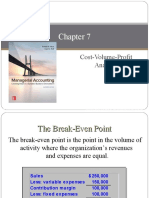

Equation Method: Sales Variable Expenses + Fixed Expenses + Profits (At The Break-Even Point Profits Equal Zero)

Equation Method: Sales Variable Expenses + Fixed Expenses + Profits (At The Break-Even Point Profits Equal Zero)

You might also like

- LittleAcorns DWNLDDocument27 pagesLittleAcorns DWNLDGraeme Cunningham100% (3)

- Problem Set 1 PDFDocument3 pagesProblem Set 1 PDFrenjith0% (2)

- CVP Analysis Review Problem SolutionDocument3 pagesCVP Analysis Review Problem SolutionSUNNY BHUSHANNo ratings yet

- DocxDocument6 pagesDocxLeo Sandy Ambe CuisNo ratings yet

- Marginal Costing Problems&Solutions 2Document51 pagesMarginal Costing Problems&Solutions 2Dr.Ashok Kumar Panigrahi100% (4)

- A181 Bkam3023 Topic 1 - CVP AnalysisDocument64 pagesA181 Bkam3023 Topic 1 - CVP AnalysisJagethiswari RajahNo ratings yet

- Cost-Volume-Profit Relationships1Document52 pagesCost-Volume-Profit Relationships1Kamrul Huda100% (1)

- Cost-Volume-Profit Relationships: Chapter FiveDocument82 pagesCost-Volume-Profit Relationships: Chapter FiveRahamat UllahNo ratings yet

- ACT202 Chapter 5 NewDocument82 pagesACT202 Chapter 5 NewAminaMatinNo ratings yet

- CVP AnalysisDocument22 pagesCVP AnalysisMolly RastogiNo ratings yet

- CVP AnalysisDocument36 pagesCVP Analysisghosh71No ratings yet

- Chapter Six Ba 315-Lpc Umsl: (Contribution Margin)Document53 pagesChapter Six Ba 315-Lpc Umsl: (Contribution Margin)NAZHIM KERENNo ratings yet

- Cost Volume Profit Analysis - Chapter 6Document39 pagesCost Volume Profit Analysis - Chapter 6Maria Maganda MalditaNo ratings yet

- Hilton 11e Chap007 StudentsDocument38 pagesHilton 11e Chap007 StudentsMelix SianturiNo ratings yet

- Chap 06 NotesDocument74 pagesChap 06 NotesNancy HineyNo ratings yet

- Chap 008Document34 pagesChap 008alishamrozNo ratings yet

- Break Even Answer KeyDocument8 pagesBreak Even Answer Keyyea okayNo ratings yet

- CVP PPT 1st YrDocument81 pagesCVP PPT 1st YrZachary AstorNo ratings yet

- Chapter 1 Cost-Volume-Profit RelationshipsDocument51 pagesChapter 1 Cost-Volume-Profit Relationshipspamela dequillamorteNo ratings yet

- Cost-Volume-Profit Analysis: Mcgraw-Hill/IrwinDocument78 pagesCost-Volume-Profit Analysis: Mcgraw-Hill/IrwinSheila Jane Maderse AbraganNo ratings yet

- The Basics of Cost-Volume-Profit (CVP) Analysis: After Covering Fixed Costs, Any Remaining CM Contributes To IncomeDocument10 pagesThe Basics of Cost-Volume-Profit (CVP) Analysis: After Covering Fixed Costs, Any Remaining CM Contributes To IncomeMozahar SujonNo ratings yet

- 2020 Session 6 CVP MBA CompleteDocument42 pages2020 Session 6 CVP MBA CompleteAbhishek BaruaNo ratings yet

- MAS Hilton Chap07Document30 pagesMAS Hilton Chap07YahiMicuaVillandaNo ratings yet

- Topic 11 (CVP)Document41 pagesTopic 11 (CVP)PrabhuNo ratings yet

- Chapter - 8 - Cost-Volume-Profit Analysis - UETDocument19 pagesChapter - 8 - Cost-Volume-Profit Analysis - UETZia UddinNo ratings yet

- Chapter 9 - CVP AnalysisDocument60 pagesChapter 9 - CVP AnalysisKunal ObhraiNo ratings yet

