Raymond LTD: Market Outperformer (Rs. 411)

Raymond LTD: Market Outperformer (Rs. 411)

You might also like

- DA4387 Level II CFA Mock Exam 2018 Afternoon ADocument36 pagesDA4387 Level II CFA Mock Exam 2018 Afternoon ARain_Maker11250% (2)

- Management Trust SampleDocument37 pagesManagement Trust SampleElpress Shemu'a Maha Yahudah-ElNo ratings yet

- History, Salient Features and Social Control of Banking Regulation Act, 1949Document9 pagesHistory, Salient Features and Social Control of Banking Regulation Act, 1949Anuj Kamal67% (3)

- Motilal Oswal PVR Q2FY21 Result UpdateDocument12 pagesMotilal Oswal PVR Q2FY21 Result Updateumaj25No ratings yet

- Bhel (Bhel In) : Q4FY19 Result UpdateDocument6 pagesBhel (Bhel In) : Q4FY19 Result Updatesaran21No ratings yet

- Maruti Suzuki (MSIL IN) : Q1FY20 Result UpdateDocument6 pagesMaruti Suzuki (MSIL IN) : Q1FY20 Result UpdateHitesh JainNo ratings yet

- Hero Motocorp: CMP: Inr3,707 TP: Inr3,818 (+3%)Document12 pagesHero Motocorp: CMP: Inr3,707 TP: Inr3,818 (+3%)SAHIL SHARMANo ratings yet

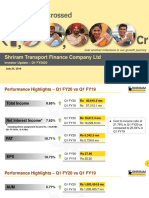

- Shriram Transport Q1 FY20 PresentationDocument18 pagesShriram Transport Q1 FY20 PresentationVenkata Reddy KNo ratings yet

- Motherson Sumi System DataDocument4 pagesMotherson Sumi System DataNishaVishwanathNo ratings yet

- IDirect SKFIndia Q2FY20Document10 pagesIDirect SKFIndia Q2FY20praveensingh77No ratings yet

- Golden Stocks PortfolioDocument6 pagesGolden Stocks PortfoliocompangelNo ratings yet

- Parag Milk Foods: CMP: INR207 TP: INR255 (+23%) BuyDocument10 pagesParag Milk Foods: CMP: INR207 TP: INR255 (+23%) BuyNiravAcharyaNo ratings yet

- Fineorg 25 5 23 PLDocument8 pagesFineorg 25 5 23 PLSubhash MsNo ratings yet

- Avenue Supermarts (DMART IN) : Q1FY20 Result UpdateDocument8 pagesAvenue Supermarts (DMART IN) : Q1FY20 Result UpdatejigarchhatrolaNo ratings yet

- Mahindra & Mahindra: CMP: INR672 TP: INR810 (+20%)Document14 pagesMahindra & Mahindra: CMP: INR672 TP: INR810 (+20%)Yash DoshiNo ratings yet

- Equity Research BritaniaDocument8 pagesEquity Research BritaniaVaibhav BajpaiNo ratings yet

- Pricing Pressure Continues To Hurt Performance: CMP: INR5,987 TP: INR5,670 (-5%)Document10 pagesPricing Pressure Continues To Hurt Performance: CMP: INR5,987 TP: INR5,670 (-5%)karnasutputra0No ratings yet

- Tata Motors: Demand Concerns Persist, Not Out of The Woods YetDocument10 pagesTata Motors: Demand Concerns Persist, Not Out of The Woods YetVARUN SINGLANo ratings yet

- Stock Report On Baja Auto in India Ma 23 2020Document12 pagesStock Report On Baja Auto in India Ma 23 2020PranavPillaiNo ratings yet

- Coal India: Steady Performance...Document8 pagesCoal India: Steady Performance...Tejas ShahNo ratings yet

- ICICI - Piramal EnterprisesDocument16 pagesICICI - Piramal EnterprisessehgalgauravNo ratings yet

- Tata Motors Limited: Improved JLR Performance in ChinaDocument5 pagesTata Motors Limited: Improved JLR Performance in ChinaUdayan KarnatakNo ratings yet

- JK Lakshmi Cement 18062019Document6 pagesJK Lakshmi Cement 18062019saran21No ratings yet

