Professional Documents

Culture Documents

International Taxation: A Capsule For Quick Recap

International Taxation: A Capsule For Quick Recap

Uploaded by

Shubham jindalOriginal Title

Copyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

International Taxation: A Capsule For Quick Recap

International Taxation: A Capsule For Quick Recap

Uploaded by

Shubham jindalCopyright:

Available Formats

INTERNATIONAL TAXATION

International Taxation:

A Capsule for Quick Recap

Globalisation, capital mobility and increased trade and services have resulted in the whole world virtually becoming

one market and consequently, international taxation has become a key concern area both for business enterprises

engaged in cross border transactions as well as for tax administrations of the concerned States. Considering its

significance, international taxation has been included as a dedicated part (i.e., Part-II) for 30 marks in Final (New)

Paper 7: Direct Tax Laws & International Taxation in the New Scheme of Education and Training.

In this capsule, diagrams, tables and flow charts have been extensively used to help you recap the significant

concepts, provisions and principles relating to international taxation, which have been discussed in detail in

Module 4 [International Taxation] of September 2018 edition of Study Material of Final (New) Paper 7. The Capsule

is divided into eight chapters in line with Module 4 of the Study Material. It may be noted that Chapters 1 to 5 of

Module 4 is relevant for Final (Old) Paper 7: Direct Tax Laws also, and to that extent this capsule is relevant for Final

(Old) course students also. As indicated in the title, remember that the capsule will only serve as a quick recap for

May 2019 and Nov 2019 Examinations. For comprehensive study, read the Study Material and RTP.

CHAPTER 1: NON RESIDENT TAXATION

The residential status of a person determines the scope of income to be included in his/its total income (TI), which

is subject to income-tax in India. The provisions for determining the residential status of a person are contained in

section 6 and the scope of TI is defined u/s 5 of IT Act, 1961.

Fig 1.1

RESIDENCE IN INDIA [SECTION 6]

(I) INDIVIDUAL

The residential status of an individual is determined on the basis of the period of his stay in India.

Basic conditions:

(i) He must be present in India for a period of 182 days or more during the previous year (P.Y.); or

(ii) He must be present in India for a period of 60 days or more during the P.Y. and 365 days or more during the 4 years

immediately preceding the relevant P.Y.

Cases where condition (ii) is not applicable:

(a) Where an Indian citizen leaves India during the P.Y. for the purpose of employment outside India or as a member of the crew

of an Indian ship;

(b) Where an Indian citizen or a person of Indian origin who, being outside India, comes on a visit to India during the P.Y.

Additional conditions:

(1) He is a resident in at least 2 out of 10 PYs preceding the relevant P.Y.;

(2) His stay in India in the last 7 years preceding the relevant P.Y. is 730 days or more.

Resident and ordinarily resident (ROR) Resident but not ordinarily resident (RNOR) Non-resident (NR)

Must satisfy at least one of the basic conditions Must satisfy at least one of the basic conditions [(i) Must not satisfy either of the

[(i) or (ii)] and both the additional conditions or (ii)] and one or none of the additional conditions basic conditions [Neither (i)

[(1) & (2)]. [(1) or (2) or neither]. nor (ii)].

(II) COMPANY Determination of POEM on the basis of ABOI test

A company is said to be engaged in ABOI, if it fulfills

The Co. the cumulative conditions:

Is the Co. an No Whether POEM No is a NR

Indian Co.? of the Co. is for the Its passive

in India in the relevant Less than Less than Payroll

income*

relevant P.Y.? P.Y. 50% of its 50% of expenses

Yes (wherever

total assets the total incurred

Yes earned) is 50%

situated in number of on such

or less of its

India employees employees

total income

are situated are less than

in India or 50% of its

The Co. is

a resident are residents total payroll

in India POEM – Place of Effective in India expenditure

for the Management

relevant

* Passive income of a company shall be aggregate of:

P.Y.

(i) Income from the transactions where both the purchase and sale

of goods is from/ to its AEs; and

(ii) Income by way of royalty, dividend, capital gains, interest

(except for banking Cos and public financial institutions) or

rental income, whether or not involving AEs.

The Chartered Accountant Student January 2019 05

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

Active Business Outside

India (ABOI)

Companies fulfilling the Companies other than those

test of ABOI fulfilling the test of ABOI

• POEM outside India, if majority BOD meetings are Stage 1: Identification of persons who actually make

held outside India the key management and commercial decision for

• If de facto decision making authority is not BOD conduct of the company’s business as a whole

but Indian holding Co. or any other person Stage 2: Determination of place where these decisions

resident in India, POEM shall be in India are, in fact, made

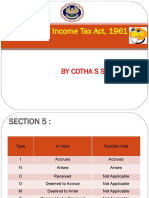

SCOPE OF TOTAL INCOME [SECTION 5]: Whether the following incomes are to be included in TI?

Particulars ROR RNOR NR

Income received or deemed to be

received in India during the relevant Yes Yes Yes

P.Y.

Income accruing or arising or

deeming to accrue or arise in India Yes Yes Yes

during the relevant P.Y.

Income accruing or arising outside Yes, even if such income is not Yes, but only if such income is

India during the relevant P.Y. received or brought into India derived from a business controlled

during the P.Y. from or profn set up in India; No

Otherwise, No.

Fig 1.2

Income deemed to accrue or arise in

India [Section 9(1)]

Salary earned Income Salary payable

for services Dividend Interest, Royalty, FTS, if

accruing or by the Govt.

rendered in paid by an if payable if payable payable by

arising outside to an Indian

India Indian Co. by by

India, directly Citizen for outside India

or indirectly, services

through or rendered

from outside India

Government Person resident

A non resident in India

Any Business

Connection in India Exceptions

If debt incurred or money

is borrowed and used for If debt incurred or money

the purpose of business or is borrowed and used or

Any property/ asset profn carried on in India technical services or royalty

or source of income in services are utilised for the

India purpose of business or profn

If technical services or royalty carried on outside India

services are utilised for the

Transfer of capital purpose of business or profn

If the money is borrowed and

carried on in India or earning used or technical services or

asset situated in India

income from any source in India royalty services are utilised

for earning income from any

source outside India

06 January 2019 The Chartered Accountant Student

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

Fig 1.3

Income exempted specifically in the hands of Non-residents [Section 10]

Section Income Available to

10(4)(ii) Int on money standing to the credit in a NRE A/c of an individual (indvl) in any bank Indvl resident outside

in India as per the FEMA Act, 1999 India (under FEMA Act)

or an indvl who has been

permitted to maintain said

account by RBI

10(6)(ii) Remuneration (Remn) recd by Foreign Diplomats/ Consulate and their staff Indvl (not being a citizen

Conditions: of India)

1. The remn recd by our corresponding Govt. officials/member of staff resident in

such foreign countries should be exempt.

2. The member of staff should be the subjects of the respective countries and should

not be engaged in any other business or profn or employment in India.