- Module 3 CVP AnswersDocument18 pagesModule 3 CVP AnswersSophia DayaoNo ratings yet

- Assignment 02 - SolutionDocument4 pagesAssignment 02 - SolutionSuman Paul ChowdhuryNo ratings yet

- CVP Analysis 08Document52 pagesCVP Analysis 08Maulani DwiNo ratings yet

- IPPTChap 007Document53 pagesIPPTChap 007Khaled BarakatNo ratings yet

- C - 2021MBA160 - Case ScenariosRBCDocument7 pagesC - 2021MBA160 - Case ScenariosRBCmohammedsuhaim abdul gafoorNo ratings yet

- Cost Volume Profit (CVP) AnalysisDocument40 pagesCost Volume Profit (CVP) AnalysisAnne PrestosaNo ratings yet

- 1chapter 7-Cost Volume-Profit Relationship and Break-Even AnalysisDocument4 pages1chapter 7-Cost Volume-Profit Relationship and Break-Even AnalysisShenedy Lauresta QuizanaNo ratings yet

- CAC Computations Chap 4 1 20Document9 pagesCAC Computations Chap 4 1 20rochelle lagmayNo ratings yet

- TH E PL Ofit Grai H: Graph 1Document13 pagesTH E PL Ofit Grai H: Graph 1aprilNo ratings yet

- Cost-Volume-Profit Relationships: Principles of Management AccountingDocument16 pagesCost-Volume-Profit Relationships: Principles of Management Accountingsyed haider ali shah shah100% (1)

- ProblemsDocument11 pagesProblemsMohamed RefaayNo ratings yet

- Cost-Volume-Profit RelationshipsDocument81 pagesCost-Volume-Profit RelationshipsAbdirahim HusseinNo ratings yet

- W11-12 Cost-Volume-Profit RelationshipsDocument82 pagesW11-12 Cost-Volume-Profit RelationshipsQurat SaboorNo ratings yet

- Chapter 20: Break Even and Cost Volume Profit Analysis: Group MemebersDocument34 pagesChapter 20: Break Even and Cost Volume Profit Analysis: Group MemebersMuhammad HasanNo ratings yet

- CVP Bba 2020Document58 pagesCVP Bba 2020Loreen Maya0% (1)

- TLA 4 Answers For DiscussionDocument21 pagesTLA 4 Answers For DiscussionTrisha Monique VillaNo ratings yet

- CVP ExercisesDocument7 pagesCVP ExercisesEunize Escalona100% (1)

- Break Even PointDocument11 pagesBreak Even Pointrahi4ever86% (7)

- Cost Concepts and CVP AnalysisDocument7 pagesCost Concepts and CVP AnalysisLara Lewis AchillesNo ratings yet

- Chapter 11 Cost-Volume-Profit Analysis A Managerial Planning ToolDocument40 pagesChapter 11 Cost-Volume-Profit Analysis A Managerial Planning Toolsalsa azzahra0% (1)

- Hilton 11e Chap007PPTDocument53 pagesHilton 11e Chap007PPTNgô Khánh HòaNo ratings yet

- CVP ExercisesDocument10 pagesCVP ExercisesDaiane AlcaideNo ratings yet

- Segment ReportingDocument4 pagesSegment ReportingMurshid IqbalNo ratings yet

- CH 11 AM Minggu 9Document37 pagesCH 11 AM Minggu 9Amelia BrilianaNo ratings yet

- PremiumsDocument10 pagesPremiumsPhoebe Dayrit CunananNo ratings yet

- Oroya Corporation - Oroya SegregationDocument8 pagesOroya Corporation - Oroya SegregationJULLIE CARMELLE H. CHATTONo ratings yet

- Bud GettingDocument8 pagesBud GettingLorena Mae LasquiteNo ratings yet

- CH 03 CPVDocument101 pagesCH 03 CPVsurpluslemonNo ratings yet

- A WK6 Chp5Document97 pagesA WK6 Chp5Jocelyn LimNo ratings yet

- Marginal Costing-Problems&Solutions-2Document45 pagesMarginal Costing-Problems&Solutions-2nahi batanaNo ratings yet

- BY Abhay Kumar Miba Iind SemDocument27 pagesBY Abhay Kumar Miba Iind SemSapna KushwahaNo ratings yet

