet

- 04 Taxation-Law-Suggested-Answer-2019 - BRI98Document20 pages04 Taxation-Law-Suggested-Answer-2019 - BRI98Margarita AvilaNo ratings yet

- Tax 1 - Ass No. 2Document2 pagesTax 1 - Ass No. 2De Guzman E AldrinNo ratings yet

- Taxing A Sovereign Wealth FundDocument6 pagesTaxing A Sovereign Wealth FundEllis Louise LansanganNo ratings yet

- 1999 ITAD RulingsDocument97 pages1999 ITAD RulingsJerwin DaveNo ratings yet

- Review Questions On Standard-1Document4 pagesReview Questions On Standard-1George Adjei100% (1)

- Taxation Philippines Leasehold Improvements PDF FreeDocument17 pagesTaxation Philippines Leasehold Improvements PDF FreejjNo ratings yet

- Revenews 201709 PDFDocument5 pagesRevenews 201709 PDFScott FullerNo ratings yet

- Philippine National Construction Corporation Executive Summary 2019Document5 pagesPhilippine National Construction Corporation Executive Summary 2019reslazaroNo ratings yet

- Ias 12,7 Ifrs 9Document10 pagesIas 12,7 Ifrs 9AssignemntNo ratings yet

- Slaughter and May: Equipment LeasingDocument53 pagesSlaughter and May: Equipment LeasingpitamberNo ratings yet

- Chapter 3 - Measuring and Reporting Financial Performance: Discussion Questions - Easy 3.5 LO5Document4 pagesChapter 3 - Measuring and Reporting Financial Performance: Discussion Questions - Easy 3.5 LO5Yosua SaroinsongNo ratings yet

- My Tax Espresso Newsletter Apr2023Document18 pagesMy Tax Espresso Newsletter Apr2023Claudine TanNo ratings yet

- Indian GST Reference ManualDocument594 pagesIndian GST Reference ManualY M Shah & Co100% (5)

- Module 6Document4 pagesModule 6Rachelle Mae NagalesNo ratings yet

- BLGF Opinion To Alsons Consolidated Resources Inc Dated 23 September 2009Document4 pagesBLGF Opinion To Alsons Consolidated Resources Inc Dated 23 September 2009Chasmere MagloyuanNo ratings yet

- A) Date Description Debit $ Credit $Document5 pagesA) Date Description Debit $ Credit $simranNo ratings yet

- Mail To Sana SB - Final QuerriesDocument2 pagesMail To Sana SB - Final QuerriesMuhammad Ammar KhanNo ratings yet

- Case Study: American AirlinesDocument4 pagesCase Study: American Airlinesapi-243311267No ratings yet

- Green Revolution in Pakistan by Umair Alam 1817143Document4 pagesGreen Revolution in Pakistan by Umair Alam 1817143Umair RehmanNo ratings yet

- Credit Annual STMTDocument9 pagesCredit Annual STMTKunalKumarNo ratings yet

- Marketing Management Final ExamDocument1 pageMarketing Management Final ExamDavy RoseNo ratings yet

- Reckitt Benckiser Is A World Leader in HouseholdDocument16 pagesReckitt Benckiser Is A World Leader in HouseholdWaqasNo ratings yet

- Three Levels of StrategyDocument14 pagesThree Levels of Strategytmaha87No ratings yet

- Cutviewer Mill User Guide V3Document19 pagesCutviewer Mill User Guide V3Arya SengkuniNo ratings yet

- List of Qualified Manufacturers Supplierss July 2019 Final DraftDocument49 pagesList of Qualified Manufacturers Supplierss July 2019 Final DraftMohammad Abo AliNo ratings yet

- Activity Analysis and Linkages For Shelter EfficiencyDocument11 pagesActivity Analysis and Linkages For Shelter EfficiencyRezelle May Manalo Dagooc100% (3)

- JSC Healthy Water IncDocument16 pagesJSC Healthy Water IncMargebeliHoldingNo ratings yet

