Download as pdf or txt

You might also like

- To What Extent Did The Position of Women Improve in The Period From 1865 To 1992Document3 pagesTo What Extent Did The Position of Women Improve in The Period From 1865 To 1992Kathleen StrijdomNo ratings yet

- Body A4Document219 pagesBody A4Rodante VillaflorNo ratings yet

- The Progressive Era WorksheetDocument3 pagesThe Progressive Era Worksheetapi-298884028No ratings yet

- (Cambridge Historical Studies in American Law and Society) James D. Schmidt - Industrial Violence and The Legal Origins of Child Labor-Cambridge University Press (2010)Document305 pages(Cambridge Historical Studies in American Law and Society) James D. Schmidt - Industrial Violence and The Legal Origins of Child Labor-Cambridge University Press (2010)RamiroNo ratings yet

- The Growth and Development of Administrative LawDocument20 pagesThe Growth and Development of Administrative LawBoikobo Moseki100% (2)

- The Statuto AlbertinoDocument5 pagesThe Statuto AlbertinoMarica Dall'astaNo ratings yet

- Political Cartoons Lesson PlanDocument3 pagesPolitical Cartoons Lesson Planapi-256444300No ratings yet

- Assainment NewDocument3 pagesAssainment Newmr9898860No ratings yet

- Budget, Institutions and Fiscal Policy - Tanzi (2014)Document41 pagesBudget, Institutions and Fiscal Policy - Tanzi (2014)Maria DiazNo ratings yet

- Balanced Budgets, Fiscal Responsibility, and The Constitution: (Cato Public Policy Research Monograph No. 1)From EverandBalanced Budgets, Fiscal Responsibility, and The Constitution: (Cato Public Policy Research Monograph No. 1)No ratings yet

- Chapter 2Document10 pagesChapter 2Jimmy LojaNo ratings yet

- Was This A Period of Government GrowthDocument4 pagesWas This A Period of Government GrowthMrSilky232No ratings yet

- The End of The TreasuryDocument27 pagesThe End of The TreasuryNestaNo ratings yet

- Making Sense of The Economic MorassDocument6 pagesMaking Sense of The Economic MorassJim HickeyNo ratings yet

- Government Budget - WikipediaDocument41 pagesGovernment Budget - Wikipediapaulabishak179No ratings yet

- Generation Gap EssaysDocument8 pagesGeneration Gap Essaysafabkgddu100% (2)

- Economic History Teaching ModelDocument174 pagesEconomic History Teaching Modelleonidasleo300No ratings yet

- Evolution FMCGDocument93 pagesEvolution FMCGPrasanna VenkateshNo ratings yet

- Jack Greene On The American RevolutionDocument11 pagesJack Greene On The American Revolutionkashishsehrawat2adNo ratings yet

- The French RevolutionDocument57 pagesThe French RevolutionChristiana Oniha0% (1)

- The Rise of Managerial Bureaucracy 1St Ed Edition Lorenzo Castellani Full ChapterDocument67 pagesThe Rise of Managerial Bureaucracy 1St Ed Edition Lorenzo Castellani Full Chaptertheodore.mcavoy351100% (8)

- French Revolution Notes by KGDocument25 pagesFrench Revolution Notes by KGZhi Yi LimNo ratings yet

- Test Bank For Principles of Managerial Finance Arab World Edition Pack Lawrence J Gitman Chad J Zutter Wajeeh Elali Amer Al Roubaie 2Document35 pagesTest Bank For Principles of Managerial Finance Arab World Edition Pack Lawrence J Gitman Chad J Zutter Wajeeh Elali Amer Al Roubaie 2bibberbombycid.p13z100% (45)

- The Power of the Purse: A History of American Public Finance, 1776-1790From EverandThe Power of the Purse: A History of American Public Finance, 1776-1790No ratings yet

- Government and Administration of the United StatesFrom EverandGovernment and Administration of the United StatesNo ratings yet

- Balance of PaymentDocument15 pagesBalance of PaymentSaurav SatsangiNo ratings yet

