Download as pdf or txt

You might also like

- Assignment # 3 - Solution PDFDocument7 pagesAssignment # 3 - Solution PDFMUHAMMAD ZEESHAN TARIQNo ratings yet

- UntitledDocument26 pagesUntitledanandpandatNo ratings yet

- Interested Parties Needs ExpectationsDocument4 pagesInterested Parties Needs Expectationsvishvendan100% (8)

- Business Analysis Planning and Monitoring: H0NL60M4 - Business-Analyst-Plan - Mmap - 17/10/2011 - MindjetDocument1 pageBusiness Analysis Planning and Monitoring: H0NL60M4 - Business-Analyst-Plan - Mmap - 17/10/2011 - MindjetnhungNo ratings yet

- Gap AnalysisDocument11 pagesGap AnalysisMurugesh Balaguru100% (1)

- Incred AIFDocument20 pagesIncred AIFvarunNo ratings yet

- FishbaumDocument25 pagesFishbaumZaman HaiderNo ratings yet

- New Product Development Process PDFDocument31 pagesNew Product Development Process PDFcanhizNo ratings yet

- Wallfort - 29 April 2022Document24 pagesWallfort - 29 April 2022Utsav LapsiwalaNo ratings yet

- Seya-Industries-Result-Presentation - Q1FY201 Seya IndustriesDocument24 pagesSeya-Industries-Result-Presentation - Q1FY201 Seya Industriesabhishek kalbaliaNo ratings yet

- E2G Risk Based Inspection Brochure PDFDocument6 pagesE2G Risk Based Inspection Brochure PDFleepondiffNo ratings yet

- Class: Sem: Subject: Cost Accounting Subject Code: Q.NoDocument6 pagesClass: Sem: Subject: Cost Accounting Subject Code: Q.NoDivyeshNo ratings yet

- SMART - Competitive AnalysisDocument13 pagesSMART - Competitive AnalysisJay PonsaranNo ratings yet

- Growth StrategiesDocument28 pagesGrowth Strategieshitek6No ratings yet

- Asiatic Laboratories Limited - IPO AnalyticsDocument4 pagesAsiatic Laboratories Limited - IPO AnalyticsAbdullah Mohammed ArifNo ratings yet

- Capital Market Presentation 03 2019 NKn9QBGSfDocument39 pagesCapital Market Presentation 03 2019 NKn9QBGSfMuhammad Affan UsmaniNo ratings yet

- 05 Performance ChemicalsDocument10 pages05 Performance ChemicalsMarcos De Castro OsórioNo ratings yet

- Introduction To CarvanaDocument28 pagesIntroduction To CarvanaOleksandr YaroshenkoNo ratings yet

- Marketing Planning ToolsDocument13 pagesMarketing Planning ToolsFATHIMA FATHIMANo ratings yet

- Credit Rating Rationale in The Distillers Industry: The Case of Brown-Forman and DiageoDocument18 pagesCredit Rating Rationale in The Distillers Industry: The Case of Brown-Forman and DiageokokoNo ratings yet

- Tanla Investor Update Q2 FY23Document37 pagesTanla Investor Update Q2 FY23hakim shaikhNo ratings yet

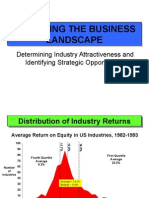

- Analyzing The Business LandscapeDocument18 pagesAnalyzing The Business Landscapedanic13No ratings yet

- CFA Investment Research Challenge University of BahrainDocument32 pagesCFA Investment Research Challenge University of BahrainMuhammad Hamza RizwanNo ratings yet

- Gap Analysis: Presented by You ExecDocument11 pagesGap Analysis: Presented by You ExecJuan Gómez100% (1)

- PP B3 Singapore NUSDocument164 pagesPP B3 Singapore NUSAchmad Rifaie de JongNo ratings yet

- Technology Consulting - by SlidesgoDocument7 pagesTechnology Consulting - by Slidesgokriti.u24No ratings yet

- Aqsa TechDocument5 pagesAqsa TechDua jumaniNo ratings yet

- Project PaotoongDocument167 pagesProject Paotoongpatchayar9557No ratings yet

- Break Even FormulaDocument8 pagesBreak Even FormulaYuval AlfiNo ratings yet

- You Exec - Innovation and Transformation Tools FreeDocument11 pagesYou Exec - Innovation and Transformation Tools FreeEnrique ArinNo ratings yet

- Ledermna 2010Document148 pagesLedermna 2010L Laura Bernal HernándezNo ratings yet

