Un Acercamiento A La Teoria de Juegos

Un Acercamiento A La Teoria de Juegos

You might also like

- 2012-05-21 Gini Index WorksheetDocument14 pages2012-05-21 Gini Index WorksheetSam Shah100% (1)

- Racism & Capitalism. Chapter 1: Racism Today - Iggy KimDocument5 pagesRacism & Capitalism. Chapter 1: Racism Today - Iggy KimIggy KimNo ratings yet

- ACORN: Missing MillionsDocument13 pagesACORN: Missing MillionsMatthew VadumNo ratings yet

- Income Inequality in Singapore: Causes, Consequences and Policy Options - Ishita DhamaniDocument31 pagesIncome Inequality in Singapore: Causes, Consequences and Policy Options - Ishita DhamaniJunyuan100% (1)

- Wealth Tax EvasionDocument50 pagesWealth Tax EvasionJoseph SteinbergNo ratings yet

- The Art of Deduction (WEB)Document7 pagesThe Art of Deduction (WEB)Derrie SuttonNo ratings yet

- How Do Marginal Tax Rates WorkDocument7 pagesHow Do Marginal Tax Rates WorkFelippe QueirozNo ratings yet

- Agriculture Law: RS20593Document6 pagesAgriculture Law: RS20593AgricultureCaseLawNo ratings yet

- The California State Budget and Revenue Volatility: Fiscal Health in A Deficit ContextDocument16 pagesThe California State Budget and Revenue Volatility: Fiscal Health in A Deficit ContextHoover InstitutionNo ratings yet

- High Taxes HurtDocument7 pagesHigh Taxes HurtZachary JanowskiNo ratings yet

- Joint Tax Hearing-Ron DeutschDocument18 pagesJoint Tax Hearing-Ron DeutschZacharyEJWilliamsNo ratings yet

- Reforming The New York Tax Code: A Fiscal Policy Institute Report December 5, 2011Document25 pagesReforming The New York Tax Code: A Fiscal Policy Institute Report December 5, 2011fmauro7531No ratings yet

- NO On One - Website-ResponseDocument6 pagesNO On One - Website-ResponseMelinda JoyceNo ratings yet

- Democratic Budget Framework: A Balanced, Pro-Growth, and Fair Deficit Reduction PlanDocument4 pagesDemocratic Budget Framework: A Balanced, Pro-Growth, and Fair Deficit Reduction PlanInterActionNo ratings yet

- Chapter 6Document19 pagesChapter 6Steve CouncilNo ratings yet

- The 99%'s Deficit Proposal - How To Create Jobs, Reduce The Wealth Divide and Control SpendingDocument23 pagesThe 99%'s Deficit Proposal - How To Create Jobs, Reduce The Wealth Divide and Control SpendingA.J. MacDonald, Jr.No ratings yet

- Reward Work, Not Wealth: Methodology NoteDocument12 pagesReward Work, Not Wealth: Methodology NoteRaduNo ratings yet

- Shifting Responsibility: How 50 Years of Tax Cuts Benefited The Wealthiest AmericansDocument14 pagesShifting Responsibility: How 50 Years of Tax Cuts Benefited The Wealthiest AmericansStephen GrahamNo ratings yet

- Tax For Inclusive GrowthDocument19 pagesTax For Inclusive GrowthMercedes Baño HifóngNo ratings yet

- A Tale of Three TaxpayersDocument16 pagesA Tale of Three TaxpayersMercatus Center at George Mason UniversityNo ratings yet

- Chapter 5Document21 pagesChapter 5Steve CouncilNo ratings yet

- Livingston County Adopted Budget (2023)Document401 pagesLivingston County Adopted Budget (2023)Watertown Daily TimesNo ratings yet

- Budget Analysis and Deficit FinancingDocument7 pagesBudget Analysis and Deficit FinancingAKÇA ELGİNNo ratings yet

- October, 2012: Propositions 30 & 38 in Context - California Funding For Public SchoolsDocument40 pagesOctober, 2012: Propositions 30 & 38 in Context - California Funding For Public Schoolsk12newsnetworkNo ratings yet

- AmericanOpportunityAccountsAct PDFDocument2 pagesAmericanOpportunityAccountsAct PDFSenator Cory BookerNo ratings yet

- An Analysis of The "Buffett Rule": Thomas L. HungerfordDocument14 pagesAn Analysis of The "Buffett Rule": Thomas L. HungerfordPeter FinocchiaroNo ratings yet