- The Political Economy of State Reform - Political To The CoreDocument20 pagesThe Political Economy of State Reform - Political To The CoreCuztina LiuNo ratings yet

- Unit 2 Political Transition in Britain:: 2.0 ObjectivesDocument20 pagesUnit 2 Political Transition in Britain:: 2.0 ObjectivesUtkarsh DubeyNo ratings yet

- Chapter 2 IMPERIALISMDocument4 pagesChapter 2 IMPERIALISMsharief.aa90No ratings yet

- Rizal Technological University - Pasig City Graduate School StudiesDocument41 pagesRizal Technological University - Pasig City Graduate School StudiesPhilippe CamposanoNo ratings yet

- Textbook The Rise of Managerial Bureaucracy Lorenzo Castellani Ebook All Chapter PDFDocument53 pagesTextbook The Rise of Managerial Bureaucracy Lorenzo Castellani Ebook All Chapter PDFpeggy.peachey435100% (1)

- Book Edcoll 9789004277878 B9789004277878-S011-PreviewDocument2 pagesBook Edcoll 9789004277878 B9789004277878-S011-PreviewEmre Satıcı100% (1)

- Lessons of The Stimulus, by James Q. Wilson and Pietro S. NivolaDocument28 pagesLessons of The Stimulus, by James Q. Wilson and Pietro S. NivolaHoover InstitutionNo ratings yet

- Summary of Capital in the Twenty-First Century: by Thomas Piketty | Includes AnalysisFrom EverandSummary of Capital in the Twenty-First Century: by Thomas Piketty | Includes AnalysisNo ratings yet

- Summary of Capital in the Twenty-First Century: by Thomas Piketty | Includes AnalysisFrom EverandSummary of Capital in the Twenty-First Century: by Thomas Piketty | Includes AnalysisNo ratings yet

- CH4.Anne Booth - Varieties of ExploitationDocument46 pagesCH4.Anne Booth - Varieties of ExploitationIxionNo ratings yet

- StateDocument21 pagesStateAdrian DeoancaNo ratings yet

- The Origins of French RevolutionDocument6 pagesThe Origins of French Revolutionsumedha bhowmick100% (1)

- Public FinanceDocument61 pagesPublic FinancePlatonic100% (9)

- Backhaus & Wagner - From Continental Public Finance To Public Choice - Mapping ContinuityDocument32 pagesBackhaus & Wagner - From Continental Public Finance To Public Choice - Mapping ContinuityIsra LopezNo ratings yet

- Origins of French RevolutionDocument7 pagesOrigins of French Revolution98No ratings yet

- Protestant Road To Bureaucracy.Document50 pagesProtestant Road To Bureaucracy.Emilio Lautaro Cornejo ArayaNo ratings yet

- Who Decides in Last Resort? Elected Officials and Judges in Historical PerspectiveDocument12 pagesWho Decides in Last Resort? Elected Officials and Judges in Historical PerspectiveYannis KoutsangelouNo ratings yet

- Chapter 3 Political DevelopmentDocument5 pagesChapter 3 Political DevelopmentMarivic CaderaoNo ratings yet

- Neo Constitutional Is MDocument20 pagesNeo Constitutional Is MFausto CésarNo ratings yet

- French RevolutionDocument28 pagesFrench Revolutiontayyab236100% (1)

- Part Iithe Development of Public FinanceDocument6 pagesPart Iithe Development of Public FinanceJo Che RenceNo ratings yet

- Chapter 16 International Political Economy I: Theory & HistoryDocument22 pagesChapter 16 International Political Economy I: Theory & Historyunique20No ratings yet

- The Academy of Political Science Political Science QuarterlyDocument9 pagesThe Academy of Political Science Political Science QuarterlyRicardo CruzNo ratings yet

- Duque, Nicole Marie T. Bsa 2ADocument3 pagesDuque, Nicole Marie T. Bsa 2ANicole MarieNo ratings yet