10(6)(vi) Remn recd as an employee of a foreign enterprise(FE) for services rendered by him Indvl - Salaried Employee

during his stay in India, if: (not being a citizen of

a) FE is not engaged in any trade or business in India; India) of a FE

b) His stay in India does not exceed 90 days in aggregate in such P.Y.; and

c) Such remn is not liable to be deducted from the income of employer chargeable

under IT Act

10(6)(viii) Salary recd by or due for services rendered in connection with his employment on a Indvl - Salaried Employee

foreign ship if his total stay in India does not exceed 90 days in the P.Y. (NR who is not a citizen of

India) of a foreign ship

10(6)(xi) Remn recd as an employee of the Govt. of a foreign State during his stay in India in Indvl - Salaried Employee

connection with his training in any Govt. Office/ State Undertaking/ corporation/ (not being a citizen of

registered society etc. India) of Govt. of foreign

State

10(6BB) Tax paid by Indian Co., engaged in the business of operation of aircraft, which has Govt. of foreign State or FE

acquired an aircraft or an aircraft engine on lease, under an approved (by CG) agrmt, (i.e., a person who is a NR)

on lease rental/income derived (other than payt for providing spares or services in

connection with operation of leased aircraft) by the Govt. of a foreign State or FE.

10(6C) Royalty income or FTS under an agrmt with the Central Government (CG) for Foreign Co. (notified by

providing services in or outside India in projects connected with security of India the CG)

10(6D) Royalty income from or FTS rendered in or outside India to, the National Technical Non-corporate NR and

Research Organisation (NTRO) foreign Co.

10(15)(iii)(a) Int on deposits made by a foreign bank with any scheduled bank with approval of RBI. Bank incorporated outside

India and authorised to

perform Central Banking

functions in that country.

10(15)(iv)(fa) Int payable by scheduled bank on deposits in foreign currency (FC) where the a) NR or

acceptance of such deposits is duly approved by RBI. [Scheduled bank does not include b) Indvl or HUF, being

co-operative bank] a resident but not

10(15)(viii) Int on deposit made on or after 01.04.2005 in an Offshore Banking Unit ordinarily resident

10(48) Income received in India in Indian currency on a/c of sale of crude oil or any other Foreign Co. on a/c of sale of

goods or rendering of services as may be notified by the CG in this behalf. Foreign Co. crude oil, any other goods

and agreement (agrmnt) should be notified by the CG in national interest. or rendering of service. It

should not be engaged in

any other activity in India.

10(48A) Income accruing or arsing on a/c of storage of crude oil in a facility in India and sale of Foreign Co.

crude oil therefrom to any person resident in India. Foreign Co. and agrmnt should be

notified by the CG in national interest.

10(48B) Income from sale of leftover stock of crude oil from facility in India after the expiry of Foreign Co.

agrmt ref u/s 10(48A) or on termination of the said agrmt

The Chartered Accountant Student January 2019 07

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

Fig 1.4

Presumptive Income provisions applicable to NRs

Particulars Section 44B Section 44BBA Section 44BB Section 44BBB

Nature of Shipping Operation of aircraft Business of providing services or Business of civil construction

business business facilities in connection with, or or the business of erection

supplying P & M on hire used, or to of P&M or testing or

be used, in the prospecting for, or commissioning thereof, in

extraction or production of, mineral connection with turnkey

oils power projects approved by

the CG.

Eligible NR NR NR Only Foreign Co.

assessee

Presumptive 7.5% of specified 5% of specified sum 10% of specified sum 10% of specified sum

income sum

Specified (i) Amt paid or payable on a/c of carriage (i) Amt paid or payable on a/c Amt paid or payable on a/c

sum of passengers, livestock, mail or goods of the provn of such services of such civil construction,

shipped at/ from any port/place in or facilities for the aforesaid erection, testing or

India; and purposes in India; and commissioning

(ii) Amt recd or deemed to be recd in India (ii) Amt recd or deemed to be recd

on a/c of the carriage of passengers, in India on a/c of the provn of

livestock mail or goods shipped at/ services or facilities for the

from any port/place outside India aforesaid purpose outside India.

Option to Not available Lower profits may be claimed u/s 44BB and u/s 44BBB provided the

declare assessee maintains BOA u/s 44AA and gets them audited u/s 44AB.

lower profits

Fig 1.5

Dedn of HO exp in case of NRs while computing PGBP

Lower of

5% of adjusted TI Amt. of HO exp incurred by the NR attributable to the business or

profn in India

Meaning of Adj. TI Meaning of HO exp

TI, without giving effect to:

(i) HO exp Executive and general admin exp incurred by the NR outside India, incl:

(i) Unabsorbed depreciation (a) Rent, rates, taxes, repairs or ins of any premises outside India used for

(ii) Capital exp. on family planning business or profn

(iii) Losses c/f : (b) Salary, wages, perqs etc. to any employee or other person managing the

Business loss u/s 72(1) affairs of any office outside India

Spec. bus. Loss u/s 73(2) (c) Travelling exp by any employee or other person managing the affairs of any

LTCL/STCL u/s 74(1) office outside India

Loss from owning and maintaining (d) Such other executive and general admin exp prescribed

race horses u/s 74A(3)

(iv) Dedns under Chap VI-A from GTI

08 January 2019 The Chartered Accountant Student

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

Fig 1.6

Chapter XII-A : Special Provisions relating to certain incomes of NR individual, being a

citizen of India or person of Indian Origin

Investment LTCG relating to LTCG of an asset, other

than a specified asset Other Income

Income1 from FEA FEA, being a LTCA

Rate of 10% 20% Normal rates of tax

20%

tax

Dedn for Not Allowable. However, Allowable. Allowable

exp or allowable benefit of indexation Benefit of indexation

allowance of COA is not of COA is available.

available.

Dedn under Not

Chapter Not allowable Not allowable Allowable

allowable

VI-A

Exemption Allowable

u/s 115F

If entire net consideration is invested in If part of net consideration is invested in

specified asset (new asset) specified asset (new asset)

Exemption of entire LTCG Exemption of proportionate LTCG

In case of transfer of new asset/conversion into Exempted LTCG deemed to be income

money within 3 years of acquisition chargeable to tax in the year of transfer

1

Other than dividend referred to in section 115-O

Fig 1.7

Fig 1.6 (Contd.) Special provisions for computing tax on income by way of

interest and dividend [Section 115A]

Meaning of Foreign Exchange Asset (FEA) Where the total income of a NR includes any income Rate of

by way of Tax

(1) Dividends [other than dividend ref u/s 115-O] 20%

(2) Interest recd from the Govt. or an Indian concern 20%

Acquired/purchased/ on moneys borrowed or debt incurred by the Govt./

Specified asset subscribed to in convertible Indian concern in FC, other than (3), (4), (5) and (6)

foreign exchange mentioned below

(3) Interest received from an infrastructure debt fund 5%

ref u/s 10(47)

Shares in an Indian Co.

(4) Interest ref u/s 194LC [Refer Fig. 1.11] 5%

Debentures issued by an Indian Co. (other than a Pvt. (5) Interest ref u/s 194LD [Refer Fig. 1.11] 5%

Co.)

(6) Interest ref u/s 194LBA(2) [Refer Fig. 1.11] 5%

Deposits with an Indian Co. (other than a Pvt. Co.) (7) Income received in respect of units purchased in FC 20%

of a mutual fund (MF) specified u/s 10(23D) or UTI

Notes:

Any security of the CG • No dedn in respect of any exp or allowance shall be allowed u/s 28

to 44C and 57.