- Livingston County 2024 Proposed BudgetDocument395 pagesLivingston County 2024 Proposed BudgetThe Livingston County NewsNo ratings yet

- Big Bank Tax DrainDocument25 pagesBig Bank Tax DrainpublicaccountabilityNo ratings yet

- Homework 3Document15 pagesHomework 3Marie StéphanNo ratings yet

- ITEP Testimony NH HB 642-1Document7 pagesITEP Testimony NH HB 642-1Dean BarkerNo ratings yet

- Taxes and The EconomyDocument23 pagesTaxes and The Economychristian_trejbal100% (1)

- The Secret IRS Files - Trove of Never-Before-Seen Records Reveal How The Wealthiest Avoid Income Tax - ProPublicaDocument25 pagesThe Secret IRS Files - Trove of Never-Before-Seen Records Reveal How The Wealthiest Avoid Income Tax - ProPublicaDouglas PierreNo ratings yet

- Workforce Development Requires Educational Reform: by L. Brooke ConawayDocument14 pagesWorkforce Development Requires Educational Reform: by L. Brooke ConawaySteve CouncilNo ratings yet

- The Federal Income Tax System For Individuals: WebextensionDocument5 pagesThe Federal Income Tax System For Individuals: WebextensionBecky Bergeon SteeleNo ratings yet

- Chapter 10Document24 pagesChapter 10Steve CouncilNo ratings yet

- Research Essay AssignmentDocument5 pagesResearch Essay AssignmentRahul SetiaNo ratings yet

- Median Increase Percentage in Home Prices 2010-PresentDocument6 pagesMedian Increase Percentage in Home Prices 2010-PresentAnonymous iVoSPSV0sNo ratings yet

- Chapter 2Document28 pagesChapter 2Steve CouncilNo ratings yet

- Chapter 3Document22 pagesChapter 3Steve CouncilNo ratings yet

- 09.07.12 JPM Fiscal Cliff White PaperDocument16 pages09.07.12 JPM Fiscal Cliff White PaperRishi ShahNo ratings yet

- Im PaperDocument8 pagesIm Paperapi-353484105No ratings yet

- 2010 Albany BudgetDocument187 pages2010 Albany BudgettulocalpoliticsNo ratings yet

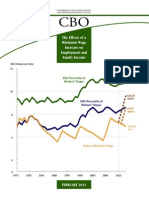

- The Effects of A Minimum-Wage Increase On Employment and Family IncomeDocument43 pagesThe Effects of A Minimum-Wage Increase On Employment and Family IncomeJeffrey DunetzNo ratings yet

- Details: California's Proposition 13Document4 pagesDetails: California's Proposition 13Somapa Mitra100% (1)

- "Headwinds To Growth": The IMF Program in EcuadorDocument27 pages"Headwinds To Growth": The IMF Program in EcuadorCenter for Economic and Policy ResearchNo ratings yet

- Bergoloetal OxREPDocument32 pagesBergoloetal OxREPregalovicNo ratings yet

- Canadian Tax Versus Necessities StudyDocument11 pagesCanadian Tax Versus Necessities StudyTyler McLeanNo ratings yet

- Options To Finance Medicare For All: $500 BillionDocument6 pagesOptions To Finance Medicare For All: $500 BillionBradyNo ratings yet

- CH 11 HW SolutionsDocument9 pagesCH 11 HW SolutionsAriefka Sari DewiNo ratings yet

- Measuring Progressivity in Canadas Tax SystemDocument10 pagesMeasuring Progressivity in Canadas Tax SystemAbid faisal AhmedNo ratings yet

- Fiscal Committees Taxes Kink Testimony 02.07.17 FinalDocument10 pagesFiscal Committees Taxes Kink Testimony 02.07.17 FinalMichael KinkNo ratings yet

- Affordability Crisis: New YorkDocument14 pagesAffordability Crisis: New YorkrkarlinNo ratings yet

- Eco208 Assignment p2Document7 pagesEco208 Assignment p2Yash AgarwalNo ratings yet

- Distributional National Accounts: Methods and Estimates For The United StatesDocument52 pagesDistributional National Accounts: Methods and Estimates For The United StatesSrinivasaNo ratings yet

- Fair Tax For IllinoisDocument8 pagesFair Tax For IllinoisjroneillNo ratings yet

