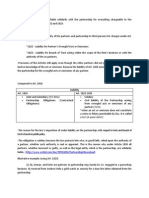

Partnership I. Contract of Partnership A. Definition: Artnership

Partnership I. Contract of Partnership A. Definition: Artnership

You might also like

- Tally Practice QuestionsDocument68 pagesTally Practice Questionspranav tomar50% (4)

- Amazon ProjectDocument55 pagesAmazon ProjectMahesh Kumar86% (21)

- Revised Corporation CodeDocument17 pagesRevised Corporation CodeMikey Fabella100% (10)

- Corporation Law ReviewerDocument165 pagesCorporation Law ReviewerKaren Cue89% (19)

- UST Golden Notes 2011 - Partnership and Agency PDFDocument42 pagesUST Golden Notes 2011 - Partnership and Agency PDFVenus Leilani Villanueva-Granado100% (11)

- Mengo Senior School S1 - S5 Payment Reference GuideDocument5 pagesMengo Senior School S1 - S5 Payment Reference GuidePentNo ratings yet

- San Beda PartnershipDocument32 pagesSan Beda PartnershipLenard Trinidad79% (14)

- Leadership Development at Goldman SachsDocument2 pagesLeadership Development at Goldman SachsCyril Scaria50% (4)

- DASP Hostplus FormDocument4 pagesDASP Hostplus FormpaulaNo ratings yet

- INTAX Chapter 8Document15 pagesINTAX Chapter 8Levy PanganNo ratings yet

- LAW On PARTNERSHIPS & PRIVATE CORPORATIONS - ReviewerDocument18 pagesLAW On PARTNERSHIPS & PRIVATE CORPORATIONS - ReviewerOne DozenNo ratings yet

- Acompre DatedDocument1 pageAcompre DatedAnonymous t1lbUug0A50% (4)

- PartnershipDocument7 pagesPartnershipami50% (2)

- ObliCon BAR Q&ADocument106 pagesObliCon BAR Q&AMaan50% (4)

- Judicial AffidavitDocument5 pagesJudicial AffidavitChe PuebloNo ratings yet

- I. Objectives: Semi-Detailed Lesson PlanDocument3 pagesI. Objectives: Semi-Detailed Lesson PlanChe PuebloNo ratings yet

- Acrf Partnership and Corporation DomingoDocument43 pagesAcrf Partnership and Corporation Domingowaeyo girlNo ratings yet

- Income Taxation Reviewer : With TRAIN Law UpdatesDocument25 pagesIncome Taxation Reviewer : With TRAIN Law UpdatesTristanMaglinaoCanta75% (4)

- Law On Partnership (Review)Document3 pagesLaw On Partnership (Review)Yumar Nico MediavilloNo ratings yet

- COBLAW2 2ndterm20192020 Topic21Jan2020Document9 pagesCOBLAW2 2ndterm20192020 Topic21Jan2020Rina TugadeNo ratings yet

- THE CORPORATION CODE OF THE PHILIPPINES FINAL 1 SorianoDocument160 pagesTHE CORPORATION CODE OF THE PHILIPPINES FINAL 1 Sorianoshynette escoverNo ratings yet

- Law2 Parcor de Leon Full Study GuideDocument89 pagesLaw2 Parcor de Leon Full Study GuideCindy Evangelista100% (4)

- Law On Corporations Test Bank With Revised Corporate Code References - CompressDocument62 pagesLaw On Corporations Test Bank With Revised Corporate Code References - CompressCharles MateoNo ratings yet

- Corporation CodeDocument54 pagesCorporation Codecomkeeper1100% (3)

- Partnership 1767 1799Document24 pagesPartnership 1767 1799Ally CapacioNo ratings yet

- Chapter 6 To Chapter 8Document4 pagesChapter 6 To Chapter 8Jarren BasilanNo ratings yet

- Revised Corporation Reviewer PDFDocument83 pagesRevised Corporation Reviewer PDFAnna Charlotte100% (1)

