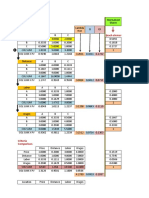

Sharpe Ratio Optimal Portfolio

Sharpe Ratio Optimal Portfolio

You might also like

- Mercedes - Benz Vito & V-Class Petrol & Diesel Models: Workshop Manual - 2000 - 2003From EverandMercedes - Benz Vito & V-Class Petrol & Diesel Models: Workshop Manual - 2000 - 2003Rating: 5 out of 5 stars5/5 (1)

- Sensitivity Analysis: Capital CostDocument4 pagesSensitivity Analysis: Capital CostZaini AhNo ratings yet

- Sharpe Ratio Optimal PortfolioDocument2 pagesSharpe Ratio Optimal PortfoliomaazwasifNo ratings yet

- Corporate Climate Risk and Bond Credit Spreads - 2024 - Finance Research Letters 4Document1 pageCorporate Climate Risk and Bond Credit Spreads - 2024 - Finance Research Letters 4JohnNo ratings yet

- Con R RSD (%) STD Average Range Max Min Replicates 5 0.752573 0.0063544 0.8443567 0.0239 0.8576 0.8337 0.8427 0.8494 0.8437 RDocument31 pagesCon R RSD (%) STD Average Range Max Min Replicates 5 0.752573 0.0063544 0.8443567 0.0239 0.8576 0.8337 0.8427 0.8494 0.8437 RMichael ThioNo ratings yet

- Kurva Kalibrasi Larutan Standar C-Organik: 1. Penentuan LinieritasDocument4 pagesKurva Kalibrasi Larutan Standar C-Organik: 1. Penentuan Linieritasaprilia kurnia putriNo ratings yet

- Heroine, Percentage: Ave 2 Ave 2 Ave 2Document3 pagesHeroine, Percentage: Ave 2 Ave 2 Ave 2Ayesha KhanNo ratings yet

- KHX3200A 1gDocument2 pagesKHX3200A 1gOvidiu VranceanuNo ratings yet

- Enter Your Data Column in A1-A90, Appraiser-Trial-PartDocument8 pagesEnter Your Data Column in A1-A90, Appraiser-Trial-PartAlejandro OlguinNo ratings yet

- Cable Sizing CalculationDocument1 pageCable Sizing Calculationmathan_aeNo ratings yet

- Bulletin #D15EDocument4 pagesBulletin #D15EPanos PanosNo ratings yet

- X Bar & R Bar SampleDocument2 pagesX Bar & R Bar SampleRaajha MunibathiranNo ratings yet

- VIFmodel 3Document2 pagesVIFmodel 3Van Joshua NunezNo ratings yet

- Number 3Document2 pagesNumber 3Mhiamar AbelladaNo ratings yet

- Branch Losses Summary Report: Etap Etap EtapDocument1 pageBranch Losses Summary Report: Etap Etap EtapJohar PradityoNo ratings yet

- Engsolutions RCB: Foundation Soil PropertiesDocument2 pagesEngsolutions RCB: Foundation Soil PropertiesReynaldo Tejada PiñerezNo ratings yet

- Expected Return Covariance Matrix: E (R) STDDocument1 pageExpected Return Covariance Matrix: E (R) STDElijah LeslieNo ratings yet

- Adams Auto-Lubrication System DesignDocument4 pagesAdams Auto-Lubrication System DesignRobin Ace SamonteNo ratings yet

- Pneumatic Control Valve Sizing GuideDocument1 pagePneumatic Control Valve Sizing GuideJOSE MARTIN MORA RIVEROSNo ratings yet

- Planilla de Cómputos MétricosDocument21 pagesPlanilla de Cómputos Métricosluis reynaldo ibarra delgadoNo ratings yet

- Verificacion de Analisis ModalDocument5 pagesVerificacion de Analisis ModalFz LlanosNo ratings yet

