Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5822)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- Format Sopl and SofpDocument3 pagesFormat Sopl and SofpMuhammad Faaiz IzzeawanNo ratings yet

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Essay QuestionsDocument16 pagesEssay Questionssheldon100% (1)

- Discussion Questions: Manila Cavite Laguna Cebu Cagayan de Oro DavaoDocument7 pagesDiscussion Questions: Manila Cavite Laguna Cebu Cagayan de Oro DavaoMae Angiela TansecoNo ratings yet

- Ebook Company Accounting 10Th Edition Leo Solutions Manual Full Chapter PDFDocument67 pagesEbook Company Accounting 10Th Edition Leo Solutions Manual Full Chapter PDFjezebelkaylinvpoqn100% (15)

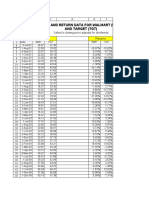

- Price and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsDocument19 pagesPrice and Return Data For Walmart (WMT) and Target (TGT) : Prices Returns Yahoo's Closing Price Adjusts For DividendsSyed Ameer Ali ShahNo ratings yet

- OBN - Small Bank Snapshot - Issue 31Document6 pagesOBN - Small Bank Snapshot - Issue 31Nate TobikNo ratings yet

- TAXN7321 - Semester PlanDocument4 pagesTAXN7321 - Semester Plansadz3690No ratings yet

- Esperenza Bakeshop, IncDocument3 pagesEsperenza Bakeshop, IncKizziah ClaveriaNo ratings yet

- Sổ tay thuế PWC 2024Document47 pagesSổ tay thuế PWC 2024Trần Thị Bích TuyềnNo ratings yet

- Assignment-2 (Cost Accounting)Document24 pagesAssignment-2 (Cost Accounting)Iqra AbbasNo ratings yet

- Massmart 2019 - RemovedDocument1 pageMassmart 2019 - RemovedtmNo ratings yet

- Analysis Costco & Walt-Mart (Ratios) FinalDocument33 pagesAnalysis Costco & Walt-Mart (Ratios) FinalVerónica Aguilar Villacís100% (1)

- Sales & Receivables JournalDocument2 pagesSales & Receivables JournalriyadiNo ratings yet

- CH-3 Advanced Financial MGTDocument53 pagesCH-3 Advanced Financial MGTMusxii TemamNo ratings yet

- ARK Autonomous Tech. & Robotics ETF: Holdings Data - ARKQDocument2 pagesARK Autonomous Tech. & Robotics ETF: Holdings Data - ARKQSpiker ValorantNo ratings yet

- Newzen Mba Finance 2022Document12 pagesNewzen Mba Finance 2022New Zen InfotechNo ratings yet

- Financial Services Provided by Anand RathiDocument65 pagesFinancial Services Provided by Anand RathimiksharmaNo ratings yet

- Batch 16 2nd Preboard (TOA)Document12 pagesBatch 16 2nd Preboard (TOA)Patrick Walters50% (2)

- Icici Bank, HDFC Bank &: Evaluation & Comparison of PerformanceDocument7 pagesIcici Bank, HDFC Bank &: Evaluation & Comparison of PerformanceNabarun MajumderNo ratings yet

- Portfolio As On 30.11.2019Document275 pagesPortfolio As On 30.11.2019ishan bapatNo ratings yet

- Horizontal AnalysisDocument6 pagesHorizontal AnalysisjohhanaNo ratings yet

- Accounting 2Document3 pagesAccounting 2Minas SydNo ratings yet

- Private Equity Portfolio Company FeesDocument78 pagesPrivate Equity Portfolio Company Feesed_nycNo ratings yet

- BAC306 - 03 Advanced Financial Accounting and ReportingDocument2 pagesBAC306 - 03 Advanced Financial Accounting and ReportingldlNo ratings yet

- Solution MERGER & ACQUISITION, CA-FINAL-SFM by CA PRAVINN MAHAJANDocument51 pagesSolution MERGER & ACQUISITION, CA-FINAL-SFM by CA PRAVINN MAHAJANPravinn_Mahajan80% (5)

- Alto 5 - Depreciation - Answer KeyDocument4 pagesAlto 5 - Depreciation - Answer KeyAlexa AbaryNo ratings yet

- Accounting Practice Set Forms ANIMEDocument20 pagesAccounting Practice Set Forms ANIMETrishia Camille SatuitoNo ratings yet

- Bukit Uluwatu 2014Document144 pagesBukit Uluwatu 2014Aida FitriNo ratings yet

- LCCI Level 3 Certificate in Accounting ASE20104 ASE20104 Sam Jul-2017Document8 pagesLCCI Level 3 Certificate in Accounting ASE20104 ASE20104 Sam Jul-2017Aung Zaw HtweNo ratings yet

- Lecture Note 02 - Bond Valuation and Yield MeasuresDocument75 pagesLecture Note 02 - Bond Valuation and Yield Measuresben tenNo ratings yet