Download as docx, pdf, or txt

You might also like

- Policy Paperwork 19-09508Document1 pagePolicy Paperwork 19-09508donnaintexas67100% (3)

- Risk Involved in Internet Banking of SBIDocument52 pagesRisk Involved in Internet Banking of SBIij EducationNo ratings yet

- Brijesh Project All Set To PrintDocument59 pagesBrijesh Project All Set To Printv raviNo ratings yet

- E-Banking in India: Division: C PRN: 16010324225 Program: BBALLB Semester-8thDocument16 pagesE-Banking in India: Division: C PRN: 16010324225 Program: BBALLB Semester-8thGurava reddyNo ratings yet

- Training ReportDocument65 pagesTraining ReportÂShu KaLràNo ratings yet

- E Banking ReportDocument40 pagesE Banking ReportVansh Patel100% (2)

- E-Marketing and Online BankingDocument8 pagesE-Marketing and Online BankingAnonymous CwJeBCAXpNo ratings yet

- Abhi FileDocument71 pagesAbhi FileÂShu KaLràNo ratings yet

- Rohan FinanceDocument39 pagesRohan FinanceTasmay EnterprisesNo ratings yet

- E-Bank Impact Project AkashDocument7 pagesE-Bank Impact Project AkashGAME SPOT TAMIZHANNo ratings yet

- e Banking ReportDocument40 pagese Banking Reportleeshee351No ratings yet

- MKTNG Term PaperDocument22 pagesMKTNG Term Paperbinzidd007No ratings yet

- Aditya ShindeDocument19 pagesAditya ShindeMohmmed KhayyumNo ratings yet

- Project 10davDocument49 pagesProject 10davShivam YadavNo ratings yet

- E BankingDocument18 pagesE BankingHuelien_Nguyen_1121No ratings yet

- Gouse SnyopsisDocument14 pagesGouse Snyopsisdanbaig096No ratings yet

- A Project Report OnDocument19 pagesA Project Report OnKaren WatsonNo ratings yet

- Internet BankingDocument38 pagesInternet Bankingsonalikhande100% (1)

- National Law Institute University, Bhopal: Basics of E-BankingDocument21 pagesNational Law Institute University, Bhopal: Basics of E-BankingDikshaNo ratings yet

- E Banking 1Document25 pagesE Banking 1Vivek BishiNo ratings yet

- Customers Perception Towards Online Banking Services: Vol. 2 No. 2 October 2014 ISSN: 2321 - 4643Document9 pagesCustomers Perception Towards Online Banking Services: Vol. 2 No. 2 October 2014 ISSN: 2321 - 4643hifeztobgglNo ratings yet

- Dissertation On Internet Banking in IndiaDocument8 pagesDissertation On Internet Banking in IndiaOrderAPaperBillings100% (1)

- E BankingDocument62 pagesE BankingShraddha Yellattikar89% (19)

- E Banking ReportDocument28 pagesE Banking ReportJagwinder SekhonNo ratings yet

- E - BankingDocument32 pagesE - BankingSanoj Kumar Yadav0% (1)

- Chapter 1.editedDocument15 pagesChapter 1.editedamrozia mazharNo ratings yet

- My Main ProjectDocument29 pagesMy Main ProjectRahul VermaNo ratings yet

- Project On E BankingDocument57 pagesProject On E BankingPartik Bansal100% (1)

- GOWTHAMIDocument12 pagesGOWTHAMIMohmmed KhayyumNo ratings yet

- The Role of Internet Banking and Society: C.A.Mahesh Kumar, Y.Lokesh Kumar Reddy, B.SreenivasuluDocument9 pagesThe Role of Internet Banking and Society: C.A.Mahesh Kumar, Y.Lokesh Kumar Reddy, B.SreenivasuluPavan PaviNo ratings yet

- Future of Internet Banking in IndiaDocument17 pagesFuture of Internet Banking in IndiaDrHarman Preet SinghNo ratings yet

- Role of Online Banking in Economy by Anita Bindal Phulia, Monika Sharma, Deepak KumarDocument6 pagesRole of Online Banking in Economy by Anita Bindal Phulia, Monika Sharma, Deepak Kumarijr_journalNo ratings yet

- DissertationDocument35 pagesDissertationAshutosh Kishan50% (2)

- Customer Perception On E-Banking Services - A Study With Reference To Private and Public Sector BanksDocument12 pagesCustomer Perception On E-Banking Services - A Study With Reference To Private and Public Sector BanksVenkat 19P259No ratings yet

- Role of e - Banking in Current ScenarioDocument5 pagesRole of e - Banking in Current ScenarioInternational Jpurnal Of Technical Research And ApplicationsNo ratings yet

- Prakhar BankingDocument11 pagesPrakhar BankingBharat Bhushan ShuklaNo ratings yet

