Download as pdf or txt

You might also like

- Walt Disney Yen Financing I - Group 8Document6 pagesWalt Disney Yen Financing I - Group 8Sonal Choudhary100% (1)

- CIR vs. Pilipinas ShellDocument3 pagesCIR vs. Pilipinas ShellArchie Torres88% (8)

- 7 P's of PatanjaliDocument4 pages7 P's of PatanjaliRavi Gautam20% (5)

- G.R. No. 210836 Chevron Philippines Inc., Petitioner, Commissioner of Internal Revenue, RespondentDocument39 pagesG.R. No. 210836 Chevron Philippines Inc., Petitioner, Commissioner of Internal Revenue, RespondentEva TrinidadNo ratings yet

- Revenue Code (NIRC) Exempt From Excise Tax Is Deemed Illegal or Erroneous, and Should Be Credited orDocument5 pagesRevenue Code (NIRC) Exempt From Excise Tax Is Deemed Illegal or Erroneous, and Should Be Credited orJan Veah CaabayNo ratings yet

- Chevron V BIRDocument6 pagesChevron V BIRMark Anthony AlvarioNo ratings yet

- G.R. No. 210836 Chevron Philippines Inc., Petitioner, Commissioner of Internal Revenue, RespondentDocument5 pagesG.R. No. 210836 Chevron Philippines Inc., Petitioner, Commissioner of Internal Revenue, Respondentavalavenia2abadNo ratings yet

- September 1, 2105 G.R. No. 210836 Chevron Philippines Inc., Petitioner, Commissioner of Internal Revenue, RespondentDocument4 pagesSeptember 1, 2105 G.R. No. 210836 Chevron Philippines Inc., Petitioner, Commissioner of Internal Revenue, RespondentandreaNo ratings yet

- Chevron Vs CIRDocument12 pagesChevron Vs CIRMark Anthony AlvarioNo ratings yet

- En Banc: Resolution ResolutionDocument35 pagesEn Banc: Resolution Resolutionaspiringlawyer1234No ratings yet

- Motion For Reconsideration Filed by Petitioner Chevron Philippines, Inc. (Chevron) 1Document4 pagesMotion For Reconsideration Filed by Petitioner Chevron Philippines, Inc. (Chevron) 1Oliveros DMNo ratings yet

- Chevron v. CIR (2015)Document47 pagesChevron v. CIR (2015)Avocado DreamsNo ratings yet

- G.R. No. 210836Document4 pagesG.R. No. 210836GH IAYAMAENo ratings yet

- 37 - Chevron Philippines vs. CIRDocument2 pages37 - Chevron Philippines vs. CIRLEIGH TARITZ GANANCIALNo ratings yet

- CIR Vs ShellDocument2 pagesCIR Vs ShellSherry Mae Malabago100% (1)

- Commissioner of Internal Revenue vs. Pilipinas Shell Petroleum CorporationDocument3 pagesCommissioner of Internal Revenue vs. Pilipinas Shell Petroleum CorporationmjpjoreNo ratings yet

- Chevron vs. CIRDocument1 pageChevron vs. CIRJan EchonNo ratings yet

- 94 CIR v. ShellDocument2 pages94 CIR v. ShellNN DDLNo ratings yet

- TAx 2 Final CasesDocument15 pagesTAx 2 Final CasesGellian eve OngNo ratings yet

- Excise Tax G.R. No. 210836, 01 September 2015 Chevron vs. CIRDocument4 pagesExcise Tax G.R. No. 210836, 01 September 2015 Chevron vs. CIRcharmainejalaNo ratings yet

- Estate Tax CasesDocument51 pagesEstate Tax CasesHanna Liia GeniloNo ratings yet

- CIR Vs Pilipinas Shell Petroleum Corporation: CaseDocument3 pagesCIR Vs Pilipinas Shell Petroleum Corporation: CaseBoom EbronNo ratings yet

- Tax 2aDocument38 pagesTax 2aCharisa BelistaNo ratings yet

- G.R. No. 188497 February 19, 2014 Commissioner of Internal Revenue, Petitioner, Pilipinas Shell Petroleum Corporation, RespondentDocument5 pagesG.R. No. 188497 February 19, 2014 Commissioner of Internal Revenue, Petitioner, Pilipinas Shell Petroleum Corporation, RespondentCharisa BelistaNo ratings yet