- Chapter 1-3 Law On SalesDocument5 pagesChapter 1-3 Law On SalesKathrina TonidoNo ratings yet

- Business Laws and Regulations - Prelim Exam (BAYNA, TRIXIA MAE)Document2 pagesBusiness Laws and Regulations - Prelim Exam (BAYNA, TRIXIA MAE)Trixia Mae BaynaNo ratings yet

- Partnership 1847 1856Document32 pagesPartnership 1847 1856Sunhine50% (2)

- C. Property Rights of A PartnerDocument5 pagesC. Property Rights of A PartnerClyde Tan0% (2)

- Corpo ReviewerDocument62 pagesCorpo ReviewerLorelie Sakiwat VargasNo ratings yet

- UST Golden Notes - Corporation LawDocument75 pagesUST Golden Notes - Corporation Lawaugustofficials100% (9)

- LECTURE NOTES - Corporation and Cooperative LawDocument11 pagesLECTURE NOTES - Corporation and Cooperative LawJean Ysrael Marquez100% (6)

- PartnershipDocument8 pagesPartnershipFrancis Ray Arbon FilipinasNo ratings yet

- Art. 1815 - 1827Document41 pagesArt. 1815 - 1827erikha_aranetaNo ratings yet

- Partnership 1767 - 1783 2Document5 pagesPartnership 1767 - 1783 2vea domingoNo ratings yet

- 1848-1852 General Rules and ExceptionDocument7 pages1848-1852 General Rules and ExceptionJulo R. Taleon100% (1)

- Summary Notes - Property Relations & Estate Tax Credit and Distributable EstateDocument3 pagesSummary Notes - Property Relations & Estate Tax Credit and Distributable EstateKiana FernandezNo ratings yet

- Tax2 Midterm Exam-SentDocument12 pagesTax2 Midterm Exam-SentRen A EleponioNo ratings yet

- Acctax1 AY 2016-2017 ProblemsDocument77 pagesAcctax1 AY 2016-2017 ProblemsRebekahNo ratings yet

- Art 1848-1852Document4 pagesArt 1848-1852Rea Jane B. MalcampoNo ratings yet

- Ra 11232 (Revised Corporation Code of The Philippines)Document26 pagesRa 11232 (Revised Corporation Code of The Philippines)Darryl Sarte BoocNo ratings yet

- Congress Passed A Proposed Law Creating A Corporation To Engage in Agricultural ActivitiesDocument1 pageCongress Passed A Proposed Law Creating A Corporation To Engage in Agricultural ActivitiesrockerNo ratings yet

- Law On Partnership and Corporation Study Guide de LeonDocument9 pagesLaw On Partnership and Corporation Study Guide de LeonLhorene Hope Dueñas0% (2)

- Art 1772-1774Document3 pagesArt 1772-1774CML100% (1)

- Law On Partnership and Corporation by Hector de LeonDocument41 pagesLaw On Partnership and Corporation by Hector de LeonMary Claudette Unabia100% (3)

- Notes - Law On Partnerships and Private CorporationsDocument20 pagesNotes - Law On Partnerships and Private CorporationsJeremyDream Lim100% (3)

- Law On Partnership and Corporation NotesDocument26 pagesLaw On Partnership and Corporation NotesJahzeel Y. Nolasco83% (6)

- RFBT 2 Partnership Midterm ReviewerDocument6 pagesRFBT 2 Partnership Midterm ReviewerJamaica DavidNo ratings yet

- Jose Rizal Memorial State University Main Campus, Dapitan City College of Business and AccountancyDocument6 pagesJose Rizal Memorial State University Main Campus, Dapitan City College of Business and AccountancyBernadette CaduyacNo ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document30 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- Law On Partnership and Corporation Study GuideDocument109 pagesLaw On Partnership and Corporation Study GuideAlma Landero100% (1)

- Delectus PersonaeDocument59 pagesDelectus Personaeleahtabs100% (3)

