Download as docx, pdf, or txt

You might also like

- CFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)From EverandCFA Level 1 Calculation Workbook: 300 Calculations to Prepare for the CFA Level 1 Exam (2023 Edition)Rating: 4.5 out of 5 stars4.5/5 (5)

- Muslim Rajputs of RajouriDocument10 pagesMuslim Rajputs of RajouriEPILOGUE MAGAZINE100% (2)

- Accounting QuestionsDocument16 pagesAccounting QuestionsPrachi ChananaNo ratings yet

- 7 HOTS Questions PDFDocument33 pages7 HOTS Questions PDFNishant ShyaraNo ratings yet

- Admission of A Partner: Other Educational PortalsDocument31 pagesAdmission of A Partner: Other Educational Portalskkaur4No ratings yet

- Admission of Partner PDFDocument6 pagesAdmission of Partner PDFBHUMIKA JAINNo ratings yet

- Assignment 3 AdmissionDocument8 pagesAssignment 3 AdmissionKavyashri PNo ratings yet

- Accounting For Partnership Firms: Short Answer Type QuestionsDocument8 pagesAccounting For Partnership Firms: Short Answer Type QuestionssalumNo ratings yet

- Class XII Commerce (1) GGBDocument10 pagesClass XII Commerce (1) GGBAditya KocharNo ratings yet

- Worksheet - 1 Unit 1 - Accounting For Partnership Firm Chapter 4 - Admission of A PartnerDocument14 pagesWorksheet - 1 Unit 1 - Accounting For Partnership Firm Chapter 4 - Admission of A PartnerRica Jane LlorenNo ratings yet

- Adjustment of Goodwill-Admission PDFDocument2 pagesAdjustment of Goodwill-Admission PDFarnav trivediNo ratings yet

- Holiday Homework Accountancy Class 12Document15 pagesHoliday Homework Accountancy Class 12Sambhav GargNo ratings yet

- Sample Paper 2 G 12 - Accountancy - SUMMER BREAKDocument9 pagesSample Paper 2 G 12 - Accountancy - SUMMER BREAKpriya longaniNo ratings yet

- The Indian Public School, ErodeDocument3 pagesThe Indian Public School, ErodeMadhumithaa SvNo ratings yet

- Accounting Question BankDocument4 pagesAccounting Question BankdhruvNo ratings yet

- Question Bank Accountancy (055) Class XiiDocument5 pagesQuestion Bank Accountancy (055) Class XiiDHIRENDRA KUMARNo ratings yet

- Accounts CH 2 Admission of PartnerDocument5 pagesAccounts CH 2 Admission of Partnerapsonline8585No ratings yet

- Change in Profit Sharing Ratio Among Existing PartnersDocument3 pagesChange in Profit Sharing Ratio Among Existing Partnerssengaryashraj375No ratings yet

- Summer Holiday Homework 2024 - Accountancy & Business StudiesDocument5 pagesSummer Holiday Homework 2024 - Accountancy & Business Studiessanskarprasad18No ratings yet

- Asm 25560Document9 pagesAsm 25560shivanshu11o3o6No ratings yet

- Acc Class 12 Admission of PartnerDocument20 pagesAcc Class 12 Admission of Partnermaverickxxx1029No ratings yet

- Quiz 3Document14 pagesQuiz 3Jyasmine Aura V. AgustinNo ratings yet

- MCQs - Partnership (All Chapters)Document6 pagesMCQs - Partnership (All Chapters)bdharshini06No ratings yet

- Change in PSRDocument7 pagesChange in PSRBHUMIKA JAINNo ratings yet

- GoodwillDocument4 pagesGoodwilldivyarwt0No ratings yet

- Worksheet Accounts Ut 1 RefrenceDocument10 pagesWorksheet Accounts Ut 1 Refrencemayankkochar216No ratings yet

- Account 12th ClassDocument4 pagesAccount 12th ClassMandeep KaurNo ratings yet

- 7730239-Retirement of A Partner - WS 1Document2 pages7730239-Retirement of A Partner - WS 1Sandra SanthoshNo ratings yet

- Accountancy PB 1 Mock Test PaperDocument10 pagesAccountancy PB 1 Mock Test PaperUjwal Anish ReddyNo ratings yet

- Admission of PartnerDocument7 pagesAdmission of Partneradarshrathore12341234No ratings yet

- Accounts Holiday HW 1Document4 pagesAccounts Holiday HW 1AlishbaNo ratings yet

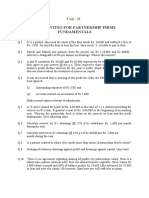

- Accounting For Partnership Firms Fundamental PDFDocument10 pagesAccounting For Partnership Firms Fundamental PDFMarivisiasNo ratings yet

- Term One Accountancy 12 QP & MSDocument13 pagesTerm One Accountancy 12 QP & MSVarun HurriaNo ratings yet

