Download as pdf or txt

You might also like

- Zycus P2P Benchmark Report 2019 PDFDocument33 pagesZycus P2P Benchmark Report 2019 PDFpradeepvedulaNo ratings yet

- Future Proofing Your BrandDocument37 pagesFuture Proofing Your BrandOzzy López100% (2)

- Conquering the Seven Faces of Risk: Automated Momentum Strategies that Avoid Bear Markets, Empower Fearless Retirement PlanningFrom EverandConquering the Seven Faces of Risk: Automated Momentum Strategies that Avoid Bear Markets, Empower Fearless Retirement PlanningNo ratings yet

- Guo S Solutions To Derivatives Markets Fall 2007Document11 pagesGuo S Solutions To Derivatives Markets Fall 2007Nathaniel ArchibaldNo ratings yet

- NJ India InvestDocument43 pagesNJ India Investsachin100% (5)

- Derivatives Market Structure 2020 PRINT.20 2012 PDFDocument16 pagesDerivatives Market Structure 2020 PRINT.20 2012 PDFlaurence34No ratings yet

- 3Q18 Industrial Sentiment Survey October 2018Document19 pages3Q18 Industrial Sentiment Survey October 2018Mario Di MarcantonioNo ratings yet

- Asia Research - Stakeholder Survey 2021-22 (Final)Document34 pagesAsia Research - Stakeholder Survey 2021-22 (Final)rikasusanNo ratings yet

- GIIN - 2019 Annual Impact Investor Survey - ExecSumm - WebfileDocument8 pagesGIIN - 2019 Annual Impact Investor Survey - ExecSumm - Webfilemonomono90No ratings yet

- Fintech SurveyDocument22 pagesFintech Surveyali fatehiNo ratings yet

- Money Market Funds Survey ReportDocument53 pagesMoney Market Funds Survey Reporttalwareswapnil5No ratings yet

- 2018 GIIN AnnualSurvey ExecutiveSummary WebfileDocument8 pages2018 GIIN AnnualSurvey ExecutiveSummary WebfileLaxNo ratings yet

- ISDA Future of Derivatives SurveyDocument6 pagesISDA Future of Derivatives SurveySimon AltkornNo ratings yet

- A Study On Investors Preferences Towards Various Investment Avenues in Capital Market With Special Reference To DerivativesDocument10 pagesA Study On Investors Preferences Towards Various Investment Avenues in Capital Market With Special Reference To Derivativesmehul_mistry_30% (1)

- UTI Aggressive Hybrid Fund (Formerly UTI Hybrid Equity Fund)Document28 pagesUTI Aggressive Hybrid Fund (Formerly UTI Hybrid Equity Fund)rinkuparekh13No ratings yet

- Stress Testing at Major Financial Institutions:: Survey Results and PracticeDocument46 pagesStress Testing at Major Financial Institutions:: Survey Results and Practicebing mirandaNo ratings yet

- July 14 Understanding The CommitmentDocument3 pagesJuly 14 Understanding The Commitmentmecho satoNo ratings yet

- Sea Fas 2016 Global FX SurveyDocument22 pagesSea Fas 2016 Global FX SurveyMd. Al MamunNo ratings yet

- Research Note India's Hatchback IndustryDocument11 pagesResearch Note India's Hatchback IndustryVilluri BhargavNo ratings yet

- E Tailing Market - Clubfactory GMV - Ajio GMV - Redseer ConsultingDocument10 pagesE Tailing Market - Clubfactory GMV - Ajio GMV - Redseer ConsultingredseerNo ratings yet

- The State of Surveillance Storage 2018 SeagateDocument14 pagesThe State of Surveillance Storage 2018 SeagatePopa CatalinNo ratings yet

- In Consulting Strategy Bfs Consumerbehavior 062016 NoexpDocument12 pagesIn Consulting Strategy Bfs Consumerbehavior 062016 NoexpPhương TrầnNo ratings yet

- JaneStreet Inst ETF Trading Survey 2021Document16 pagesJaneStreet Inst ETF Trading Survey 2021Alan AnggaraNo ratings yet

- Eurex Factsheet - Msci - Index - Dividend - FuturesDocument2 pagesEurex Factsheet - Msci - Index - Dividend - Futures0840328818zNo ratings yet

- Tink Open Banking Survey 2019Document62 pagesTink Open Banking Survey 2019Anonymous 3fTQeuhBf100% (1)

- 10G Nick CiancioDocument69 pages10G Nick CiancioVedran BerkecNo ratings yet

- Accenture Investment Banking Survey ResearchDocument12 pagesAccenture Investment Banking Survey Researchjerry zaidiNo ratings yet

- Trust RadiusDocument64 pagesTrust RadiusAshishNo ratings yet

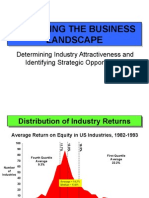

- Analyzing The Business LandscapeDocument18 pagesAnalyzing The Business Landscapedanic13No ratings yet