- Foreign Tax CreditDocument2 pagesForeign Tax CreditSophiaFrancescaEspinosaNo ratings yet

- Article 1808-1827Document7 pagesArticle 1808-1827Janaisa Bugayong EspantoNo ratings yet

- UST Golden Notes in Partnership and AgenDocument42 pagesUST Golden Notes in Partnership and AgenDominique O. BerinoNo ratings yet

- Partnership I. Contract of Partnership 23definition: ArtnershipDocument44 pagesPartnership I. Contract of Partnership 23definition: ArtnershipHyviBaculiSaynoNo ratings yet

- Law On Partnership - Chapter 1 by DomingoDocument11 pagesLaw On Partnership - Chapter 1 by Domingojhoana morenoNo ratings yet

- Law in PartnershipDocument15 pagesLaw in Partnershipmelody agravanteNo ratings yet

- Review PartnershipDocument77 pagesReview PartnershipRoy Samuel HalasanNo ratings yet

- Mercantile Law Case Digests: Case Name Subject and Topic Facts Issue RulingDocument8 pagesMercantile Law Case Digests: Case Name Subject and Topic Facts Issue RulingJohn Dexter FuentesNo ratings yet

- CHAPTER 1 - General ProvisionDocument36 pagesCHAPTER 1 - General ProvisionziahnepostreliNo ratings yet

- Acrf Partnership and Corporation DomingoDocument42 pagesAcrf Partnership and Corporation DomingoJullie AnnNo ratings yet

- Articuna - GENERAL OVERVIEW OF THE LAW ON PARTNERSHIPDocument4 pagesArticuna - GENERAL OVERVIEW OF THE LAW ON PARTNERSHIPIrish ArticunaNo ratings yet

- Docshare - Tips - Co Ownership DigestDocument12 pagesDocshare - Tips - Co Ownership DigestRae Marie Cadeliña ManarNo ratings yet

- LAW Chapter I (1767-1783)Document11 pagesLAW Chapter I (1767-1783)JaimeMorNo ratings yet

- Transportation Law Cases.1Document140 pagesTransportation Law Cases.1Che PuebloNo ratings yet

- Learners With Emotional - OutlineDocument1 pageLearners With Emotional - OutlineChe PuebloNo ratings yet

- First Name Last NameDocument5 pagesFirst Name Last NameChe PuebloNo ratings yet

- Address One of The Students To Lead The PrayerDocument6 pagesAddress One of The Students To Lead The PrayerChe PuebloNo ratings yet

- introToLAw CasesDocument12 pagesintroToLAw CasesChe PuebloNo ratings yet

- Long Quiz in Assessment of LearningDocument2 pagesLong Quiz in Assessment of LearningChe PuebloNo ratings yet

- Buffet Service 320Document1 pageBuffet Service 320Che PuebloNo ratings yet

- Buffet Service PHP 375.00/head: (Soup, Salad, 3 Main Courses, Rice, Dessert and Drinks)Document2 pagesBuffet Service PHP 375.00/head: (Soup, Salad, 3 Main Courses, Rice, Dessert and Drinks)Che PuebloNo ratings yet

- Wedding Package 2 - P 65,000Document1 pageWedding Package 2 - P 65,000Che PuebloNo ratings yet

- 7 Ways To Generate Extra Income From HomeDocument5 pages7 Ways To Generate Extra Income From HomeChe PuebloNo ratings yet

- Buffet Service PHP 360.00/head (3 Main Courses W/ Soup, Rice, Dessert and Drinks)Document2 pagesBuffet Service PHP 360.00/head (3 Main Courses W/ Soup, Rice, Dessert and Drinks)Che PuebloNo ratings yet

- Nature of Special ProceedingsDocument479 pagesNature of Special ProceedingsChe PuebloNo ratings yet

- TAX Course OutlineDocument4 pagesTAX Course OutlineChe PuebloNo ratings yet

- QUIZ No1.Final - AssessmentDocument1 pageQUIZ No1.Final - AssessmentChe PuebloNo ratings yet

