Download as pdf or txt

You might also like

- Outstanding DigestDocument10 pagesOutstanding DigestKarthi KeyanNo ratings yet

- Booking Report 11-23-2021Document3 pagesBooking Report 11-23-2021WCTV Digital TeamNo ratings yet

- Excerpt - Eastsouth AsiaDocument63 pagesExcerpt - Eastsouth AsiaAbhi Karmyal100% (2)

- Module 6.9 TLEDocument115 pagesModule 6.9 TLEroseavy90% (10)

- Development Perspectives of The Natural Gas Industry: Superintendência de Infraestrutura e Movimentação-SIMDocument19 pagesDevelopment Perspectives of The Natural Gas Industry: Superintendência de Infraestrutura e Movimentação-SIMRuan Duarte Jales AnselmoNo ratings yet

- Webinar Vehicle To GridDocument28 pagesWebinar Vehicle To GridProvocateur SamaraNo ratings yet

- Asianpaints: Sub: Investor PresentationDocument25 pagesAsianpaints: Sub: Investor PresentationPrathamNo ratings yet

- Mastering The Steel CyclesDocument33 pagesMastering The Steel CyclesSiddharthNo ratings yet

- 2019.06.04 Bisaggio Natural GasDocument18 pages2019.06.04 Bisaggio Natural GasVictor MafraNo ratings yet

- Report On Tyres Sector by PACRADocument31 pagesReport On Tyres Sector by PACRAKhuram KhanNo ratings yet

- ENR Top 250 InternationalContractorsDocument77 pagesENR Top 250 InternationalContractorsIuliana FolteaNo ratings yet

- Combustion Course-982Document70 pagesCombustion Course-982hassan ghNo ratings yet

- Moss Soil Cement FDR ACPA MTG Nov 2018Document29 pagesMoss Soil Cement FDR ACPA MTG Nov 2018Jose RamirNo ratings yet

- Downstream GCC Market - May2018 PDFDocument84 pagesDownstream GCC Market - May2018 PDFvaruninderNo ratings yet

- 2015-09-17 PM 12 by Li Yao CNDocument21 pages2015-09-17 PM 12 by Li Yao CNDare SmithNo ratings yet

- Applied Maths ProjectDocument10 pagesApplied Maths ProjectDarsh KansalNo ratings yet

- April Cars UVsDocument37 pagesApril Cars UVsMalay Kumar PatraNo ratings yet

- Article Impairment Study 2008Document12 pagesArticle Impairment Study 2008Aung Kyaw MyoNo ratings yet

- Integrating Refining petrochemicaGBPs For Increased chemicaGBPs ProductionDocument4 pagesIntegrating Refining petrochemicaGBPs For Increased chemicaGBPs ProductionajayNo ratings yet

- Residential%Document2 pagesResidential%Anonymous 0jVmoZNo ratings yet

- Pitch Madison Advertising Report 2020 (Mid Year Review)Document31 pagesPitch Madison Advertising Report 2020 (Mid Year Review)Aadhar BhardwajNo ratings yet

- Mi Ken Conference 08Document7 pagesMi Ken Conference 08sebascianNo ratings yet

- TVS MOTORS by AmbitDocument15 pagesTVS MOTORS by Ambitrs reddy100% (1)

- Britannia P&I Annual Report and Financial Statements 2017 - 06 PDFDocument54 pagesBritannia P&I Annual Report and Financial Statements 2017 - 06 PDFToheid AsadiNo ratings yet

- Sample - Caramel Ingredients Market - Global Trends and Forecast To 2021Document19 pagesSample - Caramel Ingredients Market - Global Trends and Forecast To 2021bucadinhoNo ratings yet

- Hidden Gems Portfolio StrategyDocument6 pagesHidden Gems Portfolio StrategyAllur Sai Vijay KumarNo ratings yet

- Chemicals Infographic November 2020Document1 pageChemicals Infographic November 2020SimranNo ratings yet

- India Pesticides LimitedDocument2 pagesIndia Pesticides LimitedyashNo ratings yet

- Insights 2030 Energy Mix Marching Towards A Cleaner FutureDocument80 pagesInsights 2030 Energy Mix Marching Towards A Cleaner Future@yuanNo ratings yet

- Ev in IndiaDocument26 pagesEv in Indiakiran kumarNo ratings yet

- Amara Raja Maximus ResearchDocument12 pagesAmara Raja Maximus ResearchVikas SinghNo ratings yet

- Power Sector - PACRA Research - Jan'21 - 1611329371Document36 pagesPower Sector - PACRA Research - Jan'21 - 1611329371ZarkKhanNo ratings yet

- Automobile July 2018Document1 pageAutomobile July 2018Tanmay AgarwalNo ratings yet

- Energy Markets 2018Document6 pagesEnergy Markets 2018jjavaid2k16No ratings yet

- Revision Notes On Economy of J&K by Vidhya Tutorials.Document7 pagesRevision Notes On Economy of J&K by Vidhya Tutorials.MuzaFar100% (1)

