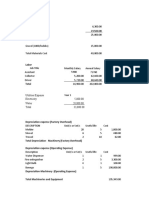

Task 1 1.sales Budget: First Quarter Sales Unit Quarterly Unit Increment Selling Price

Task 1 1.sales Budget: First Quarter Sales Unit Quarterly Unit Increment Selling Price

You might also like

- Groupe Ariel CaseDocument9 pagesGroupe Ariel CasePaco Colín86% (7)

- Math Preparedness WorkbookDocument26 pagesMath Preparedness WorkbookAnonymous czkmnf100% (2)

- Elliott Wave Cheat SheetsDocument56 pagesElliott Wave Cheat SheetsXuân Bắc100% (5)

- Vic 2019 CatalogDocument893 pagesVic 2019 CatalogAnna Mae Marantan100% (1)

- Flexible BudgetDocument3 pagesFlexible BudgetJasdeep Singh Deepu0% (2)

- Informatica FunctionsDocument46 pagesInformatica FunctionsManoj Krishna100% (1)

- Sales Budget: Q1 Q2 Q3 Q4 YearDocument23 pagesSales Budget: Q1 Q2 Q3 Q4 YearMuhamad Izuan RamliNo ratings yet

- Sales Budget Q1 Q2 Q3 Q4 Year 2021Document9 pagesSales Budget Q1 Q2 Q3 Q4 Year 2021Judith DurensNo ratings yet

- Ponderosa-IncDocument6 pagesPonderosa-IncpompomNo ratings yet

- Enterprenuer FinancialsDocument10 pagesEnterprenuer FinancialsSichen UpretyNo ratings yet

- Expected Month Cost Percent CollectionsDocument4 pagesExpected Month Cost Percent CollectionsAustin ReevuNo ratings yet

- Colin - BookDocument15 pagesColin - BookrizwanNo ratings yet

- Class Case 3 - Star Engineering CompanyDocument3 pagesClass Case 3 - Star Engineering Company9ry5gsghybNo ratings yet

- Sabit FSDocument8 pagesSabit FSMilagrosa VillasNo ratings yet

- Group 02 Aggregate Planning-1Document22 pagesGroup 02 Aggregate Planning-1Mohammad Abid MiahNo ratings yet

- TsefaDocument4 pagesTsefaAhmed SaeedNo ratings yet

- S.N. Particulars Amount (RS.) : Cost of ProjectDocument27 pagesS.N. Particulars Amount (RS.) : Cost of ProjectSuman yadavNo ratings yet

- SolutionDocument8 pagesSolutionSajakul SornNo ratings yet

- K S Oils LTD.: Unsecured LoanDocument51 pagesK S Oils LTD.: Unsecured Loanshilpatiwari1989No ratings yet

- Koreksi Fiskal KelompokDocument15 pagesKoreksi Fiskal KelompokAlfin m.r.No ratings yet

- Problem Solving AssignmentDocument13 pagesProblem Solving AssignmentRajesh MongerNo ratings yet

- Maruti Suzuki India Limited: Unsecured LoanDocument45 pagesMaruti Suzuki India Limited: Unsecured LoanMithilesh Singh0% (1)

- Spinning Project FeasibilityDocument19 pagesSpinning Project FeasibilityMaira ShahidNo ratings yet

- Exercise 1: Schedule of Expected Cash CollectionDocument7 pagesExercise 1: Schedule of Expected Cash CollectionLenard Josh IngallaNo ratings yet

- Cupcake Exports LTD.: Pre Cost Sheet-StarntalerDocument23 pagesCupcake Exports LTD.: Pre Cost Sheet-StarntalerromanNo ratings yet

- Engaging Activity B - Bruegas, Elaiza Rein A.Document2 pagesEngaging Activity B - Bruegas, Elaiza Rein A.Akawnting MaterialsNo ratings yet

- Best Financial Forecast FinalDocument13 pagesBest Financial Forecast Finalitsmethird.26No ratings yet

- Projected IncomeDocument17 pagesProjected IncomecarlomaderazoNo ratings yet

- Entrep Financial Template ComputationDocument35 pagesEntrep Financial Template ComputationJo MalaluanNo ratings yet