- Love QuotesDocument1 pageLove QuotesChe PuebloNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument54 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledChe PuebloNo ratings yet

- Complaint - AffidavitDocument3 pagesComplaint - AffidavitChe PuebloNo ratings yet

- Assessment of Learning 1: Long QuizDocument5 pagesAssessment of Learning 1: Long QuizChe Pueblo100% (1)

- Ids PDFDocument397 pagesIds PDFMinh Ngô HảiNo ratings yet

- The Cultural Politics of Femvertising Selling Empowerment Joel Gwynne Full Chapter PDFDocument69 pagesThe Cultural Politics of Femvertising Selling Empowerment Joel Gwynne Full Chapter PDFeachurjallai100% (5)

- Curriculam Vitae: Vemula Govinda Raju Personal DataDocument3 pagesCurriculam Vitae: Vemula Govinda Raju Personal DataAJAYNo ratings yet

- Case Study Champions League FinalDocument14 pagesCase Study Champions League FinalRakeem DavidsonNo ratings yet

- 01 - Introduction To E-CommerceDocument19 pages01 - Introduction To E-Commercehioctane10No ratings yet

- 2023 SDF Budget PlannerDocument44 pages2023 SDF Budget PlannerJoyce D. FernandezNo ratings yet

- 1988 Motorola Annual Report PDFDocument40 pages1988 Motorola Annual Report PDFmrinal1690No ratings yet

- VictoriaDocument2 pagesVictoriaapi-535156077No ratings yet

- Founder's Guide To b2b SalesDocument60 pagesFounder's Guide To b2b SalesdesignerskreativNo ratings yet

- 250,000 300,000 400,000 500,000 Cash Flow: Year 1 2 3 4Document9 pages250,000 300,000 400,000 500,000 Cash Flow: Year 1 2 3 4Kai ZhaoNo ratings yet

- Women in CryptoDocument26 pagesWomen in CryptoRodrix DigitalNo ratings yet

- How To Back Up A Database UPS (WORLDSHIP)Document2 pagesHow To Back Up A Database UPS (WORLDSHIP)Wagner Esteban Cepeda AquinoNo ratings yet

- Solved ProblemDocument4 pagesSolved ProblemSophiya NeupaneNo ratings yet

- ANS AlagangWency-2nd-quizDocument13 pagesANS AlagangWency-2nd-quizJazzy MercadoNo ratings yet

- Microservice ArchitectureDocument22 pagesMicroservice ArchitecturenamNo ratings yet

- Bs en 12Document10 pagesBs en 12Alvin BadzNo ratings yet

- Spandana Sphoorty Financial PDFDocument4 pagesSpandana Sphoorty Financial PDFdarshanmadeNo ratings yet

- Grupo 3 Crucigrama ResueltoDocument2 pagesGrupo 3 Crucigrama ResueltoKevin LancherosNo ratings yet

- Qp-Luxm-Gs & SJDocument2 pagesQp-Luxm-Gs & SJRaksha StarNo ratings yet

- S4hana CopaDocument10 pagesS4hana CopaGhosh2100% (1)

- Affidavit of incOMEDocument5 pagesAffidavit of incOMEPedro Silo100% (1)

- Ensilo/Fortiedr: Course DescriptionDocument2 pagesEnsilo/Fortiedr: Course DescriptionhoadiNo ratings yet

- Financial Institutions and Markets: Subject Code: EL15FN505Document63 pagesFinancial Institutions and Markets: Subject Code: EL15FN505Anusha RajNo ratings yet

- Developing Sustainable Tourism Product For Sailing Sapa Homestay - Rational ReportDocument73 pagesDeveloping Sustainable Tourism Product For Sailing Sapa Homestay - Rational ReportQTKD 4D-18 Vuong Thuy TrangNo ratings yet

- PoM Unit Wise QBDocument11 pagesPoM Unit Wise QBNirmal KumarNo ratings yet

Download as docx, pdf, or txt

You might also like

- Tally Practice QuestionsDocument68 pagesTally Practice Questionspranav tomar50% (4)

