Download as pdf or txt

You might also like

- Structured Trade Finance in Africa Rwanda Coffee and Tea Case StudiesDocument41 pagesStructured Trade Finance in Africa Rwanda Coffee and Tea Case StudiesmsidaNo ratings yet

- BlackBuck - Case StudyDocument7 pagesBlackBuck - Case StudySwetank SahaiNo ratings yet

- Sample Question Papers For Certificate Course On Ind AS: The Institute of Chartered Accountants of IndiaDocument36 pagesSample Question Papers For Certificate Course On Ind AS: The Institute of Chartered Accountants of IndiaChristen CastilloNo ratings yet

- Iiqe Paper 5 Pastpaper 20200518Document33 pagesIiqe Paper 5 Pastpaper 20200518Tsz Ngong Ko0% (1)

- Making Exit Interviews CountDocument15 pagesMaking Exit Interviews CountRavikanth ReddyNo ratings yet

- Intacc 1 Notes - Financial Assets StartDocument8 pagesIntacc 1 Notes - Financial Assets StartKing BelicarioNo ratings yet

- FAFVPL-FAFVOCI IARev RLPDocument2 pagesFAFVPL-FAFVOCI IARev RLPBrian Daniel BayotNo ratings yet

- Equity FVPL AND FVOCI Theory For PrintingDocument3 pagesEquity FVPL AND FVOCI Theory For PrintingJaycee Ryan DimacaliNo ratings yet

- Advanced AccountingDocument33 pagesAdvanced AccountingvijaykumartaxNo ratings yet

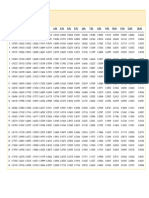

- Present Value TablesDocument3 pagesPresent Value TablesAlya SalsabilaNo ratings yet

- L2 Innovation Taxonomy 2019 2020Document40 pagesL2 Innovation Taxonomy 2019 2020JonasBasilioNo ratings yet

- Professional Pronouncement On Public Sector Accounting, Economic and Financial ImplicationDocument53 pagesProfessional Pronouncement On Public Sector Accounting, Economic and Financial ImplicationGodfrey MosesNo ratings yet

- 1 Overview of The Auditing ProfessionDocument23 pages1 Overview of The Auditing ProfessionLiam ArmendrudNo ratings yet

- Quiz 1 Ia2Document4 pagesQuiz 1 Ia2Angelica NilloNo ratings yet

- CMO - 03 - s2007 BSADocument222 pagesCMO - 03 - s2007 BSAcristinaNo ratings yet

- College of Commerce General Luna ST., Iloilo City: University of San AgustinDocument12 pagesCollege of Commerce General Luna ST., Iloilo City: University of San AgustinCJ GranadaNo ratings yet

- Analysis of Financial StatementDocument23 pagesAnalysis of Financial StatementMohammad Tariq AnsariNo ratings yet

- Ms ConsultancyDocument3 pagesMs Consultancynda0403No ratings yet

- Service CostingDocument4 pagesService CostingDr. Mustafa KozhikkalNo ratings yet

- Chapter 1 Introduction To Cost Accounting - PDF PDFDocument27 pagesChapter 1 Introduction To Cost Accounting - PDF PDFAyushi GuptaNo ratings yet

- Strategic Management PDFDocument41 pagesStrategic Management PDFArielle Joyce de JesusNo ratings yet

- Special Economic ZoneDocument34 pagesSpecial Economic ZonevrathiaNo ratings yet

- Introduction To Management Accounting: Asst Prof. Jonlen DesaDocument22 pagesIntroduction To Management Accounting: Asst Prof. Jonlen DesaAryanSainiNo ratings yet

- Additional Cash Flow ProblemsDocument3 pagesAdditional Cash Flow ProblemsChelle HullezaNo ratings yet

- Basic Notes For Borrowing CostDocument5 pagesBasic Notes For Borrowing CostIqra HasanNo ratings yet

- Transfer PricingDocument9 pagesTransfer Pricingpruthvi9999No ratings yet

- Icai Study Material MCQS: Be Chargeable To TaxDocument19 pagesIcai Study Material MCQS: Be Chargeable To TaxMr. indigoNo ratings yet

- Case StudyDocument3 pagesCase StudyPurvi LadgeNo ratings yet

- Toaz - Info Instructional Material Auditing Theory 2020 PRDocument169 pagesToaz - Info Instructional Material Auditing Theory 2020 PRVeronica Rivera100% (1)

- Financial Analysis of Food IndustryDocument8 pagesFinancial Analysis of Food Industrysona0% (1)