- Tolerance StacksDocument15 pagesTolerance StacksSanjay MehrishiNo ratings yet

- Blue Bus485 FinalDocument13 pagesBlue Bus485 FinalTamzid Ahmed AnikNo ratings yet

- Aero TrapzDocument1 pageAero TrapzHimanshu MatoNo ratings yet

- LEA20kV Ciocarlia-S2-23.03.2011Document8 pagesLEA20kV Ciocarlia-S2-23.03.2011NellyUSANo ratings yet

- Faris Zainul Arifin - BAB 4 - Konsolidasi - RevisiDocument2 pagesFaris Zainul Arifin - BAB 4 - Konsolidasi - RevisiFarisNo ratings yet

- MV Cable Technical Information - 2017Document10 pagesMV Cable Technical Information - 2017PukraDastNo ratings yet

- Censo de Carga: Estudiante: Victor Rafael Palmett ArizaDocument10 pagesCenso de Carga: Estudiante: Victor Rafael Palmett ArizaVictor PalmettNo ratings yet

- Conductor DatabaseDocument105 pagesConductor DatabaseJusTin EsteBan ArtAga HernAndezNo ratings yet

- 408 Exp 1 GraphsDocument13 pages408 Exp 1 Graphsgoabaone kgopaNo ratings yet

- MODULO 6 Analisis Sismico EstaticoDocument11 pagesMODULO 6 Analisis Sismico EstaticoLUIZ FERNANDO ALARCÓN ROJASNo ratings yet

- Two-Way Slab Check Slab Mark: Analysis CriteriaDocument8 pagesTwo-Way Slab Check Slab Mark: Analysis CriteriaAnonymous PVQdLoYnpNo ratings yet

- LinPro PrintingDocument9 pagesLinPro PrintingtresspasseeNo ratings yet

- Multiple Logistic Regression Model-LPDocument7 pagesMultiple Logistic Regression Model-LPmanjushreeNo ratings yet

- RollPower Calculator V2.2Document28 pagesRollPower Calculator V2.2Crypto FriendlyNo ratings yet

- Stab LityDocument7 pagesStab LityRenzo Gonzales EsquenNo ratings yet

- Homework No. 3..Document7 pagesHomework No. 3..Katherine PaterninaNo ratings yet

- Sementara Cdo HighDocument2 pagesSementara Cdo Highsri hastutiNo ratings yet

- NP (Conc.) (Señal) : Patrones Calibracion Informe Calibrado X y X 2 Y 2 XYDocument4 pagesNP (Conc.) (Señal) : Patrones Calibracion Informe Calibrado X y X 2 Y 2 XYLorenza MeddaNo ratings yet

- Parameters of The Model: Name Live Probabilistic Deterministic Alpha Beta DescriptionDocument6 pagesParameters of The Model: Name Live Probabilistic Deterministic Alpha Beta DescriptionAngga Prawira KautsarNo ratings yet

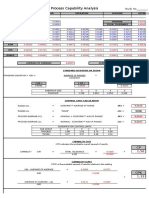

- Process Capability Analysis: Part Number Discription Operation Machine DepartmentDocument3 pagesProcess Capability Analysis: Part Number Discription Operation Machine DepartmentYATHISH BABUNo ratings yet

- MME3110 Assign Project 1617-2Document6 pagesMME3110 Assign Project 1617-2Muhammad Sollehen MisnanNo ratings yet

- Ventilation Sizing Summary For BLOCK LOAD BARKA MALLDocument2 pagesVentilation Sizing Summary For BLOCK LOAD BARKA MALLmechmohsin4745No ratings yet

- Each Element Is Devided by Column SumDocument3 pagesEach Element Is Devided by Column SumClutch And FlywheelNo ratings yet

- Each Element Is Devided by Column SumDocument3 pagesEach Element Is Devided by Column SumClutch And FlywheelNo ratings yet