• Dedn under Chapter VI-A is not available.

Other assets notified by the CG • The assessee is not required to furnish a return of his income (ROI)

if the following conditions are satisfied:

(a) The TI consists of only the abovementioned incomes and

(b) TDS has been deducted from such income.

The Chartered Accountant Student January 2019 09

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

Fig 1.8

Tax treatment of Royalty & FTS received from Govt / Ind. Concern in pursuance of approved agrmt

Is right, property or contract effectively connected with PE/Fixed Place of Profn (FPP) in India?

Yes No

Royalty & FTS would be computed as per sec 44DA under the head Concessional rate of tax@10% u/s 115A on

“PGBP” as per the provisions of the IT Act, 1961; and normal rates of gross royalty/FTS would apply

tax would apply

No dedn of any exp or allowance is allowable

u/s 28 to 44C or u/s 57

A/cs & Audit Dedn of exp Dedn under Chap VI-A permissible

No exemption from

filing ROI u/s 139(1)

BoA to be No dedn in resp of No dedn in respect of

BoA to be exp not incurred amts paid (other than

maintained as

audited & Audit wholly & exclusively reimbursement of

per sec 44AA

Report to be in relation to PE/ actual exp) by PE/FPP

furnished along FPP in India to HO & other offices

with ROI

Fig 1.9

Special provisions for computing tax on income of FIIs from securities [Section 115AD]

S. No. Income Rate of Tax

(a) Income recd in respect of securities other than 20%

• income by way of dividends ref u/s 115-O

• income on units ref u/s 115AB i.e., units of MF specified u/s 10(23D) or UTI

• Interest ref u/s 194LD

(b) Interest referred u/s 194LD [Refer Fig 1.11] 5%

(c) Income by way of STCG arising from the transfer of securities (other than STCG u/s 111A) 30%

(d) Income by way of STCG u/s 111A 15%

(e) Income by way of LTCG arising from the transfer of securities (other than LTCG u/s 112A) 10%

(f ) Income by way of LTCG u/s 112A exceeding R 1 lakh 10%

Notes:

• No dedn for any exp or allowance shall be allowed u/s 28 to 44C and 57 from income from securities (ref. to in (a) and (b) above).

• Dedn under Chapter VI-A is not allowable in case of income from securities, STCG or LTCG arising from transfer of securities.

• Conversion to foreign currency and indexation benefit would not be available while computing capital gains on transfer of securities.

Fig 1.10

Special provisions for computing tax in case of NR sportsmen or sports associations [Section 115BBA]

S. No. Assessee Income Rate of Tax

(a) A sportsman (including Any income recd or receivable by way of—

an athlete), who is not a (i) participation in India in any game (other than a game winnings wherefrom are

citizen of India and is a taxable u/s 115BB) or sport; or

NR (ii) advertisement; or

(iii) contribution of articles relating to any game or sport in India in newspapers,

magazines or journals;

(b) A NR sports association Any amt guaranteed to be paid or payable to such association or institution in relation 20%

or institution to any game (other than a game the winnings wherefrom are taxable u/s 115BB) or

sport played in India

(c) An entertainer who is not Any income recd or receivable from his performance in India

a citizen of India and is a

NR

Notes:

1. No dedn of any exp or allowance shall be allowed under the Act from the income referred above.

2. The assessee is not required to furnish a return of his income if the following conditions are satisfied:

(a) The TI consists of only above mentioned income and

(b) TDS has been fully deducted from such income.

3. “Match referee” does not fall within the meaning of “sportsmen” to attract the provisions of sec 115BBA. Therefore, although the payments

made to NR ‘match referee’ are “income” which has accrued and arisen in India, the same are not taxable under the provisions of sec 115BBA.

They are subject to the normal rates of tax [Calcutta High Court in Indcom v. CIT (TDS)(2011) 335 ITR 485]

10 January 2019 The Chartered Accountant Student

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

Fig 1.11

WITHHOLDING TAX PROVISIONS IN RESPECT OF PAYTS TO NRs

Section Nature of payment Rate of TDS

192 Salary Normal Slab rates

192A Premature withdrawals from EPF, aggregating to R50,000 or more 10%

194B Income by way of winnings from lotteries, crossword puzzles, card games and other games of

30%

any sort, where payt to a person > R10,000

194BB Income by way of winnings from horse races, where payt to a person > R 10,000 30%

194E Specified payts referred u/s 115BBA to NR sportsmen/sports association or an entertainer 20%

194G Commission etc. on the sale of lottery tickets, where payt > R15,000 5%

194LB Payment of interest on infrastructure debt fund 5%

194LBA(2) Distribution of any interest income, recd or receivable by a business trust (BT) from a SPV, to

5%

its unit holders.

194LBA(3) Distribution of any income received from renting or leasing or letting out any real estate asset

directly owned by the BT, to its unit holders.

194LBB Investment fund paying income to a unit holder [other than income chargeable under PGBP At the rates in

which is exempted u/s 10(23FBB)]. force

194LBC(2) Income in respect of investment made in a securitisation trust (specified in Explanation to

section 115TCA)

194LC Payment of interest by an Indian Co. or BT –

- in respect of monies borrowed by an Indian Co. or BT in FC from sources outside India

• Under a loan agrmt between 1.7.2012 and 30.6.2020 or

• by way of issue of long-term infrastructure bonds (LTIB) between 1.7.2012 and

30.9.2014 or 5

• by way of issue of long-term bonds including LTIB between 1.10.2014 and 30.6.2020 as

approved by the CG

- in respect of monies borrowed from sources outside India by way of rupee denominated

bond (RDB) before 1.7.2020

194LD Interest payable between 1.6.2013 and 30.6.2020 to a FIl or QFI on investment made in –

- RDB of an Indian Co. 5

- Govt. security

195 Payment of any other sum to a Non-corporate non resident or Foreign Co. At the rates in

force

196B Income from units of a MF or UTI purchased in FC (including LTCG on transfer of such units)

10

payable to an Offshore Fund

196C Income by way of interest on bonds of an Indian Co. or public sector Co. sold by the Govt.

and purchased by a NR in FC or dividend on GDRs referred to u/s 115AC (including LTCG on 10

transfer of such bonds or GDRs) payable to a NR

196D Income of FII from securities referred u/s 115AD(1) (not being income by way of interest u/s

20

194LD, dividend u/s 115-O or capital gain arising from such securities)

Notes –

(i) In all the above cases, the rate of tax would be increased by surcharge, wherever applicable, and health and education cess @4%.

(ii) The rates in force are specified in the Finance Act, 2018 or in the DTAA entered into u/s 90 or 90A, as the case may be.

The Chartered Accountant Student January 2019 11

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

CHAPTER 2: DOUBLE TAXATION RELIEF

Fig 2.1

This arises on a/c of In order to avoid

Double taxation (DT) income being taxed such double

means taxing the in the country of taxation, Double

same income twice residence as well as Tax Avoidance

in the hands of an in the country of Agreements (DTAAs)

assessee. source come into play.