- United Breweries: CMP: INR1,048 TP: INR700 (-33%) Worsening Outlook, Expensive Valuations Maintain SellDocument10 pagesUnited Breweries: CMP: INR1,048 TP: INR700 (-33%) Worsening Outlook, Expensive Valuations Maintain Selldnwekfnkfnknf skkjdbNo ratings yet

- Maruti Suzuki India: Volume Decline in Offing, Expensive ValuationsDocument13 pagesMaruti Suzuki India: Volume Decline in Offing, Expensive ValuationsPulkit TalujaNo ratings yet

- Indsec ABFRL Q1 FY'21Document9 pagesIndsec ABFRL Q1 FY'21PriyankaNo ratings yet

- HDFC Securities ITC 27-6-2020Document13 pagesHDFC Securities ITC 27-6-2020Sivas SubramaniyanNo ratings yet

- Q1 2021 ICICI Bandhan BankDocument9 pagesQ1 2021 ICICI Bandhan BankS.Sharique HassanNo ratings yet

- Dabur India: Strong Domestic Volume Growth Lifts RevenuesDocument9 pagesDabur India: Strong Domestic Volume Growth Lifts RevenuesRaghavendra Pratap SinghNo ratings yet

- CD Equisearchpvt LTD CD Equisearchpvt LTD: Quarterly HighlightsDocument10 pagesCD Equisearchpvt LTD CD Equisearchpvt LTD: Quarterly HighlightsBhaveek OstwalNo ratings yet

- Sun Pharma - EQuity Reserch ReportDocument6 pagesSun Pharma - EQuity Reserch ReportsmitNo ratings yet

- Ashok Leyland: CMP: INR115 TP: INR134 (+17%)Document10 pagesAshok Leyland: CMP: INR115 TP: INR134 (+17%)Jitendra GaglaniNo ratings yet

- Kotak Mahindra Bank: CMP: INR1,629 TP: INR1,600 (-2%)Document12 pagesKotak Mahindra Bank: CMP: INR1,629 TP: INR1,600 (-2%)HARDIK SHAHNo ratings yet

- Koutons Retail India (KOURET) : Dismal PerformanceDocument6 pagesKoutons Retail India (KOURET) : Dismal Performancevir_4uNo ratings yet

- Abfrl 20240215 Mosl Ru PG012Document12 pagesAbfrl 20240215 Mosl Ru PG012krishna_buntyNo ratings yet

- Zensar Technologies (ZENT IN) : Q3FY19 Result UpdateDocument8 pagesZensar Technologies (ZENT IN) : Q3FY19 Result Updatesaran21No ratings yet

- IDirect MarutiSuzuki Q2FY19Document12 pagesIDirect MarutiSuzuki Q2FY19Rajani KantNo ratings yet

- Mastek LTD: Index DetailsDocument12 pagesMastek LTD: Index DetailsAshokNo ratings yet

- Digitally Signed by VIVEK Pritamlal Raizada Date: 2020.05.11 17:25:48 +05'30'Document20 pagesDigitally Signed by VIVEK Pritamlal Raizada Date: 2020.05.11 17:25:48 +05'30'DIPAN BISWASNo ratings yet

- Annual Report of Info Edge by Icici SecurityDocument12 pagesAnnual Report of Info Edge by Icici SecurityGobind yNo ratings yet

- GSK PharmaDocument10 pagesGSK PharmaSasidharan Sajeev ChathathuNo ratings yet

- SP Apparels 3QFY24 PresentationDocument46 pagesSP Apparels 3QFY24 PresentationAnand SrinivasanNo ratings yet

- Reliance Industries: CMP: INR1,077 TP: INR1,057 (-2%)Document18 pagesReliance Industries: CMP: INR1,077 TP: INR1,057 (-2%)Abhiroop DasNo ratings yet

- S Chand and Company (SCHAND IN) : Q4FY20 Result UpdateDocument6 pagesS Chand and Company (SCHAND IN) : Q4FY20 Result UpdateRaj PrakashNo ratings yet

- Ultratech Cement: CMP: Inr6,485 TP: Inr8,050 (+24%) Market Share Gains Con Nue BuyDocument10 pagesUltratech Cement: CMP: Inr6,485 TP: Inr8,050 (+24%) Market Share Gains Con Nue BuyLive NIftyNo ratings yet

- Investor Presentation (Company Update)Document24 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- Equity Research Report On Titan Company LTDDocument10 pagesEquity Research Report On Titan Company LTDmundadaharsh1No ratings yet

