Adoption of New and Revised Accounting Standards Basis of Preparation of The Financial Statements

Adoption of New and Revised Accounting Standards Basis of Preparation of The Financial Statements

You might also like

- HBL Bank Statement SampleDocument9 pagesHBL Bank Statement SampleEriag WguioaNo ratings yet

- IFRS Simplified: A fast and easy-to-understand overview of the new International Financial Reporting StandardsFrom EverandIFRS Simplified: A fast and easy-to-understand overview of the new International Financial Reporting StandardsRating: 4 out of 5 stars4/5 (11)

- Sabya BhaiDocument6 pagesSabya BhaiamanNo ratings yet

- Summer Training Report OnDocument49 pagesSummer Training Report OnKriti Maheshwari95% (22)

- Credit Monitoring ArrangementDocument19 pagesCredit Monitoring ArrangementRachita Tilak67% (3)

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)IT MalurNo ratings yet

- Day 1 - Communism Vs Capitalism MaterialsDocument2 pagesDay 1 - Communism Vs Capitalism MaterialsJaredNo ratings yet

- SEC Form F-100Document2 pagesSEC Form F-100Jheng Nuqui50% (2)

- Presentation On CRISILDocument14 pagesPresentation On CRISILChanchal Gulati80% (5)

- Soumik Sen 12PGDM055 Section ADocument15 pagesSoumik Sen 12PGDM055 Section ASoumik SenNo ratings yet

- Adverse Effects of NPA On The Working of Commercial BanksDocument6 pagesAdverse Effects of NPA On The Working of Commercial Banksjatt_tinka_3760No ratings yet

- Commercial Bank ManagementDocument4 pagesCommercial Bank ManagementFat PandaNo ratings yet

- SecuritisationGuidelines ICRA 090512Document4 pagesSecuritisationGuidelines ICRA 090512Melissa Jane Rafols YuNo ratings yet

- FASB's Current Expected Credit Loss Model For Credit Loss Accounting (CECL) : Background and FAQ 'S For Bankers June 2016Document23 pagesFASB's Current Expected Credit Loss Model For Credit Loss Accounting (CECL) : Background and FAQ 'S For Bankers June 2016biswarup1988No ratings yet

- Pasaran Yang MenyusahkanDocument2 pagesPasaran Yang MenyusahkanDave NiceeNo ratings yet

- Assignment Working Capital MGMT SP 2015Document2 pagesAssignment Working Capital MGMT SP 2015JustinHallNo ratings yet

- Ifrs 9Document8 pagesIfrs 96suraz9No ratings yet

- Porter: Five Forces - Buyer Power (Low)Document7 pagesPorter: Five Forces - Buyer Power (Low)Aniruddha PatilNo ratings yet

- Measuring Commercial Bank Profitability: Proceed With CautionDocument18 pagesMeasuring Commercial Bank Profitability: Proceed With CautionShubham GuptaNo ratings yet

- BAC Stress Testing Results - FinalDocument18 pagesBAC Stress Testing Results - FinalOSRNo ratings yet

- For Example, Both Standards Measure Probability of Default (PD) at A Point in Time (RatherDocument13 pagesFor Example, Both Standards Measure Probability of Default (PD) at A Point in Time (Ratherduc anhNo ratings yet

- 2631IIBF Vision January 2013Document8 pages2631IIBF Vision January 2013Sukanta DasNo ratings yet

- Act380 Case Study Hasan Mahmuud MarufDocument5 pagesAct380 Case Study Hasan Mahmuud MarufHasan Mahmud Maruf 1621513630No ratings yet

- China Accounting StandardsDocument3 pagesChina Accounting StandardsAaron Joy Dominguez PutianNo ratings yet

- Declaration of Dividend by CooperativesDocument5 pagesDeclaration of Dividend by CooperativesManuel MoralesNo ratings yet

- Anual ReportDocument8 pagesAnual ReportjanuNo ratings yet

- 2 - Causes and Consequences of NPADocument6 pages2 - Causes and Consequences of NPAAdhiraj K. RajputNo ratings yet

- Indian Banks - CLSADocument4 pagesIndian Banks - CLSAPranjayNo ratings yet

- Us Advisory Ifrs 9 PovDocument8 pagesUs Advisory Ifrs 9 Pov2k8.bobNo ratings yet

- ASSIGNMENT 3 Seminar No 2.2 5CDocument3 pagesASSIGNMENT 3 Seminar No 2.2 5CAhmad NaqibNo ratings yet

