Download as pdf or txt

You might also like

- ACC 211 Financial Accounting 1-Ekiti AdealuDocument63 pagesACC 211 Financial Accounting 1-Ekiti AdealuShehu100% (1)

- Summary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownFrom EverandSummary of William H. Pike & Patrick C. Gregory's Why Stocks Go Up and DownNo ratings yet

- Dissolution of PartnershipDocument20 pagesDissolution of PartnershipChandrasekaran Iyer100% (4)

- Acca Paper 1.2Document25 pagesAcca Paper 1.2anon-280248No ratings yet

- Checklist ProformaDocument4 pagesChecklist ProformasandipgargNo ratings yet

- Chapter 4: Joint Venture: Rohit AgarwalDocument4 pagesChapter 4: Joint Venture: Rohit Agarwalbcom100% (2)

- Joint VenturesDocument6 pagesJoint VenturesAnimeshSahaNo ratings yet

- Joint Venture AccountsDocument125 pagesJoint Venture AccountsShoukat HaralNo ratings yet

- Unit 3 Accting For Joint VenturesDocument10 pagesUnit 3 Accting For Joint VenturesAyana Giragn AÿøNo ratings yet

- Joint Ventures 2nd Sem BcomDocument6 pagesJoint Ventures 2nd Sem Bcomsubashrao5522No ratings yet

- Joint VentureDocument17 pagesJoint VentureNIKHIL KumarNo ratings yet

- Joint VentureDocument7 pagesJoint VentureCoolNo ratings yet

- DownloadDocument8 pagesDownloadMithilesh KumarNo ratings yet

- 16777joint VentureDocument63 pages16777joint VentureDevanshu JulkaNo ratings yet

- Chapter 4 Joint Venture2Document4 pagesChapter 4 Joint Venture2subba1995333333No ratings yet

- Chapter 5 Chapter 5.dissolution of Partnership-1599071962652Document8 pagesChapter 5 Chapter 5.dissolution of Partnership-1599071962652gyannibaba2007No ratings yet

- Joint Venture AccountsDocument5 pagesJoint Venture AccountsSanzida Rahman AshaNo ratings yet

- Advance Chapter 1Document16 pagesAdvance Chapter 1abel habtamuNo ratings yet

- 28901cpt Fa SM Cp7 Part2Document0 pages28901cpt Fa SM Cp7 Part2Vikas ZurmureNo ratings yet

- Unit - I - Corporate Accounting Ii - Sba1401: School of Management StudiesDocument99 pagesUnit - I - Corporate Accounting Ii - Sba1401: School of Management StudiesPalani Udhayakumar100% (1)

- Sbaa 1401Document126 pagesSbaa 1401gayuammu1135No ratings yet

- Joint VentureDocument17 pagesJoint VentureShailesh PrajapatiNo ratings yet

- Chapter 5 Dissolution of PartnershipDocument4 pagesChapter 5 Dissolution of PartnershipKalidas ChembariNo ratings yet

- Accounting For Joint VentureDocument44 pagesAccounting For Joint VentureRam KumarNo ratings yet

- JointventureDocument2 pagesJointventuremmuneebsdaNo ratings yet

- Amalgamation of Companies: Sushil KumarDocument49 pagesAmalgamation of Companies: Sushil KumarSundaramNo ratings yet

- 12 Accountancy Notes CH06 Dissolution of Partnership 01Document14 pages12 Accountancy Notes CH06 Dissolution of Partnership 01hazeleydenhereNo ratings yet

- Joint Venture Accounts: 1. MeaningDocument22 pagesJoint Venture Accounts: 1. Meaningkuldeep_chand10No ratings yet

- Joint VentureDocument37 pagesJoint VentureKHUSHI MEHTANo ratings yet

- Adfa I & II Module NewDocument36 pagesAdfa I & II Module NewEyob EyobaNo ratings yet

- 15 Joint VentureDocument11 pages15 Joint VentureJanani PriyaNo ratings yet

- Unit 13 Joint Venture Accounts: 13.0 ObjectivesDocument22 pagesUnit 13 Joint Venture Accounts: 13.0 ObjectivesChandreshNo ratings yet

- Joint VentureDocument7 pagesJoint VentureUzair SaeedNo ratings yet

- Dissolution of Partnership FirmDocument6 pagesDissolution of Partnership Firmbbv44443No ratings yet

- Chapter 4 Partnership Liquidation 2021 v2.0Document56 pagesChapter 4 Partnership Liquidation 2021 v2.0Aj ZNo ratings yet

- Debentures: Fundamentals of AccountingDocument63 pagesDebentures: Fundamentals of AccountingSangam NeupaneNo ratings yet

- CH - 04 Dissolution of Partnership FirmDocument10 pagesCH - 04 Dissolution of Partnership FirmMahathi AmudhanNo ratings yet