- A Comparative Study On Financial Performance of Private and PublicDocument17 pagesA Comparative Study On Financial Performance of Private and PublicaskmeeNo ratings yet

- Accounting Post Mid QuizDocument3 pagesAccounting Post Mid QuiztjsamiNo ratings yet

- Unit-I Introduction To Operations ManagementDocument55 pagesUnit-I Introduction To Operations ManagementMonica PurushothamanNo ratings yet

- Coneptual Frameworks and Accounting Standards Probs and TheoriesDocument17 pagesConeptual Frameworks and Accounting Standards Probs and TheoriesIris MnemosyneNo ratings yet

- IAS-37 Provisions, Contingent Liabilities and Contingent AssetsDocument3 pagesIAS-37 Provisions, Contingent Liabilities and Contingent AssetsAbdul SamiNo ratings yet

- Tax Guidelines For E-Commerce Transactions in The PhilippinesDocument44 pagesTax Guidelines For E-Commerce Transactions in The PhilippinesJanette ToralNo ratings yet

- Bond Investment - FVOCI: Subject Intermediate Accounting Teacher Dessa Dianna MadridDocument23 pagesBond Investment - FVOCI: Subject Intermediate Accounting Teacher Dessa Dianna MadridJohn Warren MestiolaNo ratings yet

- Investment in Associates ProblemsDocument4 pagesInvestment in Associates ProblemsLDB Ashley Jeremiah Magsino - ABMNo ratings yet

- IntangiblesDocument3 pagesIntangiblesJP DCNo ratings yet

- Asset For A Period of Time in Exchange For Consideration (IFRS #16)Document6 pagesAsset For A Period of Time in Exchange For Consideration (IFRS #16)Its meh SushiNo ratings yet

- Chapter 8Document6 pagesChapter 8Tooba AhmedNo ratings yet

- Capital BudgetingDocument10 pagesCapital BudgetingAkatsuki no YonaNo ratings yet

- 1.unit - 1 Nature of Financial ManagementDocument74 pages1.unit - 1 Nature of Financial ManagementGaganGabrielNo ratings yet

- Basic Financial and Accounting Systems ToolkitDocument78 pagesBasic Financial and Accounting Systems ToolkitAhsin KhanNo ratings yet

- Concept Map - Cooperatives & Construction CompaniesDocument2 pagesConcept Map - Cooperatives & Construction CompaniesSherilyn BunagNo ratings yet

- Pfrs 7 Financial Instruments DisclosuresDocument3 pagesPfrs 7 Financial Instruments DisclosuresR.A.No ratings yet

- Accounting For Borrowing Cost (English)Document9 pagesAccounting For Borrowing Cost (English)gracel angela tolejanoNo ratings yet

- Week 05 - 02 - Module 11 - Investment in Equity InstrumentsDocument10 pagesWeek 05 - 02 - Module 11 - Investment in Equity Instruments지마리No ratings yet

- 9 Property Plant and EquipmentDocument51 pages9 Property Plant and EquipmentAshraf Uz ZamanNo ratings yet

- Sabir Auto Parts Working CapitalDocument88 pagesSabir Auto Parts Working CapitalGopi NathNo ratings yet

- Ias 16Document33 pagesIas 16Kiri chris100% (1)

- PGDFM Finacial Mangment Final PDFDocument260 pagesPGDFM Finacial Mangment Final PDFAnonymous H4xWhTmNo ratings yet

- Accounting For Investment in Variable Income Bearing Securities Lesson 27Document10 pagesAccounting For Investment in Variable Income Bearing Securities Lesson 27Sumantha SahaNo ratings yet

- Annual Repot 2021-22Document110 pagesAnnual Repot 2021-22Md. Ibrahim KhalilNo ratings yet

- Investment PropertyDocument26 pagesInvestment PropertyLovemore ChigwandaNo ratings yet

- FINANCIAL MANAGEMENT AssignmentDocument9 pagesFINANCIAL MANAGEMENT AssignmentMayank BhavsarNo ratings yet

- Partnership FormationDocument24 pagesPartnership FormationKC PaulinoNo ratings yet

- Investment Vs SpeculatonDocument11 pagesInvestment Vs Speculatonkapil garg100% (1)

- CA Final Old Syllabus PDFDocument114 pagesCA Final Old Syllabus PDFKovvuri Bharadwaj ReddyNo ratings yet

- 01 Equity MethodDocument41 pages01 Equity MethodAngel Obligacion100% (1)

- Summer Internship Program Project ProposalDocument2 pagesSummer Internship Program Project ProposalPrakashNo ratings yet