- Studiu Anuar 2010 - BalogDocument12 pagesStudiu Anuar 2010 - BalogIosif Marin BalogNo ratings yet

- Byrd and Chens Canadian Tax Principles 2011 2012 Edition Canadian 1st Edition Byrd Test BankDocument32 pagesByrd and Chens Canadian Tax Principles 2011 2012 Edition Canadian 1st Edition Byrd Test BankMarkBakersxnrNo ratings yet

- Functions of French Constituent AssemblyDocument5 pagesFunctions of French Constituent AssemblyDibakarMajumderNo ratings yet

- 1.2 The Traditions of State AuditDocument5 pages1.2 The Traditions of State AuditYessie Marwah FauziahNo ratings yet

- Welfarestate in Historical PerspectiveDocument40 pagesWelfarestate in Historical PerspectiveIm Stuck With THisNo ratings yet

- Production and Public Powers in Classical AntiquityFrom EverandProduction and Public Powers in Classical AntiquityE. Lo CascioNo ratings yet

- Pa 241 Introduction To Public Fiscal Administration: Dr. Luzviminda G. Manangan - Ozarraga ProfessorDocument40 pagesPa 241 Introduction To Public Fiscal Administration: Dr. Luzviminda G. Manangan - Ozarraga ProfessorMomoNo ratings yet

- Social Origins of Protestant ReformationDocument19 pagesSocial Origins of Protestant Reformationapi-307981601No ratings yet

- Instant Download Microelectronic Circuits Analysis and Design 2nd Edition Rashid Solutions Manual PDF Full ChapterDocument33 pagesInstant Download Microelectronic Circuits Analysis and Design 2nd Edition Rashid Solutions Manual PDF Full Chaptergisellesamvb3100% (6)

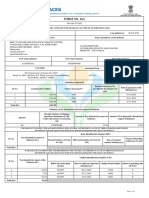

- Form No. 16A: From ToDocument2 pagesForm No. 16A: From ToAkriti JhaNo ratings yet

- English PDFDocument58 pagesEnglish PDFAkriti JhaNo ratings yet

- Council For The Indian School Certificate ExaminationsDocument1 pageCouncil For The Indian School Certificate ExaminationsAkriti JhaNo ratings yet

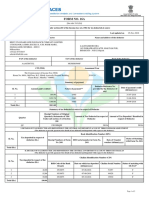

- Form No. 16A: From ToDocument2 pagesForm No. 16A: From ToAkriti JhaNo ratings yet

- Economics: Council For The Indian School Certificate ExaminationsDocument34 pagesEconomics: Council For The Indian School Certificate ExaminationsAkriti JhaNo ratings yet

- On Titan CompanyDocument14 pagesOn Titan CompanyAkriti JhaNo ratings yet

- Kpo in India and It'S Impact On Indian Economy: KeywordsDocument5 pagesKpo in India and It'S Impact On Indian Economy: KeywordsAkriti JhaNo ratings yet

- Bank Reconciliation Statement: Learning OutcomesDocument33 pagesBank Reconciliation Statement: Learning OutcomesAkriti JhaNo ratings yet

- A Case Study On Recruitment & Selection-The HR Aspect in RetailDocument10 pagesA Case Study On Recruitment & Selection-The HR Aspect in RetailAkriti JhaNo ratings yet

- ISC English Language Paper 1 2016 Solved PaperDocument14 pagesISC English Language Paper 1 2016 Solved PaperAkriti JhaNo ratings yet

- Aralin 17Document13 pagesAralin 17Marinela Juanatas GravidezNo ratings yet

- Council For The Indian School Certificate ExaminationsDocument1 pageCouncil For The Indian School Certificate ExaminationsAkriti JhaNo ratings yet

- Economics Project: Name: Akriti Jha STD - XII Commerce Roll No.: 2Document1 pageEconomics Project: Name: Akriti Jha STD - XII Commerce Roll No.: 2Akriti JhaNo ratings yet

- 7 Progressive Era Infographic Gilder LehrmanDocument1 page7 Progressive Era Infographic Gilder LehrmanCherry WhippleNo ratings yet