- Chevron v. CIRDocument2 pagesChevron v. CIRannedefrancoNo ratings yet

- G.R. No. 188497Document15 pagesG.R. No. 188497ericson dela cruzNo ratings yet

- CIR v. Pilipinas Shell 2012Document13 pagesCIR v. Pilipinas Shell 2012Elle BaylonNo ratings yet

- CIR Vs Pilipinas Shell PDFDocument2 pagesCIR Vs Pilipinas Shell PDFcncrned_ctzenNo ratings yet

- Tax Review Part 1Document29 pagesTax Review Part 1JImlan Sahipa IsmaelNo ratings yet

- Chevron Philippines Inc. V. Cir G.R. No. 210836, September 01, 2015 FactsDocument1 pageChevron Philippines Inc. V. Cir G.R. No. 210836, September 01, 2015 FactsHIGHSENBERG BERGSENHIGHNo ratings yet

- Chevron Phils Inc Vs CIRDocument2 pagesChevron Phils Inc Vs CIRmonmonmonmon21100% (1)

- Chevron Vs CIRDocument2 pagesChevron Vs CIRKim Lorenzo CalatravaNo ratings yet

- Pilipinas Shell Vs CIR: Separate OpinionDocument58 pagesPilipinas Shell Vs CIR: Separate OpinionJhon Anthony BrionesNo ratings yet

- Chevron Philippines, Inc. vs. Commissioner of Internal RevenueDocument75 pagesChevron Philippines, Inc. vs. Commissioner of Internal RevenueLuigi JaroNo ratings yet

- Tax Digests On RemediesDocument22 pagesTax Digests On Remediesmadotan100% (2)

- 1 Cir, vs. Pilipinas Shell Petroleum CorporationDocument32 pages1 Cir, vs. Pilipinas Shell Petroleum CorporationChristineNo ratings yet

- TaxDocument7 pagesTaxArvi April NarzabalNo ratings yet

- PAL vs. CIRDocument16 pagesPAL vs. CIRVictoria aytonaNo ratings yet

- Philippine Airline Vs CIR GR No. 198759Document26 pagesPhilippine Airline Vs CIR GR No. 198759Janin GallanaNo ratings yet

- Parts and Wares of Every Description, Except Those Prohibited by Law, Brought Into The Zone To Be SoldDocument7 pagesParts and Wares of Every Description, Except Those Prohibited by Law, Brought Into The Zone To Be SoldStela PantaleonNo ratings yet

- Philippine Phosphate Fertilizer Corporation v. CirDocument2 pagesPhilippine Phosphate Fertilizer Corporation v. CirLoNo ratings yet

- PAL Vs CIR Proper Party To File Refund 1Document12 pagesPAL Vs CIR Proper Party To File Refund 1Evan NervezaNo ratings yet

- Phil. Airlines vs. CIR, G.R. No. 198759, July 1, 2013Document8 pagesPhil. Airlines vs. CIR, G.R. No. 198759, July 1, 2013Lou Ann AncaoNo ratings yet

- (J. Bersamin) : Code of Services Subject To VAT Is ExclusiveDocument7 pages(J. Bersamin) : Code of Services Subject To VAT Is ExclusiveED RCNo ratings yet

- Cir Vs Pilipinas ShellDocument13 pagesCir Vs Pilipinas ShellJeff GomezNo ratings yet

- Tax Review Cases 1Document76 pagesTax Review Cases 1Janice DulotanNo ratings yet

- 09 CIR Vs Pilipinas ShellDocument14 pages09 CIR Vs Pilipinas ShellEMNo ratings yet

- 5 Phil Ass SmeltingDocument4 pages5 Phil Ass SmeltingWayne ViernesNo ratings yet

- Davao Gulf Lumber Vs CIRDocument13 pagesDavao Gulf Lumber Vs CIRgsNo ratings yet

- Suggested Answers To The 2017 Bar Examinations in Taxation LawDocument15 pagesSuggested Answers To The 2017 Bar Examinations in Taxation LawRyan S. GodChild100% (2)

- Qeourt: L/epublir of Tbe TlbilippinesDocument7 pagesQeourt: L/epublir of Tbe TlbilippineswewNo ratings yet