- Essay # 1. Meaning of Internet Banking:: ContentsDocument8 pagesEssay # 1. Meaning of Internet Banking:: ContentsdfgsgfywNo ratings yet

- NANA VISHNU - e BankDocument10 pagesNANA VISHNU - e BankMOHAMMED KHAYYUMNo ratings yet

- Niteesh Kumar Research ReportDocument13 pagesNiteesh Kumar Research ReportBittu MallikNo ratings yet

- 10 - Chapter 3Document24 pages10 - Chapter 3Eloysa CarpoNo ratings yet

- Online BankingDocument15 pagesOnline BankingRokon UddinNo ratings yet

- Prospects and Problems of Information Technology in Banking Sector in NigeriaDocument16 pagesProspects and Problems of Information Technology in Banking Sector in NigeriaAnonymous RoAnGpANo ratings yet

- Final-Project-on-E-banking FINAL REORTDocument38 pagesFinal-Project-on-E-banking FINAL REORTrohit maddeshiyaNo ratings yet

- E Banking FerozpurDocument7 pagesE Banking FerozpurGunjan JainNo ratings yet

- Online BankingDocument43 pagesOnline BankingArafat AkramNo ratings yet

- ASIYA SULTANA - Digital BankDocument24 pagesASIYA SULTANA - Digital BankMohmmed KhayyumNo ratings yet

- A Study of Customer Perception Towards E-Banking Services Offered in Banking Sector (Accf)Document56 pagesA Study of Customer Perception Towards E-Banking Services Offered in Banking Sector (Accf)Saurabh Chawla100% (1)

- How Technology Is Helping in Increasing Operational Efficiency in Service OrganizationDocument2 pagesHow Technology Is Helping in Increasing Operational Efficiency in Service OrganizationAroon KumarNo ratings yet

- What Is The Definition of E-BankingDocument2 pagesWhat Is The Definition of E-Bankingdivyangamin100% (1)

- Introduction To E-Commerce, E-Business & E-Banking: N. Krishna VeniDocument12 pagesIntroduction To E-Commerce, E-Business & E-Banking: N. Krishna VeniAna Mae Antig CaneteNo ratings yet

- CP ReportDocument25 pagesCP ReportAdarsh KumarNo ratings yet

- E BankingDocument23 pagesE Bankingimnagin100% (1)

- Review of Some Online Banks and Visa/Master Cards IssuersFrom EverandReview of Some Online Banks and Visa/Master Cards IssuersNo ratings yet

- Evaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersFrom EverandEvaluation of Some Online Payment Providers Services: Best Online Banks and Visa/Master Cards IssuersNo ratings yet

- Evaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersFrom EverandEvaluation of Some Online Banks, E-Wallets and Visa/Master Card IssuersNo ratings yet

- Payment Collection for Small Business: QuickStudy Laminated Reference Guide to Customer Payment OptionsFrom EverandPayment Collection for Small Business: QuickStudy Laminated Reference Guide to Customer Payment OptionsNo ratings yet

- Essentials of Online payment Security and Fraud PreventionFrom EverandEssentials of Online payment Security and Fraud PreventionNo ratings yet

- Aftryp SWG PDFDocument182 pagesAftryp SWG PDFij EducationNo ratings yet

- The Trypanosomiases: SeminarDocument12 pagesThe Trypanosomiases: Seminarij EducationNo ratings yet

- Option - I: 5 SemesterDocument7 pagesOption - I: 5 Semesterij EducationNo ratings yet

- African Trypanosomiasis Gambiense, Italy: Patient 1Document3 pagesAfrican Trypanosomiasis Gambiense, Italy: Patient 1ij EducationNo ratings yet

- Risk Involved in Internet Banking of SBIDocument52 pagesRisk Involved in Internet Banking of SBIij EducationNo ratings yet

- Trypano TsetseDocument5 pagesTrypano Tsetseij EducationNo ratings yet

- DESERTATION REPORT of Om Patel 123Document62 pagesDESERTATION REPORT of Om Patel 123ij EducationNo ratings yet

- Capital and Liabilities:: Comparative Balance Sheet of HDFC Bank From 2015-2016 To 2017-2018Document1 pageCapital and Liabilities:: Comparative Balance Sheet of HDFC Bank From 2015-2016 To 2017-2018ij EducationNo ratings yet

- Filariasis Due To Wuchereria Bancrofti: February 2018Document69 pagesFilariasis Due To Wuchereria Bancrofti: February 2018ij EducationNo ratings yet

- CSR BY SBI InamDocument56 pagesCSR BY SBI Inamij Education50% (2)

- Collection Analysis:: Sponsored by ALCTS CMDS Measures & Education CommitteesDocument25 pagesCollection Analysis:: Sponsored by ALCTS CMDS Measures & Education Committeesij EducationNo ratings yet

