Download as docx, pdf, or txt

You might also like

- Central Banking and Monetary Policy PDFDocument43 pagesCentral Banking and Monetary Policy PDFWindyee TanNo ratings yet

- Manufacturing SectorDocument6 pagesManufacturing SectorPrachi MishraNo ratings yet

- IE - Article ReviewDocument8 pagesIE - Article Review541ANUDEEP VADLAKONDANo ratings yet

- Italy Equities GarthwaiteDocument23 pagesItaly Equities GarthwaiteRichard WoolhouseNo ratings yet

- Indian Economic Growth-A1Document6 pagesIndian Economic Growth-A1parn_sharma9226No ratings yet

- Country Risk Overview: July 2010Document54 pagesCountry Risk Overview: July 2010treby22No ratings yet

- Fdi Reports From PG 6-18Document13 pagesFdi Reports From PG 6-18bn2380No ratings yet

- Balance of Payments: Recent Developments and ImplicationsDocument3 pagesBalance of Payments: Recent Developments and Implicationsshobu_iujNo ratings yet

- The Nature of Finland's Economic Crisis and The Prerequisites For Growth - MemorandumDocument30 pagesThe Nature of Finland's Economic Crisis and The Prerequisites For Growth - MemorandumHudson RabeloNo ratings yet

- Indian Economy - Nov 2019Document6 pagesIndian Economy - Nov 2019Rajeshree JadhavNo ratings yet

- Is The Economy Turning Around?Document4 pagesIs The Economy Turning Around?Rana WaqasNo ratings yet

- Emerging Market Macro Comment Recovery in Chinese Growth Is On TrackDocument2 pagesEmerging Market Macro Comment Recovery in Chinese Growth Is On TrackFlametreeNo ratings yet

- SGX-Listed InnoTek Announces Marginally Higher Q2'12 Revenue From Continuing OperationsDocument3 pagesSGX-Listed InnoTek Announces Marginally Higher Q2'12 Revenue From Continuing OperationsWeR1 Consultants Pte LtdNo ratings yet

- Indian EconomyDocument17 pagesIndian EconomymanboombaamNo ratings yet

- INSTA Economic Survey2019 20 Volume 2Document76 pagesINSTA Economic Survey2019 20 Volume 2Sri Harsha DannanaNo ratings yet

- Fis 2021 Q 1 SDocument13 pagesFis 2021 Q 1 Sdani20102015No ratings yet

- Economic Factors PESTELDocument11 pagesEconomic Factors PESTELnatalie_calabreseNo ratings yet

- Levi Institute Greece Analysis 2016Document13 pagesLevi Institute Greece Analysis 2016Chatzianagnostou GeorgeNo ratings yet

- Global Recession and Its Impact On Indian EconomyDocument4 pagesGlobal Recession and Its Impact On Indian EconomyPankaj DograNo ratings yet

- Key Issues For The Global Economy and Construction in 2011: Program, Cost, ConsultancyDocument14 pagesKey Issues For The Global Economy and Construction in 2011: Program, Cost, ConsultancyUjjal RegmiNo ratings yet

- MGSSI Japan Economic Quarterly October 2017Document4 pagesMGSSI Japan Economic Quarterly October 2017Romy Bennouli TambunanNo ratings yet

- Indian Economy FinalDocument24 pagesIndian Economy FinalArkadyuti PatraNo ratings yet

- Investor Letter - Third Quarter 2017: Source: FactsetDocument8 pagesInvestor Letter - Third Quarter 2017: Source: FactsetAnonymous Ht0MIJNo ratings yet

- Is Malaysia Deindustrializing For The Wrong Reasons?Document3 pagesIs Malaysia Deindustrializing For The Wrong Reasons?fatincameliaNo ratings yet

- ASK India Vision - Commentary - June 2020Document5 pagesASK India Vision - Commentary - June 2020Manish TandaleNo ratings yet

- ASK IEP - Commentary - June 2020Document4 pagesASK IEP - Commentary - June 2020Manish TandaleNo ratings yet

- For Next Government, How To Meet The Demand Challenge - The Indian ExpressDocument5 pagesFor Next Government, How To Meet The Demand Challenge - The Indian ExpressJayesh RathodNo ratings yet

- Investment and Growth: 1.1 Contribution AnalysisDocument5 pagesInvestment and Growth: 1.1 Contribution AnalysisaoulakhNo ratings yet

- Iv. Saving and Investment: Determinants and Policy ImplicationsDocument22 pagesIv. Saving and Investment: Determinants and Policy ImplicationsShepherd NdouNo ratings yet

