Download as pdf or txt

You might also like

- Đề thi Tiếng Anh vào lớp 6 Chất lượng caoDocument21 pagesĐề thi Tiếng Anh vào lớp 6 Chất lượng caoNguyễn Ngọc Huyền57% (7)

- Fne306 Assignment 6 AnsDocument9 pagesFne306 Assignment 6 AnsMichael PironeNo ratings yet

- Account List in Grand Plaza Hanoi Ms. GiangDocument33 pagesAccount List in Grand Plaza Hanoi Ms. GiangCá NhỏNo ratings yet

- Trai Phieu 2Document7 pagesTrai Phieu 2NguyenNo ratings yet

- Trai Phieu 25Document7 pagesTrai Phieu 25NguyenNo ratings yet

- Trai Phieu 7Document6 pagesTrai Phieu 7NguyenNo ratings yet

- Trai Phieu 21Document6 pagesTrai Phieu 21NguyenNo ratings yet

- Trai Phieu 15Document6 pagesTrai Phieu 15NguyenNo ratings yet

- Trai Phieu 18Document6 pagesTrai Phieu 18NguyenNo ratings yet

- Trai Phieu 14Document6 pagesTrai Phieu 14NguyenNo ratings yet

- Trai Phieu 6Document6 pagesTrai Phieu 6NguyenNo ratings yet

- Current Macroeconomic SituationDocument13 pagesCurrent Macroeconomic SituationMonkey.D. LuffyNo ratings yet

- HTTPS:/WWW - Pnbmetlife.com/documents/met Invest - ULIP - Aug18 - tcm47-66816 PDFDocument33 pagesHTTPS:/WWW - Pnbmetlife.com/documents/met Invest - ULIP - Aug18 - tcm47-66816 PDFAbhinav VermaNo ratings yet

- Current Macroeconomic SituationDocument8 pagesCurrent Macroeconomic SituationMonkey.D. LuffyNo ratings yet

- GGP Ackman Presentation Ira Sohn Conf 5-26-10Document89 pagesGGP Ackman Presentation Ira Sohn Conf 5-26-10fstreet100% (2)

- Weekly Market Snapshot: Philippine EquitiesDocument2 pagesWeekly Market Snapshot: Philippine EquitiesJM CrNo ratings yet

- Research: State Bank of IndiaDocument7 pagesResearch: State Bank of IndiatihadaNo ratings yet

- Current Macroeconomic SituationDocument9 pagesCurrent Macroeconomic SituationMonkey.D. LuffyNo ratings yet

- Weekly Economic & Financial Commentary 15julyDocument13 pagesWeekly Economic & Financial Commentary 15julyErick Abraham MarlissaNo ratings yet

- BCG India Economic Monitor Dec 2020Document42 pagesBCG India Economic Monitor Dec 2020akashNo ratings yet

- Bond Market Weekly: China Merchants Securities Debt Capital MarketDocument4 pagesBond Market Weekly: China Merchants Securities Debt Capital MarketougyajNo ratings yet

- Wealth Insights Newsletter March 2021Document49 pagesWealth Insights Newsletter March 2021P.S.K.B MohanNo ratings yet

- 2Q10 Conference Call PresentationDocument27 pages2Q10 Conference Call PresentationJBS RINo ratings yet

- WW 2023.08.07-MinDocument3 pagesWW 2023.08.07-MinAlyssa TomanengNo ratings yet

- Bond MKT 2024Document16 pagesBond MKT 2024Dương Quốc Đạt 12A1No ratings yet

- Weekly Economic & Financial Commentary 18novDocument12 pagesWeekly Economic & Financial Commentary 18novErick Abraham MarlissaNo ratings yet

- Equity Market Update - December 2022Document32 pagesEquity Market Update - December 2022YasahNo ratings yet

- ICRA - Mutual Fund Screener - June 2021Document29 pagesICRA - Mutual Fund Screener - June 2021Dhanush KodiNo ratings yet

- Group18 Report123 VCB Tut2Document8 pagesGroup18 Report123 VCB Tut2Quynh Ngoc DangNo ratings yet

- Gathering Speed - Update On The Monetary Policy - June 2022Document5 pagesGathering Speed - Update On The Monetary Policy - June 2022Huzefa BharmalNo ratings yet