- 202-0101-001 - ARIF HOSEN - Management Accounting Assignment 1Document11 pages202-0101-001 - ARIF HOSEN - Management Accounting Assignment 1Sayhan Hosen Arif100% (1)

- Module 3 Practice ProblemsDocument13 pagesModule 3 Practice ProblemsLiza Mae MirandaNo ratings yet

- Midway Greasy 2002 2003 2002 2003Document6 pagesMidway Greasy 2002 2003 2002 2003Pang SiulienNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- SM Ch-6 International StrategiesDocument112 pagesSM Ch-6 International StrategiesjaykishanfefarNo ratings yet

- MCQ in Geas by Perc DC - 2 (October 2011)Document15 pagesMCQ in Geas by Perc DC - 2 (October 2011)Zyren Jay G. MaganaNo ratings yet

- QMLR (Q) BankDocument27 pagesQMLR (Q) BankaymanNo ratings yet

- DepEd Income Generating Project Proposal and Terminal ReportDocument6 pagesDepEd Income Generating Project Proposal and Terminal ReportHart Franada100% (2)

- Unit 4 Quotation and OfferDocument37 pagesUnit 4 Quotation and OfferthuhienNo ratings yet

- Job Order CostingDocument51 pagesJob Order CostingKenneth TallmanNo ratings yet

- Cpa Review School of The Philippines ManilaDocument2 pagesCpa Review School of The Philippines ManilaAljur SalamedaNo ratings yet

- 37 Wyckoff TimeDocument4 pages37 Wyckoff TimeACasey101100% (1)

- Decision Making QuestionsDocument3 pagesDecision Making QuestionsJaya GuptaNo ratings yet

- Symbiosis Institute of Management Studies: Submitted To: Dr. Komal ChopraDocument8 pagesSymbiosis Institute of Management Studies: Submitted To: Dr. Komal ChopraPalak TeotiaNo ratings yet

- Required:: Complete This Question by Entering Your Answers in The Tabs BelowDocument2 pagesRequired:: Complete This Question by Entering Your Answers in The Tabs BelowAbdiasisNo ratings yet

- TOA Bond Payable and Notes PayableDocument3 pagesTOA Bond Payable and Notes PayablePatrick BacongalloNo ratings yet

- From Brand To LovemarkDocument5 pagesFrom Brand To LovemarkAlexandraIlieNo ratings yet

- NCERT Solutions Class 10 Social Science Economics Chapter 4Document4 pagesNCERT Solutions Class 10 Social Science Economics Chapter 4Partha NathNo ratings yet

- Microeconomics Course SyllabusDocument5 pagesMicroeconomics Course SyllabusSamira AlhashimiNo ratings yet

- Case Presentation PART 2+PART 3Document3 pagesCase Presentation PART 2+PART 3jackywen1024No ratings yet

- Just Baked Inventory ManagementDocument1 pageJust Baked Inventory ManagementRasheeq Rayhan0% (2)

- Quiz 2 - Business ValuationDocument17 pagesQuiz 2 - Business ValuationJacinta Fatima ChingNo ratings yet

- Chapter10 Reviewquestions AnswersDocument2 pagesChapter10 Reviewquestions AnswersEANNA15No ratings yet

- Process of Fundamental Analysis PDFDocument8 pagesProcess of Fundamental Analysis PDFajay.1k7625100% (1)

- Session 2Document32 pagesSession 2Spetznaz SaiNo ratings yet

- Mohd. Faid Khan: ObjectiveDocument4 pagesMohd. Faid Khan: Objectiveanon_948045789No ratings yet

- Financial Modeling With Excel and VBADocument113 pagesFinancial Modeling With Excel and VBAakash_sugumaran100% (11)

- Study Unit 2.1 Demand and Supply in Action: Ms. Precious MncayiDocument32 pagesStudy Unit 2.1 Demand and Supply in Action: Ms. Precious MncayiZiphelele VilakaziNo ratings yet

- Toyota RecallDocument2 pagesToyota RecallJohnChoiNo ratings yet

- World: Oats - Market Report. Analysis and Forecast To 2020Document7 pagesWorld: Oats - Market Report. Analysis and Forecast To 2020IndexBox MarketingNo ratings yet

- Micro Economics AssignmentDocument10 pagesMicro Economics AssignmentsipanjegivenNo ratings yet

