Download as pdf or txt

You might also like

- NVDXT ParametersDocument5 pagesNVDXT ParametersStephen Blommestein50% (2)

- Cruz V Valero and Luzon Sugar CompanyDocument2 pagesCruz V Valero and Luzon Sugar CompanyPatricia Gonzaga0% (1)

- Motherson Sumi Systems LTD Excel FinalDocument30 pagesMotherson Sumi Systems LTD Excel Finalwritik sahaNo ratings yet

- Morning Star Report 20171119125636Document2 pagesMorning Star Report 20171119125636wesamNo ratings yet

- QNBFS Daily Market Report - Sept 17Document5 pagesQNBFS Daily Market Report - Sept 17QNBGroupNo ratings yet

- JS Income FundDocument9 pagesJS Income Fundcoolbouy85No ratings yet

- DMR Eng 3Document9 pagesDMR Eng 3faheemmpNo ratings yet

- Trade Performance and Fund Flow Week Ended 9 February 2024-258Document5 pagesTrade Performance and Fund Flow Week Ended 9 February 2024-258Shabandi MnNo ratings yet

- QFR 03-March 2022 LDocument70 pagesQFR 03-March 2022 LNapolean DynamiteNo ratings yet

- Screenshot 2022-07-24 at 9.04.59 PMDocument46 pagesScreenshot 2022-07-24 at 9.04.59 PMieda1718No ratings yet

- A Potential USD 140 BN Industry: Kuwait Financial Centre S.A.K "Markaz"Document19 pagesA Potential USD 140 BN Industry: Kuwait Financial Centre S.A.K "Markaz"Adama KoneNo ratings yet

- KazakhstanDocument13 pagesKazakhstanЛяззат НуртайNo ratings yet

- Muthoot Finance LTD.: Business OverviewDocument5 pagesMuthoot Finance LTD.: Business OverviewAvinash ThakurNo ratings yet

- Markets Ranking - Markets Adspend by Quarter Y2007Document2 pagesMarkets Ranking - Markets Adspend by Quarter Y2007Misk CommunicationNo ratings yet

- August ETF ReportDocument5 pagesAugust ETF ReportzoetechocNo ratings yet

- Mutual FundDocument8 pagesMutual FundMayur khambhatiNo ratings yet

- GCC Markets Monthly Report - June-2023Document10 pagesGCC Markets Monthly Report - June-2023Nirmal MenonNo ratings yet

- PSX Quote 31-08-2022Document42 pagesPSX Quote 31-08-2022wasayrazaNo ratings yet

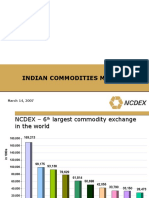

- Indian Commodities Market: March 14, 2007Document40 pagesIndian Commodities Market: March 14, 2007parishkaaNo ratings yet

- Investor Digest: Equity Research - 20 March 2024Document5 pagesInvestor Digest: Equity Research - 20 March 2024brian butarNo ratings yet

- Market Update 26th February 2018Document1 pageMarket Update 26th February 2018Anonymous iFZbkNwNo ratings yet

- Market Technical Reading - Stronger Technical Bull Run Underway! - 15/09/2010Document6 pagesMarket Technical Reading - Stronger Technical Bull Run Underway! - 15/09/2010Rhb InvestNo ratings yet

- Mutual Fund Report Feb-20Document39 pagesMutual Fund Report Feb-20muddasir1980No ratings yet

- Cy 22 Return OpenDocument20 pagesCy 22 Return Openhamadashraf.swhccNo ratings yet

- Taj Hotels Balance Sheet ComparisonDocument3 pagesTaj Hotels Balance Sheet ComparisonjaykumariyerNo ratings yet

- QFR (PRS) March 2022Document20 pagesQFR (PRS) March 2022Napolean DynamiteNo ratings yet

- Commodity Exchanges - Prospects and Emerging Opportunities in IndiaDocument53 pagesCommodity Exchanges - Prospects and Emerging Opportunities in Indianb1920No ratings yet

- Markets and Commodity Figures: 04 July 2017Document4 pagesMarkets and Commodity Figures: 04 July 2017Tiso Blackstar GroupNo ratings yet

- Market Technical Reading - Next Resistance Only at 1,524.69! - 14/09/2010Document6 pagesMarket Technical Reading - Next Resistance Only at 1,524.69! - 14/09/2010Rhb InvestNo ratings yet

- Markets and Commodity Figures: 05 July 2017Document4 pagesMarkets and Commodity Figures: 05 July 2017Tiso Blackstar GroupNo ratings yet

- Markets and Commodity Figures: 06 July 2017Document4 pagesMarkets and Commodity Figures: 06 July 2017Tiso Blackstar GroupNo ratings yet

