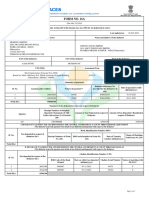

19 - Tds Chart For Fy 2008 - 09

19 - Tds Chart For Fy 2008 - 09

You might also like

- Swaminee PDFDocument16 pagesSwaminee PDFajay singh67% (21)

- TDS RateDocument9 pagesTDS RateGaurav SharmaNo ratings yet

- Tds Chart Fy2009 10Document1 pageTds Chart Fy2009 10hka90No ratings yet

- TDS Rate Chart For AY 2009-2010: Prepared By-Himanshu MalikDocument2 pagesTDS Rate Chart For AY 2009-2010: Prepared By-Himanshu Malikysr_cool100% (6)

- Less: Deduction@30%: © The Institute of Chartered Accountants of IndiaDocument12 pagesLess: Deduction@30%: © The Institute of Chartered Accountants of IndiaAashish soniNo ratings yet

- Img - 2134 2Document4 pagesImg - 2134 2Jasvinder SolankiNo ratings yet

- UBL Annual Report 2018-121Document1 pageUBL Annual Report 2018-121IFRS LabNo ratings yet

- Tax Practice Math Solution PDFDocument1 pageTax Practice Math Solution PDFnurulaminNo ratings yet

- Add: Depreciation As Per Books: © The Institute of Chartered Accountants of IndiaDocument15 pagesAdd: Depreciation As Per Books: © The Institute of Chartered Accountants of IndiaShubham KumarNo ratings yet

- Nnu LedgerDocument2 pagesNnu LedgermukeshnathmjNo ratings yet

- 9lso 2007 Jun ADocument6 pages9lso 2007 Jun ALucio Indiana WalazaNo ratings yet

- Audit Working LeaseDocument28 pagesAudit Working LeaseMuhammad Zain ShaikhNo ratings yet

- TDS Rates For AY 10-11 PDFDocument1 pageTDS Rates For AY 10-11 PDFjiten1986No ratings yet

- Aadcp9992n Q3 2023-24Document3 pagesAadcp9992n Q3 2023-24Harikrishan BhattNo ratings yet

- 2015 Jun Ans-8Document1 page2015 Jun Ans-8何健珩No ratings yet

- UBL Annual Report 2018-119Document1 pageUBL Annual Report 2018-119IFRS LabNo ratings yet

- Form No. 16A: From ToDocument3 pagesForm No. 16A: From ToPravat Kumar MohapatraNo ratings yet

- (I) (B) (Ii) (D) (Iii) (D) (Iv) (C) (V) (A) (Vi) (C) (Vii) (A) (Viii) (D) (Ix) (C) (X) (C)Document8 pages(I) (B) (Ii) (D) (Iii) (D) (Iv) (C) (V) (A) (Vi) (C) (Vii) (A) (Viii) (D) (Ix) (C) (X) (C)santosh palNo ratings yet

- 1967 - 202223 - REVISED - Revised 1 - Statement of IncomeDocument2 pages1967 - 202223 - REVISED - Revised 1 - Statement of IncomeSmita desaiNo ratings yet

- Report On Violations (RMO 15-2018)Document12 pagesReport On Violations (RMO 15-2018)Christian Albert HerreraNo ratings yet

- La Sallian Educational Innovators FoundationDocument15 pagesLa Sallian Educational Innovators FoundationDailyn JaectinNo ratings yet

- Apr-Jun 23Document3 pagesApr-Jun 23Vivian VaidyaNo ratings yet

- Taxation Sec A May 2024 1703224575Document10 pagesTaxation Sec A May 2024 1703224575Umang NagarNo ratings yet

- La Sallian Educational Innovators Foundation20211014-12-1nwllmnDocument16 pagesLa Sallian Educational Innovators Foundation20211014-12-1nwllmnmarie janNo ratings yet

- BTS Asst Details Cat B FY 2022-23Document5 pagesBTS Asst Details Cat B FY 2022-23kanishkasrivastava7No ratings yet

- TDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Document3 pagesTDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Prince RaichandNo ratings yet

- TAXATION - Tambunting Vs CIR - Tax DeductionDocument14 pagesTAXATION - Tambunting Vs CIR - Tax DeductionAimeeGraceAraniegoGarciaNo ratings yet

