Download as pdf or txt

You might also like

- Annex B-2 Guide, Instructions and Blank Copy: (Lone Income Payor)Document4 pagesAnnex B-2 Guide, Instructions and Blank Copy: (Lone Income Payor)Kristel Anne Liwag100% (2)

- Income Tax Return Sat-Ita22: Official StampDocument6 pagesIncome Tax Return Sat-Ita22: Official Stamptsere butsere50% (2)

- Tax Banggawan2019 Ch15BDocument17 pagesTax Banggawan2019 Ch15BNoreen Ledda100% (1)

- CH 10 TBDocument18 pagesCH 10 TBjhaydn100% (1)

- Case Studies On Direct Tax Issues in Real EstateDocument13 pagesCase Studies On Direct Tax Issues in Real EstatePremnath DegalaNo ratings yet

- 2 Residential StatusDocument30 pages2 Residential StatusVEDANT SAININo ratings yet

- Kishan Kumar Income Tax Amendments May2021Document6 pagesKishan Kumar Income Tax Amendments May2021ileshrathod0No ratings yet

- e Book PDF PDFDocument91 pagese Book PDF PDFGiri SukumarNo ratings yet

- Residential StatusDocument11 pagesResidential StatusSaurav MedhiNo ratings yet

- IT-02 Residential StatusDocument26 pagesIT-02 Residential StatusAkshat GoyalNo ratings yet

- Chapter-2 Residential StatusDocument5 pagesChapter-2 Residential StatusBrinda RNo ratings yet

- Residential Status: - Impact On Tax Liability 060820Document37 pagesResidential Status: - Impact On Tax Liability 060820Abhay GroverNo ratings yet

- Summary Book Nov 2022Document41 pagesSummary Book Nov 2022Krrish KelwaniNo ratings yet

- Residential Status and Incidence of Tax - Study MaterialDocument6 pagesResidential Status and Incidence of Tax - Study MaterialEmeline SoroNo ratings yet

- Residential Status and Tax IncidenceDocument4 pagesResidential Status and Tax IncidenceAshok Kumar MehetaNo ratings yet

- Residential Status DC 2023-24Document11 pagesResidential Status DC 2023-24avinashhpv7785No ratings yet

- Residential Status and Tax IncidenceDocument3 pagesResidential Status and Tax Incidenceambarishan mrNo ratings yet

- TTP Unit IDocument41 pagesTTP Unit IAafreen SiddiquiNo ratings yet

- Residential Status Scope of Total IncomeDocument4 pagesResidential Status Scope of Total IncomedeepakadhanaNo ratings yet

- Residential Status and Scope of Total Income - AY 2023 - 24Document12 pagesResidential Status and Scope of Total Income - AY 2023 - 24Rajan SundararajanNo ratings yet

- Residential Status and Scope of Total IncomeDocument19 pagesResidential Status and Scope of Total IncomeSamyak JainNo ratings yet

- Income Tax Cap 2Document30 pagesIncome Tax Cap 2MEGHENDRA DEV SHARMANo ratings yet

- Residential StatusDocument9 pagesResidential Statussadhana20bbaNo ratings yet

- Question BankDocument146 pagesQuestion BankSanskriti JainNo ratings yet

- Direct Tax Summary NotesDocument88 pagesDirect Tax Summary NotesAlisha LukeNo ratings yet

- 1) Residential Status of An INDIVIDUAL Ans: Residential Status For Each Previous Year - Residential Status of An Assessee IsDocument14 pages1) Residential Status of An INDIVIDUAL Ans: Residential Status For Each Previous Year - Residential Status of An Assessee Isdhananjay7No ratings yet

- Income Tax Amendment - 2021 by CA Rajat MoghaDocument46 pagesIncome Tax Amendment - 2021 by CA Rajat MoghaOm Sai Enterprises100% (1)

- MCQs of Residential Status - Incidence of Tax by CA Kishan KR SirDocument13 pagesMCQs of Residential Status - Incidence of Tax by CA Kishan KR SirHetvi VoraNo ratings yet

- Short Notes of Residential StatusDocument3 pagesShort Notes of Residential StatusutsavNo ratings yet

- Unit 3Document20 pagesUnit 3Ram KrishnaNo ratings yet

- Section 5 Which Defines The "Scope of Income" Section 6 Which Defines The "The Residential Status" of The PersonDocument8 pagesSection 5 Which Defines The "Scope of Income" Section 6 Which Defines The "The Residential Status" of The PersondipxxxNo ratings yet