- 9 168493-2013-Philippine Airlines Inc. v. Commissioner ofDocument14 pages9 168493-2013-Philippine Airlines Inc. v. Commissioner ofCamille CruzNo ratings yet

- Rohm Apollo vs. CIRDocument12 pagesRohm Apollo vs. CIRAsHervea AbanteNo ratings yet

- Rule 41 45 CaseDocument86 pagesRule 41 45 CaseLeizel ZafraNo ratings yet

- SILICON PHILIPPINES, INC Vs CIR G.R. No. 172378 January 17, 2011Document7 pagesSILICON PHILIPPINES, INC Vs CIR G.R. No. 172378 January 17, 2011Francise Mae Montilla MordenoNo ratings yet

- Chevron Phils Vs CIRDocument80 pagesChevron Phils Vs CIRJeanne CalalinNo ratings yet

- Tax 2Document96 pagesTax 2Luis de leonNo ratings yet

- Philippine Airlines V CIRDocument5 pagesPhilippine Airlines V CIRBettina Rayos del SolNo ratings yet

- Tax 2017 Bar Q&aDocument12 pagesTax 2017 Bar Q&aRODNA JEMA GREMILLE RE ALENTONNo ratings yet

- Philacor Credit Corporation V. Commissioner of Internal RevenueDocument10 pagesPhilacor Credit Corporation V. Commissioner of Internal RevenueCharity Gene AbuganNo ratings yet

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- Ifugao Solon On G-String: I Fight Windmills': Vincent CabrezaDocument14 pagesIfugao Solon On G-String: I Fight Windmills': Vincent Cabrezaherbs22225847No ratings yet

- Republic of The Philippines vs. Drugmakers G.R. No. 190837 March 5, 2014Document10 pagesRepublic of The Philippines vs. Drugmakers G.R. No. 190837 March 5, 2014herbs22225847No ratings yet

- Provincial Government of Camarines Norte v. Gonzalez, G.R. No. 185740, 23 July 2013Document17 pagesProvincial Government of Camarines Norte v. Gonzalez, G.R. No. 185740, 23 July 2013herbs22225847No ratings yet

- Caram Vs Segui en Banc G.R. No. 193652 August 5, 2014Document9 pagesCaram Vs Segui en Banc G.R. No. 193652 August 5, 2014herbs22225847No ratings yet

- Baguio Midland Courier V CADocument12 pagesBaguio Midland Courier V CAherbs22225847No ratings yet

- Disini v. The Secretary of Justice, G.R. No. 203335, 11 February 2014Document41 pagesDisini v. The Secretary of Justice, G.R. No. 203335, 11 February 2014herbs22225847No ratings yet

- Chavez Vs Gonzales en Banc G.R. No. 168338 February 15, 2008Document25 pagesChavez Vs Gonzales en Banc G.R. No. 168338 February 15, 2008herbs22225847No ratings yet

- Gen San Vs COA en Banc G.R. No. 199439 April 22, 2014Document20 pagesGen San Vs COA en Banc G.R. No. 199439 April 22, 2014herbs22225847No ratings yet

- Mijares Vs Ranada G.R. No. 139325 April 12, 2005Document18 pagesMijares Vs Ranada G.R. No. 139325 April 12, 2005herbs22225847No ratings yet

- F1099R RCPSDocument2 pagesF1099R RCPSherbs22225847No ratings yet

- CSC Vs Cortes G.R. No. 200103 April 23, 2014Document4 pagesCSC Vs Cortes G.R. No. 200103 April 23, 2014herbs222258470% (1)

- Timbol Vs Comelec en Banc G.R. No. 206004 February 24, 2015Document8 pagesTimbol Vs Comelec en Banc G.R. No. 206004 February 24, 2015herbs22225847No ratings yet

- Bpi V SMPDocument5 pagesBpi V SMPherbs22225847No ratings yet

- Aquino Vs Municipality of Malay G.R. No. 211356 September 29, 2014Document15 pagesAquino Vs Municipality of Malay G.R. No. 211356 September 29, 2014herbs22225847No ratings yet

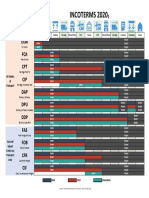

- Incoterms 2020 : Exw Fca CPTDocument1 pageIncoterms 2020 : Exw Fca CPTnilay DesaiNo ratings yet