- S Chand and Company (SCHAND IN) : Q3FY20 Result UpdateDocument6 pagesS Chand and Company (SCHAND IN) : Q3FY20 Result UpdateanjugaduNo ratings yet

- REPCO - RR - 14022024 14 February 2024 1923849091Document17 pagesREPCO - RR - 14022024 14 February 2024 1923849091Sanjeedeep Mishra , 315No ratings yet

- Trent 10 08 2023 IscDocument7 pagesTrent 10 08 2023 Iscaghosh704No ratings yet

- TVS Motor - 1QFY20 Result - JM FinancialDocument8 pagesTVS Motor - 1QFY20 Result - JM FinancialdarshanmadeNo ratings yet

- Jubilant Life Sciences: CMP: INR596 TP: INR800 (+34%)Document10 pagesJubilant Life Sciences: CMP: INR596 TP: INR800 (+34%)Shashanka HollaNo ratings yet

- Princpip 11 8 23 PLDocument6 pagesPrincpip 11 8 23 PLAnubhi Garg374No ratings yet

- Tata Motors Consolidated Q2 FY21 Results: EBIT Breakeven and Positive Free Cash Flows Delivered in The QuarterDocument4 pagesTata Motors Consolidated Q2 FY21 Results: EBIT Breakeven and Positive Free Cash Flows Delivered in The QuarterEsha ChaudharyNo ratings yet

- V Guard Industries Q3 FY22 Results PresentationDocument17 pagesV Guard Industries Q3 FY22 Results PresentationRATHINo ratings yet

- Initiating Coverage - Trident LTD - 311020Document21 pagesInitiating Coverage - Trident LTD - 311020V KeshavdevNo ratings yet

- Wipro: CMP: INR243 TP: INR260 (+7%) Largely in Line Lower ETR Drives A Beat in ProfitabilityDocument14 pagesWipro: CMP: INR243 TP: INR260 (+7%) Largely in Line Lower ETR Drives A Beat in ProfitabilityPramod KulkarniNo ratings yet

- Maruti Suzuki India: Muted Quarter Volume Trough Seemingly in SightDocument12 pagesMaruti Suzuki India: Muted Quarter Volume Trough Seemingly in SightDushyant ChaturvediNo ratings yet

- Press 15jun20Document4 pagesPress 15jun20Rama MadhuNo ratings yet

- V Guard Industries Q4 Results PresentationDocument23 pagesV Guard Industries Q4 Results PresentationIlyasNo ratings yet

- Gulf Oil Lubricants: Stable Performance..Document8 pagesGulf Oil Lubricants: Stable Performance..Doshi VaibhavNo ratings yet

- Bharat Forge: Performance HighlightsDocument13 pagesBharat Forge: Performance HighlightsarikuldeepNo ratings yet

- Economic Indicators for South and Central Asia: Input–Output TablesFrom EverandEconomic Indicators for South and Central Asia: Input–Output TablesNo ratings yet

- Chapter 6 Financial AssetsDocument6 pagesChapter 6 Financial AssetsJoyce Mae D. FloresNo ratings yet

- Problem 31 1Document3 pagesProblem 31 1CodeSeeker100% (1)

- Taxation Law 1 - Mijares SyllabusDocument11 pagesTaxation Law 1 - Mijares SyllabusAngelo Tiglao100% (1)

- Consent To Short Notice of An Annual General MeetingDocument1 pageConsent To Short Notice of An Annual General MeetingKenny NguyenNo ratings yet

- Escrow Agreement With InterestDocument5 pagesEscrow Agreement With InterestpaulmercadoNo ratings yet

- Delisting Checklist PDFDocument4 pagesDelisting Checklist PDFsnjv2621No ratings yet

- Metroplex Berhad Vs Sinophil, GR 208281, June 28, 2021Document31 pagesMetroplex Berhad Vs Sinophil, GR 208281, June 28, 2021Catherine Dimailig0% (4)

- VII ADocument17 pagesVII AtudosecristinaNo ratings yet

- The System Building BlueprintDocument8 pagesThe System Building Blueprintstormin64No ratings yet

- Bonds ValuationsDocument57 pagesBonds ValuationsarmailgmNo ratings yet

- CIG Limba Engleza 2Document54 pagesCIG Limba Engleza 2Carmen BusteaNo ratings yet

- Chapter 15 PartnershipDocument56 pagesChapter 15 PartnershipNurullita KartikaNo ratings yet