- Investments DiscussionDocument5 pagesInvestments DiscussionKathrine CruzNo ratings yet

- Saw v. CA 195 SCRA 740Document4 pagesSaw v. CA 195 SCRA 740Dennis VelasquezNo ratings yet

- Padilla v. CA 320 SCRA 208Document7 pagesPadilla v. CA 320 SCRA 208Dennis VelasquezNo ratings yet

- Petition FactsDocument1 pagePetition FactsDennis VelasquezNo ratings yet

- Sesbreno v. CA 222 SCRA 466Document12 pagesSesbreno v. CA 222 SCRA 466Dennis VelasquezNo ratings yet

- Espiritu v. Petron Corp 625 SCRA 245Document9 pagesEspiritu v. Petron Corp 625 SCRA 245Dennis VelasquezNo ratings yet

- National Coal Co. v. CIR 46 Phil 583Document6 pagesNational Coal Co. v. CIR 46 Phil 583Dennis VelasquezNo ratings yet

- Pantranco v. PSCDocument6 pagesPantranco v. PSCDennis VelasquezNo ratings yet

- Philippine Airlines, Inc. v. Civil Aeronautics BoardDocument11 pagesPhilippine Airlines, Inc. v. Civil Aeronautics BoardDennis VelasquezNo ratings yet

- People v. Quasha 93 Phil 333Document5 pagesPeople v. Quasha 93 Phil 333Dennis VelasquezNo ratings yet

- ABS CBN Broadcasting Corporation v. CA 301 SCRA 589Document20 pagesABS CBN Broadcasting Corporation v. CA 301 SCRA 589Dennis VelasquezNo ratings yet

- Roman Catholic Administrator of Davao Inc. v. The LRC 102 Phil 597Document26 pagesRoman Catholic Administrator of Davao Inc. v. The LRC 102 Phil 597Dennis VelasquezNo ratings yet

- Wensha Spa Center, Inc. v. Yung 628 SCRA 311Document10 pagesWensha Spa Center, Inc. v. Yung 628 SCRA 311Dennis VelasquezNo ratings yet

- Lim Tong Lim v. Philippine Fishing Gear Industries Inc. 317 SCRA 728Document12 pagesLim Tong Lim v. Philippine Fishing Gear Industries Inc. 317 SCRA 728Dennis VelasquezNo ratings yet

- People v. Tan Boon Kong 54 Phil 607Document3 pagesPeople v. Tan Boon Kong 54 Phil 607Dennis VelasquezNo ratings yet

- Asiavest Limited vs. Court of Appeals, G.R. No. 128803, 25 September 1998Document11 pagesAsiavest Limited vs. Court of Appeals, G.R. No. 128803, 25 September 1998Dennis VelasquezNo ratings yet

- Stonehill v. Diokno 20 SCRA 383Document14 pagesStonehill v. Diokno 20 SCRA 383Dennis VelasquezNo ratings yet

- The Iloilo Ice and Cold Storage Company v. Public Utility BoardDocument7 pagesThe Iloilo Ice and Cold Storage Company v. Public Utility BoardDennis VelasquezNo ratings yet

- PNB v. Andrada Electric & Engineering Co. 381 SCRA 244Document8 pagesPNB v. Andrada Electric & Engineering Co. 381 SCRA 244Dennis VelasquezNo ratings yet

- Agan v. PIATCODocument64 pagesAgan v. PIATCODennis VelasquezNo ratings yet

- NPC v. CADocument12 pagesNPC v. CADennis VelasquezNo ratings yet

- Vazquez v. Borja 74 Phil 560Document6 pagesVazquez v. Borja 74 Phil 560Dennis VelasquezNo ratings yet

- Bank of America vs. CA, G.R. No. 120135, 31 March 2003Document8 pagesBank of America vs. CA, G.R. No. 120135, 31 March 2003Dennis VelasquezNo ratings yet

- Case Doctrines in Corporation LawDocument34 pagesCase Doctrines in Corporation LawDennis VelasquezNo ratings yet

- Saudi Arabian Airlines vs. Court of Appeals, G.R. No. 122191, 8 October 1998Document13 pagesSaudi Arabian Airlines vs. Court of Appeals, G.R. No. 122191, 8 October 1998Dennis VelasquezNo ratings yet

