Download as docx, pdf, or txt

You might also like

- AIA Contract Documents-Contract Relationship Diagrams (2017.04)Document11 pagesAIA Contract Documents-Contract Relationship Diagrams (2017.04)ed booker100% (2)

- Examples and Tutorial1Document7 pagesExamples and Tutorial1Hilman Abdullah67% (3)

- New Estate Tax Under TRAINDocument19 pagesNew Estate Tax Under TRAINNica09_forever100% (2)

- Supporting Community-Based Disaster ResponseDocument10 pagesSupporting Community-Based Disaster ResponseBill de BlasioNo ratings yet

- Villagracia Vs Fifth 5th Shari A District Court Case DigestDocument2 pagesVillagracia Vs Fifth 5th Shari A District Court Case Digestyannie110% (1)

- New Estate Tax Under TRAINDocument24 pagesNew Estate Tax Under TRAINDianne MedianeroNo ratings yet

- BIR Revenue Regulations No. 12-2018 - ESTATE TAXDocument11 pagesBIR Revenue Regulations No. 12-2018 - ESTATE TAXAngelette BulacanNo ratings yet

- BIR Revenue Regulations No. 12-2018Document27 pagesBIR Revenue Regulations No. 12-2018Alissa Mae PinoNo ratings yet

- Estate Tax: 1. Residents and Citizens 2. Non-Resident AliensDocument15 pagesEstate Tax: 1. Residents and Citizens 2. Non-Resident AliensJustine BartolomeNo ratings yet

- BIR Revenue Regulations No. 12-2018Document24 pagesBIR Revenue Regulations No. 12-2018Vangogh clarkNo ratings yet

- BIR Revenue Regulations No. 12-2018Document24 pagesBIR Revenue Regulations No. 12-2018Ednel LoterteNo ratings yet

- Republic of The Philippines Department of Finance Bureau of Internal RevenueDocument20 pagesRepublic of The Philippines Department of Finance Bureau of Internal RevenueVergel MartinezNo ratings yet

- Ilo Convention No. 98Document20 pagesIlo Convention No. 98pkdg1995No ratings yet

- RR No 12-2018Document20 pagesRR No 12-2018june Alvarez100% (1)

- Republic of The Philippines Department of Finance Bureau of Internal RevenueDocument22 pagesRepublic of The Philippines Department of Finance Bureau of Internal RevenueMJ FloresNo ratings yet

- RR 12-18Document33 pagesRR 12-18Greg JalosNo ratings yet

- Digest RR 12-2018Document5 pagesDigest RR 12-2018Jesi CarlosNo ratings yet

- Estate TaxDocument31 pagesEstate TaxMa.annNo ratings yet

- Estate TaxDocument14 pagesEstate TaxEM DOMINGONo ratings yet

- Estate Taxation ReportDocument15 pagesEstate Taxation ReportJan Gabriel VillanuevaNo ratings yet

- Estate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andDocument6 pagesEstate Tax - A Tax Levied On The Transmission of Properties From A To His Lawful Heirs andAngelyn SamandeNo ratings yet

- RR 12-18Document21 pagesRR 12-18Kath MativoNo ratings yet

- RR 12-18Document31 pagesRR 12-18Donna DelgadoNo ratings yet

- Estate and Donors TaxDocument31 pagesEstate and Donors TaxchiongNo ratings yet

- RR 12-2018Document32 pagesRR 12-2018rodrigoNo ratings yet

- Bir Estate TaxDocument4 pagesBir Estate Taxlonitsuaf100% (1)

- Notes in Estate TaxDocument32 pagesNotes in Estate TaxAngelyn SamandeNo ratings yet

- Estate Tax AmnestyDocument22 pagesEstate Tax AmnestyRobert Jayson UyNo ratings yet

- Section 11 BankingDocument6 pagesSection 11 BankingMay TanNo ratings yet

- TAX With TRAIN LAW - Transfer and Business TaxDocument61 pagesTAX With TRAIN LAW - Transfer and Business TaxRamon AngelesNo ratings yet

- Estate and Donor Rrs and RamoDocument12 pagesEstate and Donor Rrs and Ramocmv mendozaNo ratings yet

- Estate Tax and Donor Tax NotesDocument12 pagesEstate Tax and Donor Tax NotesClaudenne Steffanie CastilloNo ratings yet

- Tax SummaryDocument15 pagesTax SummaryCassiopeia Cashmere GodheidNo ratings yet

- Session 2Document21 pagesSession 2Yippella De JesusNo ratings yet

- Revenue Regulations 02-03Document22 pagesRevenue Regulations 02-03Anonymous HIBt2h6z7No ratings yet

- Taxation Up To VAT Complete With Notes From RR and RMC. Tababa 1Document96 pagesTaxation Up To VAT Complete With Notes From RR and RMC. Tababa 1Val Escobar Magumun100% (1)

