Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5823)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Final Business Plan For Quarrying and Aggregate PlantDocument46 pagesFinal Business Plan For Quarrying and Aggregate PlantTedros AbrehamNo ratings yet

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Dillons Rule - Should It Stay or Should It GoDocument34 pagesDillons Rule - Should It Stay or Should It GoProgressAndMainNo ratings yet

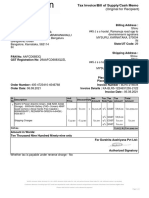

- Tax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Document1 pageTax Invoice/Bill of Supply/Cash Memo: (Original For Recipient)Shiva Kumar0% (1)

- Right To Be InformedDocument3 pagesRight To Be InformedAmy Lou CabayaoNo ratings yet

- Republic Act 9208 or The Anti-Trafficking in PersonsDocument23 pagesRepublic Act 9208 or The Anti-Trafficking in PersonsAmy Lou Cabayao50% (2)

- Crim 2 #12 Nostradamus Villanueva Petitioner, vs. Priscilla R. DomingoDocument2 pagesCrim 2 #12 Nostradamus Villanueva Petitioner, vs. Priscilla R. DomingoAmy Lou CabayaoNo ratings yet

- People v1Document5 pagesPeople v1Amy Lou CabayaoNo ratings yet

- Militarizarization of ALCADEV Lumad SchoolsDocument3 pagesMilitarizarization of ALCADEV Lumad SchoolsAmy Lou CabayaoNo ratings yet

- Section 10Document3 pagesSection 10Amy Lou CabayaoNo ratings yet

- Crim 2 #02 Dr. Jarcia, Jr. and Dr. Bastan Vs People, GR No. 187926 Reckless Imprudence ArtajoDocument13 pagesCrim 2 #02 Dr. Jarcia, Jr. and Dr. Bastan Vs People, GR No. 187926 Reckless Imprudence ArtajoAmy Lou Cabayao100% (1)

- Right To BailDocument13 pagesRight To BailAmy Lou CabayaoNo ratings yet

- Legal Technique and Logic Prelims Reviewer - Part I ADocument13 pagesLegal Technique and Logic Prelims Reviewer - Part I AAmy Lou Cabayao100% (1)

- Void or Inexistent ContractsDocument7 pagesVoid or Inexistent ContractsAmy Lou CabayaoNo ratings yet

- Sec 8Document3 pagesSec 8Amy Lou CabayaoNo ratings yet

- Right To Form AssociationDocument6 pagesRight To Form AssociationAmy Lou CabayaoNo ratings yet

- The Following Contracts Are Voidable or Annullable, Even Though There May Have Been No Damage To The Contracting PartiesDocument9 pagesThe Following Contracts Are Voidable or Annullable, Even Though There May Have Been No Damage To The Contracting PartiesAmy Lou Cabayao100% (1)

- Freedom of Expressio1Document13 pagesFreedom of Expressio1Amy Lou CabayaoNo ratings yet

- Right To InformationDocument13 pagesRight To InformationAmy Lou CabayaoNo ratings yet

- Facts:Petitioner Winston Garcia (PGM Garcia), As President and General Manager of The GSIS, FiledDocument3 pagesFacts:Petitioner Winston Garcia (PGM Garcia), As President and General Manager of The GSIS, FiledAmy Lou CabayaoNo ratings yet

- Signed by Pres. Aquino: Biraogo vs. PTC of 2010Document5 pagesSigned by Pres. Aquino: Biraogo vs. PTC of 2010Amy Lou CabayaoNo ratings yet

- Facts:: Equal Protection Clause 20b.) Republic vs. Daisy Yahon (2014)Document2 pagesFacts:: Equal Protection Clause 20b.) Republic vs. Daisy Yahon (2014)Amy Lou CabayaoNo ratings yet