- OTHER+PERCENTAGE+TAXES-OCT.+24-student 3Document9 pagesOTHER+PERCENTAGE+TAXES-OCT.+24-student 3Aristeia NotesNo ratings yet

- The Institute of Computer AccountantsDocument1 pageThe Institute of Computer AccountantsankitNo ratings yet

- Dry de Fashion Pvt. Ltd. CALCUTTA - 711 102Document5 pagesDry de Fashion Pvt. Ltd. CALCUTTA - 711 102api-3706890No ratings yet

- 1098242CIT001 - Aboudi Private Limited NEWDocument1 page1098242CIT001 - Aboudi Private Limited NEWchanakaNo ratings yet

- Aacca3193k Q3 2024-25Document3 pagesAacca3193k Q3 2024-25Yogesh KanojiyaNo ratings yet

- Prayag Pande - Ajypp0194m - Q1 - Ay202223 - 16aDocument2 pagesPrayag Pande - Ajypp0194m - Q1 - Ay202223 - 16agitu sorgtNo ratings yet

- Aqxpa3351p Q1 2024-25Document3 pagesAqxpa3351p Q1 2024-25amrithavinilNo ratings yet

- S.Samanta & Co.: (Chartered Accountants)Document2 pagesS.Samanta & Co.: (Chartered Accountants)Samrat MajumderNo ratings yet

- Tax 2 Final Cheat Sheet 1.2Document2 pagesTax 2 Final Cheat Sheet 1.2HelloWorldNowNo ratings yet

- CIR v. Ayala HotelsDocument20 pagesCIR v. Ayala HotelsnoonalawNo ratings yet

- Viraj Wijeratne 2223 Revised SET ComputationDocument1 pageViraj Wijeratne 2223 Revised SET Computationattackdfg2002No ratings yet

- Adlpc4428j Q2 2023-24 1Document2 pagesAdlpc4428j Q2 2023-24 1jayashrimohanreddyNo ratings yet

- Aaaca4267a Q1 2023-24-1Document2 pagesAaaca4267a Q1 2023-24-1amrj27609No ratings yet

- TOPDocument2 pagesTOPMuhammad Zain ShaikhNo ratings yet

- 57 TDS Rate Chart BOARDDocument1 page57 TDS Rate Chart BOARDSatish GoenkaNo ratings yet

- Updated Concorde Amber Price Sheet 2016Document1 pageUpdated Concorde Amber Price Sheet 2016Mudit SrivastavaNo ratings yet

- Kasamahan Realty Development Corporation v. CIR, CTA Case No. 6204, February 16, 2005 PDFDocument25 pagesKasamahan Realty Development Corporation v. CIR, CTA Case No. 6204, February 16, 2005 PDFMary Fatima BerongoyNo ratings yet

- Part 2Document8 pagesPart 2Kushagra BurmanNo ratings yet

- Rashmi RanaDocument2 pagesRashmi RanaRashmi RanaNo ratings yet

- KBT Proposal SheetDocument14 pagesKBT Proposal SheetSouvik BakshiNo ratings yet

- Nabil Bank Q1 FY 2021Document28 pagesNabil Bank Q1 FY 2021Raj KarkiNo ratings yet

- PRINT Total Audit of Sidama Elto Civil Final September 24Document139 pagesPRINT Total Audit of Sidama Elto Civil Final September 24Jaspergroup 15No ratings yet

- Mkombozi Commercial Bank - Financial Statement Dec - 2019 PDFDocument1 pageMkombozi Commercial Bank - Financial Statement Dec - 2019 PDFMsuyaNo ratings yet

- 020520240633-Annexure 5 - Penalty ClausesDocument5 pages020520240633-Annexure 5 - Penalty ClausesPrateek JainNo ratings yet

- Basu Deb SharmaDocument1 pageBasu Deb SharmaBasudev SharmaNo ratings yet

- Ízf3Tè9Â Makatiâfinanceâco Âââ Â Ç, Â, 6hî Makati Finance CorpDocument2 pagesÍzf3Tè9Â Makatiâfinanceâco Âââ Â Ç, Â, 6hî Makati Finance CorpFelipe SorianoNo ratings yet

- Ulb 114 11 75Document3 pagesUlb 114 11 75psatyam2921No ratings yet

- T523 - Cashflow and Payment SchedDocument2 pagesT523 - Cashflow and Payment Schedbert cruzNo ratings yet