- Residential StatusDocument24 pagesResidential StatusGaurav BeniwalNo ratings yet

- Definitions Residence and Tax LiabilityDocument23 pagesDefinitions Residence and Tax LiabilityVicky DNo ratings yet

- Residential Status and Tax IncidenceDocument3 pagesResidential Status and Tax IncidenceAshok Kumar Meheta0% (1)

- Amndmnt I-M'21Document25 pagesAmndmnt I-M'21kri satNo ratings yet

- 3.2 Incidence of TaxDocument5 pages3.2 Incidence of Taxswathi jaiganeshNo ratings yet

- Lesson 2 Residential Status & Scope of Total IncomeDocument27 pagesLesson 2 Residential Status & Scope of Total Income1A 10 ASWIN RNo ratings yet

- It - Lesson 3Document14 pagesIt - Lesson 3Sugandha AgarwalNo ratings yet

- Residential StatusDocument7 pagesResidential Statusjames17stevensNo ratings yet

- Chapter 11 - Residence and Scope of Total Income - NotesDocument14 pagesChapter 11 - Residence and Scope of Total Income - NotesAkshay PooniaNo ratings yet

- MB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Document70 pagesMB FM 03 TAX PLANNING AND FINANCIAL REPORTING New-1Khushboo SinghNo ratings yet

- Residential Status & Exempted IncomesDocument8 pagesResidential Status & Exempted IncomesMr UniqueNo ratings yet

- MOCK TEST of INCOME TAX WITHOUT SOLUTIONDocument19 pagesMOCK TEST of INCOME TAX WITHOUT SOLUTIONRajender SinghNo ratings yet

- Residential Status and Tax LiabilityDocument2 pagesResidential Status and Tax LiabilityPrachi AlungNo ratings yet

- 5 Sem Bcom - Income TaxDocument46 pages5 Sem Bcom - Income TaxVikranthNo ratings yet

- Presentation On Residential Status & Its Incidence On Tax LiabilityDocument13 pagesPresentation On Residential Status & Its Incidence On Tax LiabilitypriyaniNo ratings yet

- Day4 Residential Status and Incidence of Tax (9 Oct)Document12 pagesDay4 Residential Status and Incidence of Tax (9 Oct)1986anuNo ratings yet

- 4thSem-Taxation-1-Residential Status by Avinash K Prasad - 26Apr2020-DayDocument9 pages4thSem-Taxation-1-Residential Status by Avinash K Prasad - 26Apr2020-Dayvijay anandNo ratings yet

- Solution of CS PROFESSIONAL Income Tax Test by CA Vivek GabaDocument13 pagesSolution of CS PROFESSIONAL Income Tax Test by CA Vivek Gabaarohi guptaNo ratings yet

- Direct Tax Module 1 & 2Document9 pagesDirect Tax Module 1 & 2gazalashaikh910No ratings yet

- CHAPTER:-1 Definitions U/s - 2, Basis of Charge and Exclusions From Total IncomeDocument12 pagesCHAPTER:-1 Definitions U/s - 2, Basis of Charge and Exclusions From Total IncomeshyamiliNo ratings yet

- Income Tax ActDocument12 pagesIncome Tax ActSomnath GuptaNo ratings yet

- Week 4-7Document9 pagesWeek 4-7Vijayant DalalNo ratings yet

- Model Answers Taxation 1. Residential Status of Assessee Under IT Act ?Document47 pagesModel Answers Taxation 1. Residential Status of Assessee Under IT Act ?Samata BohraNo ratings yet

- Residential StatusDocument13 pagesResidential StatusABC 123No ratings yet

- Residence in IndiaDocument7 pagesResidence in IndiaSuryaNo ratings yet

- R S T I: Esidence and Cope of Otal NcomeDocument5 pagesR S T I: Esidence and Cope of Otal NcomeMnk BhkNo ratings yet

- Law of Taxation Law of Taxation Class Notes CompressDocument48 pagesLaw of Taxation Law of Taxation Class Notes CompressThrishul MaheshNo ratings yet

- The Institute of Chartered Accountants of Nepal: Suggested Answers of Income Tax and VATDocument8 pagesThe Institute of Chartered Accountants of Nepal: Suggested Answers of Income Tax and VATDipen AdhikariNo ratings yet