- Amalgam TionDocument24 pagesAmalgam Tionyogitabhootra99No ratings yet

- Amalgamation of Firms FADocument44 pagesAmalgamation of Firms FAGayatri VaityNo ratings yet

- Dissolution of Firm Notes +2Document9 pagesDissolution of Firm Notes +2Arsifatpreet kaurNo ratings yet

- Chapter OneDocument8 pagesChapter Onetasfa zNo ratings yet

- C1 Group Account SDocument15 pagesC1 Group Account S郑妙卿No ratings yet

- M1 - Partnership FormationDocument11 pagesM1 - Partnership FormationJhay MenesesNo ratings yet

- ACC 311 PartnershipDocument34 pagesACC 311 PartnershipokeowoNo ratings yet

- Notes To Diss 12Document3 pagesNotes To Diss 12Kartikay UpadhyayNo ratings yet

- AmalgamationDocument10 pagesAmalgamationSatya_kanha100% (1)

- Financial Accounting CIA - 1Document31 pagesFinancial Accounting CIA - 1shriyanshu padhiNo ratings yet

- Accounting For Joint VenturesDocument18 pagesAccounting For Joint VenturesRyan Dave AlutayaNo ratings yet

- Fdocuments - in - Adv Accounting by Ma GhaniDocument107 pagesFdocuments - in - Adv Accounting by Ma GhaniInayat Ur Rehman0% (1)

- 5 AmalgamationDocument52 pages5 AmalgamationsmartshivenduNo ratings yet

- Dissolution Revision FinalDocument9 pagesDissolution Revision FinalAnish MohantyNo ratings yet

- Dissolution of FirmDocument16 pagesDissolution of FirmPrathamNo ratings yet

- Chapter 9-2Document25 pagesChapter 9-2runescapealt452No ratings yet

- Issue of DebenturesDocument39 pagesIssue of Debenturesyashwanth86No ratings yet

- Chapter-5 Dissolution of Partnership FirmDocument8 pagesChapter-5 Dissolution of Partnership FirmManu BabuNo ratings yet

- Dissolution of A Partnership FirmDocument14 pagesDissolution of A Partnership Firmrose rose100% (1)

- 3 PartnershipDocument49 pages3 PartnershipKrrish KelwaniNo ratings yet

- General de Jesus CollegeDocument16 pagesGeneral de Jesus CollegeErwin Labayog MedinaNo ratings yet

- Partnership NotesDocument35 pagesPartnership Notesa86476007No ratings yet

- Mediocre Non-Profit OrganizationDocument12 pagesMediocre Non-Profit OrganizationveenaNo ratings yet

- Dividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementFrom EverandDividend Growth Investing: A Step-by-Step Guide to Building a Dividend Portfolio for Early RetirementNo ratings yet

- Business Organizations: Outlines and Case Summaries: Law School Survival Guides, #10From EverandBusiness Organizations: Outlines and Case Summaries: Law School Survival Guides, #10No ratings yet

- Audit Report: Ca Kanika KhetanDocument14 pagesAudit Report: Ca Kanika KhetanChandreshNo ratings yet

- Ipcc Acc 28 Sep 2015 PDFDocument16 pagesIpcc Acc 28 Sep 2015 PDFChandreshNo ratings yet

- Hsslive-Chapter 2 Theory Base of Acc 1Document5 pagesHsslive-Chapter 2 Theory Base of Acc 1ChandreshNo ratings yet

- AccountancyDocument40 pagesAccountancydher1234No ratings yet

- Accounting For Non-Profit Organization: Presenting by Mohammed Nasih B.MDocument8 pagesAccounting For Non-Profit Organization: Presenting by Mohammed Nasih B.MChandreshNo ratings yet

- Hsslive Xii Ch1 Accouting For Nop Organisation SignedDocument4 pagesHsslive Xii Ch1 Accouting For Nop Organisation SignedChandreshNo ratings yet

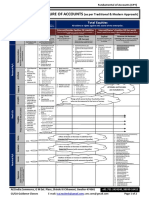

- 36 Nature of Accounts As Per Traditional Modern ApproachDocument2 pages36 Nature of Accounts As Per Traditional Modern ApproachChandresh100% (1)

- Retirement and Death of A PartnerDocument25 pagesRetirement and Death of A PartnerChandreshNo ratings yet

- BrochureDocument2 pagesBrochureChandreshNo ratings yet

- Hsslive XII Accountancy Ch1 Not For Profit OrganizationDocument4 pagesHsslive XII Accountancy Ch1 Not For Profit OrganizationChandreshNo ratings yet

- Declaration and Payment of DividendDocument5 pagesDeclaration and Payment of DividendChandreshNo ratings yet

- Hsslive-Chapter 12 Not For Profit OrganisationsDocument7 pagesHsslive-Chapter 12 Not For Profit OrganisationsChandreshNo ratings yet

