Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5825)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- Human Biology 16th Mader Test Bank PDFDocument28 pagesHuman Biology 16th Mader Test Bank PDFkuldeep saini100% (1)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- MIS Case StudiesDocument6 pagesMIS Case Studiesabhi1809198950% (2)

- The Australian Floating Hotel Project - A Retrospective AnalysisDocument16 pagesThe Australian Floating Hotel Project - A Retrospective Analysisnizzu_shaikhNo ratings yet

- Study 2Document33 pagesStudy 2nizzu_shaikhNo ratings yet

- Environmental Impact Assessment: of Forestry ProjectsDocument12 pagesEnvironmental Impact Assessment: of Forestry Projectsnizzu_shaikhNo ratings yet

- Infosys Financial Analysis: Nizamuddin Shaikh Pritesh ShahDocument10 pagesInfosys Financial Analysis: Nizamuddin Shaikh Pritesh Shahnizzu_shaikhNo ratings yet

- PE Firm To Acquire Optimal Blue, Names Scott Happ CEODocument2 pagesPE Firm To Acquire Optimal Blue, Names Scott Happ CEOJacob PassyNo ratings yet

- Customer Satisfaction and Employee InvolvementDocument36 pagesCustomer Satisfaction and Employee InvolvementMaria Rebecca Toledo SalarNo ratings yet

- LAS 1A The Magic PomegranateDocument2 pagesLAS 1A The Magic PomegranateCherry Maravilla Basa MingoaNo ratings yet

- Important Battles of IslamDocument3 pagesImportant Battles of IslamAneesUrRehman100% (1)

- LC320EM9 Service EmersonDocument61 pagesLC320EM9 Service EmersonDamon BrungerNo ratings yet

- SCI 8008SEF Medical Microbiology & Virology II - Lecture 10 - OLEDocument70 pagesSCI 8008SEF Medical Microbiology & Virology II - Lecture 10 - OLEYY CheungNo ratings yet

- Ub 92Document60 pagesUb 92Mohamed AbrarNo ratings yet

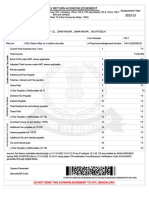

- Itr 22-23 PDFDocument1 pageItr 22-23 PDFPixel computerNo ratings yet

- Language PoliticsDocument20 pagesLanguage PoliticsAkshatNo ratings yet

- C Record CORRECTEDDocument40 pagesC Record CORRECTEDMR KishoreNo ratings yet

- Wildenradt ThesisDocument59 pagesWildenradt ThesisMuhammad jawadNo ratings yet

- ME PED-Scheme & Syllabus 2018Document21 pagesME PED-Scheme & Syllabus 2018Angamuthu AnanthNo ratings yet

- Stanford - Discrete Time Markov Chains PDFDocument23 pagesStanford - Discrete Time Markov Chains PDFSofoklisNo ratings yet

- Tesira Ex-Logic Manual Sep12-1Document10 pagesTesira Ex-Logic Manual Sep12-1Rachmat Guntur Dwi PutraNo ratings yet

- Service Sheet - Mercedes Benz W211Document8 pagesService Sheet - Mercedes Benz W211Pedro ViegasNo ratings yet

- Neonatal Ventilation: Edward G. ShepherdDocument43 pagesNeonatal Ventilation: Edward G. ShepherdIBRAHIM100% (1)

- PDF Data Science and Machine Learning Mathematical and Statistical Methods Chapman Hall CRC Machine Learning Pattern Recognition 1St Edition Dirk P Kroese Ebook Full ChapterDocument54 pagesPDF Data Science and Machine Learning Mathematical and Statistical Methods Chapman Hall CRC Machine Learning Pattern Recognition 1St Edition Dirk P Kroese Ebook Full Chaptercatherine.cottingham887100% (5)

- Engels As Interpreter of Marx's EconomicsDocument37 pagesEngels As Interpreter of Marx's EconomicsJuan HermidasNo ratings yet

- SKYPAD Pocket Firmware Instructions PDFDocument3 pagesSKYPAD Pocket Firmware Instructions PDFAbelito FloresNo ratings yet

- ASUS RT-AC58U ManualDocument122 pagesASUS RT-AC58U ManualSeungpyo HongNo ratings yet

- Red Black TreeDocument22 pagesRed Black TreeBelLa Quiennt BeycaNo ratings yet

- Math BingoDocument6 pagesMath BingoKelly CollovaNo ratings yet

- PSM SeminarDocument33 pagesPSM SeminarSamarth JainNo ratings yet

- Labour: Employer'S Report of An Occupational DiseaseDocument4 pagesLabour: Employer'S Report of An Occupational DiseaseJadon TheophilusNo ratings yet

- Drainage SystemDocument48 pagesDrainage SystemArt Wadsilang100% (1)

- ICEP CSS - PMS Current Affairs - Editorial E - Magazine (April)Document158 pagesICEP CSS - PMS Current Affairs - Editorial E - Magazine (April)Hamza Minhas100% (3)

- Resume Sr. Software Test Engineer, CRIF Solution, PuneDocument4 pagesResume Sr. Software Test Engineer, CRIF Solution, PuneamanNo ratings yet

- Metriso 5000ADocument14 pagesMetriso 5000Ahellfire22000No ratings yet

- Mco 2 3 337 PDF PDFDocument4 pagesMco 2 3 337 PDF PDFhendra ardiantoNo ratings yet