Source Rule Residence Rule

Income taxed in the country in which

it originates irrespective of whether the Income taxed in the country in which

income accrues to a resident or NR the taxpayer is resident

Fig 2.2

DT Relief under the IT Act, 1961

Bilateral Relief [Section 90/90A] Unilateral Relief [Section 91]

Agrmt with foreign countries or Countries with which no agrmt exists

specified territories

OBJECTIVE APPLICABILITY

The CG may enter into an agrmt with the Govt of any Assessee, who is a resident in India during the PY

country outside India or specified territory or specified

assn outside India,—

• for the granting of relief in respect of doubly taxed income CONDITIONS

• for the avoidance of DT of income • The income accrues or arises to him outside India.

• for exchange of information for the prevention of evasion • The income is not deemed to accrue or arise in India

or avoidance of income-tax during the PY.

• for recovery of income-tax • The income in question has been subjected to

income-tax in the foreign country in the hands of

the assessee.

TAXABILITY

• The assessee has paid tax on the income in the

Taxability of income would be detd based on DTAA or the IT foreign country.

Act, 1961, whichever is more beneficial. • There is no agrmt for relief from DT between

India and the other country where the income has

accrued or arisen.

CHARGE OF TAX ON FOREIGN CO.

The charge of tax in respect of a foreign Co. at a rate higher

than the rate at which a domestic Co. is chargeable, shall not COMPUTATION OF RELIEF

be regarded as less favourable charge or levy of tax in respect Doubly taxed income x Indian rate of tax or Rate of tax

of such foreign Co. in the said country, whichever is lower

TAX RESIDENCY CERTIFICATE TRC

• In order to claim DT relief, the NR to whom such DTAA applies, has to

obtain a TRC from the Govt of that country or specified territory.

• The NR to also provide such other docs and info, as may be prescribed,

for claiming treaty benefits.

12 January 2019 The Chartered Accountant Student

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

CHAPTER 3 TRANSFER PRICING & OTHER ANTI-AVOIDANCE MEASURES

Multinational Companies (MNC) operating in more than one country transfer physical goods and intangible

property or provides services to their associated enterprises (AEs) in another country. Two enterprises are “AEs” if

one of the enterprises participates directly or indirectly in the management, control or capital of the other or if both

enterprises are under common control. While doing so, the MNC concerned has in mind the goal of minimising

tax burden and maximising profits but the two tax jurisdictions have also the consideration of maximising their

revenue while making laws that govern such transactions (transns.) It is an internationally accepted practice that

such ‘transfer pricing’ should be governed by the Arm’s Length Principle (ALP) and the transfer price should be

the price applicable in case of a transaction of arm’s length. In other words, the transaction between associates

should be priced in the same way as a transaction between independent enterprises to avoid loss of revenue to the

concerned tax jurisdictions.

Fig 3.1

Chapter X: Special provisions relating to Avoidance of Tax [Transfer Pricing provisions]

Income should arise from Income to be computed Computation of income as per ALP

having regard to ALP should have the effect of ing taxa-

ble income or ing loss computed

International Specified domestic

transaction (SDT) ALP is the price

Transaction (InTn) applied/ proposed

[See Fig 3.6] • Nature & class

to be applied in a

transn b/w persons of InTn

other than AEs • Class(es) of

Transn b/w 2 or more AEs [See Fig 3.2] in uncontrolled AEs, functions

condns. performed,

Either or both of AEs should be NRs

assets

employed &

Transn is in the nature of- ALP to be computed

risks assumed

a Purchase, sale or lease of – as per most

Factors • Availability,

tangible or intangible property appropriate method

for coverage &

b Provn of services (MAM) amongst

presc methods selecting reliability of

c Lending or borrowing of money data reqd for

d Any other transn having a bearing on pfts, [See Fig 3.3] MAM

appln of the

income, losses or assets of AEs

method

Transn incl a mutual agrmt or arrangemt b/w Is more than one The price

No • Degree of

two or more AEs for allocatn of cost or exp. price detd by the so detd is

comparability

incurred w.r.t a benefit, service or facility MAM? the ALP

provided to any AE. bet. the InTn &

Yes uncontrolled

Whether the Arithmetic transn(CUT)

MAM selected mean of • Extent to

is CUP, RPM, all values which reliable

CPM or No incl. in the & accurate adjs

TNMM?. dataset can be made to

would be a/c for diff. b/w

Yes

the ALP InTn & CUT

Does the dataset • Nature, extent

constructed & reliability of

have 6 or more No

assumpns reqd

entries? to be made

Yes in appln of a

method

Range Concept

to be applied to

determine ALP

[Refer Study

Matl]

The Chartered Accountant Student January 2019 13

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

Deemed International Transaction

A Ltd Mr. B C Inc.

(Deemed AE

(Unrelated of A Ltd.)

party)

Agreement for sale of Product Agreement for sale of product

X entered into on 1/6/2018 X entered into on 31/5/2018

Transaction between A Ltd. and Mr. B is deemed to be an

InTn between AEs, whether or not Mr. B is NR

Fig 3.2

Associated Enterprises (AEs) [Section 92A(1)]

Condition Example

(1) An enterprise (entr) which participates, directly (DP) or Where A Ltd. DP in mgt of B Ltd. and B Ltd. DP in mgt of C

indirectly (IDP), or through one or more intermediaries, in: Ltd. In such situation, A Ltd. has DP in mgt of B Ltd. but has

• Management (mgt) of the other entr (OE), or an IDP in mgt of C Ltd.

• control of OE, or

• capital of OE A B C

In such scenario, both B Ltd. and C Ltd. would be AEs of A

Ltd.

(2) If one or more persons participates, directly or indirectly, or

through one or more intermediaries in: Mr. A directly has control in A Ltd. and B Ltd. In such

• mgt of the two different entrs a scenario, both A Ltd. & B Ltd. are AEs since they have a

• control of two different entrs common person i.e. Mr. A, who controls both entities A Ltd.

• capital of two different entrs & B Ltd.

Then, those two entrs are AEs.

Deemed Associated Enterprises [Section 92A(2)]

Condition Situation Example

Substantial One entr holds 26% A Ltd. holds 33% of VP in B Ltd. and B Ltd. holds 40% VP in C Ltd.

Voting Power or more of the VP, 33% 40%

(VP) directly or indirectly,

in the other entr

A B C

(OE). In above situation, A Ltd. holds 33% of VP in B Ltd. directly and 40% of VP in C Ltd.

indirectly (i.e. through B Ltd.). Therefore, both B Ltd. & C Ltd. are deemed AEs of A

Ltd.

Substantial VP Any person or entr Mr. A holds 40% of shareholding in both X Ltd. and Y Ltd. where

in two entities by holds 26% or more neither X Ltd. has any holding in Y Ltd. nor Y Ltd. has any holding in X Ltd.

common person of the VP power,

directly or indirectly, Mr. A

in each of two

40% 40%

different entrs.

X Ltd. Y Ltd.

In this situation, since Mr. A directly holds 40% of shareholding in both X Ltd. and Y

Ltd., X Ltd. & Y Ltd. will be deemed AEs.