- Parameters of The Model: Name Live Alpha Beta DescriptionDocument5 pagesParameters of The Model: Name Live Alpha Beta DescriptionAngga Prawira KautsarNo ratings yet

- Project BEM 92303Document12 pagesProject BEM 92303Jair BoulosNo ratings yet

- 02 w95 LRT OverallDocument100 pages02 w95 LRT OverallPRASARANA LRTJNo ratings yet

- ReinforcementDocument11 pagesReinforcementjvanandhNo ratings yet

- Conductoare Neizolate Din Al: Po (KW) PSCC (KW)Document5 pagesConductoare Neizolate Din Al: Po (KW) PSCC (KW)Ciprian ApalaghițeiNo ratings yet

- Tatt Agrotek BDocument17 pagesTatt Agrotek BJun AdityaNo ratings yet

- Check List For Design Building 1Document49 pagesCheck List For Design Building 1Prajwol ShresthaNo ratings yet

- Manual Transaxle PDFDocument53 pagesManual Transaxle PDFClaudio Godoy GallegosNo ratings yet

- Table - 68: A.C. Resistance and Reactance Values For Xlpe Insulated CablesDocument1 pageTable - 68: A.C. Resistance and Reactance Values For Xlpe Insulated CablesarshadbayaNo ratings yet

- Test Report AngulosDocument2 pagesTest Report Angulosdeportesaldia2014No ratings yet

- Certificate of Analysis: BS Number CC-17Document4 pagesCertificate of Analysis: BS Number CC-17Sidneide Ferreira SantosNo ratings yet

- Engine Lubrication & Cooling SystemsDocument15 pagesEngine Lubrication & Cooling SystemsMikiboi LugueNo ratings yet

- Process Capability Analysis: Part Number Discription Operation Machine DepartmentDocument9 pagesProcess Capability Analysis: Part Number Discription Operation Machine DepartmentdayalumeNo ratings yet

- Addressing Mixed Surfactant Systems and HLDDocument6 pagesAddressing Mixed Surfactant Systems and HLDMichael Taylor WarrenNo ratings yet

- HT Xlpe PDFDocument3 pagesHT Xlpe PDFrengaramanujanNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Mercedes - Benz Vito & V-Class Petrol & Diesel Models: Workshop Manual - 2000 - 2003From EverandMercedes - Benz Vito & V-Class Petrol & Diesel Models: Workshop Manual - 2000 - 2003Rating: 5 out of 5 stars5/5 (1)

- Sensitivity Analysis: Capital CostDocument4 pagesSensitivity Analysis: Capital CostZaini AhNo ratings yet

- Sharpe Ratio Optimal PortfolioDocument2 pagesSharpe Ratio Optimal PortfoliomaazwasifNo ratings yet

- Corporate Climate Risk and Bond Credit Spreads - 2024 - Finance Research Letters 4Document1 pageCorporate Climate Risk and Bond Credit Spreads - 2024 - Finance Research Letters 4JohnNo ratings yet

- Con R RSD (%) STD Average Range Max Min Replicates 5 0.752573 0.0063544 0.8443567 0.0239 0.8576 0.8337 0.8427 0.8494 0.8437 RDocument31 pagesCon R RSD (%) STD Average Range Max Min Replicates 5 0.752573 0.0063544 0.8443567 0.0239 0.8576 0.8337 0.8427 0.8494 0.8437 RMichael ThioNo ratings yet

- Kurva Kalibrasi Larutan Standar C-Organik: 1. Penentuan LinieritasDocument4 pagesKurva Kalibrasi Larutan Standar C-Organik: 1. Penentuan Linieritasaprilia kurnia putriNo ratings yet

- Heroine, Percentage: Ave 2 Ave 2 Ave 2Document3 pagesHeroine, Percentage: Ave 2 Ave 2 Ave 2Ayesha KhanNo ratings yet