- FAMA '22 SolutionDocument4 pagesFAMA '22 SolutionRushil JoshiNo ratings yet

- Final CMAC (SOL) Midterm Q.Paper Aut-23Document4 pagesFinal CMAC (SOL) Midterm Q.Paper Aut-23Anmoul ZahraNo ratings yet

- Pm-Section D - BudgetingDocument43 pagesPm-Section D - BudgetingAlbee Koh Jia YeeNo ratings yet

- 278.47 Cost X Rate X DeprecmonthsDocument3 pages278.47 Cost X Rate X DeprecmonthslowienerNo ratings yet

- Plywood Project Report by Yogesh AgrawalDocument22 pagesPlywood Project Report by Yogesh AgrawalYOGESH AGRAWALNo ratings yet

- P23-1A 1. Sale Budget Quarter 1 2 TotalDocument7 pagesP23-1A 1. Sale Budget Quarter 1 2 TotalVõ Huỳnh BăngNo ratings yet

- Enterprenuership Project For Garments Sticthing Unit Financail Section - Xls 2012, 13Document20 pagesEnterprenuership Project For Garments Sticthing Unit Financail Section - Xls 2012, 13KabeerMalikNo ratings yet

- Musanity Financial StatementsDocument20 pagesMusanity Financial StatementsRenelyn DavidNo ratings yet

- Assignment Day 2Document5 pagesAssignment Day 2Indahna SulfaNo ratings yet

- Forecast Ets ExampleDocument12 pagesForecast Ets ExampleAbhinav PrakashNo ratings yet

- ABC Practice Problems Answer KeyDocument10 pagesABC Practice Problems Answer KeyKemberly AribanNo ratings yet

- Template 05 Financial ProjectionsDocument21 pagesTemplate 05 Financial Projectionsokymk13No ratings yet

- Cash 5,000 Accounts Receivable 1,500 Raw Materials Inventory 258 Finished Goods Inventory 1,462Document17 pagesCash 5,000 Accounts Receivable 1,500 Raw Materials Inventory 258 Finished Goods Inventory 1,462Nhu Le ThaoNo ratings yet

- Jessy CorporationDocument18 pagesJessy CorporationShovon MustaryNo ratings yet

- 5 Year Financial PlanDocument30 pages5 Year Financial Planrainesiusdohling.iitrNo ratings yet

- Jawaban ABCDocument25 pagesJawaban ABCNabella Roma DesiNo ratings yet

- AsratDocument27 pagesAsratMechal Awerka SmammoNo ratings yet

- Budget InformationDocument10 pagesBudget InformationIsabella BattiataNo ratings yet

- Cost Accounting: Allocation Basis Alpha Beta Gamma TotalDocument6 pagesCost Accounting: Allocation Basis Alpha Beta Gamma TotalShehrozSTNo ratings yet

- Assignment 1-1Document19 pagesAssignment 1-1mishal zikriaNo ratings yet

- PT Sam Putra Inti: Production CostDocument19 pagesPT Sam Putra Inti: Production CostIkhsan Al IzyraNo ratings yet

- Total Project CostDocument17 pagesTotal Project Costfrescy mosterNo ratings yet

- Monthly Vol Aht (Mins) Workload (HRS) Occupancy Fte Hours Per MonthDocument3 pagesMonthly Vol Aht (Mins) Workload (HRS) Occupancy Fte Hours Per MonthMohitNo ratings yet

- 2015 - Regular - Solved PaperDocument7 pages2015 - Regular - Solved PaperHassan AliNo ratings yet

- Ariel - ICFDocument9 pagesAriel - ICFSannya DuggalNo ratings yet

- NRG AUTO LIMITED-5-Year-Financial-PlanDocument21 pagesNRG AUTO LIMITED-5-Year-Financial-Plandariaivanov25No ratings yet

- Convention CentreDocument21 pagesConvention CentrerootofsoulNo ratings yet

- P1 Solution Dec 2018Document6 pagesP1 Solution Dec 2018Awal ShekNo ratings yet

- 5 Year Financial PlanDocument29 pages5 Year Financial PlanFrankieNo ratings yet

- Group Assignment Business Valuation and AnalysisDocument8 pagesGroup Assignment Business Valuation and Analysischarlesmicky82No ratings yet