14 January 2019 The Chartered Accountant Student

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

Deemed Associated Enterprises [Section 92A(2)]

Condition Situation

Example

Advancing of One entr advances loan to the OE

BV of total assets of Y Ltd. is R 100 crores. X Ltd. advances loan of R 60

substantial sum of of an amount of 51% or more of

crores to Y Ltd.

money the book value (BV) of the total

assets of OE Since, in this case, X Ltd. advances loan which is 60% of the BV of total

assets of Y Ltd., X Ltd. & Y Ltd. are deemed AEs.

Guaranteeing One entr guarantees 10% or

P Inc. has total loan of 1 million dollars from XYZ Bank of America. Out

borrowings more of the total borrowings of

of that, A Ltd., an Indian company, guarantees 20% of total borrowings. In

the OE.

such case, P Inc. and A Ltd. would be deemed AEs.

Appointment of One Entr appoints more than X Ltd. has 15 directors on its Board. Out of that, Y Ltd. has appointed

majority directors half of the BoD or members of 8 directors. In such case, X Ltd. and Y Ltd. would be deemed AEs.

of OE the governing board (GB), or one

or more executive directors (EDs)

or executive members (EMs) of

the GB of OE.

Appointment of More than half of the directors

majority directors or members of the GB, or one Mr. A appointed 9 directors out of 15 directors of X Ltd. and appointed

of two different or more of the EDs or members 2 EDs on the board of Y Ltd. In such case, since a common person

entrs by same of the GB of each of the two

i.e. Mr. A appointed more than half of the directors in X Ltd. and

person(s) entrs are appointed by the same

person(s). appointed 2 EDs in Y Ltd., both X Ltd. and Y Ltd. are deemed AEs.

Dependence on The manufacture (mfre) or processing of goods or articles or business carried out by one entr is wholly

intangibles w.r.t dependent (i.e. 100%) on the know-how, patents, copyrights etc., or any data, documentation, drawing or

which OE has specification relating to any patent, invention, model etc. of which the OE is the owner or in respect of which

exclusive rights the OE has exclusive rights.

Dependence on 90% or more of RMs and consumables required for the mfre or processing of goods or articles or business

RM supplied by carried out by one entr, are supplied by the OE, or by persons specified by the OE, where the prices and other

OE conditions relating to the supply are influenced by such OE.

Dependence on The goods or articles mfrd or processed by one entr, are sold to the OE or to persons specified by the OE,

sale and the prices and other conditions relating thereto are influenced by such OE.

Control by Where one entr is controlled

common by an indvl, the OE is also

individual (indvl) controlled by such indvl or his Mr. A and Mr. B are relatives. Mr. A has control over X Ltd. and Mr. B has

relative or jointly by such indvl control over Y Ltd. In such a case, both X Ltd. and Y Ltd. would be deemed AEs.

and his relatives.

Control by HUF Where one entr is controlled by

or member an HUF and the OE is controlled HUF Member of HUF/

Relative of member

thereof by a member of such HUF or by of such HUF

relative of a member of such Control

HUF or jointly by such member A Ltd & B Ltd are Control

and his relative. A Ltd. deemed AEs B Ltd.

Interest in a firm, Where one entr is a firm, AOPs or BOls, the OE holds 10% or more interest in firm/HUF/BOI.

AOPs or BOIs

Mutual interest There exists b/w the two entrs, any relationship of mutual interest, as may be prescribed.

relationship

The Chartered Accountant Student January 2019 15

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

Fig 3.3

Methods for computing ALP [Section 92C]

Resale Price Cost Plus Method Profit Split Method Transactional Net

CUP Method Margin Method (TNMM)

Method(RPM) (CPM) (PSM)

This method is This method is This method is This method is Compute NP margin of

applied where applied where item generally applied applied where there the entr from InTn with

there are similar obtained from AE is where semi-finished is transfer of unique AE having regard to cost

transaction(s) b/w resold to unrelated goods are sold to AEs intangibles or in incurred/sales effected/

unconnected parties party multiple InTns assets employed

Identify the RP at Identify direct & Determine combined Compute the NP margin

Identify price which the item is indirect COP incurred NP of the AEs arising realised by the Entr or

in a comparable resold to unrelated for property trfd or out of InTn unrelated entr in a CUCT

uncontrolled party services provided to AE by applying the same base

transaction (CUCT)

Reduce the RP by the Determine normal Evaluate the relative Adjust NP margin realised

normal GP margin on GP mark up to such contribution of each entr from CUCT to a/c for

CUCT & exp incurred costs by an unrelated to the earning of combined differences affecting NP

(customs duty) w.r.t. entr in CUCTs NP on the basis of FAR margin in the OM

purchase

Adjust the price for Adjust the price for Adjust the normal GP Split the combined Compare NP margin

material diffr. in functional & other mark-up for functional NP amongst the entrs relative to costs/sales/

terms of contract, diffr. materially and other diffr in proportion to mkt assets of the AE with NP

credit, transport etc. affecting GP margin materially affecting GP returns; & residual pfts margin of uncontrolled

in open market (OM) mark-up in OM in prop. to their relative party in comparable

contribution transactions

Adjusted price is ALP Adjusted price is ALP Total Costs ↑d by adjusted ALP to be detd on the Adjusted NP margin taken

mark up = ALP basis of profit apportioned. into A/c to arrive at ALP

Fig 3.4

Advance Pricing Agreements [Section 92CC]

An Advance Pricing Agreement (APA) is an agrmt between a taxpayer and a taxing authority on an appropriate TP methodology for a

set of transns. over a fixed period of time in future for not exceeding 5 consecutive PYs.

APA may also provide for determination of ALP or for specifying the manner in which ALP is to be determined in relation to an InTn

entered into by a person during the rollback year. Rollback year is the PY, falling within the period not exceeding four PYs preceding

the first of the PYs for which the APA applies in respect of the InTn to be undertaken.

Purpose of APA Detrmination (dtrmn) of ALP or specifying the manner for dtrmn of ALP for an InTn to be entered into.

Manner of dtrmn

The manner for dtrmn of ALP ref. above may include methods ref. to u/s 92C(1) or any other

of ALP in APA

method with necessary adjustments or variations.

Non-applicability of

Where an APA has been entered for an InTn, then, computation of ALP as per the methods specified u/s

sec 92C & sec 92CA

92C and reference to TPO would not apply for such InTn.

Validity of APA For the period specified in the agrmt which shall not exceed five consecutive PYs. In case of

rollback, the total period shall not exceed 9 PYs [4 PY + maximum 5 consecutive PY]

Binding APA will be binding on:

nature • the person and in respect of the transns. in relation to which, the APA has been entered into; and

of APA • the PC or C and the ITAs subordinate to him, in respect of the said person and the said transns.

The APA, however, would not be binding, if there is any change in law or facts having bearing on such APA.

Consqs. where • Where APA obtained by way of fraud or misrepresantation of facts, the Board with the approval of CG can

declare APA void ab initio.

APA is • All the prov of the Act shall apply to such person, as if such APA had never been entered into.

obtained by • The period beginning with the date of such APA and ending on the date of order declaring the APA as void

fraud: ab initio, shall be excluded for the purpose of compting any period of limitation (POL) under this Act.

• In case the PoL after exclusion of the above period is less than 60 days, such remaining PoL shall be

extended to 60 days.