- Bank Central Asia TBK: Loan Restructuring To Suppress NIMDocument6 pagesBank Central Asia TBK: Loan Restructuring To Suppress NIMValentinus AdelioNo ratings yet

- TBAC Presentation Q2 2020Document31 pagesTBAC Presentation Q2 2020ZerohedgeNo ratings yet

- ICSC Mall REIT Presentation 12-7-2009Document68 pagesICSC Mall REIT Presentation 12-7-2009Terry Tate Buffett100% (1)

- February 17, 2014 Fixed Income Market Review: Pham Luu Hung (MR.) Associate DirectorDocument5 pagesFebruary 17, 2014 Fixed Income Market Review: Pham Luu Hung (MR.) Associate DirectorChrispy DuckNo ratings yet

- Market Highlights PDFDocument8 pagesMarket Highlights PDFPranati BhattacharjeeNo ratings yet

- Icici Bank: Strong Show ContinuesDocument15 pagesIcici Bank: Strong Show ContinuesMuskan ChoudharyNo ratings yet

- 1706018913-BP Equities Q3FY24 Result Update ICICI BankDocument5 pages1706018913-BP Equities Q3FY24 Result Update ICICI Banknilniruke14No ratings yet

- Treasury Outlook MarDocument6 pagesTreasury Outlook Marelise_stefanikNo ratings yet

- SageOne Investor Memo May 2023Document9 pagesSageOne Investor Memo May 2023debarkaNo ratings yet

- Utkarsh Small Finance Bank Report IciciDocument10 pagesUtkarsh Small Finance Bank Report IciciMohak PalNo ratings yet

- February 10, 2014 Fixed Income Market Review: Pham Luu Hung (MR.) Associate DirectorDocument5 pagesFebruary 10, 2014 Fixed Income Market Review: Pham Luu Hung (MR.) Associate DirectorChrispy DuckNo ratings yet

- Banking Sector UpdateDocument27 pagesBanking Sector UpdateAngel BrokingNo ratings yet

- Fixed Income Weekly 03082007Document3 pagesFixed Income Weekly 03082007FarahZBNo ratings yet

- May 2022 Strategy Call How To Make Money in A Recession Final.01Document40 pagesMay 2022 Strategy Call How To Make Money in A Recession Final.01xtremewhizNo ratings yet

- IDFC Research Motilal OswalDocument12 pagesIDFC Research Motilal OswalRohit GuptaNo ratings yet

- Lic Housing Finance - : Proxy To Play The Real Estate RecoveryDocument4 pagesLic Housing Finance - : Proxy To Play The Real Estate Recoverysaipavan999No ratings yet

- Shriram City Union Finance Ltd. - 204 - QuarterUpdateDocument12 pagesShriram City Union Finance Ltd. - 204 - QuarterUpdateSaran BaskarNo ratings yet

- Math Project ExampleDocument7 pagesMath Project Examplezaeemsiddiqi8No ratings yet

- Axis Bank Q1FY11Result UpdateDocument6 pagesAxis Bank Q1FY11Result UpdateSukesh KothariNo ratings yet

- Bank Central Asia TBK: 9M20 Review: Solid Capital and PPOPDocument7 pagesBank Central Asia TBK: 9M20 Review: Solid Capital and PPOPHamba AllahNo ratings yet

- Thematic-Weekly SDL Auction UpdateDocument8 pagesThematic-Weekly SDL Auction UpdateAjaya SahuNo ratings yet

- Bulan Bahagia Dan Sedih Di PMDocument24 pagesBulan Bahagia Dan Sedih Di PMSiti Hutami pratiwiNo ratings yet

- Indian Derivative Markets Future Prospects: CAPAM 2003 August 7, 2003Document27 pagesIndian Derivative Markets Future Prospects: CAPAM 2003 August 7, 2003api-19739167No ratings yet

- Bandhan Bankinvestor - Presentation - Q2FY21-22Document28 pagesBandhan Bankinvestor - Presentation - Q2FY21-22dumboooodogNo ratings yet

- Monthly Investment Recommendations August 2023Document18 pagesMonthly Investment Recommendations August 2023mark.muitaNo ratings yet