- Suraj Gir's Guess Paper For AISSCE-2008: Accountancy (67/1/2)Document5 pagesSuraj Gir's Guess Paper For AISSCE-2008: Accountancy (67/1/2)Shalini SharmaNo ratings yet

- Asm1 25560Document12 pagesAsm1 25560shivanshu11o3o6No ratings yet

- Screenshot 2023-03-11 at 12.52.38 PM PDFDocument56 pagesScreenshot 2023-03-11 at 12.52.38 PM PDFpalak sanghviNo ratings yet

- 12 Accountancy Ch03 Test Paper 02 Treatment of GoodwillDocument3 pages12 Accountancy Ch03 Test Paper 02 Treatment of GoodwillSachin AlmalNo ratings yet

- 12 Cbse Accountancy Set 1 QPDocument12 pages12 Cbse Accountancy Set 1 QPAymenNo ratings yet

- 12 Acc WT 2 QPDocument2 pages12 Acc WT 2 QPYashikNo ratings yet

- Unit 2 Partmership Firms FundamentsDocument10 pagesUnit 2 Partmership Firms FundamentsSunlight SirSundeepNo ratings yet

- Admission of A Partner-1Document1 pageAdmission of A Partner-1Hema AnanthNo ratings yet

- Xii Acc WorksheetssDocument55 pagesXii Acc WorksheetssUnknown patelNo ratings yet

- Xii Acc Worksheetss-1-29Document29 pagesXii Acc Worksheetss-1-29Unknown patelNo ratings yet

- Chapter 4 - Admission of A PartnerDocument110 pagesChapter 4 - Admission of A Partnerakshaya sangeethaNo ratings yet

- XII ACC Holiday HomeworkDocument3 pagesXII ACC Holiday HomeworkGaurav SainNo ratings yet

- ACC Assignment Questions Extra PractiseDocument20 pagesACC Assignment Questions Extra Practisesikeee.exeNo ratings yet

- ACCOUNTING FOR PARTNERSHIP FIRMS - WorksheetDocument2 pagesACCOUNTING FOR PARTNERSHIP FIRMS - WorksheetMAYOOKHA MADHU ATTIPPILNo ratings yet

- PT-1 Accountancy 2022-23Document3 pagesPT-1 Accountancy 2022-23Ajit HuidromNo ratings yet

- Change in Profit RatioDocument10 pagesChange in Profit RatioHansika SahuNo ratings yet

- AdmissionDocument2 pagesAdmissionshubhamsundraniNo ratings yet

- Change in Profit Sharing Ratio Amongst TDocument2 pagesChange in Profit Sharing Ratio Amongst TSukhjinder SinghNo ratings yet

- Commerce Fundamental: Class 12 - AccountancyDocument9 pagesCommerce Fundamental: Class 12 - AccountancySACHIN KumarNo ratings yet

- Ch-4 Admission of A PartnerDocument4 pagesCh-4 Admission of A PartnerAmna SarfrazNo ratings yet

- Accountancy Test 2Document2 pagesAccountancy Test 2dixa mathpalNo ratings yet

- Retirement and Death (Revision) PDFDocument7 pagesRetirement and Death (Revision) PDFBHUMIKA JAINNo ratings yet

- Xyhhj 3 of 1 Aud 1 W EKXw QLDocument11 pagesXyhhj 3 of 1 Aud 1 W EKXw QLhk6206131516No ratings yet

- Q.1 What Is Meant by Reconstitution of Partnership Firm?: New Ratio 11:7:6Document24 pagesQ.1 What Is Meant by Reconstitution of Partnership Firm?: New Ratio 11:7:6SUSHANTNo ratings yet

- Ad Account Question PaperDocument3 pagesAd Account Question PaperAbdul Lathif0% (1)

- 06 Sample PaperDocument40 pages06 Sample Papergaming loverNo ratings yet

- Partnership - Admission of Partner - DPP 02 (Of Lecture 04) - (Kautilya)Document8 pagesPartnership - Admission of Partner - DPP 02 (Of Lecture 04) - (Kautilya)DevanshuNo ratings yet

- Sharada Mandir ISC 12 Accounts Term1 2017Document3 pagesSharada Mandir ISC 12 Accounts Term1 2017Manish SainiNo ratings yet

- Revision Notes On Chemical ThermodynamicsDocument6 pagesRevision Notes On Chemical ThermodynamicsManish SainiNo ratings yet

- Economics Class 11 Unit 15 Collection of DATADocument3 pagesEconomics Class 11 Unit 15 Collection of DATAManish SainiNo ratings yet

- Economics Class 11 Unit 15 Collection of DATADocument3 pagesEconomics Class 11 Unit 15 Collection of DATAManish SainiNo ratings yet

- QUES19Document2 pagesQUES19Manish Saini0% (1)

- Consumer Protection ActDocument25 pagesConsumer Protection ActManish SainiNo ratings yet