- Iqra University: TO Business Finance / Finance FOR ManagersDocument9 pagesIqra University: TO Business Finance / Finance FOR ManagersKanwal NaazNo ratings yet

- MBA4013 Management of Banking andDocument7 pagesMBA4013 Management of Banking andNurfaiqah AmniNo ratings yet

- Thermo Fisher To Acquire Life Technologies IR PresentationDocument13 pagesThermo Fisher To Acquire Life Technologies IR PresentationTariq MotiwalaNo ratings yet

- Theories of Exchange RateDocument37 pagesTheories of Exchange Ratedranita@yahoo.comNo ratings yet

- 20.2 Letter of Intent To Purchase A BusinessDocument5 pages20.2 Letter of Intent To Purchase A BusinessPeeve Kaye BalbuenaNo ratings yet

- Risk Management Summary: Calpers Trust Level ReviewDocument9 pagesRisk Management Summary: Calpers Trust Level ReviewOluwaloseyi SekoniNo ratings yet

- Mark Plan and Examiner'S Commentary: General CommentsDocument9 pagesMark Plan and Examiner'S Commentary: General Commentscima2k15100% (1)

- VALUATION by Reynaldo NogralesDocument29 pagesVALUATION by Reynaldo NogralesresiajhiNo ratings yet

- Rev CTA 8835 8790 Chevron Holdings Inc vs. CIRDocument20 pagesRev CTA 8835 8790 Chevron Holdings Inc vs. CIRJerome Delos ReyesNo ratings yet

- Ford Motor CompanyDocument5 pagesFord Motor CompanyFaria CHNo ratings yet

- Godrej Financial AnalysisDocument16 pagesGodrej Financial AnalysisVaibhav Jain100% (1)

- Amit Kumar Share KhanDocument77 pagesAmit Kumar Share KhanRohit GanjooNo ratings yet

- BRACEY - William FP - Profile 21042016 v2 3 1 PDFDocument1 pageBRACEY - William FP - Profile 21042016 v2 3 1 PDFVivek GhosalNo ratings yet

- Chapter 8Document5 pagesChapter 8Fahad UmarNo ratings yet

- Moody's FrameworkDocument30 pagesMoody's FrameworkbulbNo ratings yet

Download as pdf or txt

You might also like

- DA4387 Level II CFA Mock Exam 2018 Afternoon ADocument36 pagesDA4387 Level II CFA Mock Exam 2018 Afternoon ARain_Maker11250% (2)

- Management Trust SampleDocument37 pagesManagement Trust SampleElpress Shemu'a Maha Yahudah-ElNo ratings yet

- History, Salient Features and Social Control of Banking Regulation Act, 1949Document9 pagesHistory, Salient Features and Social Control of Banking Regulation Act, 1949Anuj Kamal67% (3)

- Motilal Oswal PVR Q2FY21 Result UpdateDocument12 pagesMotilal Oswal PVR Q2FY21 Result Updateumaj25No ratings yet

- Bhel (Bhel In) : Q4FY19 Result UpdateDocument6 pagesBhel (Bhel In) : Q4FY19 Result Updatesaran21No ratings yet

- Maruti Suzuki (MSIL IN) : Q1FY20 Result UpdateDocument6 pagesMaruti Suzuki (MSIL IN) : Q1FY20 Result UpdateHitesh JainNo ratings yet

- Hero Motocorp: CMP: Inr3,707 TP: Inr3,818 (+3%)Document12 pagesHero Motocorp: CMP: Inr3,707 TP: Inr3,818 (+3%)SAHIL SHARMANo ratings yet

- Shriram Transport Q1 FY20 PresentationDocument18 pagesShriram Transport Q1 FY20 PresentationVenkata Reddy KNo ratings yet

- Motherson Sumi System DataDocument4 pagesMotherson Sumi System DataNishaVishwanathNo ratings yet

- IDirect SKFIndia Q2FY20Document10 pagesIDirect SKFIndia Q2FY20praveensingh77No ratings yet

- Golden Stocks PortfolioDocument6 pagesGolden Stocks PortfoliocompangelNo ratings yet

- Parag Milk Foods: CMP: INR207 TP: INR255 (+23%) BuyDocument10 pagesParag Milk Foods: CMP: INR207 TP: INR255 (+23%) BuyNiravAcharyaNo ratings yet