- DSE New Board Members 2016Document1 pageDSE New Board Members 2016Anonymous FnM14a0No ratings yet

- Development EconomicsDocument4 pagesDevelopment EconomicstitimaNo ratings yet

- Techtonic Summit 2019 - Exhibitor's Manual (Final)Document20 pagesTechtonic Summit 2019 - Exhibitor's Manual (Final)Mei AcuinNo ratings yet

- Grade 6-Pretest On ComsumerDocument17 pagesGrade 6-Pretest On ComsumerAndrea Jarani LinezoNo ratings yet

- Sovereign Wealth FundsDocument1 pageSovereign Wealth Fundschris jonasNo ratings yet

- 2 - Economics - Formula Sheet Mini TestDocument6 pages2 - Economics - Formula Sheet Mini Testcpacfa100% (1)

- The Myth of Basic Science - WSJDocument8 pagesThe Myth of Basic Science - WSJDenizen GuptaNo ratings yet

- Students' Login & Password For PMS SystemDocument26 pagesStudents' Login & Password For PMS SystemDiana ZholdubaevaNo ratings yet

- 858 Accounts QPDocument11 pages858 Accounts QPRudra SahaNo ratings yet

- FCRA Notice To FurnishersDocument3 pagesFCRA Notice To Furnishersfox_pae_pevmou100% (1)

- 5 WEEK GEHon Economics IIth Semeter Introductory MacroeconomicsDocument14 pages5 WEEK GEHon Economics IIth Semeter Introductory Macroeconomicskasturisahoo20No ratings yet

- Global Cosmetics Industry Prospects 2009 Euromonitor 08 09Document66 pagesGlobal Cosmetics Industry Prospects 2009 Euromonitor 08 09Gaurav Om SharmaNo ratings yet

- U S DividendchampionsDocument251 pagesU S Dividendchampionstirath5uNo ratings yet

- ®J ML B CN G¡ycDocument10 pages®J ML B CN G¡ycSwapan GhoshNo ratings yet

- Vodacom Annual Report PDFDocument148 pagesVodacom Annual Report PDFDaniel DumitricăNo ratings yet

- College of Agriculture and ForestryDocument3 pagesCollege of Agriculture and ForestryMercy FullNo ratings yet

- Case Study Fashion Enterprises ABCDocument2 pagesCase Study Fashion Enterprises ABCArun KCNo ratings yet

- Land Rent Theory RevisitedDocument23 pagesLand Rent Theory Revisitedezguerra100% (1)

Download as pdf or txt

You might also like

- Buckwold20e Solutions Ch06Document93 pagesBuckwold20e Solutions Ch06Aman Lottay100% (1)

- BIR Ruling (DA-005-07) (Travel Agencies) PDFDocument4 pagesBIR Ruling (DA-005-07) (Travel Agencies) PDFAl Marvin0% (2)

- Fiscal and Monetary Policy of GermanyDocument125 pagesFiscal and Monetary Policy of Germanyarpit vora100% (2)

- Tugasan Berkumpulan Valuation Methodology (DDWF 1423) : Nama Pensyarah: Puan DR Noraini Binti RejabDocument27 pagesTugasan Berkumpulan Valuation Methodology (DDWF 1423) : Nama Pensyarah: Puan DR Noraini Binti Rejabhilman afiq100% (1)

- 7capital Gain TaxationDocument23 pages7capital Gain TaxationWINSTON YATICHNo ratings yet

- Proposed Tax Changes Under The Finance Bill 2023 Snapshot - ALN Kenya Legal AlertDocument20 pagesProposed Tax Changes Under The Finance Bill 2023 Snapshot - ALN Kenya Legal AlertKafonyi JohnNo ratings yet

- Canadian Income Taxation 2014 2015 Planning and Decision Making Canadian 17th Edition Buckwold Solutions Manual 1Document36 pagesCanadian Income Taxation 2014 2015 Planning and Decision Making Canadian 17th Edition Buckwold Solutions Manual 1aliciahollandygimjrqotk100% (29)