- Risk Assessment For Capital Construction ProjectsDocument27 pagesRisk Assessment For Capital Construction ProjectsM.TauqeerNo ratings yet

- Dividend Policy - Problems For Class DiscussionDocument5 pagesDividend Policy - Problems For Class Discussionchandel08No ratings yet

- Executive SummaryDocument23 pagesExecutive SummaryLois RazonNo ratings yet

- Banking & Finance: Transfer Pricing of Interest Rates in The post-LIBOR EraDocument5 pagesBanking & Finance: Transfer Pricing of Interest Rates in The post-LIBOR Eraankur taunkNo ratings yet

- Challenges For Human Resource Management and Global Business StrategyDocument6 pagesChallenges For Human Resource Management and Global Business StrategyRoselle AbuelNo ratings yet

- Pas 7 - Statement of Cashflow: Conceptual Framework and Accounting StandardsDocument7 pagesPas 7 - Statement of Cashflow: Conceptual Framework and Accounting StandardsMeg sharkNo ratings yet

- Financial Issues Faced by Retail InvestorsDocument51 pagesFinancial Issues Faced by Retail InvestorsMoneylife Foundation100% (2)

- Chapter # 16 - Marketing GloballyDocument23 pagesChapter # 16 - Marketing GloballyAnonymous gf3tINCNo ratings yet

- Ifrs 10 Consolidated Financial Statements SnapshotDocument2 pagesIfrs 10 Consolidated Financial Statements SnapshotangaNo ratings yet

- Building Cross-Cultural Leadership Competence: An Interview With Carlos GhosnDocument3 pagesBuilding Cross-Cultural Leadership Competence: An Interview With Carlos GhosnPRIYANKA BATRANo ratings yet

- Revision MarketingDocument8 pagesRevision MarketingAnna FossiNo ratings yet

- Tax Assignment 4Document5 pagesTax Assignment 4pfungwaNo ratings yet

- Mutual Fund ScriptDocument12 pagesMutual Fund ScriptSudheesh Murali NambiarNo ratings yet

- Fundamentals Cost Accounting 5th Edition Lanen Solutions ManualDocument24 pagesFundamentals Cost Accounting 5th Edition Lanen Solutions ManualJanetSmithonyb100% (33)

- How Digital Tools Can Help Transform African Agri-Food SystemsDocument9 pagesHow Digital Tools Can Help Transform African Agri-Food SystemsRodrigo GiorgiNo ratings yet

- Project On Career Planning and DevelopmentDocument24 pagesProject On Career Planning and Developmenthema durgaNo ratings yet

- Documentary Analysis For "Magtanim Ay Di Biro" by Kara DavidDocument1 pageDocumentary Analysis For "Magtanim Ay Di Biro" by Kara DavidEishley Gwen Espiritu CabatbatNo ratings yet

- Form GST REG-06: (Amended)Document3 pagesForm GST REG-06: (Amended)ARUNNo ratings yet

- Dwnload Full Contemporary Financial Management 10th Edition Moyer Solutions Manual PDFDocument35 pagesDwnload Full Contemporary Financial Management 10th Edition Moyer Solutions Manual PDFquachhaitpit100% (19)

- App - G, Accounting PrinciplesDocument28 pagesApp - G, Accounting PrinciplesH.R. RobinNo ratings yet

- Mr. Yasir Ali: The Bright Future SchoolDocument47 pagesMr. Yasir Ali: The Bright Future SchoolWaqas AliNo ratings yet

- Final Examination Ge3 The Contemporary WorldDocument4 pagesFinal Examination Ge3 The Contemporary WorldRamon III ObligadoNo ratings yet

- Tda ProfileDocument8 pagesTda ProfileZubair MohammedNo ratings yet

- Solutuons EmeDocument8 pagesSolutuons EmeBen TorejaNo ratings yet

- Wages For ESICDocument10 pagesWages For ESICvai8havNo ratings yet

- Problems On Ratio AnalysisDocument7 pagesProblems On Ratio AnalysisVinay H V MBA100% (1)

- GGCSR Lesson 2 Strategic Management of Stakeholder RelationshipDocument6 pagesGGCSR Lesson 2 Strategic Management of Stakeholder RelationshipSkyler FaithNo ratings yet