- Unit 2 Corporate Tax Planning and ManagementDocument21 pagesUnit 2 Corporate Tax Planning and Managementsankiworld3No ratings yet

- BTPN LKT Desember 2021 FinalDocument232 pagesBTPN LKT Desember 2021 FinalRido FebriansyahNo ratings yet

- FSMPP1416G Q1 2023-24Document3 pagesFSMPP1416G Q1 2023-24Parvez AhmadNo ratings yet

- Tendernotice 1Document12 pagesTendernotice 1Prabash BagNo ratings yet

- Chapter04.Personal ClaimsDocument181 pagesChapter04.Personal Claimsmpradip1975No ratings yet

- SB Orders Till 2011 PDFDocument202 pagesSB Orders Till 2011 PDFsmajumder_indNo ratings yet

- Introduction To TdsDocument28 pagesIntroduction To TdsGavendra BhartiNo ratings yet

- What Is TDS?: Tax Deducted at Source (TDS)Document8 pagesWhat Is TDS?: Tax Deducted at Source (TDS)Sandeep RajpootNo ratings yet

- Tds Rate Chart Fy 2014-15 Ay 2015-16 Tds Due Dates #SimpletaxindiaDocument11 pagesTds Rate Chart Fy 2014-15 Ay 2015-16 Tds Due Dates #Simpletaxindiashivashankari86No ratings yet

- Sub: Allotment of Tax Deduction Account Number (TAN) As Per Income Tax Act, 1961Document1 pageSub: Allotment of Tax Deduction Account Number (TAN) As Per Income Tax Act, 1961NitinNo ratings yet

- E Tax ManualDocument46 pagesE Tax ManualAbhai AgarwalNo ratings yet

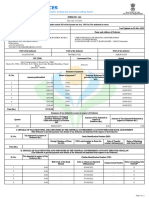

- 19 - Tds Chart For Fy 2008 - 09Document5 pages19 - Tds Chart For Fy 2008 - 09Naveen Kumar VNo ratings yet

- Form 49 B (TAN)Document4 pagesForm 49 B (TAN)Mohan NaiduNo ratings yet

- Tax Deduction/Collection Account Number: Meaning of TANDocument8 pagesTax Deduction/Collection Account Number: Meaning of TANOnkar BandichhodeNo ratings yet

Download as doc, pdf, or txt

You might also like

- Swaminee PDFDocument16 pagesSwaminee PDFajay singh67% (21)

- TDS RateDocument9 pagesTDS RateGaurav SharmaNo ratings yet

- Tds Chart Fy2009 10Document1 pageTds Chart Fy2009 10hka90No ratings yet

- TDS Rate Chart For AY 2009-2010: Prepared By-Himanshu MalikDocument2 pagesTDS Rate Chart For AY 2009-2010: Prepared By-Himanshu Malikysr_cool100% (6)

- Less: Deduction@30%: © The Institute of Chartered Accountants of IndiaDocument12 pagesLess: Deduction@30%: © The Institute of Chartered Accountants of IndiaAashish soniNo ratings yet

- Img - 2134 2Document4 pagesImg - 2134 2Jasvinder SolankiNo ratings yet

- UBL Annual Report 2018-121Document1 pageUBL Annual Report 2018-121IFRS LabNo ratings yet

- Tax Practice Math Solution PDFDocument1 pageTax Practice Math Solution PDFnurulaminNo ratings yet

- Add: Depreciation As Per Books: © The Institute of Chartered Accountants of IndiaDocument15 pagesAdd: Depreciation As Per Books: © The Institute of Chartered Accountants of IndiaShubham KumarNo ratings yet

- Nnu LedgerDocument2 pagesNnu LedgermukeshnathmjNo ratings yet

- 9lso 2007 Jun ADocument6 pages9lso 2007 Jun ALucio Indiana WalazaNo ratings yet

- Audit Working LeaseDocument28 pagesAudit Working LeaseMuhammad Zain ShaikhNo ratings yet

- TDS Rates For AY 10-11 PDFDocument1 pageTDS Rates For AY 10-11 PDFjiten1986No ratings yet

- Aadcp9992n Q3 2023-24Document3 pagesAadcp9992n Q3 2023-24Harikrishan BhattNo ratings yet

- 2015 Jun Ans-8Document1 page2015 Jun Ans-8何健珩No ratings yet

- UBL Annual Report 2018-119Document1 pageUBL Annual Report 2018-119IFRS LabNo ratings yet

