Download as pdf or txt

You might also like

- ACC20020 Management - Accounting Exam - 22-23Document12 pagesACC20020 Management - Accounting Exam - 22-23Anonymous qRU8qVNo ratings yet

- FV Sample ProposalsDocument90 pagesFV Sample ProposalsShalom ArayaNo ratings yet

- Final Local Fiscal AdministrationDocument5 pagesFinal Local Fiscal AdministrationOliver SantosNo ratings yet

- Financial Statements GuideDocument83 pagesFinancial Statements GuideAnonymous Go6Clq100% (1)

- RJR NabiscoDocument17 pagesRJR Nabiscodanielcid100% (1)

- European Regional Policies in Light of Recent Location TheoriesDocument34 pagesEuropean Regional Policies in Light of Recent Location TheoriesIELYSON JOSE RODRIGUES DE MELONo ratings yet

- Estudio de Corrupcion en EuropaDocument28 pagesEstudio de Corrupcion en EuropaJose AbadiasNo ratings yet

- Poverty Article Benz en - 1 March 2004Document24 pagesPoverty Article Benz en - 1 March 2004ARMANDONo ratings yet

- The Solow Model - The Economic Growth of Eastern European Countries After 1989Document5 pagesThe Solow Model - The Economic Growth of Eastern European Countries After 1989Elena CalarasuNo ratings yet

- International Stock Market Integration: Central and South Eastern Europe ComparedDocument20 pagesInternational Stock Market Integration: Central and South Eastern Europe ComparedmiqbaaalllNo ratings yet

- The Socioeconomic Diversity of European Regions (WPS 131) Cristina Del Campo, Carlos M. F. Monteiro and João Oliveira Soares.Document17 pagesThe Socioeconomic Diversity of European Regions (WPS 131) Cristina Del Campo, Carlos M. F. Monteiro and João Oliveira Soares.Minda de Gunzburg Center for European Studies at Harvard UniversityNo ratings yet

- Changing Czech Consumption PatternsDocument22 pagesChanging Czech Consumption Patternspanosp10No ratings yet

- 011 2004-CC20in20EstoniaDocument32 pages011 2004-CC20in20Estoniairhad3105No ratings yet

- As GZ Eastern European Lessons For The Southern MediterraneanDocument11 pagesAs GZ Eastern European Lessons For The Southern MediterraneanBruegelNo ratings yet

- Can Eastern Europe Catch UpDocument28 pagesCan Eastern Europe Catch UpIoana PataleNo ratings yet

- Work Paper 2Document35 pagesWork Paper 2Faizan QasimNo ratings yet

- Fifteen Years of Convergence: East-West Imbalance and What The EU Should Do About ItDocument12 pagesFifteen Years of Convergence: East-West Imbalance and What The EU Should Do About ItBurim GashiNo ratings yet

- Pol Okt08-2Document16 pagesPol Okt08-2asim5595No ratings yet

- Real Convergence in The Ceecs, Euro Area Accession and The Role of RomaniaDocument22 pagesReal Convergence in The Ceecs, Euro Area Accession and The Role of RomaniaAna-MariaNo ratings yet

- Consequences of The Demographic Ageing in The EUDocument19 pagesConsequences of The Demographic Ageing in The EUHajar Ben MoussaNo ratings yet

- Changing Roles - Gender Differences in Poverty in An International ComparisonDocument16 pagesChanging Roles - Gender Differences in Poverty in An International ComparisonTARKI_ResearchNo ratings yet

- EF1168ENDocument13 pagesEF1168ENJesse WellsNo ratings yet

- 20.regions2020 DemographicDocument25 pages20.regions2020 DemographicMate AttyNo ratings yet

- Are Eastern European Countries Catching Up? Time Series Evidence For Czech Republic, Hungary, and PolandDocument9 pagesAre Eastern European Countries Catching Up? Time Series Evidence For Czech Republic, Hungary, and Polandbsergiu2No ratings yet

