Download as rtf, pdf, or txt

You might also like

- Investments in Associates FA AC OverviewDocument85 pagesInvestments in Associates FA AC OverviewHannah Shaira Clemente73% (11)

- 2017 12 31 Thirteen LLC Investment SummaryDocument437 pages2017 12 31 Thirteen LLC Investment SummaryLarryDCurtis100% (2)

- Corporate Governance in UgandaDocument42 pagesCorporate Governance in UgandaXavier Francis S. LutaloNo ratings yet

- Manual of Regulations For BanksDocument840 pagesManual of Regulations For Banksdyosangpinagpala100% (5)

- GEF Case 2Document6 pagesGEF Case 2gabrielaNo ratings yet

- O Ves S R e S o S Is S I e S, Sses, S Ts S, I - . S S A: Professional ResponsibilitiesDocument2 pagesO Ves S R e S o S Is S I e S, Sses, S Ts S, I - . S S A: Professional ResponsibilitiesZeyad El-sayedNo ratings yet

- 74713bos60485 Inter p1 cp10 U2Document24 pages74713bos60485 Inter p1 cp10 U2Gurusaran SNo ratings yet

- Loan Function of BanksDocument4 pagesLoan Function of BanksSherlyn Paran Paquit-SeldaNo ratings yet

- Scan 0009Document2 pagesScan 0009Zeyad El-sayedNo ratings yet

- LLC Operating AgreementDocument13 pagesLLC Operating AgreementSucreNo ratings yet

- Independent DirectorsDocument3 pagesIndependent DirectorsadityadesaiNo ratings yet

- CH 02 - Business, Trade - Commecer AkDocument17 pagesCH 02 - Business, Trade - Commecer AkArundhoti MukherjeeNo ratings yet

- Introduction To Independence and GIP - Jan 2011Document16 pagesIntroduction To Independence and GIP - Jan 2011Praveen MalineniNo ratings yet

- Professional EthicsDocument51 pagesProfessional EthicsFremaNo ratings yet

- Neral Features of Business Forms in Vietnam - ENT LawDocument5 pagesNeral Features of Business Forms in Vietnam - ENT LawPassionNo ratings yet

- Investment in AssociatesDocument47 pagesInvestment in AssociatesHimanshu GaurNo ratings yet

- 52465bos42065final p1 cp1 U5 PDFDocument14 pages52465bos42065final p1 cp1 U5 PDFRAHUL PRASADNo ratings yet

- Duties of DirectorsDocument3 pagesDuties of DirectorsfaracgehNo ratings yet

- Jan 162022 BRPD 01 eDocument7 pagesJan 162022 BRPD 01 epk ghoshNo ratings yet

- Module 8 PAS 27 & 28Document4 pagesModule 8 PAS 27 & 28Jan JanNo ratings yet

- As 18Document13 pagesAs 18Knowledge GuruNo ratings yet

- CH 02 - Business, Trade - Commecer AkDocument13 pagesCH 02 - Business, Trade - Commecer AkArundhoti MukherjeeNo ratings yet

- Code of Business Ethics Policy GuidelinesDocument8 pagesCode of Business Ethics Policy GuidelinesowenNo ratings yet

- The Duty of Loyalty From Directors, Partners and Senior Employees - Gaby Hardwicke SolicitorsDocument17 pagesThe Duty of Loyalty From Directors, Partners and Senior Employees - Gaby Hardwicke SolicitorsAndres RestrepoNo ratings yet

- Dwnload Full Principles of Auditing Other Assurance Services 19th Edition Whittington Solutions Manual PDFDocument36 pagesDwnload Full Principles of Auditing Other Assurance Services 19th Edition Whittington Solutions Manual PDFtobijayammev100% (10)

- Full Download Principles of Auditing Other Assurance Services 19th Edition Whittington Solutions ManualDocument36 pagesFull Download Principles of Auditing Other Assurance Services 19th Edition Whittington Solutions Manualjamesturnerzdc100% (34)

- Ac Standard - AS18Document8 pagesAc Standard - AS18api-3705877No ratings yet

- The Risks and Rewards of Multiple Lender FinancingsDocument5 pagesThe Risks and Rewards of Multiple Lender Financingsjude loh wai sengNo ratings yet

- CorpoRev - Jan 8 Part 3 - EmuyDocument4 pagesCorpoRev - Jan 8 Part 3 - EmuyHannah Keziah Dela CernaNo ratings yet