- Form No. 16A: From ToDocument3 pagesForm No. 16A: From ToPravat Kumar MohapatraNo ratings yet

- (I) (B) (Ii) (D) (Iii) (D) (Iv) (C) (V) (A) (Vi) (C) (Vii) (A) (Viii) (D) (Ix) (C) (X) (C)Document8 pages(I) (B) (Ii) (D) (Iii) (D) (Iv) (C) (V) (A) (Vi) (C) (Vii) (A) (Viii) (D) (Ix) (C) (X) (C)santosh palNo ratings yet

- 1967 - 202223 - REVISED - Revised 1 - Statement of IncomeDocument2 pages1967 - 202223 - REVISED - Revised 1 - Statement of IncomeSmita desaiNo ratings yet

- Report On Violations (RMO 15-2018)Document12 pagesReport On Violations (RMO 15-2018)Christian Albert HerreraNo ratings yet

- La Sallian Educational Innovators FoundationDocument15 pagesLa Sallian Educational Innovators FoundationDailyn JaectinNo ratings yet

- Apr-Jun 23Document3 pagesApr-Jun 23Vivian VaidyaNo ratings yet

- Taxation Sec A May 2024 1703224575Document10 pagesTaxation Sec A May 2024 1703224575Umang NagarNo ratings yet

- La Sallian Educational Innovators Foundation20211014-12-1nwllmnDocument16 pagesLa Sallian Educational Innovators Foundation20211014-12-1nwllmnmarie janNo ratings yet

- BTS Asst Details Cat B FY 2022-23Document5 pagesBTS Asst Details Cat B FY 2022-23kanishkasrivastava7No ratings yet

- TDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Document3 pagesTDS Rates On Payments Other Than Salary and Wages To Residents (Including Domestic Companies)Prince RaichandNo ratings yet

- TAXATION - Tambunting Vs CIR - Tax DeductionDocument14 pagesTAXATION - Tambunting Vs CIR - Tax DeductionAimeeGraceAraniegoGarciaNo ratings yet

- OTHER+PERCENTAGE+TAXES-OCT.+24-student 3Document9 pagesOTHER+PERCENTAGE+TAXES-OCT.+24-student 3Aristeia NotesNo ratings yet

- The Institute of Computer AccountantsDocument1 pageThe Institute of Computer AccountantsankitNo ratings yet

- Dry de Fashion Pvt. Ltd. CALCUTTA - 711 102Document5 pagesDry de Fashion Pvt. Ltd. CALCUTTA - 711 102api-3706890No ratings yet

- 1098242CIT001 - Aboudi Private Limited NEWDocument1 page1098242CIT001 - Aboudi Private Limited NEWchanakaNo ratings yet

- Aacca3193k Q3 2024-25Document3 pagesAacca3193k Q3 2024-25Yogesh KanojiyaNo ratings yet

- Prayag Pande - Ajypp0194m - Q1 - Ay202223 - 16aDocument2 pagesPrayag Pande - Ajypp0194m - Q1 - Ay202223 - 16agitu sorgtNo ratings yet

- Aqxpa3351p Q1 2024-25Document3 pagesAqxpa3351p Q1 2024-25amrithavinilNo ratings yet

- S.Samanta & Co.: (Chartered Accountants)Document2 pagesS.Samanta & Co.: (Chartered Accountants)Samrat MajumderNo ratings yet

- Tax 2 Final Cheat Sheet 1.2Document2 pagesTax 2 Final Cheat Sheet 1.2HelloWorldNowNo ratings yet

- CIR v. Ayala HotelsDocument20 pagesCIR v. Ayala HotelsnoonalawNo ratings yet

- Viraj Wijeratne 2223 Revised SET ComputationDocument1 pageViraj Wijeratne 2223 Revised SET Computationattackdfg2002No ratings yet

- Adlpc4428j Q2 2023-24 1Document2 pagesAdlpc4428j Q2 2023-24 1jayashrimohanreddyNo ratings yet

- Aaaca4267a Q1 2023-24-1Document2 pagesAaaca4267a Q1 2023-24-1amrj27609No ratings yet

- TOPDocument2 pagesTOPMuhammad Zain ShaikhNo ratings yet

- 57 TDS Rate Chart BOARDDocument1 page57 TDS Rate Chart BOARDSatish GoenkaNo ratings yet