- Regional DisparitiesDocument15 pagesRegional Disparitiespoki627No ratings yet

- Art:10.1007/s00168 009 0296 5 PDFDocument14 pagesArt:10.1007/s00168 009 0296 5 PDFnisar.akNo ratings yet

- Changes in The Use ofDocument11 pagesChanges in The Use ofiankurniawanNo ratings yet

- Theodore LianosDocument21 pagesTheodore LianosMigili DjigiliNo ratings yet

- Subventii 4eeeeeeeeeeeeeDocument27 pagesSubventii 4eeeeeeeeeeeeePopa VasileNo ratings yet

- 321-Article Text-1293-2-10-20200811Document13 pages321-Article Text-1293-2-10-20200811Maximus L MadusNo ratings yet

- Il Parlamento EuropeoDocument30 pagesIl Parlamento EuropeoLucaNo ratings yet

- Cap Specific Objectives Brief 8 Jobs and Growth in Rural Areas en 0Document12 pagesCap Specific Objectives Brief 8 Jobs and Growth in Rural Areas en 0Andreea OnigaşNo ratings yet

- Cikk Tordelve V1augDocument11 pagesCikk Tordelve V1augFarkas MátéNo ratings yet

- Peter Van Der HoekDocument8 pagesPeter Van Der HoekapriknNo ratings yet

- Quality of Life Report 2013Document235 pagesQuality of Life Report 2013Quotidiano LaValsuganaNo ratings yet

- Catching Up and Falling Behind EconomicDocument33 pagesCatching Up and Falling Behind EconomicYuris ZegaNo ratings yet

- Financial Integration and European Priorities: Jean Pisani-Ferry (Bruegel)Document15 pagesFinancial Integration and European Priorities: Jean Pisani-Ferry (Bruegel)BruegelNo ratings yet

- Comparative Analysis of Rurban Case Study Regions PDFDocument24 pagesComparative Analysis of Rurban Case Study Regions PDFRomy Marlehn Schneider GutierrezNo ratings yet

- Right To Housing For Young People On The Housing Situation 5e0ln6pwteDocument10 pagesRight To Housing For Young People On The Housing Situation 5e0ln6pwtezahideepekerNo ratings yet

- Where The Yugoslav Economy Would Have Been Today?Document11 pagesWhere The Yugoslav Economy Would Have Been Today?Aakif SaleemNo ratings yet

- Diversity Management in The EuropeanDocument17 pagesDiversity Management in The Europeanhersi sambo karaengNo ratings yet

- Household Composition StatisticsDocument6 pagesHousehold Composition StatisticseferrerascidNo ratings yet

- The Financial Crisis in Greece and Its Impacts On Western Balkan CountriesDocument13 pagesThe Financial Crisis in Greece and Its Impacts On Western Balkan CountriesPrajwal KumarNo ratings yet

- Inequality and Poverty in Greece: Myths, Realities and The CrisisDocument6 pagesInequality and Poverty in Greece: Myths, Realities and The CrisisDImiskoNo ratings yet

- Zemcik CJEF Rev01Document41 pagesZemcik CJEF Rev01Adrian MorenoNo ratings yet

- Asia-Europe: The Third Link: N 2008/04 OCTOBER 2008Document37 pagesAsia-Europe: The Third Link: N 2008/04 OCTOBER 2008BruegelNo ratings yet

- Social Report 2004 - Housing Conditions and State Assistance, 1999-2003Document22 pagesSocial Report 2004 - Housing Conditions and State Assistance, 1999-2003TARKI_ResearchNo ratings yet

- Regional Patterns of Global Economic Crisis Shocks Propagation Into Romanian EconomyDocument12 pagesRegional Patterns of Global Economic Crisis Shocks Propagation Into Romanian EconomyAlexandraDobreNo ratings yet