- Ugbs Accounting For Investment in Associate and Joint VentureDocument30 pagesUgbs Accounting For Investment in Associate and Joint VentureStudy GirlNo ratings yet

- Connected LendingDocument5 pagesConnected Lending22satendraNo ratings yet

- Presentation Slide PDFDocument10 pagesPresentation Slide PDFIsa BorodoNo ratings yet

- Watered StocksDocument10 pagesWatered StocksBruno GalwatNo ratings yet

- Single Borrowers LimitDocument10 pagesSingle Borrowers LimitCamille LamadoNo ratings yet

- Suitability of PersonsDocument20 pagesSuitability of Personsjaphethmm01No ratings yet

- New Operating AgreementDocument16 pagesNew Operating AgreementMichaelAllenCrainNo ratings yet

- Cbactg01 Chapter 5 ModuleDocument7 pagesCbactg01 Chapter 5 ModuleJohn DavisNo ratings yet

- Geeta Saar 107 Auditor Not To Render Certain ServicesDocument7 pagesGeeta Saar 107 Auditor Not To Render Certain Servicesvaibhavayush994No ratings yet

- Consolidated Financial Statements - 2. DefinitionsDocument3 pagesConsolidated Financial Statements - 2. DefinitionsshubhamNo ratings yet

- Review Questions: Click On The Questions To See AnswersDocument10 pagesReview Questions: Click On The Questions To See AnswersJinjer Ann LanticanNo ratings yet

- FAR.112 - INVESTMENT IN ASSOCIATES AND JOINT VENTURES With AnswerDocument6 pagesFAR.112 - INVESTMENT IN ASSOCIATES AND JOINT VENTURES With AnswerMaeNo ratings yet

- SECTION 185 of Companies ActDocument5 pagesSECTION 185 of Companies Actimmaestro.9999No ratings yet

- To Consolidated Financial Statements: Syllabus Guide Detailed OutcomesDocument51 pagesTo Consolidated Financial Statements: Syllabus Guide Detailed OutcomesDavid MorganNo ratings yet

- Users of Financial InformationDocument2 pagesUsers of Financial InformationmingmingpspspspsNo ratings yet

- Related Party Disclosures: International Accounting Standard 24Document5 pagesRelated Party Disclosures: International Accounting Standard 24FateNo ratings yet

- Directors Duties 24sept20Document2 pagesDirectors Duties 24sept20Visakh AntonyNo ratings yet

- Pas 28Document16 pagesPas 28abeladelmundosuarezNo ratings yet

- Module2 L1elec4Document15 pagesModule2 L1elec4Cheryvel GalleonNo ratings yet

- Duty of Care and Skill of Company DirectorsDocument7 pagesDuty of Care and Skill of Company Directorsarchit malhotra100% (2)

- Topic 9 - Corporate Finance and Capital ControlDocument7 pagesTopic 9 - Corporate Finance and Capital Controllebogang mkansiNo ratings yet

- LLC Operating AgreementDocument7 pagesLLC Operating AgreementEddi Jónsson100% (1)

- The State Bank of Vietnam Socialist Republic of Viet Nam Independence - Freedom - HappinessDocument17 pagesThe State Bank of Vietnam Socialist Republic of Viet Nam Independence - Freedom - HappinessFx121No ratings yet

- INDAS28 - Consolidation For Associates PDFDocument12 pagesINDAS28 - Consolidation For Associates PDFKedarNo ratings yet

- CH 22Document8 pagesCH 22laiveNo ratings yet

- PFRS 10Document13 pagesPFRS 10lovekath09No ratings yet

- Suntrust Banks, Inc. Corporate Governance GuidelinesDocument9 pagesSuntrust Banks, Inc. Corporate Governance GuidelinesPetruța MarianNo ratings yet

- Duties and Responsibilities of Independent DirectorDocument4 pagesDuties and Responsibilities of Independent DirectorsamNo ratings yet

- Pas 28Document4 pagesPas 28iyahvrezNo ratings yet

- Haroon Tabrez Haroon Tabrez Haroon Tabrez Haroon Tabrez: Paper P1Document49 pagesHaroon Tabrez Haroon Tabrez Haroon Tabrez Haroon Tabrez: Paper P1Mohsin ZafarNo ratings yet

- Debenture Trustee: What Is A Debenture?Document11 pagesDebenture Trustee: What Is A Debenture?Shalvin SharmaNo ratings yet