- Business FinanceDocument35 pagesBusiness FinanceAliyah Belleza MusaNo ratings yet

- Joint Product and by Products Solution To Quiz 11Document3 pagesJoint Product and by Products Solution To Quiz 11Belinda SantosNo ratings yet

- Capital Structure and Profitability: S&P 500 Enterprises in the Light of the 2008 Financial CrisisFrom EverandCapital Structure and Profitability: S&P 500 Enterprises in the Light of the 2008 Financial CrisisNo ratings yet

- CHAP4 - MultiplxerDocument6 pagesCHAP4 - MultiplxerumarNo ratings yet

- Summary of Chapter 3 - Multiplexing MultiplexingDocument3 pagesSummary of Chapter 3 - Multiplexing MultiplexingumarNo ratings yet

- EMT 8.1 Biot Savart Law 2014Document25 pagesEMT 8.1 Biot Savart Law 2014umarNo ratings yet

- Test 2 2017-2018-Skee3133 PDFDocument3 pagesTest 2 2017-2018-Skee3133 PDFumarNo ratings yet

- Smart Robot HealthcareDocument9 pagesSmart Robot HealthcareumarNo ratings yet

- Chapter 5 Part 2 Bode PlotDocument45 pagesChapter 5 Part 2 Bode PlotumarNo ratings yet

- Chapter 7 Discrete Time SignalDocument19 pagesChapter 7 Discrete Time SignalumarNo ratings yet

- Final 1314.PDF Exam UTMDocument20 pagesFinal 1314.PDF Exam UTMumarNo ratings yet

- Reading Comprehension (30 Marks) Instruction: Read The Text BelowDocument8 pagesReading Comprehension (30 Marks) Instruction: Read The Text BelowumarNo ratings yet

- CookieConsumer:Tracking Online Behavioural Advertising in AustraliaDocument36 pagesCookieConsumer:Tracking Online Behavioural Advertising in AustraliaumarNo ratings yet

- Underage Access To Online Alcohol Marketing Content: A Youtube Case StudyDocument6 pagesUnderage Access To Online Alcohol Marketing Content: A Youtube Case StudyumarNo ratings yet

- Differential EquationDocument2 pagesDifferential EquationumarNo ratings yet

- Material and Equipment 1) Bbraun Infusomat Space InfusionDocument2 pagesMaterial and Equipment 1) Bbraun Infusomat Space InfusionumarNo ratings yet

- Cat 772g BRDocument28 pagesCat 772g BR111No ratings yet

- Syllabus Mcom 2017Document9 pagesSyllabus Mcom 2017khalidNo ratings yet

- 131 Lesson PlansDocument3 pages131 Lesson PlansleahmnortonNo ratings yet

- Q2 Mathematics 8 - Module 6Document19 pagesQ2 Mathematics 8 - Module 6Jose Carlos FernandezNo ratings yet

- AsiDocument30 pagesAsikholifahnwNo ratings yet

- Alcuin of YorkDocument6 pagesAlcuin of YorkemeokeNo ratings yet

- The Business of Travel and TourismDocument14 pagesThe Business of Travel and TourismJasper SumalinogNo ratings yet

- Advanced View Arduino Projects List - Use Arduino For Projects-2Document53 pagesAdvanced View Arduino Projects List - Use Arduino For Projects-2Bilal AfzalNo ratings yet

- Cinefantastique v06n04 v07n01 B (1978)Document96 pagesCinefantastique v06n04 v07n01 B (1978)Phillip Lozano100% (1)

- 8.tugas Laporan Bahasa InggrisDocument13 pages8.tugas Laporan Bahasa InggrisSanjaya JrNo ratings yet

- Multiport Diffusers For Dense Discharges: Ozeair Abessi, Aff.M.ASCE and Philip J. W. Roberts, F.ASCEDocument12 pagesMultiport Diffusers For Dense Discharges: Ozeair Abessi, Aff.M.ASCE and Philip J. W. Roberts, F.ASCEjean miguel oscorima celisNo ratings yet

- Aluminium FormworkDocument14 pagesAluminium FormworkebinVettuchirayil100% (6)