- Learning to Love Form 1040: Two Cheers for the Return-Based Mass Income TaxFrom EverandLearning to Love Form 1040: Two Cheers for the Return-Based Mass Income TaxNo ratings yet

- Assignment 2 DEDocument5 pagesAssignment 2 DEbakhtawarNo ratings yet

- Delas Llagas-Journal#3Document1 pageDelas Llagas-Journal#3neilynNo ratings yet

- The Plan For A Strong and Just City: The City of New York Mayor Bill de BlasioDocument171 pagesThe Plan For A Strong and Just City: The City of New York Mayor Bill de Blasioahawkins8223No ratings yet

- Country Analysis: INDIA: A Framework To Identify and Evaluate The National Business EnvironmentDocument18 pagesCountry Analysis: INDIA: A Framework To Identify and Evaluate The National Business Environmentuzmas_3No ratings yet

- Rethinking Global Political Economy PDFDocument311 pagesRethinking Global Political Economy PDFAshiqNo ratings yet

- HSC Economics: Sample EssayDocument6 pagesHSC Economics: Sample EssayferghscNo ratings yet

- Issues of Control, Access and Misuse of Technology: ObjectivesDocument7 pagesIssues of Control, Access and Misuse of Technology: ObjectivesaddyshkNo ratings yet

- SEM 5 - INDIAN ECONOMY - PART 1 - Unit-1-3-5-ReadingsDocument1 pageSEM 5 - INDIAN ECONOMY - PART 1 - Unit-1-3-5-Readingsdheeraj sehgalNo ratings yet

- Socio-Economical Appraisal of Brics: Group 5Document13 pagesSocio-Economical Appraisal of Brics: Group 5Ankit AgrawalNo ratings yet

- Income Distribution in Malaysia: Old Issues, New Approaches (2008)Document24 pagesIncome Distribution in Malaysia: Old Issues, New Approaches (2008)Adrian Loh100% (1)

- 02 - Gandhiji - TrusteeshipDocument37 pages02 - Gandhiji - TrusteeshipSonali PatelNo ratings yet

- ABSTRACTS The Ecological Society of America 88thannual MeetingDocument398 pagesABSTRACTS The Ecological Society of America 88thannual MeetingYendra PratamaTerrificninetyninefoldNo ratings yet

- The Structural Conditions For Lasting Economic Inequality in PeruDocument2 pagesThe Structural Conditions For Lasting Economic Inequality in PeruJan LustNo ratings yet

- UNITS 1-4 What Is Globalization?: Four Main Motives That Drove People To Leave The Sanctuary of Their Family and VillageDocument16 pagesUNITS 1-4 What Is Globalization?: Four Main Motives That Drove People To Leave The Sanctuary of Their Family and VillageSalome ChubinidzeNo ratings yet

- Kokkidou 2017 From KindergartenDocument379 pagesKokkidou 2017 From KindergartenwooyannNo ratings yet

- Economic PlanningDocument26 pagesEconomic PlanningSingh HarmanNo ratings yet

- Economics Basic NotesDocument92 pagesEconomics Basic NotesSOURAV MONDALNo ratings yet

- Politics Power Cities RDocument9 pagesPolitics Power Cities RLV15_No ratings yet

- Eapp Work CompilationDocument18 pagesEapp Work CompilationshindigzsariNo ratings yet

- Discussing School and Social InequalityDocument4 pagesDiscussing School and Social InequalityMasliana SahadNo ratings yet

- Dolenec Zitko Socialist CommonsDocument11 pagesDolenec Zitko Socialist CommonsJerko BakotinNo ratings yet

- E2030 Conceptual Framework Key Competencies For 2030Document24 pagesE2030 Conceptual Framework Key Competencies For 2030April Lei IrincoNo ratings yet

- Econ PrelimDocument3 pagesEcon PrelimCAROLYN JOY BORBONNo ratings yet

- Oxfam Report On Inequality in IndiaDocument6 pagesOxfam Report On Inequality in IndiaNaveen KumarNo ratings yet

- Introduction To Sociology 11th Edition Giddens Test BankDocument24 pagesIntroduction To Sociology 11th Edition Giddens Test Banksocketedfluoxjf5100% (39)

- Poverty in The Philippines - Juan PujolDocument10 pagesPoverty in The Philippines - Juan PujolJuan PujolNo ratings yet