- Webinar Monitorando o Futuro Com Indicadores de Risco e Compliance - Risk LeapDocument51 pagesWebinar Monitorando o Futuro Com Indicadores de Risco e Compliance - Risk LeapEmerson PintoNo ratings yet

- ProfitabilityDocument63 pagesProfitabilityAaron StoneNo ratings yet

- BADRI UAE Listed Insurance Companies Performance Analysis Q1 2022Document20 pagesBADRI UAE Listed Insurance Companies Performance Analysis Q1 2022Sandeep MazzariNo ratings yet

- CFA Institute Research Challenge: Atlanta, GA - Americas Competition Canisius College Buffalo, NYDocument23 pagesCFA Institute Research Challenge: Atlanta, GA - Americas Competition Canisius College Buffalo, NYMihir JoshiNo ratings yet

- Stage Gate: Product Development ModelDocument61 pagesStage Gate: Product Development Modelsandeep devabhaktuniNo ratings yet

- 5baee5df 4235 4aee 930d 13671813b398 Investment Workshop 3 Oilfield ChemicalsDocument40 pages5baee5df 4235 4aee 930d 13671813b398 Investment Workshop 3 Oilfield ChemicalsamitNo ratings yet

- Risk ManagementDocument10 pagesRisk ManagementHomero ReyesNo ratings yet

- Eurex Factsheet - Msci - Index - Dividend - FuturesDocument2 pagesEurex Factsheet - Msci - Index - Dividend - Futures0840328818zNo ratings yet

- Baird 2019 Global Industrial Conference PresentationDocument6 pagesBaird 2019 Global Industrial Conference PresentationValentriniti CCNo ratings yet

- Affle InvestmentAnalysis V2Document14 pagesAffle InvestmentAnalysis V2Soham BansalNo ratings yet

- Risk Appetite in Banking: Steve Townsend Tesco BankDocument15 pagesRisk Appetite in Banking: Steve Townsend Tesco BankrakhalbanglaNo ratings yet

- Riverstone Arohi Stock Pitch PDFDocument17 pagesRiverstone Arohi Stock Pitch PDFKenny ChiaNo ratings yet

- Anti Money LaundryDocument15 pagesAnti Money LaundryacanoNo ratings yet

- Global BusinessDocument38 pagesGlobal BusinessRihab Es SalmiNo ratings yet

- 2018 EXXON Downstream SpotlightDocument39 pages2018 EXXON Downstream Spotlightswaggeroni yololo100% (1)

- Leading The Evolution of Networking and Security: Driving Convergence To Enable Security at Any Network EdgeDocument12 pagesLeading The Evolution of Networking and Security: Driving Convergence To Enable Security at Any Network EdgeNhan PhanNo ratings yet

- IP and Finance - Accounting and Valuation of IP Assets and IP-based FinancingDocument27 pagesIP and Finance - Accounting and Valuation of IP Assets and IP-based FinancinglizanthusNo ratings yet

- Task 2Document2 pagesTask 2ChiroIsLiveNo ratings yet

- UTI Aggressive Hybrid Fund (Formerly UTI Hybrid Equity Fund)Document28 pagesUTI Aggressive Hybrid Fund (Formerly UTI Hybrid Equity Fund)rinkuparekh13No ratings yet

- ENV Envestnet Investor Presentation Draft 2018-01-09Document25 pagesENV Envestnet Investor Presentation Draft 2018-01-09Ala BasterNo ratings yet

- SGAP Presentation MKT and Liquidity Risk ManagementDocument15 pagesSGAP Presentation MKT and Liquidity Risk ManagementDavid IbironkeNo ratings yet

- DQ Labs Chainlake - Light BackgroundDocument2 pagesDQ Labs Chainlake - Light BackgroundMajid KhanNo ratings yet

- The WACC User's Guide: SSRN Electronic Journal April 2005Document25 pagesThe WACC User's Guide: SSRN Electronic Journal April 2005Sumantha SahaNo ratings yet

- The Fortinet Security Fabric: Broad Integrated AutomatedDocument12 pagesThe Fortinet Security Fabric: Broad Integrated AutomatedMUMNo ratings yet

- Introduction To Supply ChainDocument37 pagesIntroduction To Supply ChainnikhilNo ratings yet

- Motilal Oswal PMS PortfolioDocument25 pagesMotilal Oswal PMS PortfolioHetanshNo ratings yet

- Hexaware ReviewDocument9 pagesHexaware ReviewShrinivas PuliNo ratings yet

- FrameworksDocument13 pagesFrameworksShonit ChamadiaNo ratings yet

- SUBEXLTD 28102021225228 InvestorPresentationDocument30 pagesSUBEXLTD 28102021225228 InvestorPresentationleoharshadNo ratings yet