- Spare Parts Catalog For Rt55 Rough Terrain Crane: December, 2013 Edition: 1Document348 pagesSpare Parts Catalog For Rt55 Rough Terrain Crane: December, 2013 Edition: 1Nay SoeNo ratings yet

- Science: Quarter 1 - Module 1: Scientific Ways of Acquiring Knowledge and Solving ProblemsDocument22 pagesScience: Quarter 1 - Module 1: Scientific Ways of Acquiring Knowledge and Solving Problemsnoahzaec100% (2)

- Hindi E XDocument19 pagesHindi E XTamboli Shaikh Muaavvir AkbarNo ratings yet

- Slide Plate ApplicationsDocument2 pagesSlide Plate ApplicationsvietrossNo ratings yet

- Matlab: 'HZ Sine Wave To 20Hz Square Wave ConversionDocument10 pagesMatlab: 'HZ Sine Wave To 20Hz Square Wave ConversionSaied Aly SalamahNo ratings yet

- Switch POE 16 Porturi - Dahua PFS4218-16ET-240-wDocument1 pageSwitch POE 16 Porturi - Dahua PFS4218-16ET-240-wVasiliuNo ratings yet

- Orthodontic Treatment in The Management of Cleft Lip and PalateDocument13 pagesOrthodontic Treatment in The Management of Cleft Lip and PalatecareNo ratings yet

- Plu Grid-No.19Document1 pagePlu Grid-No.19BrijeshgevariyaNo ratings yet

- Freedom of The Human PersonDocument7 pagesFreedom of The Human PersonThreedotsNo ratings yet

- JavaScript - Math - Random Method Example - DiraskDocument3 pagesJavaScript - Math - Random Method Example - DiraskKelve AragaoNo ratings yet

- Thesis Statement For BiodieselDocument8 pagesThesis Statement For Biodieselkualxkiig100% (2)

- 725SSM Boiler Operation and Maintenance ManualDocument30 pages725SSM Boiler Operation and Maintenance Manualmochamad umarNo ratings yet

- Petronas Technical Standards: Site Preparation and EarthworksDocument29 pagesPetronas Technical Standards: Site Preparation and EarthworksFirdausi FauziNo ratings yet

- S 2Document12 pagesS 2api-406786743No ratings yet

Download as pdf or txt

You might also like

- Groupe Ariel CaseDocument9 pagesGroupe Ariel CasePaco Colín86% (7)

- Math Preparedness WorkbookDocument26 pagesMath Preparedness WorkbookAnonymous czkmnf100% (2)

- Elliott Wave Cheat SheetsDocument56 pagesElliott Wave Cheat SheetsXuân Bắc100% (5)

- Vic 2019 CatalogDocument893 pagesVic 2019 CatalogAnna Mae Marantan100% (1)

- Flexible BudgetDocument3 pagesFlexible BudgetJasdeep Singh Deepu0% (2)

- Informatica FunctionsDocument46 pagesInformatica FunctionsManoj Krishna100% (1)

- Sales Budget: Q1 Q2 Q3 Q4 YearDocument23 pagesSales Budget: Q1 Q2 Q3 Q4 YearMuhamad Izuan RamliNo ratings yet

- Sales Budget Q1 Q2 Q3 Q4 Year 2021Document9 pagesSales Budget Q1 Q2 Q3 Q4 Year 2021Judith DurensNo ratings yet

- Ponderosa-IncDocument6 pagesPonderosa-IncpompomNo ratings yet

- Enterprenuer FinancialsDocument10 pagesEnterprenuer FinancialsSichen UpretyNo ratings yet

- Expected Month Cost Percent CollectionsDocument4 pagesExpected Month Cost Percent CollectionsAustin ReevuNo ratings yet

- Colin - BookDocument15 pagesColin - BookrizwanNo ratings yet

- Class Case 3 - Star Engineering CompanyDocument3 pagesClass Case 3 - Star Engineering Company9ry5gsghybNo ratings yet

- Sabit FSDocument8 pagesSabit FSMilagrosa VillasNo ratings yet

- Group 02 Aggregate Planning-1Document22 pagesGroup 02 Aggregate Planning-1Mohammad Abid MiahNo ratings yet

