Download as doc, pdf, or txt

You might also like

- Dishonour of Cheques in India: A Guide along with Model Drafts of Notices and ComplaintFrom EverandDishonour of Cheques in India: A Guide along with Model Drafts of Notices and ComplaintRating: 4 out of 5 stars4/5 (1)

- Form No.36: (See Rule 47 (1) )Document2 pagesForm No.36: (See Rule 47 (1) )itat hyderabadNo ratings yet

- Form No. 36 Form of Appeal To The Appellate Tribunal: Applicable)Document3 pagesForm No. 36 Form of Appeal To The Appellate Tribunal: Applicable)saurav royNo ratings yet

- Appeal FormDocument3 pagesAppeal Formmuhammad zaid100% (1)

- 1 UntitledDocument8 pages1 UntitledCA N RajeshNo ratings yet

- Synopsis - Circular and Annexure - 0Document9 pagesSynopsis - Circular and Annexure - 0tskk9896No ratings yet

- Form No. 35Document2 pagesForm No. 35NitishNo ratings yet

- Request For Appeal of Offer in CompromiseDocument2 pagesRequest For Appeal of Offer in CompromiseRuss TaylorNo ratings yet

- Inland Revenue Department: A. Applicant(s) DetailsDocument12 pagesInland Revenue Department: A. Applicant(s) DetailsVintonius Raffaele PRIMUSNo ratings yet

- 2.form of Appeal ACIR - MDocument4 pages2.form of Appeal ACIR - Mwasim nisarNo ratings yet

- OMB Form 3 - Request For Copy of Complaint - Case Documents FormDocument1 pageOMB Form 3 - Request For Copy of Complaint - Case Documents Formtweety68No ratings yet

- Request For Appeal of Offer in CompromiseDocument2 pagesRequest For Appeal of Offer in CompromiseNABEEL CHNo ratings yet

- Another Form of CaveatDocument4 pagesAnother Form of CaveatmmnamboothiriNo ratings yet

- Appealform 35Document2 pagesAppealform 35matrudutta dasNo ratings yet

- DY - CMM Acting For and On Behalf of The President of India Invites E-Tenders Against Tender No 61180789Document5 pagesDY - CMM Acting For and On Behalf of The President of India Invites E-Tenders Against Tender No 61180789GS OfficeNo ratings yet

- Allied Banking Corporation Vs CirDocument13 pagesAllied Banking Corporation Vs CirAnonymous VtsflLix1No ratings yet

- Form For Appeal To Appellate Authority: B. Sriman Narayana ReddyDocument2 pagesForm For Appeal To Appellate Authority: B. Sriman Narayana ReddySamachara HakkuNo ratings yet

- Power of Attorney and Declaration of RepresentativeDocument2 pagesPower of Attorney and Declaration of RepresentativeJohn KammererNo ratings yet

- US Internal Revenue Service: f8453nr - 1993Document2 pagesUS Internal Revenue Service: f8453nr - 1993IRSNo ratings yet

- US Internal Revenue Service: f8453nr - 1992Document2 pagesUS Internal Revenue Service: f8453nr - 1992IRSNo ratings yet

- Appeal FormatDocument3 pagesAppeal FormatSumairNo ratings yet

- Name Transfer Updated On 03.02.2017Document6 pagesName Transfer Updated On 03.02.2017Sarang PalewarNo ratings yet

- (See Rule 16CC and 17B) : 1. Substituted by The Income-Tax Amendment (3rd Amendment) Rules, 2023, W.E.FDocument18 pages(See Rule 16CC and 17B) : 1. Substituted by The Income-Tax Amendment (3rd Amendment) Rules, 2023, W.E.FRaghav TibdewalNo ratings yet

- Form No.35 Appeal To The Commissioner of Income Tax (Appeals) - 1, NashikDocument3 pagesForm No.35 Appeal To The Commissioner of Income Tax (Appeals) - 1, NashikNitin RautNo ratings yet

- Pointers On Legal MattersDocument3 pagesPointers On Legal MattersLiDdy Cebrero BelenNo ratings yet

- Patent Cooperation TreatyDocument2 pagesPatent Cooperation TreatyDarlene BoylesNo ratings yet

- US Internal Revenue Service: f8453nr - 1995Document2 pagesUS Internal Revenue Service: f8453nr - 1995IRSNo ratings yet

- Commissioner of Internal Revenue vs. The Stanley Works Sales (Phils.), IncorporatedDocument8 pagesCommissioner of Internal Revenue vs. The Stanley Works Sales (Phils.), IncorporatedJonjon BeeNo ratings yet