- Amazon ProjectDocument55 pagesAmazon ProjectMahesh Kumar86% (21)

- Revised Corporation CodeDocument17 pagesRevised Corporation CodeMikey Fabella100% (10)

- Corporation Law ReviewerDocument165 pagesCorporation Law ReviewerKaren Cue89% (19)

- UST Golden Notes 2011 - Partnership and Agency PDFDocument42 pagesUST Golden Notes 2011 - Partnership and Agency PDFVenus Leilani Villanueva-Granado100% (11)

- Mengo Senior School S1 - S5 Payment Reference GuideDocument5 pagesMengo Senior School S1 - S5 Payment Reference GuidePentNo ratings yet

- San Beda PartnershipDocument32 pagesSan Beda PartnershipLenard Trinidad79% (14)

- Leadership Development at Goldman SachsDocument2 pagesLeadership Development at Goldman SachsCyril Scaria50% (4)

- DASP Hostplus FormDocument4 pagesDASP Hostplus FormpaulaNo ratings yet

- INTAX Chapter 8Document15 pagesINTAX Chapter 8Levy PanganNo ratings yet

- LAW On PARTNERSHIPS & PRIVATE CORPORATIONS - ReviewerDocument18 pagesLAW On PARTNERSHIPS & PRIVATE CORPORATIONS - ReviewerOne DozenNo ratings yet

- Acompre DatedDocument1 pageAcompre DatedAnonymous t1lbUug0A50% (4)

- PartnershipDocument7 pagesPartnershipami50% (2)

- ObliCon BAR Q&ADocument106 pagesObliCon BAR Q&AMaan50% (4)

- Judicial AffidavitDocument5 pagesJudicial AffidavitChe PuebloNo ratings yet

- I. Objectives: Semi-Detailed Lesson PlanDocument3 pagesI. Objectives: Semi-Detailed Lesson PlanChe PuebloNo ratings yet

- Acrf Partnership and Corporation DomingoDocument43 pagesAcrf Partnership and Corporation Domingowaeyo girlNo ratings yet

- Income Taxation Reviewer : With TRAIN Law UpdatesDocument25 pagesIncome Taxation Reviewer : With TRAIN Law UpdatesTristanMaglinaoCanta75% (4)

- Law On Partnership (Review)Document3 pagesLaw On Partnership (Review)Yumar Nico MediavilloNo ratings yet

- COBLAW2 2ndterm20192020 Topic21Jan2020Document9 pagesCOBLAW2 2ndterm20192020 Topic21Jan2020Rina TugadeNo ratings yet

- THE CORPORATION CODE OF THE PHILIPPINES FINAL 1 SorianoDocument160 pagesTHE CORPORATION CODE OF THE PHILIPPINES FINAL 1 Sorianoshynette escoverNo ratings yet

- Law2 Parcor de Leon Full Study GuideDocument89 pagesLaw2 Parcor de Leon Full Study GuideCindy Evangelista100% (4)

- Law On Corporations Test Bank With Revised Corporate Code References - CompressDocument62 pagesLaw On Corporations Test Bank With Revised Corporate Code References - CompressCharles MateoNo ratings yet

- Corporation CodeDocument54 pagesCorporation Codecomkeeper1100% (3)

- Partnership 1767 1799Document24 pagesPartnership 1767 1799Ally CapacioNo ratings yet

- Chapter 6 To Chapter 8Document4 pagesChapter 6 To Chapter 8Jarren BasilanNo ratings yet

- Revised Corporation Reviewer PDFDocument83 pagesRevised Corporation Reviewer PDFAnna Charlotte100% (1)

- Chapter 1-3 Law On SalesDocument5 pagesChapter 1-3 Law On SalesKathrina TonidoNo ratings yet