- Lesson Plan: Reason Assembly Chart Introduction: This Lesson Plan Will Provide Students With Experience Searching ForDocument5 pagesLesson Plan: Reason Assembly Chart Introduction: This Lesson Plan Will Provide Students With Experience Searching Forjeremie_smith_1No ratings yet

- History FairDocument5 pagesHistory Fairapi-391006015No ratings yet

- Hasenfeld - Garrow.nonprofits and Rights Advocacy - BARRIERSDocument29 pagesHasenfeld - Garrow.nonprofits and Rights Advocacy - BARRIERSjany janssenNo ratings yet

- 293 - Tone Andrea-The-Business-of-Benevolence-Industrial-Paternalism-in-Progressive-AmericaDocument333 pages293 - Tone Andrea-The-Business-of-Benevolence-Industrial-Paternalism-in-Progressive-AmericaLuis F CastrillonNo ratings yet

- APUSH Final Review - Google DocsDocument19 pagesAPUSH Final Review - Google DocsElizabeth LeeNo ratings yet

- Ch. 20 Brinkley 14Document34 pagesCh. 20 Brinkley 14baashii4No ratings yet

- Progressive Era Study Guide KEYDocument5 pagesProgressive Era Study Guide KEYRichard Cormier100% (1)

- APUSH Spring Semester SyllabusDocument6 pagesAPUSH Spring Semester SyllabusJimmy HunNo ratings yet

- Roaring Twenties: Unit 7 - Rise & Fall of ProsperityDocument71 pagesRoaring Twenties: Unit 7 - Rise & Fall of ProsperityNatalja KalarashNo ratings yet

- History of The United StatesDocument2 pagesHistory of The United StatesMohammad Ashraf OmarNo ratings yet

- Hist 1302 Exam 1 Review GMLDocument18 pagesHist 1302 Exam 1 Review GMLAnna Nguyen100% (1)

- Annotated BibliographyDocument3 pagesAnnotated Bibliographyapi-277610724No ratings yet

- Open-Ended Questions Progressive Era Test - Period 8Document3 pagesOpen-Ended Questions Progressive Era Test - Period 8Grdzelo gg5No ratings yet

- The Jungle Excerpt Questions and HIPPDocument5 pagesThe Jungle Excerpt Questions and HIPPrx dfNo ratings yet

- Unit 5Document12 pagesUnit 5Elvis BeckerNo ratings yet

- Learning Segment Educ 376 4Document14 pagesLearning Segment Educ 376 4api-489274706No ratings yet

- America's History Chapter 20: The Progressive EraDocument13 pagesAmerica's History Chapter 20: The Progressive Erairregularflowers100% (3)

- 00 Years A Centennial History of TheDocument213 pages00 Years A Centennial History of Theعبدالله سحيماتNo ratings yet

- The Enduring Vision Chapter 21Document34 pagesThe Enduring Vision Chapter 21Erna DeljoNo ratings yet

- (Williams-Ford Texas A&m University Military History Series) Dr. Nancy Gentile Ford - Americans All! - Foreign-Born Soldiers in World War I - TAMU Press (2001)Document217 pages(Williams-Ford Texas A&m University Military History Series) Dr. Nancy Gentile Ford - Americans All! - Foreign-Born Soldiers in World War I - TAMU Press (2001)Jose Mogrovejo PalomoNo ratings yet

- Scope Sequence FormatDocument7 pagesScope Sequence Formatapi-590702812No ratings yet

- Document Based Question 3: Progressive ReformDocument3 pagesDocument Based Question 3: Progressive Reformtwisted-revelation75% (4)

- Progressive Era Weekly PlanDocument4 pagesProgressive Era Weekly PlanNic HaabNo ratings yet

- USA HistoryDocument3 pagesUSA Historyslovak.jaNo ratings yet

- 2019 LASAForum Vol50 Issue3Document108 pages2019 LASAForum Vol50 Issue3Carlos Abreu MendozaNo ratings yet