- Form 35 - Filed FormDocument11 pagesForm 35 - Filed FormcodfogusNo ratings yet

- 10B FormatDocument18 pages10B FormatBulan RoyNo ratings yet

- 10 - Advance App FormDocument1 page10 - Advance App Formbibimir560No ratings yet

- Please Accomplishment 5 (Five) Copies of This FormDocument34 pagesPlease Accomplishment 5 (Five) Copies of This FormRhoda Ivy Ulep Ilin-TandaanNo ratings yet

- Detailed BSDDocument10 pagesDetailed BSDHugh DunkerleyNo ratings yet

- Stand-Up India Loan Application Form-EnglishDocument5 pagesStand-Up India Loan Application Form-EnglishRajesh KumarNo ratings yet

- Documents Required For Registration Under Service TaxDocument7 pagesDocuments Required For Registration Under Service TaxVinay SinghNo ratings yet

- Verification of Work FormDocument4 pagesVerification of Work Formsarah marthinNo ratings yet

- Who Shall File NotesDocument1 pageWho Shall File NotesVher Christopher DucayNo ratings yet

- Form No-36bDocument3 pagesForm No-36bfrancais2No ratings yet

- Public Liability Claim 2020Document4 pagesPublic Liability Claim 2020Iain mc millanNo ratings yet

- IIFL MF Common Transaction Unit Holders 022819Document2 pagesIIFL MF Common Transaction Unit Holders 022819Sabyasachi ChatterjeeNo ratings yet

- RMC No. 71-2023 Annex A.1Document2 pagesRMC No. 71-2023 Annex A.1Ron Andi RamosNo ratings yet

- PDF ViewerDocument6 pagesPDF ViewerSanjay SharmaNo ratings yet

- Acceptance and Disclosure AgreementDocument1 pageAcceptance and Disclosure Agreementpaul100% (1)

- RA 9048 Form No-Clerical Error in Birth CertDocument2 pagesRA 9048 Form No-Clerical Error in Birth CertAnonymous K286lBXoth63% (8)

- Medicash Claim FormDocument6 pagesMedicash Claim Formwaran RMNo ratings yet

- Acceptance of ServiceDocument1 pageAcceptance of Servicesteelmshelby7No ratings yet

- Application For Approval of Master or Prototype or Volume Submitter PlansDocument3 pagesApplication For Approval of Master or Prototype or Volume Submitter PlansIRSNo ratings yet

- Checklist - Immediate Measure For RE WallDocument3 pagesChecklist - Immediate Measure For RE WallRahish RaviNo ratings yet

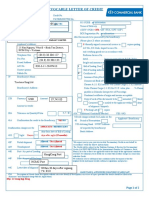

- Application For Irrevocable Letter of Credit: NH GhiDocument2 pagesApplication For Irrevocable Letter of Credit: NH GhiNguyễn Ngọc Phương LiêmNo ratings yet

- NOTICE and ANNEX A - FINAL VERSIONDocument4 pagesNOTICE and ANNEX A - FINAL VERSIONshariabordoNo ratings yet

- 4 Vat Forms 322-369.149193456 PDFDocument48 pages4 Vat Forms 322-369.149193456 PDFSravaniNo ratings yet

- Permanent Supply of EnergyDocument1 pagePermanent Supply of EnergyFecousels1960No ratings yet

- Cta - Eb - CV - 01565 - M - 2018jul16 - Ass 2Document6 pagesCta - Eb - CV - 01565 - M - 2018jul16 - Ass 27zpjrwprp4No ratings yet

- Mechanic's Lien Foreclosure: Vehicle InformationDocument2 pagesMechanic's Lien Foreclosure: Vehicle InformationToshiba userNo ratings yet

- BSBSformDocument2 pagesBSBSformProf BollaNo ratings yet

- ApplicationformDocument5 pagesApplicationformpradeepNo ratings yet

- Notice of Intention To Appeal Property Assessment: (One Parcel Per Form) Filing Deadline Is August 1Document2 pagesNotice of Intention To Appeal Property Assessment: (One Parcel Per Form) Filing Deadline Is August 1qwertyuiop1969No ratings yet

- 07 Protest Remedies Blacklisting Termination - EDITEDDocument84 pages07 Protest Remedies Blacklisting Termination - EDITEDmaricorNo ratings yet

- Court of Appeals: Chairperson, andDocument32 pagesCourt of Appeals: Chairperson, andMarcy BaklushNo ratings yet