- Business Laws and Regulations - Prelim Exam (BAYNA, TRIXIA MAE)Document2 pagesBusiness Laws and Regulations - Prelim Exam (BAYNA, TRIXIA MAE)Trixia Mae BaynaNo ratings yet

- Partnership 1847 1856Document32 pagesPartnership 1847 1856Sunhine50% (2)

- C. Property Rights of A PartnerDocument5 pagesC. Property Rights of A PartnerClyde Tan0% (2)

- Corpo ReviewerDocument62 pagesCorpo ReviewerLorelie Sakiwat VargasNo ratings yet

- UST Golden Notes - Corporation LawDocument75 pagesUST Golden Notes - Corporation Lawaugustofficials100% (9)

- LECTURE NOTES - Corporation and Cooperative LawDocument11 pagesLECTURE NOTES - Corporation and Cooperative LawJean Ysrael Marquez100% (6)

- PartnershipDocument8 pagesPartnershipFrancis Ray Arbon FilipinasNo ratings yet

- Art. 1815 - 1827Document41 pagesArt. 1815 - 1827erikha_aranetaNo ratings yet

- Partnership 1767 - 1783 2Document5 pagesPartnership 1767 - 1783 2vea domingoNo ratings yet

- 1848-1852 General Rules and ExceptionDocument7 pages1848-1852 General Rules and ExceptionJulo R. Taleon100% (1)

- Summary Notes - Property Relations & Estate Tax Credit and Distributable EstateDocument3 pagesSummary Notes - Property Relations & Estate Tax Credit and Distributable EstateKiana FernandezNo ratings yet

- Tax2 Midterm Exam-SentDocument12 pagesTax2 Midterm Exam-SentRen A EleponioNo ratings yet

- Acctax1 AY 2016-2017 ProblemsDocument77 pagesAcctax1 AY 2016-2017 ProblemsRebekahNo ratings yet

- Art 1848-1852Document4 pagesArt 1848-1852Rea Jane B. MalcampoNo ratings yet

- Ra 11232 (Revised Corporation Code of The Philippines)Document26 pagesRa 11232 (Revised Corporation Code of The Philippines)Darryl Sarte BoocNo ratings yet

- Congress Passed A Proposed Law Creating A Corporation To Engage in Agricultural ActivitiesDocument1 pageCongress Passed A Proposed Law Creating A Corporation To Engage in Agricultural ActivitiesrockerNo ratings yet

- Law On Partnership and Corporation Study Guide de LeonDocument9 pagesLaw On Partnership and Corporation Study Guide de LeonLhorene Hope Dueñas0% (2)

- Art 1772-1774Document3 pagesArt 1772-1774CML100% (1)

- Law On Partnership and Corporation by Hector de LeonDocument41 pagesLaw On Partnership and Corporation by Hector de LeonMary Claudette Unabia100% (3)

- Notes - Law On Partnerships and Private CorporationsDocument20 pagesNotes - Law On Partnerships and Private CorporationsJeremyDream Lim100% (3)

- Law On Partnership and Corporation NotesDocument26 pagesLaw On Partnership and Corporation NotesJahzeel Y. Nolasco83% (6)

- RFBT 2 Partnership Midterm ReviewerDocument6 pagesRFBT 2 Partnership Midterm ReviewerJamaica DavidNo ratings yet

- Jose Rizal Memorial State University Main Campus, Dapitan City College of Business and AccountancyDocument6 pagesJose Rizal Memorial State University Main Campus, Dapitan City College of Business and AccountancyBernadette CaduyacNo ratings yet

- Review Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020Document30 pagesReview Materials: Prepared By: Junior Philippine Institute of Accountants UC-Banilad Chapter F.Y. 2019-2020AB CloydNo ratings yet

- Law On Partnership and Corporation Study GuideDocument109 pagesLaw On Partnership and Corporation Study GuideAlma Landero100% (1)

- Delectus PersonaeDocument59 pagesDelectus Personaeleahtabs100% (3)

- Foreign Tax CreditDocument2 pagesForeign Tax CreditSophiaFrancescaEspinosaNo ratings yet