- 2008 7rules Firebaugh Chapter1Document35 pages2008 7rules Firebaugh Chapter1nicoNo ratings yet

Download as pdf or txt

You might also like

- 2012-05-21 Gini Index WorksheetDocument14 pages2012-05-21 Gini Index WorksheetSam Shah100% (1)

- Racism & Capitalism. Chapter 1: Racism Today - Iggy KimDocument5 pagesRacism & Capitalism. Chapter 1: Racism Today - Iggy KimIggy KimNo ratings yet

- ACORN: Missing MillionsDocument13 pagesACORN: Missing MillionsMatthew VadumNo ratings yet

- Income Inequality in Singapore: Causes, Consequences and Policy Options - Ishita DhamaniDocument31 pagesIncome Inequality in Singapore: Causes, Consequences and Policy Options - Ishita DhamaniJunyuan100% (1)

- Wealth Tax EvasionDocument50 pagesWealth Tax EvasionJoseph SteinbergNo ratings yet

- The Art of Deduction (WEB)Document7 pagesThe Art of Deduction (WEB)Derrie SuttonNo ratings yet

- How Do Marginal Tax Rates WorkDocument7 pagesHow Do Marginal Tax Rates WorkFelippe QueirozNo ratings yet

- Agriculture Law: RS20593Document6 pagesAgriculture Law: RS20593AgricultureCaseLawNo ratings yet

- The California State Budget and Revenue Volatility: Fiscal Health in A Deficit ContextDocument16 pagesThe California State Budget and Revenue Volatility: Fiscal Health in A Deficit ContextHoover InstitutionNo ratings yet

- High Taxes HurtDocument7 pagesHigh Taxes HurtZachary JanowskiNo ratings yet

- Joint Tax Hearing-Ron DeutschDocument18 pagesJoint Tax Hearing-Ron DeutschZacharyEJWilliamsNo ratings yet

- Reforming The New York Tax Code: A Fiscal Policy Institute Report December 5, 2011Document25 pagesReforming The New York Tax Code: A Fiscal Policy Institute Report December 5, 2011fmauro7531No ratings yet

- NO On One - Website-ResponseDocument6 pagesNO On One - Website-ResponseMelinda JoyceNo ratings yet

- Democratic Budget Framework: A Balanced, Pro-Growth, and Fair Deficit Reduction PlanDocument4 pagesDemocratic Budget Framework: A Balanced, Pro-Growth, and Fair Deficit Reduction PlanInterActionNo ratings yet

- Chapter 6Document19 pagesChapter 6Steve CouncilNo ratings yet

- The 99%'s Deficit Proposal - How To Create Jobs, Reduce The Wealth Divide and Control SpendingDocument23 pagesThe 99%'s Deficit Proposal - How To Create Jobs, Reduce The Wealth Divide and Control SpendingA.J. MacDonald, Jr.No ratings yet

- Reward Work, Not Wealth: Methodology NoteDocument12 pagesReward Work, Not Wealth: Methodology NoteRaduNo ratings yet

- Shifting Responsibility: How 50 Years of Tax Cuts Benefited The Wealthiest AmericansDocument14 pagesShifting Responsibility: How 50 Years of Tax Cuts Benefited The Wealthiest AmericansStephen GrahamNo ratings yet

- Tax For Inclusive GrowthDocument19 pagesTax For Inclusive GrowthMercedes Baño HifóngNo ratings yet

- A Tale of Three TaxpayersDocument16 pagesA Tale of Three TaxpayersMercatus Center at George Mason UniversityNo ratings yet

- Chapter 5Document21 pagesChapter 5Steve CouncilNo ratings yet

- Livingston County Adopted Budget (2023)Document401 pagesLivingston County Adopted Budget (2023)Watertown Daily TimesNo ratings yet

- Budget Analysis and Deficit FinancingDocument7 pagesBudget Analysis and Deficit FinancingAKÇA ELGİNNo ratings yet

- October, 2012: Propositions 30 & 38 in Context - California Funding For Public SchoolsDocument40 pagesOctober, 2012: Propositions 30 & 38 in Context - California Funding For Public Schoolsk12newsnetworkNo ratings yet

- AmericanOpportunityAccountsAct PDFDocument2 pagesAmericanOpportunityAccountsAct PDFSenator Cory BookerNo ratings yet