- Model Answers Taxation 1. Residential Status of Assessee Under IT Act ?Document44 pagesModel Answers Taxation 1. Residential Status of Assessee Under IT Act ?Tejasvini KhemajiNo ratings yet

- Model Answers Law of TaxationDocument46 pagesModel Answers Law of Taxationlavkush1234No ratings yet

- Unit 1, Part 2Document10 pagesUnit 1, Part 2Sandip Kumar BhartiNo ratings yet

- TaxationDocument15 pagesTaxationharshithaaba8No ratings yet

- Business Tax - Chapter 5Document37 pagesBusiness Tax - Chapter 5Anie MartinezNo ratings yet

- Income From Other SourcesDocument24 pagesIncome From Other Sourcesnikhilk222No ratings yet

- Data MakmurDocument3 pagesData MakmurFina LiaNo ratings yet

- Intercontinental Broadcasting Corporation V Noemi AmarilloDocument2 pagesIntercontinental Broadcasting Corporation V Noemi AmarilloYsabelleNo ratings yet

- Aeries Technology Group Private Limited: Full and Final Settlement - December 2018Document3 pagesAeries Technology Group Private Limited: Full and Final Settlement - December 2018तेजस्विनी रंजनNo ratings yet

- Detailed Contigent BillDocument3 pagesDetailed Contigent BillrhengongNo ratings yet

- Feastival 2019 InvoiceDocument1 pageFeastival 2019 InvoiceAnonymous 31FcJqNo ratings yet

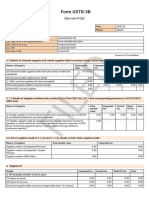

- Filed: Form GSTR-3BDocument3 pagesFiled: Form GSTR-3Bsammy shergilNo ratings yet

- Ferrer V CollectorDocument3 pagesFerrer V CollectorNico NuñezNo ratings yet

- Stationary Invoice-5080 PaidDocument2 pagesStationary Invoice-5080 PaidAnkur Agarwal100% (1)

- Taxation Law NotesDocument15 pagesTaxation Law NotesKuracha LoftNo ratings yet

- ExercisesDocument4 pagesExercisesLuân Nguyễn Đình ThànhNo ratings yet

- 5 Year Financial ProjectionsDocument2 pages5 Year Financial ProjectionsCedric JohnsonNo ratings yet

- Interglobe Aviation Ltd. (Indigo) - Balance Sheet: Figures in Rs Crore 2014 2015 2016 Sources of FundsDocument6 pagesInterglobe Aviation Ltd. (Indigo) - Balance Sheet: Figures in Rs Crore 2014 2015 2016 Sources of FundsRehan TyagiNo ratings yet

- Fundamentals of South African Income Tax 2024 CHP 9Document12 pagesFundamentals of South African Income Tax 2024 CHP 9bloomcraft.zaNo ratings yet

- Research Paper No. 2005/67: The Tax Reform Experience of KenyaDocument25 pagesResearch Paper No. 2005/67: The Tax Reform Experience of KenyaNaveen Tharanga GunarathnaNo ratings yet

- US Internal Revenue Service: Irb05-20Document72 pagesUS Internal Revenue Service: Irb05-20IRSNo ratings yet

- Solutions Manual: An Introduction To TaxDocument21 pagesSolutions Manual: An Introduction To Taxyea okayNo ratings yet

- Salary Slip: Startpoint Technologies 001Document1 pageSalary Slip: Startpoint Technologies 001PtesgNo ratings yet

- UB1Document2 pagesUB1KUNAL AMAZONNo ratings yet

- Farming Question 1Document2 pagesFarming Question 1Tawanda Tatenda HerbertNo ratings yet

- Special Economic ZoneDocument18 pagesSpecial Economic ZoneMalen Halcon ArriolaNo ratings yet

- Bevacqua 3rd Edition Chapter 3 SlidesDocument35 pagesBevacqua 3rd Edition Chapter 3 SlidesjosephrafaraciNo ratings yet

- 2 Advanced Stage TAX Module Outline Sept 2018Document5 pages2 Advanced Stage TAX Module Outline Sept 2018Aniss1296No ratings yet

- Pre Colonial Ancient Filipinos Practice Paying Taxes For The Protection From Their "Datu". The Spanish EraDocument4 pagesPre Colonial Ancient Filipinos Practice Paying Taxes For The Protection From Their "Datu". The Spanish EraAbegael Joyce RiveraNo ratings yet