- Course Project ReportDocument37 pagesCourse Project ReportHans SamNo ratings yet

- PWC Global Crypto M A and Fundraising Report April 2020Document28 pagesPWC Global Crypto M A and Fundraising Report April 2020ForkLogNo ratings yet

- UNECE-Azerbaijan RailwaysDocument18 pagesUNECE-Azerbaijan RailwaysArseneNo ratings yet

- Presentación AeropuertoDocument19 pagesPresentación AeropuertoDaniel Fumero LázaroNo ratings yet

- Accounting Closing StepsDocument24 pagesAccounting Closing StepsAnabelRodriguezNo ratings yet

- JSW FinalsDocument11 pagesJSW FinalsRahul AgrawalNo ratings yet

- ColorCity Flour-MillDocument52 pagesColorCity Flour-MillANM Azam MehrabNo ratings yet

- Sample of Fixed Asset ScheduleDocument1 pageSample of Fixed Asset ScheduleAnnie ChewNo ratings yet

- GCC Telecom Insight - Issued by STC Kuwait - April 2020Document29 pagesGCC Telecom Insight - Issued by STC Kuwait - April 2020AKNo ratings yet

- PMEX Daily Statistical Report Aug 17 2023Document3 pagesPMEX Daily Statistical Report Aug 17 2023tyb thrNo ratings yet

- A New Sugar Complex Designed To Provide Maximum Raw Material To A Paper IndustryDocument36 pagesA New Sugar Complex Designed To Provide Maximum Raw Material To A Paper IndustryTriyono S. SiNo ratings yet

- Cement Report - AurumDocument11 pagesCement Report - AurumexcitingalmeidaNo ratings yet

- Conquerors ImpactInvestorDocument10 pagesConquerors ImpactInvestorbatman jonasNo ratings yet

- Tabafresh To Base HuimanguilloDocument4 pagesTabafresh To Base HuimanguillopimowallaceNo ratings yet

- Ibiza Airport: Power BI DesktopDocument19 pagesIbiza Airport: Power BI DesktopDaniel FiañoNo ratings yet

- Pgs 13102022Document10 pagesPgs 13102022Contacto Ex-AnteNo ratings yet

- Jesus Tamang. Philippines. Low Carbon Growth Strategies and ChallengesDocument24 pagesJesus Tamang. Philippines. Low Carbon Growth Strategies and ChallengeslncguevaraNo ratings yet

- Notice With List Incoming Outgoing KMI ALL Shares July 01 2019 Dec 31 2019Document18 pagesNotice With List Incoming Outgoing KMI ALL Shares July 01 2019 Dec 31 2019Syed Huzaifa Ahmed (Larf Nalavale)No ratings yet

- ABB - Factsheet - February 3 - 2022 PDFDocument18 pagesABB - Factsheet - February 3 - 2022 PDFSaifa KhalidNo ratings yet

- Lectura 3 PANORAMA ENERGETICO 2018Document44 pagesLectura 3 PANORAMA ENERGETICO 2018Raiser Estrada MachaccaNo ratings yet

- Bioenergy TeachingDocument87 pagesBioenergy TeachingKrishnendu NayekNo ratings yet

- Account Information Sample Information Equipment InformationDocument2 pagesAccount Information Sample Information Equipment InformationHaitham YoussefNo ratings yet

- Tuesday 12pm - Li-Ion Battery Recycling - IHS Markit - Energy Storage Virtual SummitDocument19 pagesTuesday 12pm - Li-Ion Battery Recycling - IHS Markit - Energy Storage Virtual SummitRonak BhandariNo ratings yet

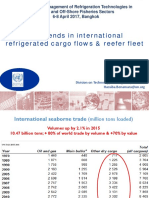

- Key Trends in International Refrigerated Cargo Flows & Reefer FleetDocument21 pagesKey Trends in International Refrigerated Cargo Flows & Reefer FleetMiguel Rodríguez SoutoNo ratings yet

- Tevta Short Course: Trade Wise Pass PercentageDocument2 pagesTevta Short Course: Trade Wise Pass PercentageKashif ChaudharyNo ratings yet

- Auto Sector ReportDocument18 pagesAuto Sector ReportAnurag KhandelwalNo ratings yet

- Kirby Market SegmentationDocument1 pageKirby Market Segmentationsuk1234No ratings yet

- Road Funds and Road User Charges in the CAREC RegionFrom EverandRoad Funds and Road User Charges in the CAREC RegionNo ratings yet

- CH 8 Answer Key CK-12 MSM Concepts - Grade 6 PDFDocument8 pagesCH 8 Answer Key CK-12 MSM Concepts - Grade 6 PDFKarthi KeyanNo ratings yet

- Understanding FRDocument11 pagesUnderstanding FRKarthi KeyanNo ratings yet

- L2 SortingDocument3 pagesL2 SortingKarthi KeyanNo ratings yet

- GraphDocument3 pagesGraphKarthi KeyanNo ratings yet

- Unless Mentioned Otherwise, Assume The Players To Be Individually Rational and Risk-NeutralDocument3 pagesUnless Mentioned Otherwise, Assume The Players To Be Individually Rational and Risk-NeutralKarthi KeyanNo ratings yet