- Affidavit of Self AdjudicationDocument4 pagesAffidavit of Self AdjudicationCPMMNo ratings yet

- Taxation Law Discussions by Professor ORTEGADocument15 pagesTaxation Law Discussions by Professor ORTEGAKring de VeraNo ratings yet

- Revenue Regulations No. 2-2003Document0 pagesRevenue Regulations No. 2-2003Lyceum LawlibraryNo ratings yet

- Estate TaxDocument13 pagesEstate Taxfly awayNo ratings yet

- What Are The Governing Rules Regarding The Liquidation?Document9 pagesWhat Are The Governing Rules Regarding The Liquidation?martin ngipolNo ratings yet

- Estate Tax - Ust PDFDocument14 pagesEstate Tax - Ust PDFFordan AntolinoNo ratings yet

- Estate Tax Amnesty ActDocument10 pagesEstate Tax Amnesty ActJocelyn MendozaNo ratings yet

- FRIA and PCADocument74 pagesFRIA and PCANiñanne Nicole Baring BalbuenaNo ratings yet

- EstateDocument10 pagesEstateGelyn CruzNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument60 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledJomer FernandezNo ratings yet

- Fria Codal Sections 1 75Document40 pagesFria Codal Sections 1 75Gayle OribeNo ratings yet

- Transfer Taxes Ust 1Document18 pagesTransfer Taxes Ust 1JAY AUBREY PINEDANo ratings yet

- Republic of The Philippines Court of Tax Appeals Quezon CityDocument11 pagesRepublic of The Philippines Court of Tax Appeals Quezon CityCJNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument8 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledAdam SmithNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippine Congress AssembledDocument76 pagesBe It Enacted by The Senate and House of Representatives of The Philippine Congress AssembledFrancis Coronel Jr.No ratings yet

- BusTax - Chapter 3 MODULEDocument8 pagesBusTax - Chapter 3 MODULETimon CarandangNo ratings yet

- Banking LawsDocument76 pagesBanking LawslikeascielNo ratings yet

- Bank Secrecy Law and Truth in Lending ActDocument23 pagesBank Secrecy Law and Truth in Lending ActJuliana ChengNo ratings yet

- R.A. No. 10142 - FINANCIAL REHABILITATION INSOLVENCY ACT of 2010Document53 pagesR.A. No. 10142 - FINANCIAL REHABILITATION INSOLVENCY ACT of 2010sinodingjr nuskaNo ratings yet

- Extrajudicial Settlement of Estate in The PhilippinesDocument4 pagesExtrajudicial Settlement of Estate in The PhilippinesDon Astorga Dehayco0% (1)

- Bar Review Companion: Taxation: Anvil Law Books Series, #4From EverandBar Review Companion: Taxation: Anvil Law Books Series, #4No ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Raising Money – Legally: A Practical Guide to Raising CapitalFrom EverandRaising Money – Legally: A Practical Guide to Raising CapitalRating: 4 out of 5 stars4/5 (1)

- Chapter 4: Accounting For Budgetary AccountsDocument37 pagesChapter 4: Accounting For Budgetary Accountsjanjan eresoNo ratings yet

- Excel ResearchDocument11 pagesExcel Researchjanjan eresoNo ratings yet

- Exually Ransmitted IseasesDocument52 pagesExually Ransmitted Iseasesjanjan eresoNo ratings yet

- Human Immunodeficiency Virus: Dr. S.K ChaturvediDocument20 pagesHuman Immunodeficiency Virus: Dr. S.K Chaturvedijanjan eresoNo ratings yet

- The Unified Accounts Code Structure: (UACS)Document67 pagesThe Unified Accounts Code Structure: (UACS)janjan eresoNo ratings yet

- The Presence of An STD Increases The Possibility Of: Infection With HIV & HIVDocument22 pagesThe Presence of An STD Increases The Possibility Of: Infection With HIV & HIVjanjan eresoNo ratings yet

- Transfer and Business Tax SolmanDocument4 pagesTransfer and Business Tax Solmanjanjan eresoNo ratings yet

- African CultureDocument47 pagesAfrican Culturejanjan eresoNo ratings yet

- Value-Added Tax: Characteristics (Abcd Vip)Document9 pagesValue-Added Tax: Characteristics (Abcd Vip)janjan eresoNo ratings yet

- Gillaco Nov 7 2018 PDFDocument1 pageGillaco Nov 7 2018 PDFjanjan eresoNo ratings yet

- de Leon ReviewerDocument6 pagesde Leon Reviewerjanjan eresoNo ratings yet

- World Culture: SubtitleDocument46 pagesWorld Culture: Subtitlejanjan eresoNo ratings yet

