Download as docx, pdf, or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5824)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (852)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (903)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (541)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (823)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (403)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- Book Report of My Brother, My Executioner byDocument7 pagesBook Report of My Brother, My Executioner bycrimsonlover17% (6)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- Communication Law Outline - 2015Document57 pagesCommunication Law Outline - 2015ifplaw0% (1)

- HLTWHS004 Learner Guide V 2.1Document70 pagesHLTWHS004 Learner Guide V 2.1rasna kc100% (4)

- WHSmith Strategy Evaluation and SelectionDocument25 pagesWHSmith Strategy Evaluation and SelectionMs. Yvonne Campbell100% (1)

- Sentence Structure NotesDocument9 pagesSentence Structure NotesNur HaNo ratings yet

- A1 Course BKDocument127 pagesA1 Course BKMs. Yvonne CampbellNo ratings yet

- Assgnmt 2 UK EconomyDocument24 pagesAssgnmt 2 UK EconomyMs. Yvonne CampbellNo ratings yet

- Unit 7 Noun ClauseDocument101 pagesUnit 7 Noun ClauseMs. Yvonne Campbell0% (1)

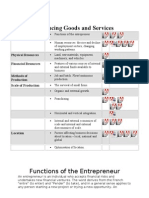

- BS1 2 Producing Goods and ServicesDocument42 pagesBS1 2 Producing Goods and ServicesMs. Yvonne CampbellNo ratings yet

- BS2 1 Marketing 2Document39 pagesBS2 1 Marketing 2Ms. Yvonne CampbellNo ratings yet

- Module BS1: The Business FrameworkDocument27 pagesModule BS1: The Business FrameworkMs. Yvonne CampbellNo ratings yet

- Identification and Analysis of The Business Strategy Formulation and Planning According To Shell Group PLCDocument37 pagesIdentification and Analysis of The Business Strategy Formulation and Planning According To Shell Group PLCMs. Yvonne Campbell100% (3)

- Marketing Concept M N S Case StudyDocument19 pagesMarketing Concept M N S Case StudyMs. Yvonne Campbell100% (1)

- NPV Budgets Managing FinanceDocument43 pagesNPV Budgets Managing FinanceMs. Yvonne CampbellNo ratings yet

- Cost of Finance and PlanningDocument16 pagesCost of Finance and PlanningMs. Yvonne CampbellNo ratings yet

- Stock Control Investment AppraisalDocument18 pagesStock Control Investment AppraisalMs. Yvonne CampbellNo ratings yet

- Puente Temburong, Brunei - Diseño de Dos Puentes AtirantadosDocument7 pagesPuente Temburong, Brunei - Diseño de Dos Puentes AtirantadosRONALD ABRAHAM SAMCA MONTAÑONo ratings yet

- Infrastructure Planning For Sustainable CitieDocument8 pagesInfrastructure Planning For Sustainable CitieAbdullah KhalilNo ratings yet

- Tenses Exercise (Paraphrasing)Document11 pagesTenses Exercise (Paraphrasing)Avtar DhaliwalNo ratings yet

- Unit 18 Global Business Environment: Student Name: Student IDDocument16 pagesUnit 18 Global Business Environment: Student Name: Student IDFahmina AhmedNo ratings yet

- Ficha Tecnica Caja SupernovaDocument2 pagesFicha Tecnica Caja SupernovaELIANA MARÍA SERNA VÉLEZ ALIANZAS ELÉCTRICAS S.A.SNo ratings yet

- Church of The Province of South East AsiaDocument6 pagesChurch of The Province of South East Asiabrian2chrisNo ratings yet

- Gmail - You Deserve It Scholarship ConfirmationDocument2 pagesGmail - You Deserve It Scholarship Confirmationapi-347833011No ratings yet

- Debat Bahasa InggrisDocument4 pagesDebat Bahasa Inggrisnadela981No ratings yet

- Uighur Culture HandbookDocument104 pagesUighur Culture HandbookAnonymous 5LDWNsNo ratings yet

- Q1-Lesson 1 - Activity 1-Pre-Assessment - MULTIPLE CHOICE: Choose The Letter of The Correct AnswerDocument4 pagesQ1-Lesson 1 - Activity 1-Pre-Assessment - MULTIPLE CHOICE: Choose The Letter of The Correct AnswerLANY T. CATAMINNo ratings yet

- Composed By: Ghanwa Shoukat DATE: 24-MARCH-2015 Jinnah Degree College of Commerce&Management Sciences Chapter#4 Hire Purchase AccountsDocument48 pagesComposed By: Ghanwa Shoukat DATE: 24-MARCH-2015 Jinnah Degree College of Commerce&Management Sciences Chapter#4 Hire Purchase AccountsshahgaloneNo ratings yet

- Pmsonline - Bih.nic - in Pmsedubcebc2223 (S (3fpo11xwuqnlp5xcehwxy3yb) ) PMS App StudentDetails - Aspx#Document3 pagesPmsonline - Bih.nic - in Pmsedubcebc2223 (S (3fpo11xwuqnlp5xcehwxy3yb) ) PMS App StudentDetails - Aspx#MUSKAN PRNNo ratings yet

- Travel Agency BrochureDocument2 pagesTravel Agency BrochureAnonymous PilotsNo ratings yet

- Thesis Lovely BonesDocument7 pagesThesis Lovely Bonesreneefrancoalbuquerque100% (2)

- Small Wonder, SummariesDocument3 pagesSmall Wonder, SummariessagarchesterNo ratings yet

- Interoperability Best Practices: Testing and Validation ChecklistDocument4 pagesInteroperability Best Practices: Testing and Validation ChecklistsusNo ratings yet

- Patent Cooperation TreatyDocument11 pagesPatent Cooperation Treatyanubha0608_169697711No ratings yet

- Istilah Akuntansi EnglishDocument2 pagesIstilah Akuntansi Englishpramesari dinarNo ratings yet

- NEPRA Excessive Billing Inquiry ReportDocument14 pagesNEPRA Excessive Billing Inquiry ReportKhawaja BurhanNo ratings yet

- Uj2 48 52Document5 pagesUj2 48 52AS BaizidiNo ratings yet

- CS Unitec - ATEX - Working in Ex ZonesDocument2 pagesCS Unitec - ATEX - Working in Ex Zonesmate_matic34No ratings yet

- Debrahlee Lorenzana - A Hot Case StudyDocument3 pagesDebrahlee Lorenzana - A Hot Case StudyHarish SunderNo ratings yet

- ESSA - Ammonia Low Carbon EnergyDocument2 pagesESSA - Ammonia Low Carbon EnergyFauzi BahananNo ratings yet

- Texas Laws About Claiming A Dead Body and Having A Family FuneralDocument3 pagesTexas Laws About Claiming A Dead Body and Having A Family Funeralclint11No ratings yet

- Examples: 2.: Environment AestheticsDocument1 pageExamples: 2.: Environment AestheticsKanding ni SoleilNo ratings yet

- Proposed Rule: Pistachios Grown In— CaliforniaDocument5 pagesProposed Rule: Pistachios Grown In— CaliforniaJustia.comNo ratings yet