- Canadian Income Taxation 2014 2015 Planning and Decision Making Canadian 17Th Edition Buckwold Solutions Manual Full Chapter PDFDocument36 pagesCanadian Income Taxation 2014 2015 Planning and Decision Making Canadian 17Th Edition Buckwold Solutions Manual Full Chapter PDFkenneth.cappello861100% (21)

- CGT Presentation - LSK CLE October 2016Document25 pagesCGT Presentation - LSK CLE October 2016Mulindi KhayesiNo ratings yet

- Guide To CW QnsDocument12 pagesGuide To CW QnsMwebembezi Mark EricNo ratings yet

- Taxation Q&ADocument18 pagesTaxation Q&AZsazsaNo ratings yet

- Chapter 11 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Document20 pagesChapter 11 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din SheryarNo ratings yet

- Question As Emailed To Us On 24 Oct 2020 by Safique SardarDocument4 pagesQuestion As Emailed To Us On 24 Oct 2020 by Safique SardarSk Asif AliNo ratings yet

- Kenya Revenue Authority: Domestic Taxes DepartmentDocument19 pagesKenya Revenue Authority: Domestic Taxes DepartmentEmeka NkemNo ratings yet

- Corporate Reporting Assignment 1 - GroupDocument18 pagesCorporate Reporting Assignment 1 - GroupangelaNo ratings yet

- AAT L3 FAPS Revision Questions 1Document7 pagesAAT L3 FAPS Revision Questions 1uzytkownik2207No ratings yet

- Uganda Issues Tax Amendment Bills 2020Document6 pagesUganda Issues Tax Amendment Bills 2020harryNo ratings yet

- Other Income Tax AccountingDocument19 pagesOther Income Tax AccountingHabtamu Hailemariam AsfawNo ratings yet

- Asia Counsel Insights August 2017Document2 pagesAsia Counsel Insights August 2017C_schaeferNo ratings yet

- Capital Cost Allowances and Cumulative Eligible Capital: How Tax Addresses Depreciable PropertyDocument31 pagesCapital Cost Allowances and Cumulative Eligible Capital: How Tax Addresses Depreciable PropertyJamalNo ratings yet

- HO 3 - Journal Entries - Revenue and Other ReceiptsDocument9 pagesHO 3 - Journal Entries - Revenue and Other ReceiptsMELBERT JOHN M. BRILLANTESNo ratings yet

- Taxation of CompaniesDocument3 pagesTaxation of CompaniesJEBET RUTH KIPLAGATNo ratings yet

- Capital Gain and Rent Income TaxDocument40 pagesCapital Gain and Rent Income TaxObeng CliffNo ratings yet

- December 2010 TC10BQDocument11 pagesDecember 2010 TC10BQkalowekamoNo ratings yet

- 1) JSK Has To Determine With Tax Method That It Wishes To Adopt Prior To We Being Able To Go Forward With The Tax SimulationsDocument2 pages1) JSK Has To Determine With Tax Method That It Wishes To Adopt Prior To We Being Able To Go Forward With The Tax SimulationsJSK1 JSK11No ratings yet

- Tax Assignment Question 3Document5 pagesTax Assignment Question 3Rick WaveyNo ratings yet

- CG Digital Assets 2022 - 0Document18 pagesCG Digital Assets 2022 - 0sami ullahNo ratings yet

- Ril Pe Price Dt. 01.11.2016Document29 pagesRil Pe Price Dt. 01.11.2016Akshat Engineers Private LimitedNo ratings yet

- Buckwold 21e - CH 6 Selected SolutionsDocument25 pagesBuckwold 21e - CH 6 Selected SolutionsLucy100% (1)

- Bir Ruling Da (Vat 050) 282 09Document3 pagesBir Ruling Da (Vat 050) 282 09doraemoanNo ratings yet

- Tax Digests VATDocument27 pagesTax Digests VATBer Sib JosNo ratings yet

- Value Added Tax Lecture Summary 2020Document72 pagesValue Added Tax Lecture Summary 2020Tatenda RamsNo ratings yet