- Non Performing AssetsDocument12 pagesNon Performing AssetsVikram SinghNo ratings yet

- Constraints::: Because This Statement Is Also Used by Banks, Shareholders, Etc., and Also As It Is TheDocument11 pagesConstraints::: Because This Statement Is Also Used by Banks, Shareholders, Etc., and Also As It Is TheamaspyNo ratings yet

- P7int 2013 Jun A PDFDocument17 pagesP7int 2013 Jun A PDFhiruspoonNo ratings yet

- CH-2 - NPAs, Its Emergence and EffectsDocument7 pagesCH-2 - NPAs, Its Emergence and EffectsNirjhar DuttaNo ratings yet

- Akbar C.MDocument6 pagesAkbar C.MSumon SumNo ratings yet

- Non Performing NpaDocument21 pagesNon Performing NpaPriya Rakeshkumar MistryNo ratings yet

- Prompt Corrective ActionDocument2 pagesPrompt Corrective ActionRatanNo ratings yet

- Topic-IDFC First Bank Results Q4FY24Document10 pagesTopic-IDFC First Bank Results Q4FY24iamrdas02No ratings yet

- Proposal For The Amendment of Murabaha Financing Profit RateDocument15 pagesProposal For The Amendment of Murabaha Financing Profit RateMohamed MustefaNo ratings yet

- Chapter1: Introduction: Nonperforming Asset in BankDocument35 pagesChapter1: Introduction: Nonperforming Asset in BankMaridasrajanNo ratings yet

- FSI Briefs: Expected Loss Provisioning Under A Global PandemicDocument9 pagesFSI Briefs: Expected Loss Provisioning Under A Global PandemicGeetika KhandelwalNo ratings yet

- Expand - Less: ScoreDocument25 pagesExpand - Less: Scoreuthanh2209No ratings yet

- Currency Gains Losses IfrsDocument8 pagesCurrency Gains Losses IfrsSatyendra KumarNo ratings yet

- Why U.S. Financial Services Investors Are Concerned That Proposed Accounting Rules Will Impede Decision MakingDocument10 pagesWhy U.S. Financial Services Investors Are Concerned That Proposed Accounting Rules Will Impede Decision Makingapi-227433089No ratings yet

- 2015-11-02 PDF JP Morgan Special Report - Proposed FRTB Ruling Endangers Securitized Products MarketsDocument10 pages2015-11-02 PDF JP Morgan Special Report - Proposed FRTB Ruling Endangers Securitized Products MarketsDivya Krishna BirthrayNo ratings yet

- Banking and Insurance Laws Project AssigmentDocument7 pagesBanking and Insurance Laws Project AssigmentmandiraNo ratings yet

- Butler Lumber Company Case Solution CasesolDocument3 pagesButler Lumber Company Case Solution CasesolTalha SiddiquiNo ratings yet

- 11-Dec 2019Document13 pages11-Dec 2019vasilikiNo ratings yet

- Financial Update Q2 FY20: Nyse: CRM @salesforce - IrDocument33 pagesFinancial Update Q2 FY20: Nyse: CRM @salesforce - IrMika DeverinNo ratings yet

- Q322 Investor PresentationDocument42 pagesQ322 Investor PresentationAlex ENo ratings yet

- Non Performing AssetsDocument24 pagesNon Performing AssetsAmarjeet DhobiNo ratings yet

- Prompt Corrective Action (Pca)Document3 pagesPrompt Corrective Action (Pca)Nikilaa ManoharanNo ratings yet

- Group 9 - BBB Audit Plan - V2-NCDocument21 pagesGroup 9 - BBB Audit Plan - V2-NCNicholas CoxNo ratings yet

- Reserve Bank of IndiaDocument57 pagesReserve Bank of IndiaAjinkya AghamkarNo ratings yet

- Geun Woo Seoh: Vol. 21, No. 15 (14 April 2012)Document13 pagesGeun Woo Seoh: Vol. 21, No. 15 (14 April 2012)Mihai PopescuNo ratings yet

- English Program: Quiz ESP319 Unit 2Document5 pagesEnglish Program: Quiz ESP319 Unit 2Camilo AndrésNo ratings yet

- RBI Guidelines Compiled From 01.01.2020 To 30.06.2020Document144 pagesRBI Guidelines Compiled From 01.01.2020 To 30.06.2020Natarajan JayaramanNo ratings yet