- CBSE Class 12 Accountancy - Retirement and Death of Partner PDFDocument5 pagesCBSE Class 12 Accountancy - Retirement and Death of Partner PDFManish SainiNo ratings yet

- Law of Demand - Elasticity of DemandDocument14 pagesLaw of Demand - Elasticity of DemandManish SainiNo ratings yet

- Track OnDocument1 pageTrack OnManish SainiNo ratings yet

- Law and IT Assignment SEM IXDocument18 pagesLaw and IT Assignment SEM IXrenu tomarNo ratings yet

- Annex B - Intake Sheet FinalDocument2 pagesAnnex B - Intake Sheet FinalCherry May Logdat-NgNo ratings yet

- Boreal Forests Canadian Shield Tundra Arctic Canadian Rockies Coast Mountains Prairies Great Lakes St. Lawrence RiverDocument2 pagesBoreal Forests Canadian Shield Tundra Arctic Canadian Rockies Coast Mountains Prairies Great Lakes St. Lawrence Riversaikiran100No ratings yet

- OO ALV Status Led LightDocument6 pagesOO ALV Status Led LightRam PraneethNo ratings yet

- Utilization of Agro-Industrial Wastes For The Production of Quality Oyster MushroomsDocument10 pagesUtilization of Agro-Industrial Wastes For The Production of Quality Oyster MushroomsMhelvene AlfarasNo ratings yet

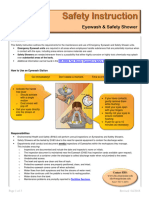

- Eyewash and Safety Shower SiDocument3 pagesEyewash and Safety Shower SiAli EsmaeilbeygiNo ratings yet

- Shezan Project Marketing 2009Document16 pagesShezan Project Marketing 2009Humayun100% (3)

- LoB Player Guide Pyram KingDocument15 pagesLoB Player Guide Pyram KingRonaldo SilveiraNo ratings yet

- Database Teach IctDocument3 pagesDatabase Teach IctMushawatuNo ratings yet

- A Conversation Explaining BiomimicryDocument6 pagesA Conversation Explaining Biomimicryapi-3703075100% (2)

- Muslim BotanistsDocument34 pagesMuslim BotanistsbilkaweNo ratings yet

- Knowledge of Cervical Cancer and Acceptance of HPVDocument6 pagesKnowledge of Cervical Cancer and Acceptance of HPVALIF FITRI BIN MOHD JASMINo ratings yet

- Form For Scholarship From INBA PDFDocument5 pagesForm For Scholarship From INBA PDFAjay SinghNo ratings yet

- The Future of Talent Management: Four Stages of Evolution: An Oracle White Paper June 2012Document19 pagesThe Future of Talent Management: Four Stages of Evolution: An Oracle White Paper June 2012aini amanNo ratings yet

- Amyand's HerniaDocument5 pagesAmyand's HerniamonoarulNo ratings yet

- Steering System (Notes On Tom)Document8 pagesSteering System (Notes On Tom)Vaibhav Vithoba Naik100% (1)

- Lataif, Exert Tafseer by Al QushayriDocument16 pagesLataif, Exert Tafseer by Al Qushayrimadanuodad100% (1)

- Evans SyndromeDocument13 pagesEvans SyndromerizeviNo ratings yet

- 4 Step Formula For A Killer IntroductionDocument8 pages4 Step Formula For A Killer IntroductionSHARMINE CABUSASNo ratings yet

- Tle Ap-Swine Q3 - WK3 - V4Document7 pagesTle Ap-Swine Q3 - WK3 - V4Maria Rose Tariga Aquino100% (1)

- Workstations InventoryDocument37 pagesWorkstations InventoryPacificNo ratings yet

- Occasional Paper 2 ICRCDocument82 pagesOccasional Paper 2 ICRCNino DunduaNo ratings yet

- CSS Assignment Case1 TheWeatherCompanyDocument6 pagesCSS Assignment Case1 TheWeatherCompanyNicole FritschNo ratings yet

- Philosophical Issues in TourismDocument2 pagesPhilosophical Issues in TourismLana Talita100% (1)

- Презентация smartwatchesDocument10 pagesПрезентация smartwatchesZiyoda AbdulloevaNo ratings yet

- Party Facility: Atty. Serrano LTD Lecture - July 12 Jzel EndozoDocument7 pagesParty Facility: Atty. Serrano LTD Lecture - July 12 Jzel EndozoJVLNo ratings yet

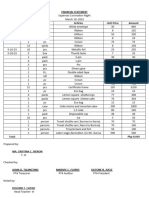

- Financial Statement Coronation NightDocument8 pagesFinancial Statement Coronation NightRuel Gapuz ManzanoNo ratings yet

- GRADE 8 NotesDocument5 pagesGRADE 8 NotesIya Sicat PatanoNo ratings yet

- Nod 321Document12 pagesNod 321PabloAyreCondoriNo ratings yet