- Apsara Vs AC 16-03Document4 pagesApsara Vs AC 16-03Usama malikNo ratings yet

- Egg Drop ResearchDocument4 pagesEgg Drop Researchapi-365288705No ratings yet

- Fosfomycin: Uses and Potentialities in Veterinary Medicine: Open Veterinary Journal March 2014Document19 pagesFosfomycin: Uses and Potentialities in Veterinary Medicine: Open Veterinary Journal March 2014Đăng LưuNo ratings yet

- Solved AnswersDocument11 pagesSolved AnswersChandrilNo ratings yet

- Cook's Illustrated 078Document36 pagesCook's Illustrated 078vicky610100% (3)

- Electromagnetic Interference (EMI) in Power SuppliesDocument41 pagesElectromagnetic Interference (EMI) in Power SuppliesAmarnath M DamodaranNo ratings yet

- Contextualized Online and Research SkillsDocument16 pagesContextualized Online and Research SkillsAubrey Castillo BrionesNo ratings yet

- DS PD Diagnostics System PD-TaD 62 BAURDocument4 pagesDS PD Diagnostics System PD-TaD 62 BAURAdhy Prastyo AfifudinNo ratings yet

- Consumers, Producers, and The Efficiency of MarketsDocument43 pagesConsumers, Producers, and The Efficiency of MarketsRoland EmersonNo ratings yet

- Normalize CssDocument8 pagesNormalize Cssreeder45960No ratings yet

- Burner Manual - 60 FTDocument18 pagesBurner Manual - 60 FTsambhajiNo ratings yet

- Salami Attacks and Their Mitigation - AnDocument4 pagesSalami Attacks and Their Mitigation - AnParmalik KumarNo ratings yet

- Chapter 3 Practice Problems Review and Assessment Solution 2 Use The V T Graph of The Toy Train in Figure 9 To Answer These QuestionsDocument52 pagesChapter 3 Practice Problems Review and Assessment Solution 2 Use The V T Graph of The Toy Train in Figure 9 To Answer These QuestionsAref DahabrahNo ratings yet

- Lab 27Document3 pagesLab 27api-239505062No ratings yet

- © The Institute of Chartered Accountants of IndiaDocument154 pages© The Institute of Chartered Accountants of IndiaJattu TatiNo ratings yet

- Bonds Payable Sample ProblemsDocument2 pagesBonds Payable Sample ProblemsErin LumogdangNo ratings yet

- Product Life Cycle Explained Stage and ExamplesDocument11 pagesProduct Life Cycle Explained Stage and ExamplesAkansha SharmaNo ratings yet

- Doing Business in Lao PDR: Tax & LegalDocument4 pagesDoing Business in Lao PDR: Tax & LegalParth Hemant PurandareNo ratings yet

- Honda CQ Eh8160akDocument37 pagesHonda CQ Eh8160aklondon335No ratings yet

- List - Parts of Bahay Na Bato - Filipiniana 101Document7 pagesList - Parts of Bahay Na Bato - Filipiniana 101Eriellynn Liza100% (1)

- Dominos Swot & 4 PsDocument10 pagesDominos Swot & 4 PsPrithvi BarodiaNo ratings yet

- Math Solo Plan NewDocument15 pagesMath Solo Plan NewMicah David SmithNo ratings yet

- (1872) Regulations For The Uniform and Dress of The Army of The United StatesDocument40 pages(1872) Regulations For The Uniform and Dress of The Army of The United StatesHerbert Hillary Booker 2nd100% (5)

- Scorpio SCDC LHD Mhawk Eiii v2 Mar12Document154 pagesScorpio SCDC LHD Mhawk Eiii v2 Mar12Romel Bladimir Valenzuela ValenzuelaNo ratings yet

- Ib 150 Al2Document16 pagesIb 150 Al2QasimNo ratings yet

- Catalog - Tesys Essential Guide - 2012 - (En)Document54 pagesCatalog - Tesys Essential Guide - 2012 - (En)Anonymous FTBYfqkNo ratings yet

- Affidavit of Loss - Bir.or - Car.1.2020Document1 pageAffidavit of Loss - Bir.or - Car.1.2020black stalkerNo ratings yet

- OISD ChecklistDocument3 pagesOISD ChecklistLoganathan DharmarNo ratings yet

- Maze ProblemDocument2 pagesMaze ProblemBhuvaneswari RamamurthyNo ratings yet

- HRM1Document13 pagesHRM1Niomi GolraiNo ratings yet