- 5003 Ste PaperDocument13 pages5003 Ste PaperLouise BrownNo ratings yet

- Emeka FMT CompletedDocument51 pagesEmeka FMT CompletedErhueh Kester AghoghoNo ratings yet

- IFRS 9 2019 PresentationDocument25 pagesIFRS 9 2019 PresentationTina PhilipNo ratings yet

- Reprt SoneriDocument23 pagesReprt SoneriMuqaddas IsrarNo ratings yet

- Approved: How to Get Your Business Loan Funded Faster, Cheaper, & with Less StressFrom EverandApproved: How to Get Your Business Loan Funded Faster, Cheaper, & with Less StressRating: 5 out of 5 stars5/5 (1)

- Summary of Howard M. Schilit, Jeremy Perler & Yoni Engelhart's Financial Shenanigans, Fourth EditionFrom EverandSummary of Howard M. Schilit, Jeremy Perler & Yoni Engelhart's Financial Shenanigans, Fourth EditionNo ratings yet

- Fiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesFrom EverandFiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesNo ratings yet

- Od 329808896732339100Document5 pagesOd 329808896732339100Rachna GuptaNo ratings yet

- Quick Notes PEZADocument8 pagesQuick Notes PEZAVic FabeNo ratings yet

- Assignment - Banking & InsuranceDocument4 pagesAssignment - Banking & Insurancesandeep_kadam_7No ratings yet

- Up SellingDocument3 pagesUp SellingNora GambronNo ratings yet

- AEF Gold Bills DoctrineDocument4 pagesAEF Gold Bills DoctrinebetancurNo ratings yet

- The Indian Shrimp Industry Organizes To Fight TheDocument9 pagesThe Indian Shrimp Industry Organizes To Fight TheVaibhav RakhejaNo ratings yet

- Project Report Business Development Analysis": NashikDocument60 pagesProject Report Business Development Analysis": NashikHarish BhagwatNo ratings yet

- KPO Case Study 01Document3 pagesKPO Case Study 01rameshkoutarapuNo ratings yet

- CH 02 Plant DesignDocument61 pagesCH 02 Plant DesignJoseph KinfeNo ratings yet

- Barila Spa - Ans-1 & Ans-3Document2 pagesBarila Spa - Ans-1 & Ans-3SiddharthNo ratings yet

- C C E (N) : ASH AND ASH Quivalents OtesDocument13 pagesC C E (N) : ASH AND ASH Quivalents OtesJoan LaroyaNo ratings yet

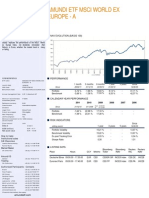

- Amundi Etf Msci World Ex Europe - A - Anglais - Eur - 3163!47!2!3!207 - MDocument2 pagesAmundi Etf Msci World Ex Europe - A - Anglais - Eur - 3163!47!2!3!207 - Mhp24714303No ratings yet

- BSIE Cost AccountingDocument5 pagesBSIE Cost AccountingJoovs JoovhoNo ratings yet

- A03Document16 pagesA03Vũ Hồng NhungNo ratings yet

- ch01R StudentDocument70 pagesch01R StudentChuan ShihNo ratings yet

- Unit 5Document22 pagesUnit 5Shivam ChandraNo ratings yet

- Fintech Payments 101 Simple ExplanationDocument9 pagesFintech Payments 101 Simple ExplanationNaheed Ghazi0% (1)

- Measurement: Impairment of LoanDocument3 pagesMeasurement: Impairment of LoanClar AgramonNo ratings yet

- Economics Chapter 2Document34 pagesEconomics Chapter 2cyndaleaNo ratings yet

- ONEASSIST InvoiceDocument1 pageONEASSIST InvoiceVinay PandeyNo ratings yet

- 4.1. Materi Leadership Journey - Pemimpin Membentuk Budaya - HLP#2Document29 pages4.1. Materi Leadership Journey - Pemimpin Membentuk Budaya - HLP#2emyNo ratings yet

- Advanced Corporate Finance 1st Edition Ogden Test BankDocument13 pagesAdvanced Corporate Finance 1st Edition Ogden Test Bankpottpotlacew8mf1t100% (17)

- Case Study Assessment 6Document2 pagesCase Study Assessment 6Christian John Resabal BiolNo ratings yet

- WHFIT Transition GuidanceDocument12 pagesWHFIT Transition GuidancejpesNo ratings yet