- Fineorg 25 5 23 PLDocument8 pagesFineorg 25 5 23 PLSubhash MsNo ratings yet

- Avenue Supermarts (DMART IN) : Q1FY20 Result UpdateDocument8 pagesAvenue Supermarts (DMART IN) : Q1FY20 Result UpdatejigarchhatrolaNo ratings yet

- Mahindra & Mahindra: CMP: INR672 TP: INR810 (+20%)Document14 pagesMahindra & Mahindra: CMP: INR672 TP: INR810 (+20%)Yash DoshiNo ratings yet

- Equity Research BritaniaDocument8 pagesEquity Research BritaniaVaibhav BajpaiNo ratings yet

- Pricing Pressure Continues To Hurt Performance: CMP: INR5,987 TP: INR5,670 (-5%)Document10 pagesPricing Pressure Continues To Hurt Performance: CMP: INR5,987 TP: INR5,670 (-5%)karnasutputra0No ratings yet

- Tata Motors: Demand Concerns Persist, Not Out of The Woods YetDocument10 pagesTata Motors: Demand Concerns Persist, Not Out of The Woods YetVARUN SINGLANo ratings yet

- Stock Report On Baja Auto in India Ma 23 2020Document12 pagesStock Report On Baja Auto in India Ma 23 2020PranavPillaiNo ratings yet

- Coal India: Steady Performance...Document8 pagesCoal India: Steady Performance...Tejas ShahNo ratings yet

- ICICI - Piramal EnterprisesDocument16 pagesICICI - Piramal EnterprisessehgalgauravNo ratings yet

- Tata Motors Limited: Improved JLR Performance in ChinaDocument5 pagesTata Motors Limited: Improved JLR Performance in ChinaUdayan KarnatakNo ratings yet

- JK Lakshmi Cement 18062019Document6 pagesJK Lakshmi Cement 18062019saran21No ratings yet

- United Breweries: CMP: INR1,048 TP: INR700 (-33%) Worsening Outlook, Expensive Valuations Maintain SellDocument10 pagesUnited Breweries: CMP: INR1,048 TP: INR700 (-33%) Worsening Outlook, Expensive Valuations Maintain Selldnwekfnkfnknf skkjdbNo ratings yet

- Maruti Suzuki India: Volume Decline in Offing, Expensive ValuationsDocument13 pagesMaruti Suzuki India: Volume Decline in Offing, Expensive ValuationsPulkit TalujaNo ratings yet

- Indsec ABFRL Q1 FY'21Document9 pagesIndsec ABFRL Q1 FY'21PriyankaNo ratings yet

- HDFC Securities ITC 27-6-2020Document13 pagesHDFC Securities ITC 27-6-2020Sivas SubramaniyanNo ratings yet

- Q1 2021 ICICI Bandhan BankDocument9 pagesQ1 2021 ICICI Bandhan BankS.Sharique HassanNo ratings yet

- Dabur India: Strong Domestic Volume Growth Lifts RevenuesDocument9 pagesDabur India: Strong Domestic Volume Growth Lifts RevenuesRaghavendra Pratap SinghNo ratings yet

- CD Equisearchpvt LTD CD Equisearchpvt LTD: Quarterly HighlightsDocument10 pagesCD Equisearchpvt LTD CD Equisearchpvt LTD: Quarterly HighlightsBhaveek OstwalNo ratings yet

- Sun Pharma - EQuity Reserch ReportDocument6 pagesSun Pharma - EQuity Reserch ReportsmitNo ratings yet

- Ashok Leyland: CMP: INR115 TP: INR134 (+17%)Document10 pagesAshok Leyland: CMP: INR115 TP: INR134 (+17%)Jitendra GaglaniNo ratings yet

- Kotak Mahindra Bank: CMP: INR1,629 TP: INR1,600 (-2%)Document12 pagesKotak Mahindra Bank: CMP: INR1,629 TP: INR1,600 (-2%)HARDIK SHAHNo ratings yet

- Koutons Retail India (KOURET) : Dismal PerformanceDocument6 pagesKoutons Retail India (KOURET) : Dismal Performancevir_4uNo ratings yet

- Abfrl 20240215 Mosl Ru PG012Document12 pagesAbfrl 20240215 Mosl Ru PG012krishna_buntyNo ratings yet