- Economic Performance in South- East European Transition Countries After the Fall of CommunismFrom EverandEconomic Performance in South- East European Transition Countries After the Fall of CommunismRating: 5 out of 5 stars5/5 (1)

- (Nugent, 2010) The Member StatesDocument22 pages(Nugent, 2010) The Member StatesReemNo ratings yet

- Urban-Rural Inequally in VietnamDocument25 pagesUrban-Rural Inequally in VietnamHoàng TùnNo ratings yet

- Bold Rin 2001Document48 pagesBold Rin 2001aleco_22_No ratings yet

- Ces 157Document24 pagesCes 157Minda de Gunzburg Center for European Studies at Harvard UniversityNo ratings yet

- Transformation Index BTI 2012: Regional Findings East-Central and Southeast EuropeFrom EverandTransformation Index BTI 2012: Regional Findings East-Central and Southeast EuropeNo ratings yet

- On The Relevance and Nature of Regional Inflation Differentials: The Case of SpainDocument38 pagesOn The Relevance and Nature of Regional Inflation Differentials: The Case of SpainViverNo ratings yet

- Discussion Paper Series: Some Aspects of Recent Trade Developments in South-East EuropeDocument22 pagesDiscussion Paper Series: Some Aspects of Recent Trade Developments in South-East EuropemarhelunNo ratings yet

- Nikitas Spiros Koutsoukis Spyridon Roukanas Auth. Anastasios Karasavvoglou Persefoni Polychronidou Eds. Economic Crisis in Europe and The Balkans Problems and ProsDocument245 pagesNikitas Spiros Koutsoukis Spyridon Roukanas Auth. Anastasios Karasavvoglou Persefoni Polychronidou Eds. Economic Crisis in Europe and The Balkans Problems and ProsSydneyNo ratings yet

- Regional Disparities of Unemployment in The European Union and in RomaniaDocument19 pagesRegional Disparities of Unemployment in The European Union and in RomaniaLindsey CohenNo ratings yet

- Ceswp2011 Iii2 BomDocument8 pagesCeswp2011 Iii2 BomAlexandraDobreNo ratings yet

- Discussion Paper Series: The Characteristics of Business Cycles in Selected European Emerging Market EconomiesDocument21 pagesDiscussion Paper Series: The Characteristics of Business Cycles in Selected European Emerging Market EconomiesmarhelunNo ratings yet

- European Structural Policy s01Document7 pagesEuropean Structural Policy s01jasminnexNo ratings yet

- Eu Agricultural Funds Web 220221Document84 pagesEu Agricultural Funds Web 220221Firuzeh AskerNo ratings yet

- Demographic OutlookDocument40 pagesDemographic OutlookAnca RaduNo ratings yet

- Content ServerDocument22 pagesContent Serverxxasesino64xxNo ratings yet

- Welfare State Reform in Continental and Southern Europe: An Overview of Challenges and StrategiesDocument25 pagesWelfare State Reform in Continental and Southern Europe: An Overview of Challenges and StrategiesPeter WhitefordNo ratings yet

- Capital Leakage From Owner-Occupied Housing: Jim Kemeny and Andrew ThomasDocument18 pagesCapital Leakage From Owner-Occupied Housing: Jim Kemeny and Andrew ThomasgioanelaNo ratings yet

- F10 5-2 PDFDocument1 pageF10 5-2 PDFgioanelaNo ratings yet

- Political Science Faculty Win 2 Major CSU AwardsDocument6 pagesPolitical Science Faculty Win 2 Major CSU AwardsgioanelaNo ratings yet

- 2020.4 Coronavirus Crisis Underlines Weak Spots in U.S. Economic System - The New York TimesDocument3 pages2020.4 Coronavirus Crisis Underlines Weak Spots in U.S. Economic System - The New York TimesgioanelaNo ratings yet

- Post Industrial Housing Crisis-A Comment On Anneli Juntto: Scandinavian Housing and Planning ResearchDocument2 pagesPost Industrial Housing Crisis-A Comment On Anneli Juntto: Scandinavian Housing and Planning ResearchgioanelaNo ratings yet