- AFF's Tax Memorandum - Changes in Finance Bill, 2023 (Pakistan)Document14 pagesAFF's Tax Memorandum - Changes in Finance Bill, 2023 (Pakistan)salahuddin ahmedNo ratings yet

- Taxation Management and PlanningDocument10 pagesTaxation Management and PlanningJoel EdauNo ratings yet

- Ril Pe Price Dt. 01.01.2017Document29 pagesRil Pe Price Dt. 01.01.2017Akshat Engineers Private LimitedNo ratings yet

- Practical Illustrations On Indirect TaxationDocument9 pagesPractical Illustrations On Indirect Taxationsridharan1969No ratings yet

- Taxation Bar QuestionsDocument32 pagesTaxation Bar QuestionsthebeautyinsideNo ratings yet

- Checklist For Post Merger - CompliancesDocument4 pagesChecklist For Post Merger - CompliancesgautamNo ratings yet

- MTF Tax Journal July 2021Document27 pagesMTF Tax Journal July 2021Earle EdraNo ratings yet

- RR 05-09 (Sale of RP)Document7 pagesRR 05-09 (Sale of RP)joefieNo ratings yet

- Newsletter V10 Oct 2023Document47 pagesNewsletter V10 Oct 2023mohinlaskar123No ratings yet

- Rental IncomeDocument3 pagesRental IncomeZhen WeiNo ratings yet

- 04 Taxation-Law-Suggested-Answer-2019 - BRI98Document20 pages04 Taxation-Law-Suggested-Answer-2019 - BRI98Margarita AvilaNo ratings yet

- Tax 1 - Ass No. 2Document2 pagesTax 1 - Ass No. 2De Guzman E AldrinNo ratings yet

- Taxing A Sovereign Wealth FundDocument6 pagesTaxing A Sovereign Wealth FundEllis Louise LansanganNo ratings yet

- 1999 ITAD RulingsDocument97 pages1999 ITAD RulingsJerwin DaveNo ratings yet

- Review Questions On Standard-1Document4 pagesReview Questions On Standard-1George Adjei100% (1)

- Taxation Philippines Leasehold Improvements PDF FreeDocument17 pagesTaxation Philippines Leasehold Improvements PDF FreejjNo ratings yet

- Revenews 201709 PDFDocument5 pagesRevenews 201709 PDFScott FullerNo ratings yet

- Philippine National Construction Corporation Executive Summary 2019Document5 pagesPhilippine National Construction Corporation Executive Summary 2019reslazaroNo ratings yet

- Ias 12,7 Ifrs 9Document10 pagesIas 12,7 Ifrs 9AssignemntNo ratings yet

- Slaughter and May: Equipment LeasingDocument53 pagesSlaughter and May: Equipment LeasingpitamberNo ratings yet

- Chapter 3 - Measuring and Reporting Financial Performance: Discussion Questions - Easy 3.5 LO5Document4 pagesChapter 3 - Measuring and Reporting Financial Performance: Discussion Questions - Easy 3.5 LO5Yosua SaroinsongNo ratings yet

- My Tax Espresso Newsletter Apr2023Document18 pagesMy Tax Espresso Newsletter Apr2023Claudine TanNo ratings yet

- Indian GST Reference ManualDocument594 pagesIndian GST Reference ManualY M Shah & Co100% (5)

- Module 6Document4 pagesModule 6Rachelle Mae NagalesNo ratings yet

- BLGF Opinion To Alsons Consolidated Resources Inc Dated 23 September 2009Document4 pagesBLGF Opinion To Alsons Consolidated Resources Inc Dated 23 September 2009Chasmere MagloyuanNo ratings yet

- A) Date Description Debit $ Credit $Document5 pagesA) Date Description Debit $ Credit $simranNo ratings yet

- Mail To Sana SB - Final QuerriesDocument2 pagesMail To Sana SB - Final QuerriesMuhammad Ammar KhanNo ratings yet