- Article 1808-1827Document7 pagesArticle 1808-1827Janaisa Bugayong EspantoNo ratings yet

- UST Golden Notes in Partnership and AgenDocument42 pagesUST Golden Notes in Partnership and AgenDominique O. BerinoNo ratings yet

- Partnership I. Contract of Partnership 23definition: ArtnershipDocument44 pagesPartnership I. Contract of Partnership 23definition: ArtnershipHyviBaculiSaynoNo ratings yet

- Law On Partnership - Chapter 1 by DomingoDocument11 pagesLaw On Partnership - Chapter 1 by Domingojhoana morenoNo ratings yet

- Law in PartnershipDocument15 pagesLaw in Partnershipmelody agravanteNo ratings yet

- Review PartnershipDocument77 pagesReview PartnershipRoy Samuel HalasanNo ratings yet

- Mercantile Law Case Digests: Case Name Subject and Topic Facts Issue RulingDocument8 pagesMercantile Law Case Digests: Case Name Subject and Topic Facts Issue RulingJohn Dexter FuentesNo ratings yet

- CHAPTER 1 - General ProvisionDocument36 pagesCHAPTER 1 - General ProvisionziahnepostreliNo ratings yet

- Acrf Partnership and Corporation DomingoDocument42 pagesAcrf Partnership and Corporation DomingoJullie AnnNo ratings yet

- Articuna - GENERAL OVERVIEW OF THE LAW ON PARTNERSHIPDocument4 pagesArticuna - GENERAL OVERVIEW OF THE LAW ON PARTNERSHIPIrish ArticunaNo ratings yet

- Docshare - Tips - Co Ownership DigestDocument12 pagesDocshare - Tips - Co Ownership DigestRae Marie Cadeliña ManarNo ratings yet

- LAW Chapter I (1767-1783)Document11 pagesLAW Chapter I (1767-1783)JaimeMorNo ratings yet

- Transportation Law Cases.1Document140 pagesTransportation Law Cases.1Che PuebloNo ratings yet

- Learners With Emotional - OutlineDocument1 pageLearners With Emotional - OutlineChe PuebloNo ratings yet

- First Name Last NameDocument5 pagesFirst Name Last NameChe PuebloNo ratings yet

- Address One of The Students To Lead The PrayerDocument6 pagesAddress One of The Students To Lead The PrayerChe PuebloNo ratings yet

- introToLAw CasesDocument12 pagesintroToLAw CasesChe PuebloNo ratings yet

- Long Quiz in Assessment of LearningDocument2 pagesLong Quiz in Assessment of LearningChe PuebloNo ratings yet

- Buffet Service 320Document1 pageBuffet Service 320Che PuebloNo ratings yet

- Buffet Service PHP 375.00/head: (Soup, Salad, 3 Main Courses, Rice, Dessert and Drinks)Document2 pagesBuffet Service PHP 375.00/head: (Soup, Salad, 3 Main Courses, Rice, Dessert and Drinks)Che PuebloNo ratings yet

- Wedding Package 2 - P 65,000Document1 pageWedding Package 2 - P 65,000Che PuebloNo ratings yet

- 7 Ways To Generate Extra Income From HomeDocument5 pages7 Ways To Generate Extra Income From HomeChe PuebloNo ratings yet

- Buffet Service PHP 360.00/head (3 Main Courses W/ Soup, Rice, Dessert and Drinks)Document2 pagesBuffet Service PHP 360.00/head (3 Main Courses W/ Soup, Rice, Dessert and Drinks)Che PuebloNo ratings yet

- Nature of Special ProceedingsDocument479 pagesNature of Special ProceedingsChe PuebloNo ratings yet

- TAX Course OutlineDocument4 pagesTAX Course OutlineChe PuebloNo ratings yet

- QUIZ No1.Final - AssessmentDocument1 pageQUIZ No1.Final - AssessmentChe PuebloNo ratings yet