- Importance of Fixed Asset Management Software For HospitalsDocument7 pagesImportance of Fixed Asset Management Software For Hospitalsswapnil_nikam0% (1)

Download as docx, pdf, or txt

You might also like

- HBL Bank Statement SampleDocument9 pagesHBL Bank Statement SampleEriag WguioaNo ratings yet

- IFRS Simplified: A fast and easy-to-understand overview of the new International Financial Reporting StandardsFrom EverandIFRS Simplified: A fast and easy-to-understand overview of the new International Financial Reporting StandardsRating: 4 out of 5 stars4/5 (11)

- Sabya BhaiDocument6 pagesSabya BhaiamanNo ratings yet

- Summer Training Report OnDocument49 pagesSummer Training Report OnKriti Maheshwari95% (22)

- Credit Monitoring ArrangementDocument19 pagesCredit Monitoring ArrangementRachita Tilak67% (3)

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)IT MalurNo ratings yet

- Day 1 - Communism Vs Capitalism MaterialsDocument2 pagesDay 1 - Communism Vs Capitalism MaterialsJaredNo ratings yet

- SEC Form F-100Document2 pagesSEC Form F-100Jheng Nuqui50% (2)

- Presentation On CRISILDocument14 pagesPresentation On CRISILChanchal Gulati80% (5)

- Soumik Sen 12PGDM055 Section ADocument15 pagesSoumik Sen 12PGDM055 Section ASoumik SenNo ratings yet

- Adverse Effects of NPA On The Working of Commercial BanksDocument6 pagesAdverse Effects of NPA On The Working of Commercial Banksjatt_tinka_3760No ratings yet

- Commercial Bank ManagementDocument4 pagesCommercial Bank ManagementFat PandaNo ratings yet

- SecuritisationGuidelines ICRA 090512Document4 pagesSecuritisationGuidelines ICRA 090512Melissa Jane Rafols YuNo ratings yet

- FASB's Current Expected Credit Loss Model For Credit Loss Accounting (CECL) : Background and FAQ 'S For Bankers June 2016Document23 pagesFASB's Current Expected Credit Loss Model For Credit Loss Accounting (CECL) : Background and FAQ 'S For Bankers June 2016biswarup1988No ratings yet

- Pasaran Yang MenyusahkanDocument2 pagesPasaran Yang MenyusahkanDave NiceeNo ratings yet

- Assignment Working Capital MGMT SP 2015Document2 pagesAssignment Working Capital MGMT SP 2015JustinHallNo ratings yet

- Ifrs 9Document8 pagesIfrs 96suraz9No ratings yet

- Porter: Five Forces - Buyer Power (Low)Document7 pagesPorter: Five Forces - Buyer Power (Low)Aniruddha PatilNo ratings yet

- Measuring Commercial Bank Profitability: Proceed With CautionDocument18 pagesMeasuring Commercial Bank Profitability: Proceed With CautionShubham GuptaNo ratings yet

- BAC Stress Testing Results - FinalDocument18 pagesBAC Stress Testing Results - FinalOSRNo ratings yet

- For Example, Both Standards Measure Probability of Default (PD) at A Point in Time (RatherDocument13 pagesFor Example, Both Standards Measure Probability of Default (PD) at A Point in Time (Ratherduc anhNo ratings yet

- 2631IIBF Vision January 2013Document8 pages2631IIBF Vision January 2013Sukanta DasNo ratings yet

- Act380 Case Study Hasan Mahmuud MarufDocument5 pagesAct380 Case Study Hasan Mahmuud MarufHasan Mahmud Maruf 1621513630No ratings yet

- China Accounting StandardsDocument3 pagesChina Accounting StandardsAaron Joy Dominguez PutianNo ratings yet

- Declaration of Dividend by CooperativesDocument5 pagesDeclaration of Dividend by CooperativesManuel MoralesNo ratings yet

- Anual ReportDocument8 pagesAnual ReportjanuNo ratings yet

- 2 - Causes and Consequences of NPADocument6 pages2 - Causes and Consequences of NPAAdhiraj K. RajputNo ratings yet

- Indian Banks - CLSADocument4 pagesIndian Banks - CLSAPranjayNo ratings yet

- Us Advisory Ifrs 9 PovDocument8 pagesUs Advisory Ifrs 9 Pov2k8.bobNo ratings yet

- ASSIGNMENT 3 Seminar No 2.2 5CDocument3 pagesASSIGNMENT 3 Seminar No 2.2 5CAhmad NaqibNo ratings yet