- An Analysis of The "Buffett Rule": Thomas L. HungerfordDocument14 pagesAn Analysis of The "Buffett Rule": Thomas L. HungerfordPeter FinocchiaroNo ratings yet

- Livingston County 2024 Proposed BudgetDocument395 pagesLivingston County 2024 Proposed BudgetThe Livingston County NewsNo ratings yet

- Big Bank Tax DrainDocument25 pagesBig Bank Tax DrainpublicaccountabilityNo ratings yet

- Homework 3Document15 pagesHomework 3Marie StéphanNo ratings yet

- ITEP Testimony NH HB 642-1Document7 pagesITEP Testimony NH HB 642-1Dean BarkerNo ratings yet

- Taxes and The EconomyDocument23 pagesTaxes and The Economychristian_trejbal100% (1)

- The Secret IRS Files - Trove of Never-Before-Seen Records Reveal How The Wealthiest Avoid Income Tax - ProPublicaDocument25 pagesThe Secret IRS Files - Trove of Never-Before-Seen Records Reveal How The Wealthiest Avoid Income Tax - ProPublicaDouglas PierreNo ratings yet

- Workforce Development Requires Educational Reform: by L. Brooke ConawayDocument14 pagesWorkforce Development Requires Educational Reform: by L. Brooke ConawaySteve CouncilNo ratings yet

- The Federal Income Tax System For Individuals: WebextensionDocument5 pagesThe Federal Income Tax System For Individuals: WebextensionBecky Bergeon SteeleNo ratings yet

- Chapter 10Document24 pagesChapter 10Steve CouncilNo ratings yet

- Research Essay AssignmentDocument5 pagesResearch Essay AssignmentRahul SetiaNo ratings yet

- Median Increase Percentage in Home Prices 2010-PresentDocument6 pagesMedian Increase Percentage in Home Prices 2010-PresentAnonymous iVoSPSV0sNo ratings yet

- Chapter 2Document28 pagesChapter 2Steve CouncilNo ratings yet

- Chapter 3Document22 pagesChapter 3Steve CouncilNo ratings yet

- 09.07.12 JPM Fiscal Cliff White PaperDocument16 pages09.07.12 JPM Fiscal Cliff White PaperRishi ShahNo ratings yet

- Im PaperDocument8 pagesIm Paperapi-353484105No ratings yet

- 2010 Albany BudgetDocument187 pages2010 Albany BudgettulocalpoliticsNo ratings yet

- The Effects of A Minimum-Wage Increase On Employment and Family IncomeDocument43 pagesThe Effects of A Minimum-Wage Increase On Employment and Family IncomeJeffrey DunetzNo ratings yet

- Details: California's Proposition 13Document4 pagesDetails: California's Proposition 13Somapa Mitra100% (1)

- "Headwinds To Growth": The IMF Program in EcuadorDocument27 pages"Headwinds To Growth": The IMF Program in EcuadorCenter for Economic and Policy ResearchNo ratings yet

- Bergoloetal OxREPDocument32 pagesBergoloetal OxREPregalovicNo ratings yet

- Canadian Tax Versus Necessities StudyDocument11 pagesCanadian Tax Versus Necessities StudyTyler McLeanNo ratings yet

- Options To Finance Medicare For All: $500 BillionDocument6 pagesOptions To Finance Medicare For All: $500 BillionBradyNo ratings yet

- CH 11 HW SolutionsDocument9 pagesCH 11 HW SolutionsAriefka Sari DewiNo ratings yet

- Measuring Progressivity in Canadas Tax SystemDocument10 pagesMeasuring Progressivity in Canadas Tax SystemAbid faisal AhmedNo ratings yet

- Fiscal Committees Taxes Kink Testimony 02.07.17 FinalDocument10 pagesFiscal Committees Taxes Kink Testimony 02.07.17 FinalMichael KinkNo ratings yet

- Affordability Crisis: New YorkDocument14 pagesAffordability Crisis: New YorkrkarlinNo ratings yet

- Eco208 Assignment p2Document7 pagesEco208 Assignment p2Yash AgarwalNo ratings yet

- Distributional National Accounts: Methods and Estimates For The United StatesDocument52 pagesDistributional National Accounts: Methods and Estimates For The United StatesSrinivasaNo ratings yet

- Fair Tax For IllinoisDocument8 pagesFair Tax For IllinoisjroneillNo ratings yet