- Policy On Loans To Directors and Senior OffcialsDocument8 pagesPolicy On Loans To Directors and Senior OffcialssagarthegameNo ratings yet

- Fede Al Securities Acts: OvervieDocument2 pagesFede Al Securities Acts: OvervieZeyad El-sayedNo ratings yet

- Scan 0001Document2 pagesScan 0001Zeyad El-sayedNo ratings yet

- Deduct From Book Income: - B - T F Dul - .Document2 pagesDeduct From Book Income: - B - T F Dul - .Zeyad El-sayedNo ratings yet

- Scan 0001Document2 pagesScan 0001Zeyad El-sayedNo ratings yet

- Se Tion 1244 Small Business Corporation (SBC) Stock Ordinary LossDocument3 pagesSe Tion 1244 Small Business Corporation (SBC) Stock Ordinary LossZeyad El-sayedNo ratings yet

- Scan 0013Document2 pagesScan 0013Zeyad El-sayedNo ratings yet

- P N 0 TH H T - T o H T: Module 36 Taxes: Co O ATEDocument3 pagesP N 0 TH H T - T o H T: Module 36 Taxes: Co O ATEZeyad El-sayedNo ratings yet

- S Y, S Ys) - Ss - ' S: Module 36 Taxes: CorporateDocument3 pagesS Y, S Ys) - Ss - ' S: Module 36 Taxes: CorporateZeyad El-sayedNo ratings yet

- I y I - D - S I - (E o - T, L: Module 36 Taxes: CorporateDocument2 pagesI y I - D - S I - (E o - T, L: Module 36 Taxes: CorporateZeyad El-sayedNo ratings yet

- Module 36 Taxes: Corporate:, - S, V e C, - ,, % S 'Document2 pagesModule 36 Taxes: Corporate:, - S, V e C, - ,, % S 'Zeyad El-sayedNo ratings yet

- Scan 0010Document3 pagesScan 0010Zeyad El-sayedNo ratings yet

- 80 de Cei Du T o D P A e ST Li D T BL N: Module 36 Taxes: CorporateDocument2 pages80 de Cei Du T o D P A e ST Li D T BL N: Module 36 Taxes: CorporateZeyad El-sayedNo ratings yet

- Module 36 Taxes: Corporate:: C % Es C, E, E, We, %, C, O, W e e G, Z C C e S V e C C S C ZDocument2 pagesModule 36 Taxes: Corporate:: C % Es C, E, E, We, %, C, O, W e e G, Z C C e S V e C C S C ZZeyad El-sayedNo ratings yet

- B Nkruptcy: Discharge of A BankruptDocument2 pagesB Nkruptcy: Discharge of A BankruptZeyad El-sayedNo ratings yet

- Module 36 Taxes: Corporate: - G, - , - C C,, S, A, I - . Es T, R, CDocument3 pagesModule 36 Taxes: Corporate: - G, - , - C C,, S, A, I - . Es T, R, CZeyad El-sayedNo ratings yet

- Module 21 Professional Responsibilities: Interpretation 101-2. A FirmDocument2 pagesModule 21 Professional Responsibilities: Interpretation 101-2. A FirmZeyad El-sayedNo ratings yet

- Scan 0012Document2 pagesScan 0012Zeyad El-sayedNo ratings yet

- Bankruptcy:: y y S e S Owed SDocument3 pagesBankruptcy:: y y S e S Owed SZeyad El-sayedNo ratings yet

- Revocation of Discharge: 2M Module27 BankruptcyDocument2 pagesRevocation of Discharge: 2M Module27 BankruptcyZeyad El-sayedNo ratings yet

- ET Section 10 01 Conce Tu LF Mework For A Cpa I e Ence StandardsDocument2 pagesET Section 10 01 Conce Tu LF Mework For A Cpa I e Ence StandardsZeyad El-sayedNo ratings yet

- Scan 0008Document2 pagesScan 0008Zeyad El-sayedNo ratings yet

- Scan 0010Document2 pagesScan 0010Zeyad El-sayedNo ratings yet

- Scan 0009Document2 pagesScan 0009Zeyad El-sayedNo ratings yet

- The Bankruptcy Abuse Prevention and Consumer Protection Act of 2005Document2 pagesThe Bankruptcy Abuse Prevention and Consumer Protection Act of 2005Zeyad El-sayedNo ratings yet