- Non Performing AssetsDocument12 pagesNon Performing AssetsVikram SinghNo ratings yet

- Constraints::: Because This Statement Is Also Used by Banks, Shareholders, Etc., and Also As It Is TheDocument11 pagesConstraints::: Because This Statement Is Also Used by Banks, Shareholders, Etc., and Also As It Is TheamaspyNo ratings yet

- P7int 2013 Jun A PDFDocument17 pagesP7int 2013 Jun A PDFhiruspoonNo ratings yet

- CH-2 - NPAs, Its Emergence and EffectsDocument7 pagesCH-2 - NPAs, Its Emergence and EffectsNirjhar DuttaNo ratings yet

- Akbar C.MDocument6 pagesAkbar C.MSumon SumNo ratings yet

- Non Performing NpaDocument21 pagesNon Performing NpaPriya Rakeshkumar MistryNo ratings yet

- Prompt Corrective ActionDocument2 pagesPrompt Corrective ActionRatanNo ratings yet

- Topic-IDFC First Bank Results Q4FY24Document10 pagesTopic-IDFC First Bank Results Q4FY24iamrdas02No ratings yet

- Proposal For The Amendment of Murabaha Financing Profit RateDocument15 pagesProposal For The Amendment of Murabaha Financing Profit RateMohamed MustefaNo ratings yet

- Chapter1: Introduction: Nonperforming Asset in BankDocument35 pagesChapter1: Introduction: Nonperforming Asset in BankMaridasrajanNo ratings yet

- FSI Briefs: Expected Loss Provisioning Under A Global PandemicDocument9 pagesFSI Briefs: Expected Loss Provisioning Under A Global PandemicGeetika KhandelwalNo ratings yet

- Expand - Less: ScoreDocument25 pagesExpand - Less: Scoreuthanh2209No ratings yet

- Currency Gains Losses IfrsDocument8 pagesCurrency Gains Losses IfrsSatyendra KumarNo ratings yet

- Why U.S. Financial Services Investors Are Concerned That Proposed Accounting Rules Will Impede Decision MakingDocument10 pagesWhy U.S. Financial Services Investors Are Concerned That Proposed Accounting Rules Will Impede Decision Makingapi-227433089No ratings yet

- 2015-11-02 PDF JP Morgan Special Report - Proposed FRTB Ruling Endangers Securitized Products MarketsDocument10 pages2015-11-02 PDF JP Morgan Special Report - Proposed FRTB Ruling Endangers Securitized Products MarketsDivya Krishna BirthrayNo ratings yet

- Banking and Insurance Laws Project AssigmentDocument7 pagesBanking and Insurance Laws Project AssigmentmandiraNo ratings yet

- Butler Lumber Company Case Solution CasesolDocument3 pagesButler Lumber Company Case Solution CasesolTalha SiddiquiNo ratings yet

- 11-Dec 2019Document13 pages11-Dec 2019vasilikiNo ratings yet

- Financial Update Q2 FY20: Nyse: CRM @salesforce - IrDocument33 pagesFinancial Update Q2 FY20: Nyse: CRM @salesforce - IrMika DeverinNo ratings yet

- Q322 Investor PresentationDocument42 pagesQ322 Investor PresentationAlex ENo ratings yet

- Non Performing AssetsDocument24 pagesNon Performing AssetsAmarjeet DhobiNo ratings yet

- Prompt Corrective Action (Pca)Document3 pagesPrompt Corrective Action (Pca)Nikilaa ManoharanNo ratings yet

- Group 9 - BBB Audit Plan - V2-NCDocument21 pagesGroup 9 - BBB Audit Plan - V2-NCNicholas CoxNo ratings yet

- Reserve Bank of IndiaDocument57 pagesReserve Bank of IndiaAjinkya AghamkarNo ratings yet

- Geun Woo Seoh: Vol. 21, No. 15 (14 April 2012)Document13 pagesGeun Woo Seoh: Vol. 21, No. 15 (14 April 2012)Mihai PopescuNo ratings yet

- English Program: Quiz ESP319 Unit 2Document5 pagesEnglish Program: Quiz ESP319 Unit 2Camilo AndrésNo ratings yet

- RBI Guidelines Compiled From 01.01.2020 To 30.06.2020Document144 pagesRBI Guidelines Compiled From 01.01.2020 To 30.06.2020Natarajan JayaramanNo ratings yet