- Guide To Using Internationa 2Document321 pagesGuide To Using Internationa 2Friista Aulia LabibaNo ratings yet

Download as docx, pdf, or txt

You might also like

- LittleAcorns DWNLDDocument27 pagesLittleAcorns DWNLDGraeme Cunningham100% (3)

- Problem Set 1 PDFDocument3 pagesProblem Set 1 PDFrenjith0% (2)

- CVP Analysis Review Problem SolutionDocument3 pagesCVP Analysis Review Problem SolutionSUNNY BHUSHANNo ratings yet

- DocxDocument6 pagesDocxLeo Sandy Ambe CuisNo ratings yet

- Marginal Costing Problems&Solutions 2Document51 pagesMarginal Costing Problems&Solutions 2Dr.Ashok Kumar Panigrahi100% (4)

- A181 Bkam3023 Topic 1 - CVP AnalysisDocument64 pagesA181 Bkam3023 Topic 1 - CVP AnalysisJagethiswari RajahNo ratings yet

- Cost-Volume-Profit Relationships1Document52 pagesCost-Volume-Profit Relationships1Kamrul Huda100% (1)

- Cost-Volume-Profit Relationships: Chapter FiveDocument82 pagesCost-Volume-Profit Relationships: Chapter FiveRahamat UllahNo ratings yet

- ACT202 Chapter 5 NewDocument82 pagesACT202 Chapter 5 NewAminaMatinNo ratings yet

- CVP AnalysisDocument22 pagesCVP AnalysisMolly RastogiNo ratings yet

- CVP AnalysisDocument36 pagesCVP Analysisghosh71No ratings yet

- Chapter Six Ba 315-Lpc Umsl: (Contribution Margin)Document53 pagesChapter Six Ba 315-Lpc Umsl: (Contribution Margin)NAZHIM KERENNo ratings yet

- Cost Volume Profit Analysis - Chapter 6Document39 pagesCost Volume Profit Analysis - Chapter 6Maria Maganda MalditaNo ratings yet

- Hilton 11e Chap007 StudentsDocument38 pagesHilton 11e Chap007 StudentsMelix SianturiNo ratings yet

- Chap 06 NotesDocument74 pagesChap 06 NotesNancy HineyNo ratings yet

- Chap 008Document34 pagesChap 008alishamrozNo ratings yet

- Break Even Answer KeyDocument8 pagesBreak Even Answer Keyyea okayNo ratings yet

- CVP PPT 1st YrDocument81 pagesCVP PPT 1st YrZachary AstorNo ratings yet

- Chapter 1 Cost-Volume-Profit RelationshipsDocument51 pagesChapter 1 Cost-Volume-Profit Relationshipspamela dequillamorteNo ratings yet

- Cost-Volume-Profit Analysis: Mcgraw-Hill/IrwinDocument78 pagesCost-Volume-Profit Analysis: Mcgraw-Hill/IrwinSheila Jane Maderse AbraganNo ratings yet

- The Basics of Cost-Volume-Profit (CVP) Analysis: After Covering Fixed Costs, Any Remaining CM Contributes To IncomeDocument10 pagesThe Basics of Cost-Volume-Profit (CVP) Analysis: After Covering Fixed Costs, Any Remaining CM Contributes To IncomeMozahar SujonNo ratings yet

- 2020 Session 6 CVP MBA CompleteDocument42 pages2020 Session 6 CVP MBA CompleteAbhishek BaruaNo ratings yet

- MAS Hilton Chap07Document30 pagesMAS Hilton Chap07YahiMicuaVillandaNo ratings yet

- Topic 11 (CVP)Document41 pagesTopic 11 (CVP)PrabhuNo ratings yet

- Chapter - 8 - Cost-Volume-Profit Analysis - UETDocument19 pagesChapter - 8 - Cost-Volume-Profit Analysis - UETZia UddinNo ratings yet

- Chapter 9 - CVP AnalysisDocument60 pagesChapter 9 - CVP AnalysisKunal ObhraiNo ratings yet

- Module 3 CVP AnswersDocument18 pagesModule 3 CVP AnswersSophia DayaoNo ratings yet

- Assignment 02 - SolutionDocument4 pagesAssignment 02 - SolutionSuman Paul ChowdhuryNo ratings yet