Prescribed The Board has prescribed rules 10F to 10T specifying an APA scheme. [For details, refer Study

scheme for APA Material]

16 January 2019 The Chartered Accountant Student

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

Fig 3.5

Secondary Adjustment [Section 92CE]

Primary Adjustment (PA) to TP

Determination of TP in acc. with ALP resulting in ↑ in TI or ↓in loss of the assessee

No No Does it relate to A.Y.2017-

Is PA > R 1 crore in a PY? No Secondary Adj is reqd

18 or later A.Y.?

Yes Yes

If answer to both questions is yes, Secondary Adjustment to TP is required, where

PA to TP is made in a case falling within (i) to (iv) in box 1 or (v) in box 2 below

Adj. in BOA of the assessee and its AE to reflect actual allocation of pfts b/w

assessee and its AE in line with TP detd in PA

Excess Money (i.e., diff. b/w ALP detd. in PA and actual TP) to be repatriated

within 90 days

From due date of filing of ROI u/s 139(1) From date of order

Box 1: In cases (i) to (iv) below Box 2: In case (v) below

• Where PA to TP has been made by the

assessee suo moto in his ROI If PA to TP as determined in the order of the AO

• Where APA is entered into by the assessee or the Appellate Authority has been accepted by

• Where safe harbor option is exercised by the assessee

assessee

• Where agmt under the MAP under a DTAA

has been entered into u/s 90 or 90A

Consequences of non-repatriation within 90 days

Excess Money would be deemed as advance made by the assessee to AE

Interest to be computed

Where the InTn is denominated in Indian Rupee Where the InTn is denominated in FC

At one year marginal cost of fund lending rate of At six month LIBOR as on 30 th Sep of the

SBI as on 1 st April of the relevant PY + 3.25% relevant PY + 3%

The Chartered Accountant Student January 2019 17

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

Fig 3.6

Transfer pricing for Specified Domestic Transactions (SDTs) [Section 92BA]

Income from domestic related party transactions to be subjected to TP

Any allowance for TP prov would ALP and income Persons Reference can Penalty

an exp. or interest not apply if of a SDT to be entering into be made to TPO provisions

or allocation of any income or allow. comptd in the a SDT to for computation would also apply

cost or exp. or any for exp. or same manner as maintain info of ALP of SDT to SDT as they

income in relation interest has the applicable to an and docs & apply to an InTn

to the SDT to be effect of ↓ing InTn furnish report

computed w.r.t. income or ↑ing of accountant

ALP loss

SDT means any of the following transactions, not being an International Transaction

Any transn ref. u/s 80A Any tfr of g & s Any business Any transn ref. to Any other

i.e., inter-unit transfer(tfr) ref. u/s 80-IA(8) transacted b/w the in any other sec transn as may be

of goods or services (g & s) i.e., inter unit tfr of assessee carrying on under Chap VI-A prescribed

by an unit/entr. or eligible g&s b/w EB & OB EB & other person or sec 10AA, to

business (EB) to other or vice versa for as ref. u/s 80-IA(10) which prov of

business (OB) or vice versa, consdn not equal sec 80-IA(8)/(10)

for consdn not equal to FMV to FMV apply

Note: However, where aggregate value of above transactions entered into by the assessee ≤ R 20 crore in the PY, then, such

transactions would not be treated as SDT , and consequently TP provisions would not be applicable.

Fig 3.7

Penalty for failure to comply with TP provisions

Section Nature of default Penalty

270A(9) Failure to report any InTn or Deemed InTn or SDT to which the prov of Chap X applies 200% of the tax payable on

would constitute ‘misreporting of income’ under-reported income

271BA Failure to furnish a report from an accountant as required by sec 92E R 1 lakh

271G Failure to furnish info or doc as required by AO or CIT(A) u/s 92D(3) within 30 days from 2% of the value of the InTn/

the date of receipt of notice or extended period not exceeding 30 days, as the case may be.. SDT for each failure

271AA (1) Failure to keep and maintain any such doc and info as required by sec 92D(1)/(2); 2% of the value of each such

(2) Failure to report such InTn or SDT which is required to be reported; or InTn/SDT

(3) Maintaining or furnishing any incorrect info or doc.

Notes:

• The penalty u/s 271AA shall be in addition and not in substitution of penalty u/s 270A(9) or 271BA.

• In all the above cases, if the assessee can show that there was reasonable cause for the failure, no penalty will be leviable.

CHAPTER 4: ADVANCE RULINGS

For the purpose of saving the high cost and significant time involved in extensive litigations relating to

determination of tax liability of a non-resident or tax liability of a resident arising out of high value transactions,

an independent quasi-judicial authority, namely, the Authority for Advance Rulings (AAR) has been given the

power to pronounce advance ruling in respect thereof relating to a specific question of law or fact. This will help

ensure certainty and at the same time will be expeditious and cost effective.

18 January 2019 The Chartered Accountant Student

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

Fig 4.1

Applicant for Advance Ruling

S.No. Applicant u/s 245N(b) Advance Ruling u/s 245N(a) means determination by the AAR in relation to

(i) NR a transn which has been undertaken (u/t) or is proposed to be u/t by him.

(ii) Resident the tax liability of a NR arising out of a transn which has been u/t or is proposed to be u/t by him

with such NR and such determination (detmn) shall incl the detmn of any question of law or of

fact specified in the application.

(iii) Resident of class or category of the tax liability of a resident applicant, arising out of a transn which has been u/t or is proposed

persons notified by CG to be u/t by such applicant and such detmn shall incl the detmn of any question of law or of fact

specified in the application.

Note: CG has notified a resident, in relation to his tax liability arising out of one or more transns. valuing ≥ R 100 crore in total.

(iv) Resident of class or category an issue relating to computation of TI which is pending before any IT Authority or the ITAT and

of persons notified by CG such detmn or decision shall incl the detmn or decision of any question of law or fact w.r.t. such

computation of TI specified in the application.

Note: A Public sector undertaking has been notified by the CG

(v) Resident or NR whether an arrangement, which is proposed to be u/t by such applicant, is an impermissible

avoidance arrangement as referred to in Chapter X-A or not.

Fig 4.2

Overview of Advance Ruling Procedure

No

Cannot make an application for Is the applicant an eligible applicant falling u/s 245N(b)?

advance ruling

Yes

Entitled to make an application for advance ruling

Yes

No further processing Is the application withdrawn by the applicant within 30 days?

No

Whether the question raised in the application

Yes • is already pending before income-tax authorities/ITAT/ Court

AAR shall not allow the [except in case of (iv) of Fig. 4.1]?

application • involves determination of FMV of any property?

• relates to a transn designed prima facie for avoidance of income-tax

[except in cases (iv) and (v) of Fig. 4.1]?

• Opportunity of being

heard to be given to No

No

the applicant Whether application accepted?