- Scan 0018Document1 pageScan 0018Zeyad El-sayedNo ratings yet

- Professional Responsibilities: S S S A o S e C I A o Ir Par S o C Ie To A A State-O,, S Ss y G S, C e S. R I S of AsDocument2 pagesProfessional Responsibilities: S S S A o S e C I A o Ir Par S o C Ie To A A State-O,, S Ss y G S, C e S. R I S of AsZeyad El-sayedNo ratings yet

- Article I Responsibilities. Article Il-The Public InterestDocument2 pagesArticle I Responsibilities. Article Il-The Public InterestZeyad El-sayedNo ratings yet

- Scan 0006Document2 pagesScan 0006Zeyad El-sayedNo ratings yet

- Scan 0008Document2 pagesScan 0008Zeyad El-sayedNo ratings yet

- Scan 0008Document2 pagesScan 0008Zeyad El-sayedNo ratings yet

- Chapter 4 Choosing A Form of Business OwnershipDocument24 pagesChapter 4 Choosing A Form of Business OwnershipPete JoempraditwongNo ratings yet

- Company Law ProjectDocument21 pagesCompany Law ProjectNayanika Bhardwaj50% (2)

- Demerger and Tax On M&aDocument5 pagesDemerger and Tax On M&aChandan SinghNo ratings yet

- Salomon V Salomon - Case SummaryDocument4 pagesSalomon V Salomon - Case SummaryParag KabraNo ratings yet

- Companies Act FoundationDocument36 pagesCompanies Act FoundationrishikeshkallaNo ratings yet

- Public Enterprise in EthiopiaDocument14 pagesPublic Enterprise in EthiopiaAmbachew Motbaynor100% (22)

- All Satellites Receivable inDocument2 pagesAll Satellites Receivable inCE capital BuildersNo ratings yet

- Banking Laws Chapters 19 21Document40 pagesBanking Laws Chapters 19 21john uyNo ratings yet

- Anticipated Endowment AssuranceDocument1 pageAnticipated Endowment AssurancePankaj BeniwalNo ratings yet

- TataDocument8 pagesTataSherry SahaNo ratings yet

- Corporate, Removal of DirectorsDocument16 pagesCorporate, Removal of DirectorsRajatAgrawalNo ratings yet

- Group Reporting I: Concepts and Context: acquisition: hợp nhất merger: sáp nhập associate: liên kếtDocument31 pagesGroup Reporting I: Concepts and Context: acquisition: hợp nhất merger: sáp nhập associate: liên kếtPhạm Ngọc ÁnhNo ratings yet

- QB of Corporate Law & Practice ACE 302 - ACM 603 2018-19Document4 pagesQB of Corporate Law & Practice ACE 302 - ACM 603 2018-19isha NarwarNo ratings yet

- SECP FunctionsDocument13 pagesSECP FunctionsMehwish Murtaza0% (2)

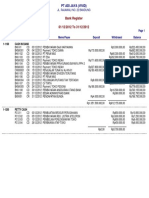

- Bank RegisterDocument1 pageBank RegisterVivid SariNo ratings yet

- Partnership LiquidationDocument13 pagesPartnership LiquidationCjhay MarcosNo ratings yet

- Corporate-Personality EasyDocument4 pagesCorporate-Personality EasyNaim AhmedNo ratings yet

- Risk Management: Case Study On AIGDocument8 pagesRisk Management: Case Study On AIGPatrick ChauNo ratings yet

- What Is BootstrappingDocument3 pagesWhat Is BootstrappingCharu SharmaNo ratings yet

- Week 1 2 Introduction To Forward and Options LMSDocument24 pagesWeek 1 2 Introduction To Forward and Options LMSKastral KokNo ratings yet

- Assignment ON Ifrs1-First Time Adoption of IfrsDocument46 pagesAssignment ON Ifrs1-First Time Adoption of IfrsMohit BansalNo ratings yet

- CSXDocument130 pagesCSXmarcelluxNo ratings yet

- Role of SEBI As Regulator in Maintaining Corporate Governance Standards in IndiaDocument4 pagesRole of SEBI As Regulator in Maintaining Corporate Governance Standards in Indiasourav kumar rayNo ratings yet

- Corporate Finance Chapter 26Document83 pagesCorporate Finance Chapter 26billy930% (1)

- A Study of Open Interest in Nifty Future PDFDocument7 pagesA Study of Open Interest in Nifty Future PDFRaghuraman ThaiyarNo ratings yet

- GRI Year Book 2011Document16 pagesGRI Year Book 2011Global Real Estate InstituteNo ratings yet