- Case Study: American AirlinesDocument4 pagesCase Study: American Airlinesapi-243311267No ratings yet

- Green Revolution in Pakistan by Umair Alam 1817143Document4 pagesGreen Revolution in Pakistan by Umair Alam 1817143Umair RehmanNo ratings yet

- Credit Annual STMTDocument9 pagesCredit Annual STMTKunalKumarNo ratings yet

- Marketing Management Final ExamDocument1 pageMarketing Management Final ExamDavy RoseNo ratings yet

- Reckitt Benckiser Is A World Leader in HouseholdDocument16 pagesReckitt Benckiser Is A World Leader in HouseholdWaqasNo ratings yet

- Three Levels of StrategyDocument14 pagesThree Levels of Strategytmaha87No ratings yet

- Cutviewer Mill User Guide V3Document19 pagesCutviewer Mill User Guide V3Arya SengkuniNo ratings yet

- List of Qualified Manufacturers Supplierss July 2019 Final DraftDocument49 pagesList of Qualified Manufacturers Supplierss July 2019 Final DraftMohammad Abo AliNo ratings yet

- Activity Analysis and Linkages For Shelter EfficiencyDocument11 pagesActivity Analysis and Linkages For Shelter EfficiencyRezelle May Manalo Dagooc100% (3)

- JSC Healthy Water IncDocument16 pagesJSC Healthy Water IncMargebeliHoldingNo ratings yet

- DSE New Board Members 2016Document1 pageDSE New Board Members 2016Anonymous FnM14a0No ratings yet

- Development EconomicsDocument4 pagesDevelopment EconomicstitimaNo ratings yet

- Techtonic Summit 2019 - Exhibitor's Manual (Final)Document20 pagesTechtonic Summit 2019 - Exhibitor's Manual (Final)Mei AcuinNo ratings yet

- Grade 6-Pretest On ComsumerDocument17 pagesGrade 6-Pretest On ComsumerAndrea Jarani LinezoNo ratings yet

- Sovereign Wealth FundsDocument1 pageSovereign Wealth Fundschris jonasNo ratings yet

- 2 - Economics - Formula Sheet Mini TestDocument6 pages2 - Economics - Formula Sheet Mini Testcpacfa100% (1)

- The Myth of Basic Science - WSJDocument8 pagesThe Myth of Basic Science - WSJDenizen GuptaNo ratings yet

- Students' Login & Password For PMS SystemDocument26 pagesStudents' Login & Password For PMS SystemDiana ZholdubaevaNo ratings yet

- 858 Accounts QPDocument11 pages858 Accounts QPRudra SahaNo ratings yet

- FCRA Notice To FurnishersDocument3 pagesFCRA Notice To Furnishersfox_pae_pevmou100% (1)

- 5 WEEK GEHon Economics IIth Semeter Introductory MacroeconomicsDocument14 pages5 WEEK GEHon Economics IIth Semeter Introductory Macroeconomicskasturisahoo20No ratings yet

- Global Cosmetics Industry Prospects 2009 Euromonitor 08 09Document66 pagesGlobal Cosmetics Industry Prospects 2009 Euromonitor 08 09Gaurav Om SharmaNo ratings yet

- U S DividendchampionsDocument251 pagesU S Dividendchampionstirath5uNo ratings yet

- ®J ML B CN G¡ycDocument10 pages®J ML B CN G¡ycSwapan GhoshNo ratings yet

- Vodacom Annual Report PDFDocument148 pagesVodacom Annual Report PDFDaniel DumitricăNo ratings yet

- College of Agriculture and ForestryDocument3 pagesCollege of Agriculture and ForestryMercy FullNo ratings yet

- Case Study Fashion Enterprises ABCDocument2 pagesCase Study Fashion Enterprises ABCArun KCNo ratings yet

- Land Rent Theory RevisitedDocument23 pagesLand Rent Theory Revisitedezguerra100% (1)