- Financing The Real Economy: Issue 30 - February 2014Document5 pagesFinancing The Real Economy: Issue 30 - February 2014Shibasish BhoumikNo ratings yet

- The Economic Importance of The SectorDocument5 pagesThe Economic Importance of The SectorSourabh SenNo ratings yet

- Lec 8Document42 pagesLec 8Veronika ChauhanNo ratings yet

- Industry ReportDocument9 pagesIndustry Reportapi-545675901No ratings yet

- Vision: Personality Test Programme 2019Document5 pagesVision: Personality Test Programme 2019sureshNo ratings yet

- 2015 0622 Hale Stewart Us Equity and Economic Review For The Week of June 15 19 Better News But Still A Touch SlogDocument11 pages2015 0622 Hale Stewart Us Equity and Economic Review For The Week of June 15 19 Better News But Still A Touch SlogcasefortrilsNo ratings yet

- Industrial Policy and Sector Growth in PakistanDocument3 pagesIndustrial Policy and Sector Growth in Pakistanshah giNo ratings yet

- Hindalco Full Annual Report 2015 16Document200 pagesHindalco Full Annual Report 2015 16neettiyath1No ratings yet

- Current State of Indian Economy: November 2008Document22 pagesCurrent State of Indian Economy: November 2008mayankmangalammNo ratings yet

- JLL Italian Retail Snapshot q4 2022Document13 pagesJLL Italian Retail Snapshot q4 2022abdalrahmananas45No ratings yet

- Auto Component Sector Report: Driving Out of Uncertain TimesDocument24 pagesAuto Component Sector Report: Driving Out of Uncertain TimesAshwani PasrichaNo ratings yet

- Current State of Indian Economy: December 2008Document24 pagesCurrent State of Indian Economy: December 2008samwaltonNo ratings yet

- Final Test Business Economics MM5006 MBA Inhouse-PT Badak NGL Batch 2 Macroeconomics 13 September 2020 InstructionDocument13 pagesFinal Test Business Economics MM5006 MBA Inhouse-PT Badak NGL Batch 2 Macroeconomics 13 September 2020 InstructionMaulani CandraNo ratings yet

- India and Its BOPDocument19 pagesIndia and Its BOPAshish KhetadeNo ratings yet

- Indian EconomyDocument15 pagesIndian EconomyleoboyrulesNo ratings yet

- Questioni Di Economia e FinanzaDocument20 pagesQuestioni Di Economia e Finanzawerner71No ratings yet

- Capital Importation 2016 Q2 ProvisionalDocument11 pagesCapital Importation 2016 Q2 ProvisionalOginni SamuelNo ratings yet

- Macroeconomic Impact of PSEsDocument5 pagesMacroeconomic Impact of PSEsSomenath BiswasNo ratings yet

- Indian Economy 2008 September StatusDocument20 pagesIndian Economy 2008 September Statusani6odbr100% (6)

- EIB Investment Report 2018/2019: Retooling Europe's economyFrom EverandEIB Investment Report 2018/2019: Retooling Europe's economyNo ratings yet

- Insights Reforms Sep 2023Document34 pagesInsights Reforms Sep 2023Stathis MetsovitisNo ratings yet

- ONUDI - World Manufacturing Production - 2020 - Q1Document16 pagesONUDI - World Manufacturing Production - 2020 - Q1Jorge Gaitan-VillegasNo ratings yet

- Economic Survey 2012Document4 pagesEconomic Survey 2012NavinkiranNo ratings yet

- Recent Economic Developments in Singapore: 5 September 2017Document20 pagesRecent Economic Developments in Singapore: 5 September 2017Aroos AhmadNo ratings yet

- Unit 3 Part 1 NotesDocument4 pagesUnit 3 Part 1 NotesaimansuhaillearningNo ratings yet

- Analysis of The Asia-Pacific Paint and Coatings MarketDocument8 pagesAnalysis of The Asia-Pacific Paint and Coatings MarketjohnNo ratings yet

- State of EconomyDocument21 pagesState of EconomyHarsh KediaNo ratings yet

- Why Did Philippine Growth Drop?Document13 pagesWhy Did Philippine Growth Drop?Dyanne Yssabelle DisturaNo ratings yet

- 04 Chap1 Gvcdevreport Bprod eDocument13 pages04 Chap1 Gvcdevreport Bprod eGervine Scola Mbou LekibiNo ratings yet

- Princes of The Apocalypse ErrataDocument2 pagesPrinces of The Apocalypse ErratatonystartNo ratings yet

- Hoard of The Dragon Queen ErrataDocument1 pageHoard of The Dragon Queen Erratatonystart100% (1)