- A Qualitative Examination of Jim Kemeny's Arguments On High Home Ownership, The Retirement Pension and The Dualist Rental System Focusing On AustraliaDocument23 pagesA Qualitative Examination of Jim Kemeny's Arguments On High Home Ownership, The Retirement Pension and The Dualist Rental System Focusing On AustraliagioanelaNo ratings yet

- Editorial: Scandinavian Housing and Planning ResearchDocument2 pagesEditorial: Scandinavian Housing and Planning ResearchgioanelaNo ratings yet

- The Significance of Swedish Rental Policy: Cost Renting: Command Economy Versus The Social Market in Comparative PerspectiveDocument14 pagesThe Significance of Swedish Rental Policy: Cost Renting: Command Economy Versus The Social Market in Comparative PerspectivegioanelaNo ratings yet

- Plagiarism in The Japanese Universities: Truly A Cultural Matter?Document13 pagesPlagiarism in The Japanese Universities: Truly A Cultural Matter?gioanelaNo ratings yet

- Figure 1.1. The Distribution of World Output 1700-2012: Asia AfricaDocument1 pageFigure 1.1. The Distribution of World Output 1700-2012: Asia AfricagioanelaNo ratings yet

- Renewable and Sustainable Energy ReviewsDocument15 pagesRenewable and Sustainable Energy ReviewsgioanelaNo ratings yet

- Paper Prompt FAll2019Document2 pagesPaper Prompt FAll2019gioanelaNo ratings yet

- F10 10 PDFDocument1 pageF10 10 PDFgioanelaNo ratings yet

- Figure I.2. The Capital/income Ratio in Europe, 1870-2010: Germany France United KingdomDocument1 pageFigure I.2. The Capital/income Ratio in Europe, 1870-2010: Germany France United KingdomgioanelaNo ratings yet

- Geopolitics Regime Type and The Internat PDFDocument22 pagesGeopolitics Regime Type and The Internat PDFgioanelaNo ratings yet

- F10 5-2 PDFDocument1 pageF10 5-2 PDFgioanelaNo ratings yet

- Sumer Travel 2020 FlightsDocument2 pagesSumer Travel 2020 FlightsgioanelaNo ratings yet

- F10 5 PDFDocument1 pageF10 5 PDFgioanelaNo ratings yet

- F1 1 PDFDocument1 pageF1 1 PDFgioanelaNo ratings yet

- Term Paper GuidelinesDocument5 pagesTerm Paper GuidelinesgioanelaNo ratings yet

- F10 10 PDFDocument1 pageF10 10 PDFgioanelaNo ratings yet

- 2020.4 Coronavirus Stimulus Package F.A.Q. - Checks, Unemployment, Layoffs and More - The New York TimesDocument12 pages2020.4 Coronavirus Stimulus Package F.A.Q. - Checks, Unemployment, Layoffs and More - The New York TimesgioanelaNo ratings yet

- UC Berkeley Mail - Call For Papers: (Post) Socialism As A Global ResourceDocument2 pagesUC Berkeley Mail - Call For Papers: (Post) Socialism As A Global ResourcegioanelaNo ratings yet

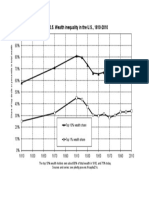

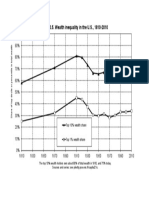

- Figure 10.5. Wealth Inequality in The U.S., 1810-2010Document1 pageFigure 10.5. Wealth Inequality in The U.S., 1810-2010gioanelaNo ratings yet

- Dan BadulescuDocument2 pagesDan BadulescugioanelaNo ratings yet

- Welcome To The Purdue OWL: On ParagraphsDocument5 pagesWelcome To The Purdue OWL: On ParagraphsgioanelaNo ratings yet