- Zensar Technologies (ZENT IN) : Q3FY19 Result UpdateDocument8 pagesZensar Technologies (ZENT IN) : Q3FY19 Result Updatesaran21No ratings yet

- IDirect MarutiSuzuki Q2FY19Document12 pagesIDirect MarutiSuzuki Q2FY19Rajani KantNo ratings yet

- Mastek LTD: Index DetailsDocument12 pagesMastek LTD: Index DetailsAshokNo ratings yet

- Digitally Signed by VIVEK Pritamlal Raizada Date: 2020.05.11 17:25:48 +05'30'Document20 pagesDigitally Signed by VIVEK Pritamlal Raizada Date: 2020.05.11 17:25:48 +05'30'DIPAN BISWASNo ratings yet

- Annual Report of Info Edge by Icici SecurityDocument12 pagesAnnual Report of Info Edge by Icici SecurityGobind yNo ratings yet

- GSK PharmaDocument10 pagesGSK PharmaSasidharan Sajeev ChathathuNo ratings yet

- SP Apparels 3QFY24 PresentationDocument46 pagesSP Apparels 3QFY24 PresentationAnand SrinivasanNo ratings yet

- Reliance Industries: CMP: INR1,077 TP: INR1,057 (-2%)Document18 pagesReliance Industries: CMP: INR1,077 TP: INR1,057 (-2%)Abhiroop DasNo ratings yet

- S Chand and Company (SCHAND IN) : Q4FY20 Result UpdateDocument6 pagesS Chand and Company (SCHAND IN) : Q4FY20 Result UpdateRaj PrakashNo ratings yet

- Ultratech Cement: CMP: Inr6,485 TP: Inr8,050 (+24%) Market Share Gains Con Nue BuyDocument10 pagesUltratech Cement: CMP: Inr6,485 TP: Inr8,050 (+24%) Market Share Gains Con Nue BuyLive NIftyNo ratings yet

- Investor Presentation (Company Update)Document24 pagesInvestor Presentation (Company Update)Shyam SunderNo ratings yet

- Equity Research Report On Titan Company LTDDocument10 pagesEquity Research Report On Titan Company LTDmundadaharsh1No ratings yet

- S Chand and Company (SCHAND IN) : Q3FY20 Result UpdateDocument6 pagesS Chand and Company (SCHAND IN) : Q3FY20 Result UpdateanjugaduNo ratings yet

- REPCO - RR - 14022024 14 February 2024 1923849091Document17 pagesREPCO - RR - 14022024 14 February 2024 1923849091Sanjeedeep Mishra , 315No ratings yet

- Trent 10 08 2023 IscDocument7 pagesTrent 10 08 2023 Iscaghosh704No ratings yet

- TVS Motor - 1QFY20 Result - JM FinancialDocument8 pagesTVS Motor - 1QFY20 Result - JM FinancialdarshanmadeNo ratings yet

- Jubilant Life Sciences: CMP: INR596 TP: INR800 (+34%)Document10 pagesJubilant Life Sciences: CMP: INR596 TP: INR800 (+34%)Shashanka HollaNo ratings yet

- Princpip 11 8 23 PLDocument6 pagesPrincpip 11 8 23 PLAnubhi Garg374No ratings yet

- Tata Motors Consolidated Q2 FY21 Results: EBIT Breakeven and Positive Free Cash Flows Delivered in The QuarterDocument4 pagesTata Motors Consolidated Q2 FY21 Results: EBIT Breakeven and Positive Free Cash Flows Delivered in The QuarterEsha ChaudharyNo ratings yet

- V Guard Industries Q3 FY22 Results PresentationDocument17 pagesV Guard Industries Q3 FY22 Results PresentationRATHINo ratings yet

- Initiating Coverage - Trident LTD - 311020Document21 pagesInitiating Coverage - Trident LTD - 311020V KeshavdevNo ratings yet

- Wipro: CMP: INR243 TP: INR260 (+7%) Largely in Line Lower ETR Drives A Beat in ProfitabilityDocument14 pagesWipro: CMP: INR243 TP: INR260 (+7%) Largely in Line Lower ETR Drives A Beat in ProfitabilityPramod KulkarniNo ratings yet

- Maruti Suzuki India: Muted Quarter Volume Trough Seemingly in SightDocument12 pagesMaruti Suzuki India: Muted Quarter Volume Trough Seemingly in SightDushyant ChaturvediNo ratings yet