• Reasons for rejection Yes

to be given in the Copy of application f/w to PC or Commissioner

order. requiring him to furnish records, if required

AAR to pronounce with ruling within 6 months of

recpt of appln

Advance Ruling pronounced is binding only on:-

• The applicant who has sought it

• in respect of the specific transaction for which the ruling has been sought

• On PC/Commnr and the IT Auth subordinate to him, in resp. of the applicant and the

transn

Advance Ruling is void ab Yes

Is the advance ruling obtained by fraud/misrepresentation?

initio

No

Advance Ruling is valid

The Chartered Accountant Student January 2019 19

© The Institute of Chartered Accountants of India

INTERNATIONAL TAXATION

CHAPTER 5: EQUALISATION LEVY

In the digital domain, business may be conducted without regard to national boundaries and may dissolve the link

between an income-producing activity and a specific location. The typical taxation issues relating to e-commerce

are:

(i) the difficulty in characterizing the nature of payment and establishing a nexus or link between taxable

transaction, activity and a taxing jurisdiction,

(ii) the difficulty of locating the transaction, activity and identifying the taxpayer for income tax purposes.

Taking into consideration the potential of new digital economy and the rapidly evolving nature of business

operations, it becomes necessary to address the challenges in terms of taxation of such digital transactions.

Chapter VIII of the Finance Act, 2016 addresses these challenges by introducing "Equalisation Levy" on such

transactions.

Fig 5.1

Equalisation Levy (EL)

6% of amt. of consideration (consdn) recd or receivable

For Specified Services Meaning of Specified Services:

(i) Online advt

(ii) Prov. for digital advtg space or any other

facility or service for online advt.

By a NR not having PE in India or (iii) Any other service notified by the Govt.

providing services not effectively

connected with his PE in India

From a resident in India From a NR having PE

carrying on business or profn in India

Does the aggregate amt of such consdn recd or receivable for

specified services by a NR exceed R 1 lakh in any PY?

Yes No

EL is attracted EL is not attracted

Deduction of Eq. Levy The person liable to deduct EL has to, in

EL@6% is deductible from consdn paid or payable for specified any case, pay the EL to the credit of the

services by a – CG by the 7 th of the next month.

- resident carrying on business or profn; or

- NR having PE in India

if the agg. consdn exceeds R 1 lakh Simple interest@1% p.m. or part of a

month is attracted for the period of delay

in remittance.

Remittance of EL

EL deducted during any month to be paid to the credit of the

CG by the 7 th of the next month

Penalty = the amt of EL deductible.

For delayed remittance, penalty@ R 1,000

Consequences of failure to deduct EL per day of failure attracted, not exceeding

the amt of EL not paid.

20 January 2019 The Chartered Accountant Student

© The Institute of Chartered Accountants of India

You might also like

- Chapter 01 - Introduction To Federal Taxation in CanadaDocument40 pagesChapter 01 - Introduction To Federal Taxation in CanadaDonna So100% (2)

- Transfer Pricing in IndonesiaDocument149 pagesTransfer Pricing in Indonesiathe1uploader0% (1)

- Capsule It PDFDocument25 pagesCapsule It PDFGiri SukumarNo ratings yet

- Non Resident TaxationDocument123 pagesNon Resident Taxationguru1barkiNo ratings yet

- Corporate Tax Planning Unit-2 E-Text Module 5 & 6: Residential Status & Taxation of Companies Scope of Total Incidence of Tax (Section 5)Document10 pagesCorporate Tax Planning Unit-2 E-Text Module 5 & 6: Residential Status & Taxation of Companies Scope of Total Incidence of Tax (Section 5)imamNo ratings yet

- 52313bosfinal 19 p7 Mod4 cp1Document84 pages52313bosfinal 19 p7 Mod4 cp1Chandan SinglaNo ratings yet

- Taxation Direct Tax Code Assignment 2: SUBMITTED TO: Mrs. Ranjani Matta SUBMITTED BY: Shalini MahawarDocument6 pagesTaxation Direct Tax Code Assignment 2: SUBMITTED TO: Mrs. Ranjani Matta SUBMITTED BY: Shalini MahawarShalini MahawarNo ratings yet

- UNIT 1 - CT - Part 1Document39 pagesUNIT 1 - CT - Part 1Amogh AroraNo ratings yet

- Day4 Residential Status and Incidence of Tax (9 Oct)Document12 pagesDay4 Residential Status and Incidence of Tax (9 Oct)1986anuNo ratings yet

- Place of Effective Management 1705112727Document4 pagesPlace of Effective Management 1705112727nirmalseervi.mkdNo ratings yet

- Budget2017 18sudha 170215110415Document89 pagesBudget2017 18sudha 170215110415Taxpert mukeshNo ratings yet

- Corporate Tax PlanningDocument18 pagesCorporate Tax PlanningSANDEEP KUMARNo ratings yet

- Notes LLB Tax NavDocument33 pagesNotes LLB Tax Navamit HCSNo ratings yet

- BFM CH 21 PDFDocument27 pagesBFM CH 21 PDFKiran KotlapatiNo ratings yet

- Relationship Between Residential Status and Incidence of TaxDocument5 pagesRelationship Between Residential Status and Incidence of Taxsuyash dugarNo ratings yet

- ResidenceDocument14 pagesResidenceguru1barkiNo ratings yet

- Relationship Between Residential Status and Incidence of TaxDocument5 pagesRelationship Between Residential Status and Incidence of Taxsuyash dugarNo ratings yet

- Residential Status of A CompanyDocument18 pagesResidential Status of A CompanyNaveenNo ratings yet

- Incidence of TaxDocument53 pagesIncidence of TaxAnurag SindhalNo ratings yet

- TDS On OTADocument4 pagesTDS On OTAabcxyznoneNo ratings yet

- Income Deemed To Arise in IndiaDocument7 pagesIncome Deemed To Arise in IndiaDebaNo ratings yet

- Formerly Air India Assets Holding LimitedDocument1 pageFormerly Air India Assets Holding Limitedamit nakraNo ratings yet

- Wealth Tax InterDocument66 pagesWealth Tax IntersamstarmoonNo ratings yet

- Note 19 - RESIDENTIAL STATUS OF HUF, FIRM AND COMPANYDocument4 pagesNote 19 - RESIDENTIAL STATUS OF HUF, FIRM AND COMPANYSumit BainNo ratings yet

- Tax NotesDocument11 pagesTax NotesVishal DeshwalNo ratings yet

- Residential Status and Incidence of Tax - Study MaterialDocument6 pagesResidential Status and Incidence of Tax - Study MaterialEmeline SoroNo ratings yet

- Mba104 Assignment Amaoed-20200115662Document64 pagesMba104 Assignment Amaoed-20200115662Shie Shiela Lalav0% (1)

- Principles of Taxation Law - (Week 6)Document56 pagesPrinciples of Taxation Law - (Week 6)ishikakeswani4No ratings yet

- 1518759148pdfjoiner PDFDocument40 pages1518759148pdfjoiner PDFAlkaNo ratings yet

- Scope of Total Income and Residential StatusDocument3 pagesScope of Total Income and Residential StatusSandeep SinghNo ratings yet

- FDI in LLPDocument5 pagesFDI in LLPpankajpatnicsNo ratings yet

- Presentation On Residential Status & Its Incidence On Tax LiabilityDocument13 pagesPresentation On Residential Status & Its Incidence On Tax LiabilitypriyaniNo ratings yet

- Assignment - TaxDocument6 pagesAssignment - TaxsuriNo ratings yet

- Investment Holding CompanyDocument6 pagesInvestment Holding CompanyAnas AjwadNo ratings yet