- TsefaDocument4 pagesTsefaAhmed SaeedNo ratings yet

- S.N. Particulars Amount (RS.) : Cost of ProjectDocument27 pagesS.N. Particulars Amount (RS.) : Cost of ProjectSuman yadavNo ratings yet

- SolutionDocument8 pagesSolutionSajakul SornNo ratings yet

- K S Oils LTD.: Unsecured LoanDocument51 pagesK S Oils LTD.: Unsecured Loanshilpatiwari1989No ratings yet

- Koreksi Fiskal KelompokDocument15 pagesKoreksi Fiskal KelompokAlfin m.r.No ratings yet

- Problem Solving AssignmentDocument13 pagesProblem Solving AssignmentRajesh MongerNo ratings yet

- Maruti Suzuki India Limited: Unsecured LoanDocument45 pagesMaruti Suzuki India Limited: Unsecured LoanMithilesh Singh0% (1)

- Spinning Project FeasibilityDocument19 pagesSpinning Project FeasibilityMaira ShahidNo ratings yet

- Exercise 1: Schedule of Expected Cash CollectionDocument7 pagesExercise 1: Schedule of Expected Cash CollectionLenard Josh IngallaNo ratings yet

- Cupcake Exports LTD.: Pre Cost Sheet-StarntalerDocument23 pagesCupcake Exports LTD.: Pre Cost Sheet-StarntalerromanNo ratings yet

- Engaging Activity B - Bruegas, Elaiza Rein A.Document2 pagesEngaging Activity B - Bruegas, Elaiza Rein A.Akawnting MaterialsNo ratings yet

- Best Financial Forecast FinalDocument13 pagesBest Financial Forecast Finalitsmethird.26No ratings yet

- Projected IncomeDocument17 pagesProjected IncomecarlomaderazoNo ratings yet

- Entrep Financial Template ComputationDocument35 pagesEntrep Financial Template ComputationJo MalaluanNo ratings yet

- FAMA '22 SolutionDocument4 pagesFAMA '22 SolutionRushil JoshiNo ratings yet

- Final CMAC (SOL) Midterm Q.Paper Aut-23Document4 pagesFinal CMAC (SOL) Midterm Q.Paper Aut-23Anmoul ZahraNo ratings yet

- Pm-Section D - BudgetingDocument43 pagesPm-Section D - BudgetingAlbee Koh Jia YeeNo ratings yet

- 278.47 Cost X Rate X DeprecmonthsDocument3 pages278.47 Cost X Rate X DeprecmonthslowienerNo ratings yet

- Plywood Project Report by Yogesh AgrawalDocument22 pagesPlywood Project Report by Yogesh AgrawalYOGESH AGRAWALNo ratings yet

- P23-1A 1. Sale Budget Quarter 1 2 TotalDocument7 pagesP23-1A 1. Sale Budget Quarter 1 2 TotalVõ Huỳnh BăngNo ratings yet

- Enterprenuership Project For Garments Sticthing Unit Financail Section - Xls 2012, 13Document20 pagesEnterprenuership Project For Garments Sticthing Unit Financail Section - Xls 2012, 13KabeerMalikNo ratings yet

- Musanity Financial StatementsDocument20 pagesMusanity Financial StatementsRenelyn DavidNo ratings yet

- Assignment Day 2Document5 pagesAssignment Day 2Indahna SulfaNo ratings yet

- Forecast Ets ExampleDocument12 pagesForecast Ets ExampleAbhinav PrakashNo ratings yet

- ABC Practice Problems Answer KeyDocument10 pagesABC Practice Problems Answer KeyKemberly AribanNo ratings yet

- Template 05 Financial ProjectionsDocument21 pagesTemplate 05 Financial Projectionsokymk13No ratings yet

- Cash 5,000 Accounts Receivable 1,500 Raw Materials Inventory 258 Finished Goods Inventory 1,462Document17 pagesCash 5,000 Accounts Receivable 1,500 Raw Materials Inventory 258 Finished Goods Inventory 1,462Nhu Le ThaoNo ratings yet

- Jessy CorporationDocument18 pagesJessy CorporationShovon MustaryNo ratings yet

- 5 Year Financial PlanDocument30 pages5 Year Financial Planrainesiusdohling.iitrNo ratings yet