- Multiple Choice: Auditing & Assurance Principles AT.113-Code of Ethics - Part II Nu Sports AcademyDocument7 pagesMultiple Choice: Auditing & Assurance Principles AT.113-Code of Ethics - Part II Nu Sports AcademyPatrickMendozaNo ratings yet

- Assignment No. 1 - The Budget ProcessDocument4 pagesAssignment No. 1 - The Budget ProcessCindy Faye CrusanteNo ratings yet

- Fishwealth Canning Corporation Vs CirDocument2 pagesFishwealth Canning Corporation Vs CirKateBarrionEspinosaNo ratings yet

- Tax Certificate: R MargabandhuDocument2 pagesTax Certificate: R MargabandhuHAJARATHNo ratings yet

- Sesa Kifle Ketema Practical AttachmentDocument14 pagesSesa Kifle Ketema Practical AttachmentTesfahun Abye100% (1)

- Handbook Setting Up Your Business in Flanders Update Jan 2018Document44 pagesHandbook Setting Up Your Business in Flanders Update Jan 2018Harish KumarNo ratings yet

- Appraisal and Assessment in Government SectorDocument2 pagesAppraisal and Assessment in Government SectorluxasuhiNo ratings yet

- Train Law PowerpointDocument82 pagesTrain Law PowerpointPaula May80% (5)

- Acc 421 JanDocument42 pagesAcc 421 JanMay ChenNo ratings yet

- Computation of Gross IncomeDocument10 pagesComputation of Gross IncomemysterymieNo ratings yet

- Strategic Management 4 - ScribdDocument18 pagesStrategic Management 4 - ScribdYour TutorNo ratings yet

- Original Petition - Gamboa v. TWIADocument113 pagesOriginal Petition - Gamboa v. TWIATWIAcaseNo ratings yet

- Construction Equipment SelectionDocument38 pagesConstruction Equipment SelectionPrasannaVenkatesan100% (1)

- What Is SAP R/3?Document35 pagesWhat Is SAP R/3?jitinmangla970No ratings yet

- C APPROVED BUDGET FOR THE CONTRACTDocument1 pageC APPROVED BUDGET FOR THE CONTRACTalfredo taguianNo ratings yet

- CIR Vs British AirwaysDocument4 pagesCIR Vs British Airwaysermeline tampusNo ratings yet

- RBI Preparation StrategyDocument21 pagesRBI Preparation StrategybinayNo ratings yet

- 840 Diansay V. National Development Company, GR L-13667, April 29,1960 (Per J. C.J. Paras, en Banc)Document9 pages840 Diansay V. National Development Company, GR L-13667, April 29,1960 (Per J. C.J. Paras, en Banc)Steve UyNo ratings yet

- Water Flow MeterDocument1 pageWater Flow MeterKali CharanNo ratings yet

- Value Added TaxDocument38 pagesValue Added TaxAhmad AbduljalilNo ratings yet

- Bir Tax Computation: Fill Up The Boxes With Fill Up Details WithDocument37 pagesBir Tax Computation: Fill Up The Boxes With Fill Up Details WithjessiecaNo ratings yet

- Module 2 Quiz Minglana Mitch TDocument4 pagesModule 2 Quiz Minglana Mitch TMitch Tokong MinglanaNo ratings yet

- PRSI Calculation and ClassesDocument17 pagesPRSI Calculation and ClassesjpdmhrNo ratings yet

- Council Policy: Land DevelopmentDocument4 pagesCouncil Policy: Land Developmentsenthilkumar kNo ratings yet

- MFT Samp Questions BusinessDocument7 pagesMFT Samp Questions BusinessKiều Thảo AnhNo ratings yet

- Modified Purchase Manual: 1.0 IntroductoryDocument40 pagesModified Purchase Manual: 1.0 IntroductoryAbdul Rashid QureshiNo ratings yet

- Tax Alert (December 2020)Document10 pagesTax Alert (December 2020)Rheneir MoraNo ratings yet