- Waters 0124 LSEG RMDDocument11 pagesWaters 0124 LSEG RMDAlexander Leanos (Xander)No ratings yet

- 2023 WIND Ventures VC Survey On Latin America For Startup GrowthDocument13 pages2023 WIND Ventures VC Survey On Latin America For Startup GrowthWIND VenturesNo ratings yet

- Key Findings: Pe Exits: 2018 Annual African Private Equity Data TrackerDocument1 pageKey Findings: Pe Exits: 2018 Annual African Private Equity Data TrackerethernalxNo ratings yet

- Hypera Pharma ApresentaçãoDocument97 pagesHypera Pharma ApresentaçãoMilton Gioia NetoNo ratings yet

- Walmart Flipkart Ir PresentationDocument17 pagesWalmart Flipkart Ir PresentationVishal JaiswalNo ratings yet

- State of PR 2022Document69 pagesState of PR 2022Nofa Haryanto Mch PrawiroNo ratings yet

- BLK 4Q22 Earnings SupplementDocument15 pagesBLK 4Q22 Earnings SupplementSatria MarhaendraNo ratings yet

- 360 ONE Balance Hybrid Fund NFO PresentationDocument35 pages360 ONE Balance Hybrid Fund NFO Presentationashish.sanghavi9218No ratings yet

- Skill Up Report 2019Document44 pagesSkill Up Report 2019v3n4No ratings yet

- Impact of Forex On Select It CompaniesDocument49 pagesImpact of Forex On Select It CompaniesvijayNo ratings yet

- Subodh Institute of Management&Career StudiesDocument14 pagesSubodh Institute of Management&Career Studieskaps_er_3No ratings yet

- BAI Business Agility Report 2018Document22 pagesBAI Business Agility Report 2018Jean Paul Saltos100% (1)

- First Round Capital Original Pitch DeckDocument10 pagesFirst Round Capital Original Pitch DeckFirst Round CapitalNo ratings yet

- First Round Capital Slide Deck PDFDocument10 pagesFirst Round Capital Slide Deck PDFEmily StanfordNo ratings yet

- First Round Capital Original Pitch DeckDocument10 pagesFirst Round Capital Original Pitch DeckJessi Craige ShikmanNo ratings yet

- Brochure Columbia Value Investing 11 Sep 19 V9Document16 pagesBrochure Columbia Value Investing 11 Sep 19 V9iwazherNo ratings yet

- Puppet State of Devops Market Segmentation Report - 1Document23 pagesPuppet State of Devops Market Segmentation Report - 1bhikshuNo ratings yet

- Dr Zero- Vietnam Shamp Market InformationsDocument25 pagesDr Zero- Vietnam Shamp Market Informationshieu.ln00456No ratings yet

- Determining The Optimal Capital Structure: A Practical Contemporary ApproachDocument16 pagesDetermining The Optimal Capital Structure: A Practical Contemporary ApproachAyudya Puti RamadhantyNo ratings yet

- Navigating Car Preferences Across Demographics - FINALDocument18 pagesNavigating Car Preferences Across Demographics - FINALgaya14No ratings yet

- Model 3 Cett ReportDocument58 pagesModel 3 Cett Reporthinduja987No ratings yet

- Industry Intelligence - Uber: Ridesharing Services Industry AnalysisDocument31 pagesIndustry Intelligence - Uber: Ridesharing Services Industry AnalysisRediet TsigeberhanNo ratings yet

- Deloitte NL S&o Global Outsourcing Survey PDFDocument17 pagesDeloitte NL S&o Global Outsourcing Survey PDFRaitei AmanoNo ratings yet

- Coping With COVID-19: Research Education DialogueDocument13 pagesCoping With COVID-19: Research Education DialogueVito NarducciNo ratings yet

- Value Investing (Online) : Making Intelligent Investment DecisionsDocument16 pagesValue Investing (Online) : Making Intelligent Investment DecisionsPepe PerezNo ratings yet

- EA Report IFMR Goa Institute of Management FinGIMDocument19 pagesEA Report IFMR Goa Institute of Management FinGIMHomo SapienNo ratings yet

- 2020 Global Divestiture Survey: Defensive M&A For A Resilient PortfolioDocument28 pages2020 Global Divestiture Survey: Defensive M&A For A Resilient PortfoliokumarbipinshahNo ratings yet

- Know Your Behavioural BiasesDocument44 pagesKnow Your Behavioural BiasesShreeraj ModiNo ratings yet

- Annual Report For The Year Ended December 31 2020Document132 pagesAnnual Report For The Year Ended December 31 2020MuhammadNo ratings yet

- Making AI A Killer App For Your Data - A Practical Guide - Sponsored by IBM Watson PresentationDocument14 pagesMaking AI A Killer App For Your Data - A Practical Guide - Sponsored by IBM Watson PresentationjombibiNo ratings yet