- Dungeon Master's Guide ErrataDocument1 pageDungeon Master's Guide ErratatonystartNo ratings yet

- 5e Monster Manual ErrataDocument2 pages5e Monster Manual Erratatonystart43% (7)

- Practice ProblemsDocument3 pagesPractice ProblemsalekhyaNo ratings yet

- Act 8 International Bus and TradeDocument8 pagesAct 8 International Bus and Tradejulie ann mayoNo ratings yet

- Invoice Poco ChanduDocument2 pagesInvoice Poco Chandusevalal vkbNo ratings yet

- Special Release Carabao Situation ReportDocument7 pagesSpecial Release Carabao Situation ReportYumie YamazukiNo ratings yet

- Lecture 35Document21 pagesLecture 35praneix100% (1)

- Concentrix CVG Philippines, Inc.: Description Hrs Total Description Total Taxable Earnings Mandatory Govt ContributionsDocument2 pagesConcentrix CVG Philippines, Inc.: Description Hrs Total Description Total Taxable Earnings Mandatory Govt ContributionsArmina Aguilar BaisNo ratings yet

- Regional Rural BanksDocument13 pagesRegional Rural Banksshivakumar N100% (1)

- 2014 CurrentDocument78 pages2014 CurrentSarita gurungNo ratings yet

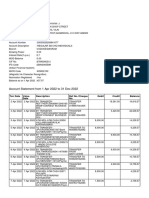

- Statement of Account: Date Tran Id Remarks UTR Number Instr. ID Withdrawals Deposits BalanceDocument2 pagesStatement of Account: Date Tran Id Remarks UTR Number Instr. ID Withdrawals Deposits BalanceNAGENDRA SINGH ShekhawatNo ratings yet

- World BankDocument9 pagesWorld BankKarnajit YengkhomNo ratings yet

- Edexcel Economics AS-level: Unit andDocument3 pagesEdexcel Economics AS-level: Unit andHussain AhmadNo ratings yet

- AtmaNirbhar BharatDocument4 pagesAtmaNirbhar Bharatsanket pandit0% (1)

- Business Environment - IIDocument1 pageBusiness Environment - IIRadhey ShyamNo ratings yet

- KC JBXDLe WU3 I 0 B AhDocument15 pagesKC JBXDLe WU3 I 0 B AhSree Rahavan100% (1)

- Zimbabwe Revenue AuthorityDocument4 pagesZimbabwe Revenue AuthorityNyasha MakoreNo ratings yet

- Banking and Insurance Law AssignmentDocument2 pagesBanking and Insurance Law AssignmentKoushiki RoyNo ratings yet

- Cashier Cashier Cashier: Payment Methods: Payment Methods: Payment MethodsDocument1 pageCashier Cashier Cashier: Payment Methods: Payment Methods: Payment MethodsMohammad HasnainNo ratings yet

- Exports - Commodities: Textiles (Garments, Bed Linen, Cotton Cloth, Yarn)Document3 pagesExports - Commodities: Textiles (Garments, Bed Linen, Cotton Cloth, Yarn)Samreen MahmoodNo ratings yet

- IBM556 Case Study ReportDocument4 pagesIBM556 Case Study ReportFaiz FahmiNo ratings yet

- Assignment On: Labor Force in BangladeshDocument6 pagesAssignment On: Labor Force in Bangladeshbony bashirNo ratings yet

- Statement 1672413844644Document11 pagesStatement 1672413844644Rachna GuptaNo ratings yet

- Trillian Eskom Invoices PDFDocument5 pagesTrillian Eskom Invoices PDFBenny BerniceNo ratings yet

- Dollar Rate Villarica Exchange Rate - Google SearchDocument1 pageDollar Rate Villarica Exchange Rate - Google SearchImelda Manzano BobisNo ratings yet

- Reserve Bank of IndiaDocument3 pagesReserve Bank of IndiaCacptCoachingNo ratings yet

- G20Document45 pagesG20NishuNo ratings yet

- International Business Case Study1Document1 pageInternational Business Case Study1RAJA SHEKHARNo ratings yet

- Manish Kandpal IBRDDocument7 pagesManish Kandpal IBRDdefdfNo ratings yet

- Questions C23-28ADocument5 pagesQuestions C23-28AQuang Anh ChuNo ratings yet

- MBA405 - Task 2: Individual Presentation: The Key External Challenges Facing Evn Finance JSC in 2011Document13 pagesMBA405 - Task 2: Individual Presentation: The Key External Challenges Facing Evn Finance JSC in 2011Nguyễn LanNo ratings yet