- Digital Category Segmentation TemplateDocument14 pagesDigital Category Segmentation Templatechsanchez1965No ratings yet

- Fair Lending Compliance: Intelligence and Implications for Credit Risk ManagementFrom EverandFair Lending Compliance: Intelligence and Implications for Credit Risk ManagementNo ratings yet

- 2025 수능특강 1강 변형문제 (1회) (30) (단지) (이게 찐자 변형문제이다)Document7 pages2025 수능특강 1강 변형문제 (1회) (30) (단지) (이게 찐자 변형문제이다)신주영No ratings yet

- Sabah Homebuyer MagazineDocument40 pagesSabah Homebuyer MagazinetshunweiNo ratings yet

- Practicalweek48 0809answersDocument8 pagesPracticalweek48 0809answersLaura BasalicNo ratings yet

- Statement Date No. of MonthsDocument6 pagesStatement Date No. of MonthscallvkNo ratings yet

- Lincoln Financial GroupDocument3 pagesLincoln Financial GroupAbhinavSatijaNo ratings yet

- RCC13 Punching ShearDocument11 pagesRCC13 Punching ShearMUTHUKKUMARAMNo ratings yet

- A Guide To The PMD ProDocument146 pagesA Guide To The PMD Proاسماعيل نعمانNo ratings yet

- Reflective Essay Final 1Document4 pagesReflective Essay Final 1Shalini JuteramNo ratings yet

- SM PresentationDocument16 pagesSM PresentationDhruvi MinotraNo ratings yet

- Chapter Eight:: Trade Restrictions: TariffsDocument23 pagesChapter Eight:: Trade Restrictions: Tariffsaffanahmed111No ratings yet

- Cfi SiloDocument4 pagesCfi SiloSyed KhalilNo ratings yet

- Declaration: I AKASH RUHELA A Student of MBA IV Semester of SRM University, NCR CampusDocument81 pagesDeclaration: I AKASH RUHELA A Student of MBA IV Semester of SRM University, NCR Campuslokesh_045No ratings yet

- Employees Old-Age Benefits InstitutionDocument10 pagesEmployees Old-Age Benefits InstitutionNasrullah ShahNo ratings yet

- Full Download Test Bank For International Management 8th Edition Fred Luthans PDF Full ChapterDocument36 pagesFull Download Test Bank For International Management 8th Edition Fred Luthans PDF Full Chapterrusmaactinalf9bf5j100% (21)

- Chapter No.53psDocument5 pagesChapter No.53psKamal SinghNo ratings yet

- Spouses Yu vs. PaclebDocument1 pageSpouses Yu vs. Paclebscartoneros_1No ratings yet

- Chklist I49q057v87 05s0lgavn 1 49s12cu0hDocument5 pagesChklist I49q057v87 05s0lgavn 1 49s12cu0hashwin_rasquinha@yahoo.comNo ratings yet

- Film FinancingDocument45 pagesFilm FinancingKuldeep BatraNo ratings yet

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)TuhinNo ratings yet

- OBS 124 Unit 2 - Manager As Planner and Strategist - Final 2023Document40 pagesOBS 124 Unit 2 - Manager As Planner and Strategist - Final 2023Lungelo Maphumulo100% (1)

- Account Override On Subledger JournalsDocument12 pagesAccount Override On Subledger JournalsKishore RavichandranNo ratings yet

- PMP Certification Practice Exam1Document18 pagesPMP Certification Practice Exam1MSK2112100% (1)

- Business Plan: Naga View Adventist College, Inc. Zone 2, Panicuason Naga City, BicolDocument8 pagesBusiness Plan: Naga View Adventist College, Inc. Zone 2, Panicuason Naga City, BicolKier Jhoem Saludar MahusayNo ratings yet

- Treasury Report TransnetDocument273 pagesTreasury Report TransnetPrimedia Broadcasting100% (4)

- Formulasi Strategi Bisnis Perusahaan Original Equipment Manufacturer (OEM) Studi Kasus Di PT XYZDocument12 pagesFormulasi Strategi Bisnis Perusahaan Original Equipment Manufacturer (OEM) Studi Kasus Di PT XYZsopingiNo ratings yet

- Lumax Auto Q1 FY18 PresentationDocument48 pagesLumax Auto Q1 FY18 PresentationshahavNo ratings yet

- As 4180.2-2008 Measurement of Drift Loss From Cooling Towers Lost Chloride MethodDocument8 pagesAs 4180.2-2008 Measurement of Drift Loss From Cooling Towers Lost Chloride MethodSAI Global - APACNo ratings yet