- WFE Annual Statistics Guide 2015Document296 pagesWFE Annual Statistics Guide 2015smitajNo ratings yet

- Markets and Commodity Figures: 12 March 2017Document4 pagesMarkets and Commodity Figures: 12 March 2017Tiso Blackstar GroupNo ratings yet

- Kenanga Today - 230322 (Kenanga)Document5 pagesKenanga Today - 230322 (Kenanga)hl lowNo ratings yet

- Market Technical Reading: Muted Trading Sentiment Expected - 09/09/2010Document6 pagesMarket Technical Reading: Muted Trading Sentiment Expected - 09/09/2010Rhb InvestNo ratings yet

- Markets and Commodity Figures: 24 July 2017Document4 pagesMarkets and Commodity Figures: 24 July 2017Tiso Blackstar GroupNo ratings yet

- Africa Investor - April 24 2017Document4 pagesAfrica Investor - April 24 2017Tiso Blackstar GroupNo ratings yet

- AfricaInvestor - March 6 2017Document4 pagesAfricaInvestor - March 6 2017Tiso Blackstar GroupNo ratings yet

- Markets and Commodity Figures: 16 July 2017Document4 pagesMarkets and Commodity Figures: 16 July 2017Tiso Blackstar GroupNo ratings yet

- 20th July, 2020Document8 pages20th July, 2020samuel debebeNo ratings yet

- Markets and Commodity Figures: 03 July 2017Document4 pagesMarkets and Commodity Figures: 03 July 2017Tiso Blackstar GroupNo ratings yet

- Africa Investor - July 25 2017Document4 pagesAfrica Investor - July 25 2017Tiso Blackstar GroupNo ratings yet

- Africa InvestorDocument4 pagesAfrica InvestorTiso Blackstar GroupNo ratings yet

- Markets and Commodity Figures: 07 March 2017Document4 pagesMarkets and Commodity Figures: 07 March 2017Tiso Blackstar GroupNo ratings yet

- Derivatives in GCCDocument32 pagesDerivatives in GCCmacocean0% (1)

- AfricaInvestor - March 13 2017Document4 pagesAfricaInvestor - March 13 2017Tiso Blackstar GroupNo ratings yet

- AfricaInvestor - September 11 2017Document4 pagesAfricaInvestor - September 11 2017Tiso Blackstar GroupNo ratings yet

- Earn - World November 2023Document7 pagesEarn - World November 2023isaacngoma2000No ratings yet

- Mutual Fund: MARCH, 2020Document60 pagesMutual Fund: MARCH, 2020RAJ STUDY WIZARDNo ratings yet

- Market Technical Reading - A Penetration of The 10-Day SMA Is Crucial To Trading Sentiment... - 30/09/2010Document6 pagesMarket Technical Reading - A Penetration of The 10-Day SMA Is Crucial To Trading Sentiment... - 30/09/2010Rhb InvestNo ratings yet

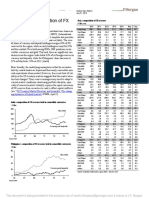

- Asia: Composition of FX ReservesDocument2 pagesAsia: Composition of FX ReservesmuhjaerNo ratings yet

- Property Sector Update: IFRIC 15 Deferred To 2012 - 01/09/2010Document2 pagesProperty Sector Update: IFRIC 15 Deferred To 2012 - 01/09/2010Rhb InvestNo ratings yet

- Markets and Commodity FiguresDocument4 pagesMarkets and Commodity FiguresTiso Blackstar GroupNo ratings yet

- SamplemarketresearchDocument21 pagesSamplemarketresearchBig4 AdsNo ratings yet

- Macro Presentation: Jazira CapitalDocument8 pagesMacro Presentation: Jazira CapitalMohamed FahmyNo ratings yet

- Markets and Commodity FiguresDocument4 pagesMarkets and Commodity FiguresTiso Blackstar GroupNo ratings yet

- Public Shariah MFR August 2021Document47 pagesPublic Shariah MFR August 2021UmmiNo ratings yet

- Markets and Commodity FiguresDocument4 pagesMarkets and Commodity FiguresTiso Blackstar GroupNo ratings yet

- सार - Last Note by Mr. Prashant JainDocument12 pagesसार - Last Note by Mr. Prashant JaindhavalNo ratings yet

- AfricaInvestor - April 11 2017Document4 pagesAfricaInvestor - April 11 2017Tiso Blackstar GroupNo ratings yet

- Markets and Commodity FiguresDocument4 pagesMarkets and Commodity FiguresTiso Blackstar GroupNo ratings yet