- GD TopicsDocument1 pageGD TopicsKarthi KeyanNo ratings yet

- Which Market & Why Set Up Cost Rent (Annual Exclation) How Much Units To Breakeven Construction Cost Human PowerDocument2 pagesWhich Market & Why Set Up Cost Rent (Annual Exclation) How Much Units To Breakeven Construction Cost Human PowerKarthi KeyanNo ratings yet

- R & D Converter: InputsDocument6 pagesR & D Converter: InputsKarthi KeyanNo ratings yet

- 03 - Rise of The Allies 1Document41 pages03 - Rise of The Allies 1evanpate0No ratings yet

- Study Guide Exponents and Scientific NotationDocument6 pagesStudy Guide Exponents and Scientific Notationapi-276774049No ratings yet

- CS701 - Theory of Computation Assignment No.1: InstructionsDocument2 pagesCS701 - Theory of Computation Assignment No.1: InstructionsIhsanullah KhanNo ratings yet

- Operating Range Recommended Applications: Mechanical Seals - Mechanical Seals For Pumps - Pusher SealsDocument3 pagesOperating Range Recommended Applications: Mechanical Seals - Mechanical Seals For Pumps - Pusher Sealsneurolepsia3790No ratings yet

- The Outlaw (1871)Document21 pagesThe Outlaw (1871)ViannisoNo ratings yet

- The Brain and Nervous System (Psychology) Unit 14: An Academic ReportDocument7 pagesThe Brain and Nervous System (Psychology) Unit 14: An Academic ReportOlatokunbo SinaayomiNo ratings yet

- Medical-Spanish TrainingDocument48 pagesMedical-Spanish TrainingDavid FastoonNo ratings yet

- Group 1 Dorb001 Bsce3aDocument16 pagesGroup 1 Dorb001 Bsce3aJan TheGamerNo ratings yet

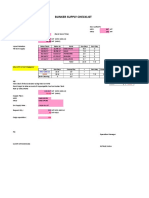

- Bunker & FW Supply ChecklistDocument3 pagesBunker & FW Supply ChecklistSampetua StmrgNo ratings yet

- Pre Board POL - SCI Paper 2Document6 pagesPre Board POL - SCI Paper 2harsh jatNo ratings yet

- Load Cell ActuatorsDocument2 pagesLoad Cell Actuatorssandeep100% (1)

- BPC Midterm Exam Math Hrs 2019Document4 pagesBPC Midterm Exam Math Hrs 2019Clara Jane CaparasNo ratings yet

- GL005 PIPE ROUTING GUIDELINE Rev 2Document22 pagesGL005 PIPE ROUTING GUIDELINE Rev 2MIlan100% (1)

- Introduction To Time and Frequency MetrologyDocument30 pagesIntroduction To Time and Frequency MetrologyJBSfanNo ratings yet

- What Is Total Quality ManagementDocument4 pagesWhat Is Total Quality ManagementJayson Villena MalimataNo ratings yet

- Opsrey - Acre 1291Document97 pagesOpsrey - Acre 1291Hieronymus Sousa PintoNo ratings yet

- UntitledDocument17 pagesUntitledCarlo MoranNo ratings yet

- IA BrochureDocument12 pagesIA BrochureChris WallaceNo ratings yet

- Math Chapter 3 Study GuideDocument3 pagesMath Chapter 3 Study Guideapi-311999132No ratings yet

- Gas/Liquid Separators: Quantifying Separation Performance - Part 1Document10 pagesGas/Liquid Separators: Quantifying Separation Performance - Part 1sara25dec689288No ratings yet

- Category:UR Madam / Sir,: Please Affix Your Recent Passport Size Colour Photograph & Sign AcrossDocument2 pagesCategory:UR Madam / Sir,: Please Affix Your Recent Passport Size Colour Photograph & Sign AcrossVasu Ram JayanthNo ratings yet

- Determining Amount of Acetic Acid in VinegarDocument18 pagesDetermining Amount of Acetic Acid in VinegarAj100% (1)

- Irctcs E-Ticketing Service Electronic Reservation Slip (Personal User)Document1 pageIrctcs E-Ticketing Service Electronic Reservation Slip (Personal User)Jay ParkheNo ratings yet

- Interfacing Seven Segment Display To 8051Document16 pagesInterfacing Seven Segment Display To 8051Virang PatelNo ratings yet

- Westinghouse Style-Tone Mercury Vapor Lamps Bulletin 1975Document2 pagesWestinghouse Style-Tone Mercury Vapor Lamps Bulletin 1975Alan MastersNo ratings yet

- Agrirobot PDFDocument103 pagesAgrirobot PDFMuhamad Azlan ShahNo ratings yet

- CRING Bank Facilitator by SPE - BNIDocument28 pagesCRING Bank Facilitator by SPE - BNIDaniel AdrianNo ratings yet

- TIME PumpsDocument13 pagesTIME PumpsAndres RedondoNo ratings yet