- 5003 Ste PaperDocument13 pages5003 Ste PaperLouise BrownNo ratings yet

- Emeka FMT CompletedDocument51 pagesEmeka FMT CompletedErhueh Kester AghoghoNo ratings yet

- IFRS 9 2019 PresentationDocument25 pagesIFRS 9 2019 PresentationTina PhilipNo ratings yet

- Reprt SoneriDocument23 pagesReprt SoneriMuqaddas IsrarNo ratings yet

- Approved: How to Get Your Business Loan Funded Faster, Cheaper, & with Less StressFrom EverandApproved: How to Get Your Business Loan Funded Faster, Cheaper, & with Less StressRating: 5 out of 5 stars5/5 (1)

- Summary of Howard M. Schilit, Jeremy Perler & Yoni Engelhart's Financial Shenanigans, Fourth EditionFrom EverandSummary of Howard M. Schilit, Jeremy Perler & Yoni Engelhart's Financial Shenanigans, Fourth EditionNo ratings yet

- Fiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesFrom EverandFiscal Decentralization Reform in Cambodia: Progress over the Past Decade and OpportunitiesNo ratings yet

- Od 329808896732339100Document5 pagesOd 329808896732339100Rachna GuptaNo ratings yet

- Quick Notes PEZADocument8 pagesQuick Notes PEZAVic FabeNo ratings yet

- Assignment - Banking & InsuranceDocument4 pagesAssignment - Banking & Insurancesandeep_kadam_7No ratings yet

- Up SellingDocument3 pagesUp SellingNora GambronNo ratings yet

- AEF Gold Bills DoctrineDocument4 pagesAEF Gold Bills DoctrinebetancurNo ratings yet

- The Indian Shrimp Industry Organizes To Fight TheDocument9 pagesThe Indian Shrimp Industry Organizes To Fight TheVaibhav RakhejaNo ratings yet

- Project Report Business Development Analysis": NashikDocument60 pagesProject Report Business Development Analysis": NashikHarish BhagwatNo ratings yet

- KPO Case Study 01Document3 pagesKPO Case Study 01rameshkoutarapuNo ratings yet

- CH 02 Plant DesignDocument61 pagesCH 02 Plant DesignJoseph KinfeNo ratings yet

- Barila Spa - Ans-1 & Ans-3Document2 pagesBarila Spa - Ans-1 & Ans-3SiddharthNo ratings yet

- C C E (N) : ASH AND ASH Quivalents OtesDocument13 pagesC C E (N) : ASH AND ASH Quivalents OtesJoan LaroyaNo ratings yet

- Amundi Etf Msci World Ex Europe - A - Anglais - Eur - 3163!47!2!3!207 - MDocument2 pagesAmundi Etf Msci World Ex Europe - A - Anglais - Eur - 3163!47!2!3!207 - Mhp24714303No ratings yet

- BSIE Cost AccountingDocument5 pagesBSIE Cost AccountingJoovs JoovhoNo ratings yet

- A03Document16 pagesA03Vũ Hồng NhungNo ratings yet

- ch01R StudentDocument70 pagesch01R StudentChuan ShihNo ratings yet

- Unit 5Document22 pagesUnit 5Shivam ChandraNo ratings yet

- Fintech Payments 101 Simple ExplanationDocument9 pagesFintech Payments 101 Simple ExplanationNaheed Ghazi0% (1)

- Measurement: Impairment of LoanDocument3 pagesMeasurement: Impairment of LoanClar AgramonNo ratings yet

- Economics Chapter 2Document34 pagesEconomics Chapter 2cyndaleaNo ratings yet

- ONEASSIST InvoiceDocument1 pageONEASSIST InvoiceVinay PandeyNo ratings yet

- 4.1. Materi Leadership Journey - Pemimpin Membentuk Budaya - HLP#2Document29 pages4.1. Materi Leadership Journey - Pemimpin Membentuk Budaya - HLP#2emyNo ratings yet

- Advanced Corporate Finance 1st Edition Ogden Test BankDocument13 pagesAdvanced Corporate Finance 1st Edition Ogden Test Bankpottpotlacew8mf1t100% (17)

- Case Study Assessment 6Document2 pagesCase Study Assessment 6Christian John Resabal BiolNo ratings yet

- WHFIT Transition GuidanceDocument12 pagesWHFIT Transition GuidancejpesNo ratings yet

- Importance of Fixed Asset Management Software For HospitalsDocument7 pagesImportance of Fixed Asset Management Software For Hospitalsswapnil_nikam0% (1)