- Securitization and Structured Finance Post Credit Crunch: A Best Practice Deal Lifecycle GuideFrom EverandSecuritization and Structured Finance Post Credit Crunch: A Best Practice Deal Lifecycle GuideNo ratings yet

- Securities Operations: A Guide to Trade and Position ManagementFrom EverandSecurities Operations: A Guide to Trade and Position ManagementRating: 4 out of 5 stars4/5 (3)

- Saros Electronics LM317 Adjustable Voltage RegulatorDocument13 pagesSaros Electronics LM317 Adjustable Voltage RegulatorReneNo ratings yet

- Bài Tập Thì Hiện Tại Tiếp DiễnDocument9 pagesBài Tập Thì Hiện Tại Tiếp DiễnHÀ PHAN HOÀNG NGUYỆTNo ratings yet

- Nagothane Manufacturing Division Summer Internship ReportDocument5 pagesNagothane Manufacturing Division Summer Internship ReportMrudu PadteNo ratings yet

- Surface Treatments and CoatingsDocument4 pagesSurface Treatments and Coatingsmightym85No ratings yet

- HP 211B Manual PDFDocument61 pagesHP 211B Manual PDFDirson Volmir WilligNo ratings yet

- Conectores FsiDocument80 pagesConectores Fsijovares2099No ratings yet

- The PTP Telecom Profiles For Frequency, Phase and Time SynchronizationDocument30 pagesThe PTP Telecom Profiles For Frequency, Phase and Time Synchronizationalmel_09No ratings yet

- TP-20 For Protective RelaysDocument20 pagesTP-20 For Protective RelayssathiyaseelanNo ratings yet

- EN - Summer - 2013 - V-2012-08-17 - 1Document17 pagesEN - Summer - 2013 - V-2012-08-17 - 1chaudharyv100% (1)

- A Complete Manual On Ornamental Fish Culture: January 2013Document222 pagesA Complete Manual On Ornamental Fish Culture: January 2013Carlos MorenoNo ratings yet

- General Suggestion For SSCDocument6 pagesGeneral Suggestion For SSCJahirulNo ratings yet

- Case Digest: Assoc of Small Landowners vs. Sec. of Agrarian ReformDocument2 pagesCase Digest: Assoc of Small Landowners vs. Sec. of Agrarian ReformMaria Anna M Legaspi100% (3)

- Test Bank For Stationen 3rd EditionDocument20 pagesTest Bank For Stationen 3rd Editionattabaldigitulejp7tl100% (37)

- Perceived Consequences of Adoption of Mentha Cultivation in Central Uttar PradeshDocument8 pagesPerceived Consequences of Adoption of Mentha Cultivation in Central Uttar PradeshImpact JournalsNo ratings yet

- Derivatives - Practice QuestionsDocument4 pagesDerivatives - Practice QuestionsAdil AnwarNo ratings yet

- Lecture Note 3: Mechanism Design: - Games With Incomplete InformationDocument128 pagesLecture Note 3: Mechanism Design: - Games With Incomplete InformationABRAHAM GEORGENo ratings yet

- Pengenalan Safety N Health PDFDocument48 pagesPengenalan Safety N Health PDFwsuzana0% (1)

- M3-Social Media Text AnalyticsDocument19 pagesM3-Social Media Text AnalyticsKHAN SANA PARVEENNo ratings yet

- Strategy and Competitive Advantage Chapter 6Document7 pagesStrategy and Competitive Advantage Chapter 6Drishtee DevianeeNo ratings yet

- Worksheet There Was There Were 82860 20190907 20160905 120402Document4 pagesWorksheet There Was There Were 82860 20190907 20160905 120402Taty Angelita Vergara GonzalezNo ratings yet

- RR-0479-02 Novel Coronavirus (2019-nCoV) Real Time RT-PCR Kit-20200227 PDFDocument1 pageRR-0479-02 Novel Coronavirus (2019-nCoV) Real Time RT-PCR Kit-20200227 PDFwijaya adidarmaNo ratings yet

- Molnupiravir LOA 03232022Document12 pagesMolnupiravir LOA 03232022ivethNo ratings yet

- Manual KYK 30000Document20 pagesManual KYK 30000Benny ScorpyoNo ratings yet

- DHC Order - Section 59 Claim AmendmentsDocument35 pagesDHC Order - Section 59 Claim AmendmentsM VridhiNo ratings yet

- Laws4112 (2014) Exam Notes (Uq)Document132 pagesLaws4112 (2014) Exam Notes (Uq)tc_bassNo ratings yet

- Reboiler Case StudyDocument6 pagesReboiler Case StudyamlhrdsNo ratings yet

- Week 1 Shs Organic AgriDocument2 pagesWeek 1 Shs Organic Agrijessica coronel100% (2)