- CH3 Handbook-for-writers-6th-Canadian-Edition-Troyka-Hesse PDFDocument24 pagesCH3 Handbook-for-writers-6th-Canadian-Edition-Troyka-Hesse PDFgioanelaNo ratings yet

- p55 PDFDocument1 pagep55 PDFpenelopegerhardNo ratings yet

- 2009 Annual Report - NSCBDocument54 pages2009 Annual Report - NSCBgracegganaNo ratings yet

- SponsorshipDocument20 pagesSponsorshipSentot NindyantonoNo ratings yet

- Keys To Effective Capex ManagementDocument4 pagesKeys To Effective Capex ManagementsscalNo ratings yet

- Enc K Corporate Risk Register PDFDocument7 pagesEnc K Corporate Risk Register PDFrioNo ratings yet

- Calm Financial Planning Unit Project RubricDocument1 pageCalm Financial Planning Unit Project Rubricapi-404247454No ratings yet

- Meaning, Definition and Principles of BudgetDocument12 pagesMeaning, Definition and Principles of BudgetAngeii Campano100% (2)

- Gemoknyer Soalan..Document6 pagesGemoknyer Soalan..Nurulizwa Bte Abdul RashidNo ratings yet

- EDU31E5Y - Project Billing OverviewDocument66 pagesEDU31E5Y - Project Billing Overviewosmaaziz44100% (1)

- Define Governmental Accounting? and According To Egyptian Law?Document9 pagesDefine Governmental Accounting? and According To Egyptian Law?Mega Pop LockerNo ratings yet

- Cost Control1Document4 pagesCost Control1AF.RISHARD FAISNo ratings yet

- Demanda Junta de Control Fiscal (Deuda/Crisis Del País) Contra UBS/ Santander Securities/Ramirez Co. UNDERWRITERS (Incl. Emisión Bonos de Retiro)Document170 pagesDemanda Junta de Control Fiscal (Deuda/Crisis Del País) Contra UBS/ Santander Securities/Ramirez Co. UNDERWRITERS (Incl. Emisión Bonos de Retiro)Emily RamosNo ratings yet

- Chapter 20 - AnswerDocument15 pagesChapter 20 - AnswerAgentSkySky100% (1)

- Puplic Policy AnalysisDocument15 pagesPuplic Policy AnalysisFahad Mubin100% (1)

- Complete Economics Notes For RRB NTPC, Group-D & SSCDocument77 pagesComplete Economics Notes For RRB NTPC, Group-D & SSCACHYUT AGRAWALNo ratings yet

- SSD 2013 Procedure ReportDocument847 pagesSSD 2013 Procedure ReportJulian A.No ratings yet

- F5 QuestionsDocument10 pagesF5 QuestionsDeanNo ratings yet

- Macroeconomics Assignment 2Document4 pagesMacroeconomics Assignment 2reddygaru1No ratings yet

- Public Debt ManagementDocument12 pagesPublic Debt ManagementKenneth Delos SantosNo ratings yet

- Answer - Capital BudgetingDocument19 pagesAnswer - Capital Budgetingchowchow123No ratings yet

- SPI & CPI For Projects PDFDocument4 pagesSPI & CPI For Projects PDFJose R C FernandesNo ratings yet

- Sangguniang Kabataan of Barangay Calzadang Bayu Municipality of Porac Province of PampangaDocument21 pagesSangguniang Kabataan of Barangay Calzadang Bayu Municipality of Porac Province of PampangaMSWD PORACNo ratings yet

- Date Prepared:: Sub - Total Total of IDocument26 pagesDate Prepared:: Sub - Total Total of IangieNo ratings yet

- How To Budget Your Money WiselyDocument2 pagesHow To Budget Your Money WiselyBrando Neil SarciaNo ratings yet

- FINS3625 Case Study Report Davy Edit 1Document15 pagesFINS3625 Case Study Report Davy Edit 1DavyZhouNo ratings yet