- Jawaban ABCDocument25 pagesJawaban ABCNabella Roma DesiNo ratings yet

- AsratDocument27 pagesAsratMechal Awerka SmammoNo ratings yet

- Budget InformationDocument10 pagesBudget InformationIsabella BattiataNo ratings yet

- Cost Accounting: Allocation Basis Alpha Beta Gamma TotalDocument6 pagesCost Accounting: Allocation Basis Alpha Beta Gamma TotalShehrozSTNo ratings yet

- Assignment 1-1Document19 pagesAssignment 1-1mishal zikriaNo ratings yet

- PT Sam Putra Inti: Production CostDocument19 pagesPT Sam Putra Inti: Production CostIkhsan Al IzyraNo ratings yet

- Total Project CostDocument17 pagesTotal Project Costfrescy mosterNo ratings yet

- Monthly Vol Aht (Mins) Workload (HRS) Occupancy Fte Hours Per MonthDocument3 pagesMonthly Vol Aht (Mins) Workload (HRS) Occupancy Fte Hours Per MonthMohitNo ratings yet

- 2015 - Regular - Solved PaperDocument7 pages2015 - Regular - Solved PaperHassan AliNo ratings yet

- Ariel - ICFDocument9 pagesAriel - ICFSannya DuggalNo ratings yet

- NRG AUTO LIMITED-5-Year-Financial-PlanDocument21 pagesNRG AUTO LIMITED-5-Year-Financial-Plandariaivanov25No ratings yet

- Convention CentreDocument21 pagesConvention CentrerootofsoulNo ratings yet

- P1 Solution Dec 2018Document6 pagesP1 Solution Dec 2018Awal ShekNo ratings yet

- 5 Year Financial PlanDocument29 pages5 Year Financial PlanFrankieNo ratings yet

- Group Assignment Business Valuation and AnalysisDocument8 pagesGroup Assignment Business Valuation and Analysischarlesmicky82No ratings yet

- Business FinanceDocument35 pagesBusiness FinanceAliyah Belleza MusaNo ratings yet

- Joint Product and by Products Solution To Quiz 11Document3 pagesJoint Product and by Products Solution To Quiz 11Belinda SantosNo ratings yet

- Capital Structure and Profitability: S&P 500 Enterprises in the Light of the 2008 Financial CrisisFrom EverandCapital Structure and Profitability: S&P 500 Enterprises in the Light of the 2008 Financial CrisisNo ratings yet

- CHAP4 - MultiplxerDocument6 pagesCHAP4 - MultiplxerumarNo ratings yet

- Summary of Chapter 3 - Multiplexing MultiplexingDocument3 pagesSummary of Chapter 3 - Multiplexing MultiplexingumarNo ratings yet

- EMT 8.1 Biot Savart Law 2014Document25 pagesEMT 8.1 Biot Savart Law 2014umarNo ratings yet

- Test 2 2017-2018-Skee3133 PDFDocument3 pagesTest 2 2017-2018-Skee3133 PDFumarNo ratings yet

- Smart Robot HealthcareDocument9 pagesSmart Robot HealthcareumarNo ratings yet

- Chapter 5 Part 2 Bode PlotDocument45 pagesChapter 5 Part 2 Bode PlotumarNo ratings yet

- Chapter 7 Discrete Time SignalDocument19 pagesChapter 7 Discrete Time SignalumarNo ratings yet

- Final 1314.PDF Exam UTMDocument20 pagesFinal 1314.PDF Exam UTMumarNo ratings yet

- Reading Comprehension (30 Marks) Instruction: Read The Text BelowDocument8 pagesReading Comprehension (30 Marks) Instruction: Read The Text BelowumarNo ratings yet

- CookieConsumer:Tracking Online Behavioural Advertising in AustraliaDocument36 pagesCookieConsumer:Tracking Online Behavioural Advertising in AustraliaumarNo ratings yet

- Underage Access To Online Alcohol Marketing Content: A Youtube Case StudyDocument6 pagesUnderage Access To Online Alcohol Marketing Content: A Youtube Case StudyumarNo ratings yet