- Press 15jun20Document4 pagesPress 15jun20Rama MadhuNo ratings yet

- V Guard Industries Q4 Results PresentationDocument23 pagesV Guard Industries Q4 Results PresentationIlyasNo ratings yet

- Gulf Oil Lubricants: Stable Performance..Document8 pagesGulf Oil Lubricants: Stable Performance..Doshi VaibhavNo ratings yet

- Bharat Forge: Performance HighlightsDocument13 pagesBharat Forge: Performance HighlightsarikuldeepNo ratings yet

- Economic Indicators for South and Central Asia: Input–Output TablesFrom EverandEconomic Indicators for South and Central Asia: Input–Output TablesNo ratings yet

- Chapter 6 Financial AssetsDocument6 pagesChapter 6 Financial AssetsJoyce Mae D. FloresNo ratings yet

- Problem 31 1Document3 pagesProblem 31 1CodeSeeker100% (1)

- Taxation Law 1 - Mijares SyllabusDocument11 pagesTaxation Law 1 - Mijares SyllabusAngelo Tiglao100% (1)

- Consent To Short Notice of An Annual General MeetingDocument1 pageConsent To Short Notice of An Annual General MeetingKenny NguyenNo ratings yet

- Escrow Agreement With InterestDocument5 pagesEscrow Agreement With InterestpaulmercadoNo ratings yet

- Delisting Checklist PDFDocument4 pagesDelisting Checklist PDFsnjv2621No ratings yet

- Metroplex Berhad Vs Sinophil, GR 208281, June 28, 2021Document31 pagesMetroplex Berhad Vs Sinophil, GR 208281, June 28, 2021Catherine Dimailig0% (4)

- VII ADocument17 pagesVII AtudosecristinaNo ratings yet

- The System Building BlueprintDocument8 pagesThe System Building Blueprintstormin64No ratings yet

- Bonds ValuationsDocument57 pagesBonds ValuationsarmailgmNo ratings yet

- CIG Limba Engleza 2Document54 pagesCIG Limba Engleza 2Carmen BusteaNo ratings yet

- Chapter 15 PartnershipDocument56 pagesChapter 15 PartnershipNurullita KartikaNo ratings yet

- Iqra University: TO Business Finance / Finance FOR ManagersDocument9 pagesIqra University: TO Business Finance / Finance FOR ManagersKanwal NaazNo ratings yet

- MBA4013 Management of Banking andDocument7 pagesMBA4013 Management of Banking andNurfaiqah AmniNo ratings yet

- Thermo Fisher To Acquire Life Technologies IR PresentationDocument13 pagesThermo Fisher To Acquire Life Technologies IR PresentationTariq MotiwalaNo ratings yet

- Theories of Exchange RateDocument37 pagesTheories of Exchange Ratedranita@yahoo.comNo ratings yet

- 20.2 Letter of Intent To Purchase A BusinessDocument5 pages20.2 Letter of Intent To Purchase A BusinessPeeve Kaye BalbuenaNo ratings yet

- Risk Management Summary: Calpers Trust Level ReviewDocument9 pagesRisk Management Summary: Calpers Trust Level ReviewOluwaloseyi SekoniNo ratings yet

- Mark Plan and Examiner'S Commentary: General CommentsDocument9 pagesMark Plan and Examiner'S Commentary: General Commentscima2k15100% (1)

- VALUATION by Reynaldo NogralesDocument29 pagesVALUATION by Reynaldo NogralesresiajhiNo ratings yet

- Rev CTA 8835 8790 Chevron Holdings Inc vs. CIRDocument20 pagesRev CTA 8835 8790 Chevron Holdings Inc vs. CIRJerome Delos ReyesNo ratings yet

- Ford Motor CompanyDocument5 pagesFord Motor CompanyFaria CHNo ratings yet

- Godrej Financial AnalysisDocument16 pagesGodrej Financial AnalysisVaibhav Jain100% (1)

- Amit Kumar Share KhanDocument77 pagesAmit Kumar Share KhanRohit GanjooNo ratings yet

- BRACEY - William FP - Profile 21042016 v2 3 1 PDFDocument1 pageBRACEY - William FP - Profile 21042016 v2 3 1 PDFVivek GhosalNo ratings yet

- Chapter 8Document5 pagesChapter 8Fahad UmarNo ratings yet

- Moody's FrameworkDocument30 pagesMoody's FrameworkbulbNo ratings yet