- Cmat Sample Paper 2019Document35 pagesCmat Sample Paper 2019ij EducationNo ratings yet

- Business Policy and Strategy As A Professional Field: January 2001Document16 pagesBusiness Policy and Strategy As A Professional Field: January 2001ij EducationNo ratings yet

- J&K Bank Working Capital (Fr0nt Pages)Document15 pagesJ&K Bank Working Capital (Fr0nt Pages)ij EducationNo ratings yet

- Payshield 9000 Payshield 9000 and DUKPT Application Note PWPR April 2013Document25 pagesPayshield 9000 Payshield 9000 and DUKPT Application Note PWPR April 2013Mario NấmNo ratings yet

- Lean Canvas Example: Facebook - Advertisers + College StudentsDocument1 pageLean Canvas Example: Facebook - Advertisers + College StudentsFreddie MendezNo ratings yet

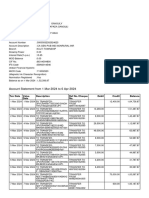

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument2 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDRISHTI MEHRANo ratings yet

- Zakat Declaration Form CZ501Document1 pageZakat Declaration Form CZ501Zahid BashirNo ratings yet

- Arris CMTS C4-RF-TroubleshootingDocument42 pagesArris CMTS C4-RF-Troubleshootingvevo Entertainment StudiosNo ratings yet

- KFS HBL Islamic Saving Account Bilingual June22Document4 pagesKFS HBL Islamic Saving Account Bilingual June22Tatheer ZeeshanNo ratings yet

- Contractor Welcome PackDocument11 pagesContractor Welcome PackerikNo ratings yet

- Case Study - ALDI & HomePlusDocument3 pagesCase Study - ALDI & HomePlusgiemansitNo ratings yet

- NCM 119 Staffing Computation ExamDocument4 pagesNCM 119 Staffing Computation ExamChristine Mae MacatangayNo ratings yet

- Sunrich: AddresssmgllwoldDocument2 pagesSunrich: AddresssmgllwoldScale ArtsInNo ratings yet

- Travel Itinerary: Supi4XDocument3 pagesTravel Itinerary: Supi4XJeffrey MendozaNo ratings yet

- Mobile Banking: A Study On Adoption by Indian UsersDocument6 pagesMobile Banking: A Study On Adoption by Indian UsersshanmukhaNo ratings yet

- Chapter 14 - Movement of MaterialsDocument15 pagesChapter 14 - Movement of MaterialsRameez RashidNo ratings yet

- Exotel Manual Get StartedDocument15 pagesExotel Manual Get StartedShekhar KumarNo ratings yet

- 5G: New Air Interface and Radio Access Virtualization: Huawei White Paper Ȕ April 2015Document11 pages5G: New Air Interface and Radio Access Virtualization: Huawei White Paper Ȕ April 2015Jose Eduardo MouraNo ratings yet

- Ticketing AbbreviationDocument3 pagesTicketing Abbreviationsaurabhjain_cool100% (1)

- Order To Cash Enterprise StructuresDocument33 pagesOrder To Cash Enterprise Structuresgpcrao143No ratings yet

- BRKDCN-2983 K8s Network DesignDocument85 pagesBRKDCN-2983 K8s Network Designsonghe zouNo ratings yet

- Your Combined Statement: Freemont Assoc LLC 370 Circle North San Diego Ca 92108Document6 pagesYour Combined Statement: Freemont Assoc LLC 370 Circle North San Diego Ca 92108Alessandro MonteiroNo ratings yet

- Lifetime Value Metrics For Subscription / A La BusinessesDocument24 pagesLifetime Value Metrics For Subscription / A La Businessesapi-20480910No ratings yet

- Gujarat Technological University: Wireless Sensor NetworksDocument2 pagesGujarat Technological University: Wireless Sensor Networkskhushali trivediNo ratings yet

- Nostalgia 2022 Registered ParticipantsDocument6 pagesNostalgia 2022 Registered ParticipantsSai Harika kNo ratings yet

- G EZWo IZIw WNa RPPNDocument3 pagesG EZWo IZIw WNa RPPNsaikat gangulyNo ratings yet

- SWF Fee Deposit SlipDocument1 pageSWF Fee Deposit SlipHarish BhatiaNo ratings yet

- Nov 2019Document1 pageNov 2019Nandan SarkarNo ratings yet

- Wa0008.Document2 pagesWa0008.chagusahoo170No ratings yet

- Competative Exams After 12Document24 pagesCompetative Exams After 12Barun SinghNo ratings yet

- Statement of Cash Flows - IAS 7Document32 pagesStatement of Cash Flows - IAS 7Ryan RascoNo ratings yet

- Bill 20100202184032 2795583Document1 pageBill 20100202184032 2795583cynthiaemmaNo ratings yet