- TDS On Commission To Non ResidentDocument6 pagesTDS On Commission To Non ResidentAdityaNo ratings yet

- Residential Status and Tax IncidenceDocument3 pagesResidential Status and Tax Incidenceambarishan mrNo ratings yet

- Regulatory Framework For Foreign Entities Operating in IndiaDocument4 pagesRegulatory Framework For Foreign Entities Operating in IndiaSatakshi N DixitNo ratings yet

- CBDT - Detailed POEM Guidelines - January 2017Document10 pagesCBDT - Detailed POEM Guidelines - January 2017bharath289No ratings yet

- Entry Strategies For Foreign InvestorsDocument6 pagesEntry Strategies For Foreign Investorsconsurd1978No ratings yet

- Doing Business in India 2021Document95 pagesDoing Business in India 2021UtiyyalaNo ratings yet

- Residential Status and Taxation For Individuals - Taxguru - inDocument2 pagesResidential Status and Taxation For Individuals - Taxguru - inSubhamNo ratings yet

- Acco 20133 - Unit Iii & Iv - CreateDocument35 pagesAcco 20133 - Unit Iii & Iv - CreateHarvey AguilarNo ratings yet

- Week 4-7Document9 pagesWeek 4-7Vijayant DalalNo ratings yet

- Tax Erosion Due To BEPSDocument27 pagesTax Erosion Due To BEPSabhishek raiNo ratings yet

- 01 Section 9Document54 pages01 Section 9ABHIJEETNo ratings yet

- 76198bos61579 cp9Document209 pages76198bos61579 cp9pikachupiki181No ratings yet

- FDI July '20Document17 pagesFDI July '20Yogesh SalujaNo ratings yet

- CA FINAL DT Amendments For MAY and NOV 2017Document98 pagesCA FINAL DT Amendments For MAY and NOV 2017Saurav KakkarNo ratings yet

- Ass Assessment of Companies.Document11 pagesAss Assessment of Companies.Safa100% (1)

- Tax Unit 1-2 - 15Document1 pageTax Unit 1-2 - 15joy BoseNo ratings yet

- Compiler NR TAXATION Q 28, 30 To 32Document7 pagesCompiler NR TAXATION Q 28, 30 To 32Gajender JhaNo ratings yet

- Types of Residents: Resident Non-ResidentDocument25 pagesTypes of Residents: Resident Non-ResidentPJ 123No ratings yet

- ch-11 Taxation of NRIsDocument25 pagesch-11 Taxation of NRIsdean.socNo ratings yet

- e Book PDF PDFDocument91 pagese Book PDF PDFGiri SukumarNo ratings yet

- Sia - Itax-2018-19Document17 pagesSia - Itax-2018-19Abhay Pethani.No ratings yet

- Summary Book Nov 2022Document41 pagesSummary Book Nov 2022Krrish KelwaniNo ratings yet

- Income Tax Law & Practice: Unit 1Document30 pagesIncome Tax Law & Practice: Unit 1jaspreet kaurNo ratings yet

- Amndmnt I-M'21Document25 pagesAmndmnt I-M'21kri satNo ratings yet

- E Bay International AGvs Assistant Directorof IncometaxDocument16 pagesE Bay International AGvs Assistant Directorof IncometaxShreyaNo ratings yet

- CH 4 Fdi Final 1Document23 pagesCH 4 Fdi Final 1arushiNo ratings yet

- Unit Iii:: Income Tax ON CorporationsDocument35 pagesUnit Iii:: Income Tax ON CorporationsElleNo ratings yet

- ST Vincent and The Grenadines Tax GuideDocument9 pagesST Vincent and The Grenadines Tax GuideWei LiNo ratings yet

- ENT 430 International Business IIDocument329 pagesENT 430 International Business IIEmeka Ken NwosuNo ratings yet

- Investment and Decision Analysis For Petroleum ExplorationDocument24 pagesInvestment and Decision Analysis For Petroleum Explorationsandro0112No ratings yet

- Impact Analysis of Tax Policy and The Performance of Small and MediumDocument25 pagesImpact Analysis of Tax Policy and The Performance of Small and Mediumkara albueraNo ratings yet

- Cyprus International CompaniesDocument11 pagesCyprus International CompaniesGigi LunetteNo ratings yet

- Jamaica Tax GuideDocument30 pagesJamaica Tax GuideAMNo ratings yet

- ADIT Paper I - Candidate Script 2010Document6 pagesADIT Paper I - Candidate Script 2010Constantinos_m0% (1)

- Barrios Et Al. (2012) International Taxation and Multinational Firm Location DecisionsDocument13 pagesBarrios Et Al. (2012) International Taxation and Multinational Firm Location DecisionsCarlos MartinsNo ratings yet

- KPMG Singapore Budget 2022 ProposalDocument63 pagesKPMG Singapore Budget 2022 ProposalMark ChuoNo ratings yet

- History of TaxationDocument12 pagesHistory of TaxationHai Bui thiNo ratings yet

- 75282bos Transition Scheme NsetDocument54 pages75282bos Transition Scheme NsetPranay JaiswalNo ratings yet

- AgendaDocument5 pagesAgendaJelena BajićNo ratings yet

- JURNALDocument9 pagesJURNALrahmat razeeqNo ratings yet

- BosicaidcscsDocument4 pagesBosicaidcscsAishwaryaNo ratings yet

- 15 Chapter 4Document29 pages15 Chapter 4Mohammad Salim HossainNo ratings yet

- Handbook Tax Base Second Edition PDFDocument796 pagesHandbook Tax Base Second Edition PDFTin RANNo ratings yet

- Why Cyprus Is An Ideal Holding Company Location - International Tax ReviewDocument3 pagesWhy Cyprus Is An Ideal Holding Company Location - International Tax ReviewAnton KoublytskiNo ratings yet

- 71240bos57247 P7aDocument27 pages71240bos57247 P7abhagirath prakrutNo ratings yet

- 2014e PDFDocument64 pages2014e PDFHenryNo ratings yet

- CH 1Document102 pagesCH 1senayNo ratings yet

- UPDATE 111120 SoreDocument103 pagesUPDATE 111120 Soremelissadevina29No ratings yet

- CauseListFile 98VS8DKF51F PDFDocument120 pagesCauseListFile 98VS8DKF51F PDFrentpe propertyNo ratings yet

- Sweden PESTELDocument10 pagesSweden PESTEL李沁恩No ratings yet

- Vietnam Tax Legal HandbookDocument52 pagesVietnam Tax Legal HandbookaNo ratings yet

- Branch OfficeDocument32 pagesBranch OfficeVedang GupteNo ratings yet

- International Taxation Adnan Islam Full ChapterDocument77 pagesInternational Taxation Adnan Islam Full Chapterrussell.amie326100% (9)

- 2012 ITAD - BIR - Ruling - No. - 310 1220190228 5466 1jldnvoDocument3 pages2012 ITAD - BIR - Ruling - No. - 310 1220190228 5466 1jldnvonathalie velasquezNo ratings yet

- International Double TaxationDocument19 pagesInternational Double Taxationpragya mishraNo ratings yet