- SPP Capital Market Update June 2023Document10 pagesSPP Capital Market Update June 2023Jake RoseNo ratings yet

- PNJ 20240506 BuyDocument11 pagesPNJ 20240506 Buydhhung92No ratings yet

- AUSmall FinancebanklimitedDocument39 pagesAUSmall FinancebanklimitedDIPAN BISWASNo ratings yet

- Quantum Strategy II: Winning Strategies of Professional InvestmentFrom EverandQuantum Strategy II: Winning Strategies of Professional InvestmentNo ratings yet

- Trai Phieu 14Document6 pagesTrai Phieu 14NguyenNo ratings yet

- Trai Phieu 18Document6 pagesTrai Phieu 18NguyenNo ratings yet

- Trai Phieu 17Document12 pagesTrai Phieu 17NguyenNo ratings yet

- Quarterly Report: Fixed - Income ResearchDocument9 pagesQuarterly Report: Fixed - Income ResearchNguyenNo ratings yet

- Trai Phieu 15Document6 pagesTrai Phieu 15NguyenNo ratings yet

- Monthly Report: Fixed-Income ResearchDocument8 pagesMonthly Report: Fixed-Income ResearchNguyenNo ratings yet

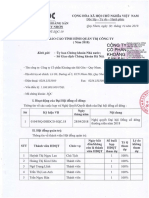

- Công Ty C PH N Khoáng S N Sài Gòn Quy NH NDocument5 pagesCông Ty C PH N Khoáng S N Sài Gòn Quy NH NNguyenNo ratings yet

- Trai Phieu 25Document7 pagesTrai Phieu 25NguyenNo ratings yet

- Trai Phieu 21Document6 pagesTrai Phieu 21NguyenNo ratings yet

- Trai Phieu 6Document6 pagesTrai Phieu 6NguyenNo ratings yet

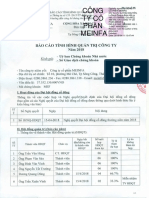

- MEF Baocaoquantri 2018Document3 pagesMEF Baocaoquantri 2018NguyenNo ratings yet

- Trai Phieu 2Document7 pagesTrai Phieu 2NguyenNo ratings yet

- Monthly Report: Fixed - Income ResearchDocument8 pagesMonthly Report: Fixed - Income ResearchNguyenNo ratings yet

- 2018-04-23 The New Yorker PDFDocument92 pages2018-04-23 The New Yorker PDFNguyen100% (2)

- Trai Phieu 7Document6 pagesTrai Phieu 7NguyenNo ratings yet

- Macroeconomic Research April 2019: by A Member of VIETCOMBANKDocument14 pagesMacroeconomic Research April 2019: by A Member of VIETCOMBANKNguyenNo ratings yet

- Tổng Công Ty Cổ Phần Y Tế DanamecoDocument14 pagesTổng Công Ty Cổ Phần Y Tế DanamecoNguyenNo ratings yet

- Energy From The Desert Ed-5 2015 LR PDFDocument171 pagesEnergy From The Desert Ed-5 2015 LR PDFNguyenNo ratings yet

- STIBET Applicationform U Ko-LaDocument3 pagesSTIBET Applicationform U Ko-LaNguyenNo ratings yet

- SLS Baocaotaichinh Q3 2019 PDFDocument25 pagesSLS Baocaotaichinh Q3 2019 PDFNguyenNo ratings yet

- Volunteers in Arts and Culture Organizations in Canada in 2007Document26 pagesVolunteers in Arts and Culture Organizations in Canada in 2007NguyenNo ratings yet

- Tong Hop 100 Topics Cho Ielts Speaking by Ngocbach PDFDocument160 pagesTong Hop 100 Topics Cho Ielts Speaking by Ngocbach PDFNguyenNo ratings yet

- 2011.01.27 Investing in Vietnam Private ClientsDocument40 pages2011.01.27 Investing in Vietnam Private ClientsNguyen Hoang DuyNo ratings yet

- Etra Exercise Unit 20Document2 pagesEtra Exercise Unit 20Nguyễn Kiều DuyênNo ratings yet

- Lý Thuyết Dịch Nhóm 9Document31 pagesLý Thuyết Dịch Nhóm 9Trương HùngNo ratings yet