- KHX3200A 1gDocument2 pagesKHX3200A 1gOvidiu VranceanuNo ratings yet

- Enter Your Data Column in A1-A90, Appraiser-Trial-PartDocument8 pagesEnter Your Data Column in A1-A90, Appraiser-Trial-PartAlejandro OlguinNo ratings yet

- Cable Sizing CalculationDocument1 pageCable Sizing Calculationmathan_aeNo ratings yet

- Bulletin #D15EDocument4 pagesBulletin #D15EPanos PanosNo ratings yet

- X Bar & R Bar SampleDocument2 pagesX Bar & R Bar SampleRaajha MunibathiranNo ratings yet

- VIFmodel 3Document2 pagesVIFmodel 3Van Joshua NunezNo ratings yet

- Number 3Document2 pagesNumber 3Mhiamar AbelladaNo ratings yet

- Branch Losses Summary Report: Etap Etap EtapDocument1 pageBranch Losses Summary Report: Etap Etap EtapJohar PradityoNo ratings yet

- Engsolutions RCB: Foundation Soil PropertiesDocument2 pagesEngsolutions RCB: Foundation Soil PropertiesReynaldo Tejada PiñerezNo ratings yet

- Expected Return Covariance Matrix: E (R) STDDocument1 pageExpected Return Covariance Matrix: E (R) STDElijah LeslieNo ratings yet

- Adams Auto-Lubrication System DesignDocument4 pagesAdams Auto-Lubrication System DesignRobin Ace SamonteNo ratings yet

- Pneumatic Control Valve Sizing GuideDocument1 pagePneumatic Control Valve Sizing GuideJOSE MARTIN MORA RIVEROSNo ratings yet

- Planilla de Cómputos MétricosDocument21 pagesPlanilla de Cómputos Métricosluis reynaldo ibarra delgadoNo ratings yet

- Verificacion de Analisis ModalDocument5 pagesVerificacion de Analisis ModalFz LlanosNo ratings yet

- Tolerance StacksDocument15 pagesTolerance StacksSanjay MehrishiNo ratings yet

- Blue Bus485 FinalDocument13 pagesBlue Bus485 FinalTamzid Ahmed AnikNo ratings yet

- Aero TrapzDocument1 pageAero TrapzHimanshu MatoNo ratings yet

- LEA20kV Ciocarlia-S2-23.03.2011Document8 pagesLEA20kV Ciocarlia-S2-23.03.2011NellyUSANo ratings yet

- Faris Zainul Arifin - BAB 4 - Konsolidasi - RevisiDocument2 pagesFaris Zainul Arifin - BAB 4 - Konsolidasi - RevisiFarisNo ratings yet

- MV Cable Technical Information - 2017Document10 pagesMV Cable Technical Information - 2017PukraDastNo ratings yet

- Censo de Carga: Estudiante: Victor Rafael Palmett ArizaDocument10 pagesCenso de Carga: Estudiante: Victor Rafael Palmett ArizaVictor PalmettNo ratings yet

- Conductor DatabaseDocument105 pagesConductor DatabaseJusTin EsteBan ArtAga HernAndezNo ratings yet

- 408 Exp 1 GraphsDocument13 pages408 Exp 1 Graphsgoabaone kgopaNo ratings yet

- MODULO 6 Analisis Sismico EstaticoDocument11 pagesMODULO 6 Analisis Sismico EstaticoLUIZ FERNANDO ALARCÓN ROJASNo ratings yet

- Two-Way Slab Check Slab Mark: Analysis CriteriaDocument8 pagesTwo-Way Slab Check Slab Mark: Analysis CriteriaAnonymous PVQdLoYnpNo ratings yet

- LinPro PrintingDocument9 pagesLinPro PrintingtresspasseeNo ratings yet

- Multiple Logistic Regression Model-LPDocument7 pagesMultiple Logistic Regression Model-LPmanjushreeNo ratings yet

- RollPower Calculator V2.2Document28 pagesRollPower Calculator V2.2Crypto FriendlyNo ratings yet