- Differential EquationDocument2 pagesDifferential EquationumarNo ratings yet

- Material and Equipment 1) Bbraun Infusomat Space InfusionDocument2 pagesMaterial and Equipment 1) Bbraun Infusomat Space InfusionumarNo ratings yet

- Cat 772g BRDocument28 pagesCat 772g BR111No ratings yet

- Syllabus Mcom 2017Document9 pagesSyllabus Mcom 2017khalidNo ratings yet

- 131 Lesson PlansDocument3 pages131 Lesson PlansleahmnortonNo ratings yet

- Q2 Mathematics 8 - Module 6Document19 pagesQ2 Mathematics 8 - Module 6Jose Carlos FernandezNo ratings yet

- AsiDocument30 pagesAsikholifahnwNo ratings yet

- Alcuin of YorkDocument6 pagesAlcuin of YorkemeokeNo ratings yet

- The Business of Travel and TourismDocument14 pagesThe Business of Travel and TourismJasper SumalinogNo ratings yet

- Advanced View Arduino Projects List - Use Arduino For Projects-2Document53 pagesAdvanced View Arduino Projects List - Use Arduino For Projects-2Bilal AfzalNo ratings yet

- Cinefantastique v06n04 v07n01 B (1978)Document96 pagesCinefantastique v06n04 v07n01 B (1978)Phillip Lozano100% (1)

- 8.tugas Laporan Bahasa InggrisDocument13 pages8.tugas Laporan Bahasa InggrisSanjaya JrNo ratings yet

- Multiport Diffusers For Dense Discharges: Ozeair Abessi, Aff.M.ASCE and Philip J. W. Roberts, F.ASCEDocument12 pagesMultiport Diffusers For Dense Discharges: Ozeair Abessi, Aff.M.ASCE and Philip J. W. Roberts, F.ASCEjean miguel oscorima celisNo ratings yet

- Aluminium FormworkDocument14 pagesAluminium FormworkebinVettuchirayil100% (6)

- Spare Parts Catalog For Rt55 Rough Terrain Crane: December, 2013 Edition: 1Document348 pagesSpare Parts Catalog For Rt55 Rough Terrain Crane: December, 2013 Edition: 1Nay SoeNo ratings yet

- Science: Quarter 1 - Module 1: Scientific Ways of Acquiring Knowledge and Solving ProblemsDocument22 pagesScience: Quarter 1 - Module 1: Scientific Ways of Acquiring Knowledge and Solving Problemsnoahzaec100% (2)

- Hindi E XDocument19 pagesHindi E XTamboli Shaikh Muaavvir AkbarNo ratings yet

- Slide Plate ApplicationsDocument2 pagesSlide Plate ApplicationsvietrossNo ratings yet

- Matlab: 'HZ Sine Wave To 20Hz Square Wave ConversionDocument10 pagesMatlab: 'HZ Sine Wave To 20Hz Square Wave ConversionSaied Aly SalamahNo ratings yet

- Switch POE 16 Porturi - Dahua PFS4218-16ET-240-wDocument1 pageSwitch POE 16 Porturi - Dahua PFS4218-16ET-240-wVasiliuNo ratings yet

- Orthodontic Treatment in The Management of Cleft Lip and PalateDocument13 pagesOrthodontic Treatment in The Management of Cleft Lip and PalatecareNo ratings yet

- Plu Grid-No.19Document1 pagePlu Grid-No.19BrijeshgevariyaNo ratings yet

- Freedom of The Human PersonDocument7 pagesFreedom of The Human PersonThreedotsNo ratings yet

- JavaScript - Math - Random Method Example - DiraskDocument3 pagesJavaScript - Math - Random Method Example - DiraskKelve AragaoNo ratings yet

- Thesis Statement For BiodieselDocument8 pagesThesis Statement For Biodieselkualxkiig100% (2)

- 725SSM Boiler Operation and Maintenance ManualDocument30 pages725SSM Boiler Operation and Maintenance Manualmochamad umarNo ratings yet

- Petronas Technical Standards: Site Preparation and EarthworksDocument29 pagesPetronas Technical Standards: Site Preparation and EarthworksFirdausi FauziNo ratings yet

- S 2Document12 pagesS 2api-406786743No ratings yet