- VHF Transceiver: June 2013Document37 pagesVHF Transceiver: June 2013Viorel AldeaNo ratings yet

- Readme Tia Portal v13 Update 1 enDocument10 pagesReadme Tia Portal v13 Update 1 enVinicius Murilo LimaNo ratings yet

- Proceso Quiros and Leonarda Villegas v. Marcelo Arjona, Teresita Balarbar, Josephine Arjona, and Conchita ArjonaDocument2 pagesProceso Quiros and Leonarda Villegas v. Marcelo Arjona, Teresita Balarbar, Josephine Arjona, and Conchita Arjonacassandra leeNo ratings yet

- Graficos de Bombas PVBasicsDocument45 pagesGraficos de Bombas PVBasicsLuis Panti EkNo ratings yet

- 18 March 2021 - BEO Kemenhub Dir. Sarana Transportasi Jalan Group 1Document2 pages18 March 2021 - BEO Kemenhub Dir. Sarana Transportasi Jalan Group 1Muhammad Wafiq AzzisNo ratings yet

- Reduction of Bending Defects in Hard Disk Drive Suspensions: Khwanchai Huailuk, Napassavong RojanarowanDocument7 pagesReduction of Bending Defects in Hard Disk Drive Suspensions: Khwanchai Huailuk, Napassavong RojanarowanIOSRJEN : hard copy, certificates, Call for Papers 2013, publishing of journalNo ratings yet

- Madison County ScoresDocument3 pagesMadison County ScoresMike BrownNo ratings yet

- Syllabus - Management 351 - Professor David Wyld, Southeastern Louisiana UniversityDocument16 pagesSyllabus - Management 351 - Professor David Wyld, Southeastern Louisiana UniversityDavid WyldNo ratings yet

- Online Recruitment SystemDocument28 pagesOnline Recruitment Systemsatya5848100% (3)

- Fish Meal-Technical SpecificationDocument2 pagesFish Meal-Technical SpecificationHitendra Nath BarmmaNo ratings yet

- Expokit: A Software Package For Computing Matrix ExponentialsDocument21 pagesExpokit: A Software Package For Computing Matrix ExponentialsAleksandarBukvaNo ratings yet

- Chapter 26 - Business Cycle, Unemployment and InflationDocument20 pagesChapter 26 - Business Cycle, Unemployment and InflationPavan PatelNo ratings yet

- Dangers of Social Networking 1Document4 pagesDangers of Social Networking 1Kerri McFarlaneNo ratings yet

- The Management of Foreign Exchange RiskDocument97 pagesThe Management of Foreign Exchange RiskVajira Weerasena100% (1)

- IRTCDocument385 pagesIRTCSatyakam MishraNo ratings yet

- School Enrollment System AbstractDocument3 pagesSchool Enrollment System AbstractsunnyNo ratings yet

- University of Gondar College of Business and Economics: Scool of Economics PPT Compiled For Macroeconomics IDocument83 pagesUniversity of Gondar College of Business and Economics: Scool of Economics PPT Compiled For Macroeconomics IMERSHANo ratings yet

- 13 Electrical Pole's TrasverseDocument7 pages13 Electrical Pole's TrasverseReza PahlepiNo ratings yet

- Name: Goutam Mandal Roll No: 1916034 PGPEM-2019 Assignment-IIDocument11 pagesName: Goutam Mandal Roll No: 1916034 PGPEM-2019 Assignment-IIGoutam MandalNo ratings yet

- CartelizationDocument5 pagesCartelizationGarima BatraNo ratings yet

- Listening Test: Directions: For Each Question in This Part, You Will Hear Four Statements About A Picture in YourDocument40 pagesListening Test: Directions: For Each Question in This Part, You Will Hear Four Statements About A Picture in YourTrương Hữu LộcNo ratings yet

- Individual Daily Log and Accomplishment Report: Enclosure No. 3 To Deped Order No. 011, S. 2020Document2 pagesIndividual Daily Log and Accomplishment Report: Enclosure No. 3 To Deped Order No. 011, S. 2020cristina maquintoNo ratings yet

- European Patent Office (Epo) As Designated (Or Elected) OfficeDocument40 pagesEuropean Patent Office (Epo) As Designated (Or Elected) Officejasont_75No ratings yet

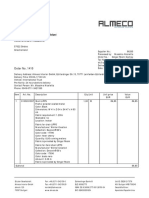

- B 1410 - B&N Contract Furniture S.A. - Almeco Interior GMBHDocument2 pagesB 1410 - B&N Contract Furniture S.A. - Almeco Interior GMBHmaxNo ratings yet

- FEU HO1 Audit of Inventories 2017 PDFDocument4 pagesFEU HO1 Audit of Inventories 2017 PDFJoshuaNo ratings yet

- 10 May 2021Document1 page10 May 2021TushNo ratings yet