- MSE v. SECDocument9 pagesMSE v. SECDennis VelasquezNo ratings yet

- Gabionsa v. CADocument11 pagesGabionsa v. CADennis VelasquezNo ratings yet

- Hilton vs. GuyotDocument54 pagesHilton vs. GuyotDennis VelasquezNo ratings yet

- PSE v. CADocument11 pagesPSE v. CADennis VelasquezNo ratings yet

- Benguet Consolidated Mining v. Pineda GR No. L7231 28 March 1956Document17 pagesBenguet Consolidated Mining v. Pineda GR No. L7231 28 March 1956Dennis VelasquezNo ratings yet

- "Microfinance in Baybay City, Leyte": FM 32 Qualitative ResearchDocument6 pages"Microfinance in Baybay City, Leyte": FM 32 Qualitative ResearchIpiphaniaeFernandezItalioNo ratings yet

- On January 1Document2 pagesOn January 1Chris Tian FlorendoNo ratings yet

- Poland Republic of SEC RegistrationDocument5 pagesPoland Republic of SEC RegistrationArtur DobkowskiNo ratings yet

- Lazy Portfolios: Core and SatelliteDocument2 pagesLazy Portfolios: Core and Satellitesan291076No ratings yet

- Replace Your Mortgage Ebook - No - Companion PDFDocument62 pagesReplace Your Mortgage Ebook - No - Companion PDFJeff Smith100% (2)

- Employee Stock Option Plans ASSOCHAM Seminar On March 7, 2006 Presenter: P V SRINIVASANDocument12 pagesEmployee Stock Option Plans ASSOCHAM Seminar On March 7, 2006 Presenter: P V SRINIVASANrohitadasNo ratings yet

- Week 13 Chapter-25 FixDocument29 pagesWeek 13 Chapter-25 FixTrisula Nurulfajri PandunitaNo ratings yet

- Management Accounting Bms-Iii: Manjiri DigheDocument67 pagesManagement Accounting Bms-Iii: Manjiri Dighebhavivyas71No ratings yet

- Sample Exam - Chapter 2Document11 pagesSample Exam - Chapter 2Harold Cedric Noleal OsorioNo ratings yet

- Cat Oa167 2009Document7 pagesCat Oa167 2009Vigneshwar Raju PrathikantamNo ratings yet

- Tugas Akuntansi P1-3B Esti FatmawatiDocument2 pagesTugas Akuntansi P1-3B Esti FatmawatiEsti FatmawatiNo ratings yet

- Pbcregd 02012011Document28 pagesPbcregd 02012011Mark Anthony GrishajNo ratings yet

- 1512 GMPDocument57 pages1512 GMPpuneet aroraNo ratings yet

- Withdrawal and Surrender Form (V. 03.2019)Document2 pagesWithdrawal and Surrender Form (V. 03.2019)Penielle SaguindanNo ratings yet

- HKSI LE Handbook EngDocument31 pagesHKSI LE Handbook EngCho Hei CHANNo ratings yet

- Risk Management in Mutual Fund IndustryDocument43 pagesRisk Management in Mutual Fund Industrydeepak100% (1)

- Anshika GuptaDocument49 pagesAnshika GuptaDiksha TanejaNo ratings yet

- 23 MergersDocument44 pages23 MergerssiaapaNo ratings yet

- Summer Training Report at "Financial Performance Analysis With Ratio Analysis With Reference To South Eastern Coal Fields Limited" Bilaspur (C.G.)Document35 pagesSummer Training Report at "Financial Performance Analysis With Ratio Analysis With Reference To South Eastern Coal Fields Limited" Bilaspur (C.G.)Sanskar YadavNo ratings yet

- Resumen Chapter 19 - Intermediate AccountingDocument7 pagesResumen Chapter 19 - Intermediate AccountingDianaa Lagunes BlancoNo ratings yet

- 1VE17MBA02 (Ksic) Project AndhandDocument70 pages1VE17MBA02 (Ksic) Project AndhandMADHU SUDHAN100% (1)

- Application Summary FormDocument3 pagesApplication Summary FormnatalieNo ratings yet

- Presentation David EatockDocument22 pagesPresentation David EatockpensiontalkNo ratings yet

- Re InsuranceDocument57 pagesRe InsuranceSnehal Sawant100% (5)

- Act1205-Quiz No. 1Document3 pagesAct1205-Quiz No. 1markNo ratings yet

- Ch01 - Australian External Reporting EnvironmentDocument37 pagesCh01 - Australian External Reporting EnvironmentNguyễn Ngọc NgânNo ratings yet

- Bidding Procedure For Goods and Infra. (TYTAR)Document80 pagesBidding Procedure For Goods and Infra. (TYTAR)DianeNo ratings yet

- MM FieldsDocument83 pagesMM FieldsmkumarshahiNo ratings yet