- Stab LityDocument7 pagesStab LityRenzo Gonzales EsquenNo ratings yet

- Homework No. 3..Document7 pagesHomework No. 3..Katherine PaterninaNo ratings yet

- Sementara Cdo HighDocument2 pagesSementara Cdo Highsri hastutiNo ratings yet

- NP (Conc.) (Señal) : Patrones Calibracion Informe Calibrado X y X 2 Y 2 XYDocument4 pagesNP (Conc.) (Señal) : Patrones Calibracion Informe Calibrado X y X 2 Y 2 XYLorenza MeddaNo ratings yet

- Parameters of The Model: Name Live Probabilistic Deterministic Alpha Beta DescriptionDocument6 pagesParameters of The Model: Name Live Probabilistic Deterministic Alpha Beta DescriptionAngga Prawira KautsarNo ratings yet

- Process Capability Analysis: Part Number Discription Operation Machine DepartmentDocument3 pagesProcess Capability Analysis: Part Number Discription Operation Machine DepartmentYATHISH BABUNo ratings yet

- MME3110 Assign Project 1617-2Document6 pagesMME3110 Assign Project 1617-2Muhammad Sollehen MisnanNo ratings yet

- Ventilation Sizing Summary For BLOCK LOAD BARKA MALLDocument2 pagesVentilation Sizing Summary For BLOCK LOAD BARKA MALLmechmohsin4745No ratings yet

- Each Element Is Devided by Column SumDocument3 pagesEach Element Is Devided by Column SumClutch And FlywheelNo ratings yet

- Each Element Is Devided by Column SumDocument3 pagesEach Element Is Devided by Column SumClutch And FlywheelNo ratings yet

- Parameters of The Model: Name Live Alpha Beta DescriptionDocument5 pagesParameters of The Model: Name Live Alpha Beta DescriptionAngga Prawira KautsarNo ratings yet

- Project BEM 92303Document12 pagesProject BEM 92303Jair BoulosNo ratings yet

- 02 w95 LRT OverallDocument100 pages02 w95 LRT OverallPRASARANA LRTJNo ratings yet

- ReinforcementDocument11 pagesReinforcementjvanandhNo ratings yet

- Conductoare Neizolate Din Al: Po (KW) PSCC (KW)Document5 pagesConductoare Neizolate Din Al: Po (KW) PSCC (KW)Ciprian ApalaghițeiNo ratings yet

- Tatt Agrotek BDocument17 pagesTatt Agrotek BJun AdityaNo ratings yet

- Check List For Design Building 1Document49 pagesCheck List For Design Building 1Prajwol ShresthaNo ratings yet

- Manual Transaxle PDFDocument53 pagesManual Transaxle PDFClaudio Godoy GallegosNo ratings yet

- Table - 68: A.C. Resistance and Reactance Values For Xlpe Insulated CablesDocument1 pageTable - 68: A.C. Resistance and Reactance Values For Xlpe Insulated CablesarshadbayaNo ratings yet

- Test Report AngulosDocument2 pagesTest Report Angulosdeportesaldia2014No ratings yet

- Certificate of Analysis: BS Number CC-17Document4 pagesCertificate of Analysis: BS Number CC-17Sidneide Ferreira SantosNo ratings yet

- Engine Lubrication & Cooling SystemsDocument15 pagesEngine Lubrication & Cooling SystemsMikiboi LugueNo ratings yet

- Process Capability Analysis: Part Number Discription Operation Machine DepartmentDocument9 pagesProcess Capability Analysis: Part Number Discription Operation Machine DepartmentdayalumeNo ratings yet

- Addressing Mixed Surfactant Systems and HLDDocument6 pagesAddressing Mixed Surfactant Systems and HLDMichael Taylor WarrenNo ratings yet

- HT Xlpe PDFDocument3 pagesHT Xlpe PDFrengaramanujanNo ratings yet