- Learning to Love Form 1040: Two Cheers for the Return-Based Mass Income TaxFrom EverandLearning to Love Form 1040: Two Cheers for the Return-Based Mass Income TaxNo ratings yet

- Assignment 2 DEDocument5 pagesAssignment 2 DEbakhtawarNo ratings yet

- Delas Llagas-Journal#3Document1 pageDelas Llagas-Journal#3neilynNo ratings yet

- The Plan For A Strong and Just City: The City of New York Mayor Bill de BlasioDocument171 pagesThe Plan For A Strong and Just City: The City of New York Mayor Bill de Blasioahawkins8223No ratings yet

- Country Analysis: INDIA: A Framework To Identify and Evaluate The National Business EnvironmentDocument18 pagesCountry Analysis: INDIA: A Framework To Identify and Evaluate The National Business Environmentuzmas_3No ratings yet

- Rethinking Global Political Economy PDFDocument311 pagesRethinking Global Political Economy PDFAshiqNo ratings yet

- HSC Economics: Sample EssayDocument6 pagesHSC Economics: Sample EssayferghscNo ratings yet

- Issues of Control, Access and Misuse of Technology: ObjectivesDocument7 pagesIssues of Control, Access and Misuse of Technology: ObjectivesaddyshkNo ratings yet

- SEM 5 - INDIAN ECONOMY - PART 1 - Unit-1-3-5-ReadingsDocument1 pageSEM 5 - INDIAN ECONOMY - PART 1 - Unit-1-3-5-Readingsdheeraj sehgalNo ratings yet

- Socio-Economical Appraisal of Brics: Group 5Document13 pagesSocio-Economical Appraisal of Brics: Group 5Ankit AgrawalNo ratings yet

- Income Distribution in Malaysia: Old Issues, New Approaches (2008)Document24 pagesIncome Distribution in Malaysia: Old Issues, New Approaches (2008)Adrian Loh100% (1)

- 02 - Gandhiji - TrusteeshipDocument37 pages02 - Gandhiji - TrusteeshipSonali PatelNo ratings yet

- ABSTRACTS The Ecological Society of America 88thannual MeetingDocument398 pagesABSTRACTS The Ecological Society of America 88thannual MeetingYendra PratamaTerrificninetyninefoldNo ratings yet

- The Structural Conditions For Lasting Economic Inequality in PeruDocument2 pagesThe Structural Conditions For Lasting Economic Inequality in PeruJan LustNo ratings yet

- UNITS 1-4 What Is Globalization?: Four Main Motives That Drove People To Leave The Sanctuary of Their Family and VillageDocument16 pagesUNITS 1-4 What Is Globalization?: Four Main Motives That Drove People To Leave The Sanctuary of Their Family and VillageSalome ChubinidzeNo ratings yet

- Kokkidou 2017 From KindergartenDocument379 pagesKokkidou 2017 From KindergartenwooyannNo ratings yet

- Economic PlanningDocument26 pagesEconomic PlanningSingh HarmanNo ratings yet

- Economics Basic NotesDocument92 pagesEconomics Basic NotesSOURAV MONDALNo ratings yet

- Politics Power Cities RDocument9 pagesPolitics Power Cities RLV15_No ratings yet

- Eapp Work CompilationDocument18 pagesEapp Work CompilationshindigzsariNo ratings yet

- Discussing School and Social InequalityDocument4 pagesDiscussing School and Social InequalityMasliana SahadNo ratings yet

- Dolenec Zitko Socialist CommonsDocument11 pagesDolenec Zitko Socialist CommonsJerko BakotinNo ratings yet

- E2030 Conceptual Framework Key Competencies For 2030Document24 pagesE2030 Conceptual Framework Key Competencies For 2030April Lei IrincoNo ratings yet

- Econ PrelimDocument3 pagesEcon PrelimCAROLYN JOY BORBONNo ratings yet

- Oxfam Report On Inequality in IndiaDocument6 pagesOxfam Report On Inequality in IndiaNaveen KumarNo ratings yet

- Introduction To Sociology 11th Edition Giddens Test BankDocument24 pagesIntroduction To Sociology 11th Edition Giddens Test Banksocketedfluoxjf5100% (39)

- Poverty in The Philippines - Juan PujolDocument10 pagesPoverty in The Philippines - Juan PujolJuan PujolNo ratings yet

- 2008 7rules Firebaugh Chapter1Document35 pages2008 7rules Firebaugh Chapter1nicoNo ratings yet