- Updated Concorde Amber Price Sheet 2016Document1 pageUpdated Concorde Amber Price Sheet 2016Mudit SrivastavaNo ratings yet

- Kasamahan Realty Development Corporation v. CIR, CTA Case No. 6204, February 16, 2005 PDFDocument25 pagesKasamahan Realty Development Corporation v. CIR, CTA Case No. 6204, February 16, 2005 PDFMary Fatima BerongoyNo ratings yet

- Part 2Document8 pagesPart 2Kushagra BurmanNo ratings yet

- Rashmi RanaDocument2 pagesRashmi RanaRashmi RanaNo ratings yet

- KBT Proposal SheetDocument14 pagesKBT Proposal SheetSouvik BakshiNo ratings yet

- Nabil Bank Q1 FY 2021Document28 pagesNabil Bank Q1 FY 2021Raj KarkiNo ratings yet

- PRINT Total Audit of Sidama Elto Civil Final September 24Document139 pagesPRINT Total Audit of Sidama Elto Civil Final September 24Jaspergroup 15No ratings yet

- Mkombozi Commercial Bank - Financial Statement Dec - 2019 PDFDocument1 pageMkombozi Commercial Bank - Financial Statement Dec - 2019 PDFMsuyaNo ratings yet

- 020520240633-Annexure 5 - Penalty ClausesDocument5 pages020520240633-Annexure 5 - Penalty ClausesPrateek JainNo ratings yet

- Basu Deb SharmaDocument1 pageBasu Deb SharmaBasudev SharmaNo ratings yet

- Ízf3Tè9Â Makatiâfinanceâco Âââ Â Ç, Â, 6hî Makati Finance CorpDocument2 pagesÍzf3Tè9Â Makatiâfinanceâco Âââ Â Ç, Â, 6hî Makati Finance CorpFelipe SorianoNo ratings yet

- Ulb 114 11 75Document3 pagesUlb 114 11 75psatyam2921No ratings yet

- T523 - Cashflow and Payment SchedDocument2 pagesT523 - Cashflow and Payment Schedbert cruzNo ratings yet

- Unit 2 Corporate Tax Planning and ManagementDocument21 pagesUnit 2 Corporate Tax Planning and Managementsankiworld3No ratings yet

- BTPN LKT Desember 2021 FinalDocument232 pagesBTPN LKT Desember 2021 FinalRido FebriansyahNo ratings yet

- FSMPP1416G Q1 2023-24Document3 pagesFSMPP1416G Q1 2023-24Parvez AhmadNo ratings yet

- Tendernotice 1Document12 pagesTendernotice 1Prabash BagNo ratings yet

- Chapter04.Personal ClaimsDocument181 pagesChapter04.Personal Claimsmpradip1975No ratings yet

- SB Orders Till 2011 PDFDocument202 pagesSB Orders Till 2011 PDFsmajumder_indNo ratings yet

- Introduction To TdsDocument28 pagesIntroduction To TdsGavendra BhartiNo ratings yet

- What Is TDS?: Tax Deducted at Source (TDS)Document8 pagesWhat Is TDS?: Tax Deducted at Source (TDS)Sandeep RajpootNo ratings yet

- Tds Rate Chart Fy 2014-15 Ay 2015-16 Tds Due Dates #SimpletaxindiaDocument11 pagesTds Rate Chart Fy 2014-15 Ay 2015-16 Tds Due Dates #Simpletaxindiashivashankari86No ratings yet

- Sub: Allotment of Tax Deduction Account Number (TAN) As Per Income Tax Act, 1961Document1 pageSub: Allotment of Tax Deduction Account Number (TAN) As Per Income Tax Act, 1961NitinNo ratings yet

- E Tax ManualDocument46 pagesE Tax ManualAbhai AgarwalNo ratings yet

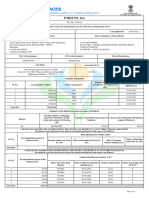

- 19 - Tds Chart For Fy 2008 - 09Document5 pages19 - Tds Chart For Fy 2008 - 09Naveen Kumar VNo ratings yet

- Form 49 B (TAN)Document4 pagesForm 49 B (TAN)Mohan NaiduNo ratings yet

- Tax Deduction/Collection Account Number: Meaning of TANDocument8 pagesTax Deduction/Collection Account Number: Meaning of TANOnkar BandichhodeNo ratings yet