- Curriculum Vitae 2016Document8 pagesCurriculum Vitae 2016Ly Thanh HaNo ratings yet

- HanoiGEO2015 First AnouncementDocument2 pagesHanoiGEO2015 First AnouncementRaphael Twin HoseaNo ratings yet

- A Special City in A Particular CountryDocument11 pagesA Special City in A Particular CountryThu TràNo ratings yet

- Mặt Bằng Bố Trí Nội ThấtDocument1 pageMặt Bằng Bố Trí Nội ThấtTrọng LêNo ratings yet

- Report On Corporate Governance: (First Half of 2013)Document40 pagesReport On Corporate Governance: (First Half of 2013)Nguyễn Vũ HoàngNo ratings yet

- Đề cương Biên dịch TA1 1Document18 pagesĐề cương Biên dịch TA1 1Ly PhamNo ratings yet

- Biên phiên Anh Việt-unitDocument10 pagesBiên phiên Anh Việt-unitgigileobuimoonNo ratings yet

- Train The Trainers 2023 - BookletDocument12 pagesTrain The Trainers 2023 - BookletHa ThaiNo ratings yet

- Itinerary Hanoi & SapaDocument2 pagesItinerary Hanoi & SapaNADZIRAH BINTI ABDUL LATIP MoeNo ratings yet

- Các yếu tố ảnh hưởng đến sự phát triển bền vững của nền kinh tế ban đêm Bằng chứng từ Hà Nội, Việt NamDocument18 pagesCác yếu tố ảnh hưởng đến sự phát triển bền vững của nền kinh tế ban đêm Bằng chứng từ Hà Nội, Việt NamPhạm Hồng SơnNo ratings yet

- AnalyseDocument5 pagesAnalyseMinh SangNo ratings yet

- Proceedings CIEMB 2023 POS - TIDocument54 pagesProceedings CIEMB 2023 POS - TIAnh LýNo ratings yet

- Habeco: Customers Service: Supply Chain ManagementDocument13 pagesHabeco: Customers Service: Supply Chain ManagementNguyễn Hồng HạnhNo ratings yet

- Macro Enviroment Report)Document5 pagesMacro Enviroment Report)api-3727690100% (1)

- Vinhomes Riverside Part 2 70 SốDocument16 pagesVinhomes Riverside Part 2 70 SốHoan Luu Van100% (1)

- Clothing and Footwear-Diesel Fashion Company-Premium ReportDocument29 pagesClothing and Footwear-Diesel Fashion Company-Premium ReporteasycarNo ratings yet

- Vietnamese Party-State and Religious Pluralism Since 1986 Building The Fatherland - Mathieu BOUQUETDocument20 pagesVietnamese Party-State and Religious Pluralism Since 1986 Building The Fatherland - Mathieu BOUQUETnvh92No ratings yet

- HISAMD2019 Program Final 02 PDFDocument12 pagesHISAMD2019 Program Final 02 PDFNguyễnMinhTuấnNo ratings yet

- Unilever Group Dove Intensive Repair: Situation Analyssis ReportDocument22 pagesUnilever Group Dove Intensive Repair: Situation Analyssis ReportQuỳnh Nguyễn Ngọc HươngNo ratings yet

- Ciemb 2022Document43 pagesCiemb 2022Hoang Anh NguyenNo ratings yet

- Thuvienkientrucchiase - 17kDocument812 pagesThuvienkientrucchiase - 17kXuanHieuTelecomNo ratings yet

- Saon LaiDocument6 pagesSaon LaiNguyễn Trung HiếuNo ratings yet

- 20 ĐỀ LUYỆN ANH KHỐI 5Document84 pages20 ĐỀ LUYỆN ANH KHỐI 5duyavk30No ratings yet

- ĐỀ THAM KHẢO ÔN TUYỂN SINH VÀO 10 CÓ KEY giaoandethitienganh 4Document5 pagesĐỀ THAM KHẢO ÔN TUYỂN SINH VÀO 10 CÓ KEY giaoandethitienganh 424 11Y6C Phạm Lâm TùngNo ratings yet

- VN Salary Guide 2019 - Lowres PDFDocument31 pagesVN Salary Guide 2019 - Lowres PDFTam HuynhNo ratings yet