- Love QuotesDocument1 pageLove QuotesChe PuebloNo ratings yet

- Be It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledDocument54 pagesBe It Enacted by The Senate and House of Representatives of The Philippines in Congress AssembledChe PuebloNo ratings yet

- Complaint - AffidavitDocument3 pagesComplaint - AffidavitChe PuebloNo ratings yet

- Assessment of Learning 1: Long QuizDocument5 pagesAssessment of Learning 1: Long QuizChe Pueblo100% (1)

- Ids PDFDocument397 pagesIds PDFMinh Ngô HảiNo ratings yet

- The Cultural Politics of Femvertising Selling Empowerment Joel Gwynne Full Chapter PDFDocument69 pagesThe Cultural Politics of Femvertising Selling Empowerment Joel Gwynne Full Chapter PDFeachurjallai100% (5)

- Curriculam Vitae: Vemula Govinda Raju Personal DataDocument3 pagesCurriculam Vitae: Vemula Govinda Raju Personal DataAJAYNo ratings yet

- Case Study Champions League FinalDocument14 pagesCase Study Champions League FinalRakeem DavidsonNo ratings yet

- 01 - Introduction To E-CommerceDocument19 pages01 - Introduction To E-Commercehioctane10No ratings yet

- 2023 SDF Budget PlannerDocument44 pages2023 SDF Budget PlannerJoyce D. FernandezNo ratings yet

- 1988 Motorola Annual Report PDFDocument40 pages1988 Motorola Annual Report PDFmrinal1690No ratings yet

- VictoriaDocument2 pagesVictoriaapi-535156077No ratings yet

- Founder's Guide To b2b SalesDocument60 pagesFounder's Guide To b2b SalesdesignerskreativNo ratings yet

- 250,000 300,000 400,000 500,000 Cash Flow: Year 1 2 3 4Document9 pages250,000 300,000 400,000 500,000 Cash Flow: Year 1 2 3 4Kai ZhaoNo ratings yet

- Women in CryptoDocument26 pagesWomen in CryptoRodrix DigitalNo ratings yet

- How To Back Up A Database UPS (WORLDSHIP)Document2 pagesHow To Back Up A Database UPS (WORLDSHIP)Wagner Esteban Cepeda AquinoNo ratings yet

- Solved ProblemDocument4 pagesSolved ProblemSophiya NeupaneNo ratings yet

- ANS AlagangWency-2nd-quizDocument13 pagesANS AlagangWency-2nd-quizJazzy MercadoNo ratings yet

- Microservice ArchitectureDocument22 pagesMicroservice ArchitecturenamNo ratings yet

- Bs en 12Document10 pagesBs en 12Alvin BadzNo ratings yet

- Spandana Sphoorty Financial PDFDocument4 pagesSpandana Sphoorty Financial PDFdarshanmadeNo ratings yet

- Grupo 3 Crucigrama ResueltoDocument2 pagesGrupo 3 Crucigrama ResueltoKevin LancherosNo ratings yet

- Qp-Luxm-Gs & SJDocument2 pagesQp-Luxm-Gs & SJRaksha StarNo ratings yet

- S4hana CopaDocument10 pagesS4hana CopaGhosh2100% (1)

- Affidavit of incOMEDocument5 pagesAffidavit of incOMEPedro Silo100% (1)

- Ensilo/Fortiedr: Course DescriptionDocument2 pagesEnsilo/Fortiedr: Course DescriptionhoadiNo ratings yet

- Financial Institutions and Markets: Subject Code: EL15FN505Document63 pagesFinancial Institutions and Markets: Subject Code: EL15FN505Anusha RajNo ratings yet

- Developing Sustainable Tourism Product For Sailing Sapa Homestay - Rational ReportDocument73 pagesDeveloping Sustainable Tourism Product For Sailing Sapa Homestay - Rational ReportQTKD 4D-18 Vuong Thuy TrangNo ratings yet

- PoM Unit Wise QBDocument11 pagesPoM Unit Wise QBNirmal KumarNo ratings yet