- CVP Analysis 08Document52 pagesCVP Analysis 08Maulani DwiNo ratings yet

- IPPTChap 007Document53 pagesIPPTChap 007Khaled BarakatNo ratings yet

- C - 2021MBA160 - Case ScenariosRBCDocument7 pagesC - 2021MBA160 - Case ScenariosRBCmohammedsuhaim abdul gafoorNo ratings yet

- Cost Volume Profit (CVP) AnalysisDocument40 pagesCost Volume Profit (CVP) AnalysisAnne PrestosaNo ratings yet

- 1chapter 7-Cost Volume-Profit Relationship and Break-Even AnalysisDocument4 pages1chapter 7-Cost Volume-Profit Relationship and Break-Even AnalysisShenedy Lauresta QuizanaNo ratings yet

- CAC Computations Chap 4 1 20Document9 pagesCAC Computations Chap 4 1 20rochelle lagmayNo ratings yet

- TH E PL Ofit Grai H: Graph 1Document13 pagesTH E PL Ofit Grai H: Graph 1aprilNo ratings yet

- Cost-Volume-Profit Relationships: Principles of Management AccountingDocument16 pagesCost-Volume-Profit Relationships: Principles of Management Accountingsyed haider ali shah shah100% (1)

- ProblemsDocument11 pagesProblemsMohamed RefaayNo ratings yet

- Cost-Volume-Profit RelationshipsDocument81 pagesCost-Volume-Profit RelationshipsAbdirahim HusseinNo ratings yet

- W11-12 Cost-Volume-Profit RelationshipsDocument82 pagesW11-12 Cost-Volume-Profit RelationshipsQurat SaboorNo ratings yet

- Chapter 20: Break Even and Cost Volume Profit Analysis: Group MemebersDocument34 pagesChapter 20: Break Even and Cost Volume Profit Analysis: Group MemebersMuhammad HasanNo ratings yet

- CVP Bba 2020Document58 pagesCVP Bba 2020Loreen Maya0% (1)

- TLA 4 Answers For DiscussionDocument21 pagesTLA 4 Answers For DiscussionTrisha Monique VillaNo ratings yet

- CVP ExercisesDocument7 pagesCVP ExercisesEunize Escalona100% (1)

- Break Even PointDocument11 pagesBreak Even Pointrahi4ever86% (7)

- Cost Concepts and CVP AnalysisDocument7 pagesCost Concepts and CVP AnalysisLara Lewis AchillesNo ratings yet

- Chapter 11 Cost-Volume-Profit Analysis A Managerial Planning ToolDocument40 pagesChapter 11 Cost-Volume-Profit Analysis A Managerial Planning Toolsalsa azzahra0% (1)

- Hilton 11e Chap007PPTDocument53 pagesHilton 11e Chap007PPTNgô Khánh HòaNo ratings yet

- CVP ExercisesDocument10 pagesCVP ExercisesDaiane AlcaideNo ratings yet

- Segment ReportingDocument4 pagesSegment ReportingMurshid IqbalNo ratings yet

- CH 11 AM Minggu 9Document37 pagesCH 11 AM Minggu 9Amelia BrilianaNo ratings yet

- PremiumsDocument10 pagesPremiumsPhoebe Dayrit CunananNo ratings yet

- Oroya Corporation - Oroya SegregationDocument8 pagesOroya Corporation - Oroya SegregationJULLIE CARMELLE H. CHATTONo ratings yet

- Bud GettingDocument8 pagesBud GettingLorena Mae LasquiteNo ratings yet

- CH 03 CPVDocument101 pagesCH 03 CPVsurpluslemonNo ratings yet

- A WK6 Chp5Document97 pagesA WK6 Chp5Jocelyn LimNo ratings yet

- Marginal Costing-Problems&Solutions-2Document45 pagesMarginal Costing-Problems&Solutions-2nahi batanaNo ratings yet

- BY Abhay Kumar Miba Iind SemDocument27 pagesBY Abhay Kumar Miba Iind SemSapna KushwahaNo ratings yet

- 202-0101-001 - ARIF HOSEN - Management Accounting Assignment 1Document11 pages202-0101-001 - ARIF HOSEN - Management Accounting Assignment 1Sayhan Hosen Arif100% (1)