- Accountancy Ebook - Class 12 - Part 1 PDFDocument130 pagesAccountancy Ebook - Class 12 - Part 1 PDFChandreshNo ratings yet

- Forex 1 PDFDocument3 pagesForex 1 PDFChandreshNo ratings yet

- As-1 and As-2 Summary NotesDocument7 pagesAs-1 and As-2 Summary NotesChandreshNo ratings yet

- CA IPC Capital Budgeting Most Important Questions 1TR8KKBFDocument12 pagesCA IPC Capital Budgeting Most Important Questions 1TR8KKBFChandreshNo ratings yet

- Unit 13 Joint Venture Accounts: 13.0 ObjectivesDocument22 pagesUnit 13 Joint Venture Accounts: 13.0 ObjectivesChandreshNo ratings yet

- Marathon Batch Final With Cover and Index PDFDocument106 pagesMarathon Batch Final With Cover and Index PDFChandreshNo ratings yet

- As Quick PDFDocument23 pagesAs Quick PDFChandreshNo ratings yet

- CA IPCC Costing & FM Quick Revision NotesDocument21 pagesCA IPCC Costing & FM Quick Revision NotesChandreshNo ratings yet

- Overview of DPWH (Andor V. Santiago)Document47 pagesOverview of DPWH (Andor V. Santiago)Bhenjhan AbbilaniNo ratings yet

- Fundamentals of Assurance EngagementsDocument10 pagesFundamentals of Assurance EngagementsBryan Red AngaraNo ratings yet

- Jurnal Internasional Seminar AuditDocument13 pagesJurnal Internasional Seminar AuditekaNo ratings yet

- Spring 2023 - ACC311 - 1Document3 pagesSpring 2023 - ACC311 - 1Tatton JodyNo ratings yet

- Environmental AuditingDocument7 pagesEnvironmental AuditingMoriel PradoNo ratings yet

- MODULE 3 - The Adjusting ProcessDocument41 pagesMODULE 3 - The Adjusting ProcessFRANCES JEANALLEN DE JESUSNo ratings yet

- Final Chapter 2 Revised 2015Document92 pagesFinal Chapter 2 Revised 2015Nearchos A. IoannouNo ratings yet

- Model ITT Marine ConstructionDocument62 pagesModel ITT Marine ConstructionRio HandokoNo ratings yet

- Human Resource ManagerDocument7 pagesHuman Resource ManagerAsif KureishiNo ratings yet

- AC403 - ADVANCED AUDITING 1 Course Outline 2Document5 pagesAC403 - ADVANCED AUDITING 1 Course Outline 2Tay?No ratings yet

- Afm 5Document2 pagesAfm 5helpevery7No ratings yet

- Gmail - Hall Ticket For Associate Account Manager, Collabera Technologies Private LimiDocument2 pagesGmail - Hall Ticket For Associate Account Manager, Collabera Technologies Private LimiKaran GillNo ratings yet

- USPS OIG Audit Report - Overtime UsageDocument16 pagesUSPS OIG Audit Report - Overtime UsagebsheehanNo ratings yet

- Acctg 17nd-Final Exam BDocument14 pagesAcctg 17nd-Final Exam BKristinelle AragoNo ratings yet

- Chapter-2 Rectification of ErrorDocument8 pagesChapter-2 Rectification of ErrorprascribdNo ratings yet

- Cost and Management Accounting: GivenDocument5 pagesCost and Management Accounting: GivenDawood Rauf BataviaNo ratings yet

- Audit in CIS Environment Quiz 3Document3 pagesAudit in CIS Environment Quiz 3ctcasipleNo ratings yet

- Asunto BSA-VeronicaDocument4 pagesAsunto BSA-Veronicakawaii yoonaNo ratings yet

- Pittsfield Pavement Management ReportDocument31 pagesPittsfield Pavement Management ReportiBerkshires.comNo ratings yet

- 4.2 Risk Treatment ProcessDocument4 pages4.2 Risk Treatment ProcessRizky Hardiana de Toulouse-LautrecNo ratings yet

- Chapter 3 Question BankDocument26 pagesChapter 3 Question Bankمحمود احمدNo ratings yet

- Audit of Cash BalancesDocument33 pagesAudit of Cash BalancesLouis ValentinoNo ratings yet

- Rural Banking in IndiaDocument45 pagesRural Banking in IndiaHarshit KatyalNo ratings yet

- New Starter FormDocument1 pageNew Starter FormRanjith GowdaNo ratings yet

- Invoice Termin Ke - IIDocument1 pageInvoice Termin Ke - IIurface998No ratings yet

- Summary ch.4 Fred R. DavidDocument8 pagesSummary ch.4 Fred R. DavidAli AtherNo ratings yet

- Sop 0025Document7 pagesSop 0025samirneseemNo ratings yet

- 112 20160617144828Document81 pages112 20160617144828Tauheed SattarNo ratings yet