- Module 3 Practice ProblemsDocument13 pagesModule 3 Practice ProblemsLiza Mae MirandaNo ratings yet

- Midway Greasy 2002 2003 2002 2003Document6 pagesMidway Greasy 2002 2003 2002 2003Pang SiulienNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- SM Ch-6 International StrategiesDocument112 pagesSM Ch-6 International StrategiesjaykishanfefarNo ratings yet

- MCQ in Geas by Perc DC - 2 (October 2011)Document15 pagesMCQ in Geas by Perc DC - 2 (October 2011)Zyren Jay G. MaganaNo ratings yet

- QMLR (Q) BankDocument27 pagesQMLR (Q) BankaymanNo ratings yet

- DepEd Income Generating Project Proposal and Terminal ReportDocument6 pagesDepEd Income Generating Project Proposal and Terminal ReportHart Franada100% (2)

- Unit 4 Quotation and OfferDocument37 pagesUnit 4 Quotation and OfferthuhienNo ratings yet

- Job Order CostingDocument51 pagesJob Order CostingKenneth TallmanNo ratings yet

- Cpa Review School of The Philippines ManilaDocument2 pagesCpa Review School of The Philippines ManilaAljur SalamedaNo ratings yet

- 37 Wyckoff TimeDocument4 pages37 Wyckoff TimeACasey101100% (1)

- Decision Making QuestionsDocument3 pagesDecision Making QuestionsJaya GuptaNo ratings yet

- Symbiosis Institute of Management Studies: Submitted To: Dr. Komal ChopraDocument8 pagesSymbiosis Institute of Management Studies: Submitted To: Dr. Komal ChopraPalak TeotiaNo ratings yet

- Required:: Complete This Question by Entering Your Answers in The Tabs BelowDocument2 pagesRequired:: Complete This Question by Entering Your Answers in The Tabs BelowAbdiasisNo ratings yet

- TOA Bond Payable and Notes PayableDocument3 pagesTOA Bond Payable and Notes PayablePatrick BacongalloNo ratings yet

- From Brand To LovemarkDocument5 pagesFrom Brand To LovemarkAlexandraIlieNo ratings yet

- NCERT Solutions Class 10 Social Science Economics Chapter 4Document4 pagesNCERT Solutions Class 10 Social Science Economics Chapter 4Partha NathNo ratings yet

- Microeconomics Course SyllabusDocument5 pagesMicroeconomics Course SyllabusSamira AlhashimiNo ratings yet

- Case Presentation PART 2+PART 3Document3 pagesCase Presentation PART 2+PART 3jackywen1024No ratings yet

- Just Baked Inventory ManagementDocument1 pageJust Baked Inventory ManagementRasheeq Rayhan0% (2)

- Quiz 2 - Business ValuationDocument17 pagesQuiz 2 - Business ValuationJacinta Fatima ChingNo ratings yet

- Chapter10 Reviewquestions AnswersDocument2 pagesChapter10 Reviewquestions AnswersEANNA15No ratings yet

- Process of Fundamental Analysis PDFDocument8 pagesProcess of Fundamental Analysis PDFajay.1k7625100% (1)

- Session 2Document32 pagesSession 2Spetznaz SaiNo ratings yet

- Mohd. Faid Khan: ObjectiveDocument4 pagesMohd. Faid Khan: Objectiveanon_948045789No ratings yet

- Financial Modeling With Excel and VBADocument113 pagesFinancial Modeling With Excel and VBAakash_sugumaran100% (11)

- Study Unit 2.1 Demand and Supply in Action: Ms. Precious MncayiDocument32 pagesStudy Unit 2.1 Demand and Supply in Action: Ms. Precious MncayiZiphelele VilakaziNo ratings yet

- Toyota RecallDocument2 pagesToyota RecallJohnChoiNo ratings yet

- World: Oats - Market Report. Analysis and Forecast To 2020Document7 pagesWorld: Oats - Market Report. Analysis and Forecast To 2020IndexBox MarketingNo ratings yet

- Micro Economics AssignmentDocument10 pagesMicro Economics AssignmentsipanjegivenNo ratings yet

- Guide To Using Internationa 2Document321 pagesGuide To Using Internationa 2Friista Aulia LabibaNo ratings yet