- Managing Global Financial and Foreign Exchange Rate RiskFrom EverandManaging Global Financial and Foreign Exchange Rate RiskNo ratings yet

- Making Foreign Direct Investment Work for Sub-Saharan AfricaFrom EverandMaking Foreign Direct Investment Work for Sub-Saharan AfricaNo ratings yet

- Beyond The Last Blue Mountain - Group - 2Document6 pagesBeyond The Last Blue Mountain - Group - 2Amna NashitNo ratings yet

- Revenue and Gross Profit Operating Expenses: (Except For Per Share Items) Income StatementDocument16 pagesRevenue and Gross Profit Operating Expenses: (Except For Per Share Items) Income StatementAmna NashitNo ratings yet

- ElectivesDocument21 pagesElectivesAmna NashitNo ratings yet

- Dabur Chyawanprash - BriefDocument12 pagesDabur Chyawanprash - BriefAmna NashitNo ratings yet

- Egypt Oil and Gas OverviewDocument5 pagesEgypt Oil and Gas OverviewAmna NashitNo ratings yet

- Ankit ResumeDocument2 pagesAnkit ResumeAmna NashitNo ratings yet

- Et - Manac - 2014 SolutionDocument5 pagesEt - Manac - 2014 SolutionAmna NashitNo ratings yet

- 9M16 Investor UpdateDocument19 pages9M16 Investor UpdateAmna NashitNo ratings yet

- Dea Annual Report 2015Document29 pagesDea Annual Report 2015Amna NashitNo ratings yet

- GeologyDocument5 pagesGeologyAmna Nashit100% (1)

- Cantu-Chapa, 2009 Ammonites Taraises FMDocument26 pagesCantu-Chapa, 2009 Ammonites Taraises FMAmna NashitNo ratings yet

- Wind Speed Map IndiaDocument12 pagesWind Speed Map IndiaAn1rudh_Sharma100% (1)

- Financial Markets and InstitutionsDocument32 pagesFinancial Markets and Institutionsalex_obregon_6No ratings yet

- Chapter 11Document11 pagesChapter 11Jonathan C. BalansagNo ratings yet

- Introduction To Swaps and Their Application in PakistanDocument17 pagesIntroduction To Swaps and Their Application in PakistanSaad Bin Mehmood100% (4)

- Legal Aspects of BusinessDocument24 pagesLegal Aspects of BusinessManoj K Singh100% (2)

- Assignment For DerivativesDocument17 pagesAssignment For DerivativesMohammad ArsalanNo ratings yet

- ICICI Prudential Mutual FundDocument36 pagesICICI Prudential Mutual FundChintan JainNo ratings yet

- VO Codes: List of Codes For Foreign Exchange and Other Transactions by Non-Resi-Dents and ResidentsDocument6 pagesVO Codes: List of Codes For Foreign Exchange and Other Transactions by Non-Resi-Dents and ResidentsLisny V MNo ratings yet

- 2 Financial Statements of Bank - For StudentDocument75 pages2 Financial Statements of Bank - For StudenttusedoNo ratings yet

- 2023-0042-Policy-SEBI Master Circular On Surveillance of Securities MarketDocument28 pages2023-0042-Policy-SEBI Master Circular On Surveillance of Securities MarketmrpankajjainetahNo ratings yet

- InvestmentDocument11 pagesInvestmentTilahun GirmaNo ratings yet

- European Dividend Swap Master Confirmation AgreementDocument12 pagesEuropean Dividend Swap Master Confirmation AgreementmartinkemberNo ratings yet

- International Financial Management: by Jeff MaduraDocument48 pagesInternational Financial Management: by Jeff MaduraBe Like ComsianNo ratings yet

- Lamco Docket 7578Document176 pagesLamco Docket 7578Troy UhlmanNo ratings yet

- CAF For Reliance SIP Insure - 24 10 2017 Full PDFDocument51 pagesCAF For Reliance SIP Insure - 24 10 2017 Full PDFARVINDNo ratings yet

- En BookDocument46 pagesEn BookEnid CallaNo ratings yet

- 2 Forex Management McqsDocument12 pages2 Forex Management McqsPadyala Sriram100% (1)

- Paper Kelompok 6 - Instrumen Efek Di Pasar Modal Revised PDFDocument18 pagesPaper Kelompok 6 - Instrumen Efek Di Pasar Modal Revised PDFDanang SufiantoNo ratings yet

- Has Finance Made The World RiskierDocument36 pagesHas Finance Made The World RiskierbbarooahNo ratings yet

- Concho Investor PresentationDocument23 pagesConcho Investor PresentationRoger MunizNo ratings yet

- L2 CFA Schedule - Jun 2011Document28 pagesL2 CFA Schedule - Jun 2011mengcheeNo ratings yet

- Re: Proposed Rules: Registration of Swap Dealers and Major Swap Participants (RIN 3038 - AC95)Document7 pagesRe: Proposed Rules: Registration of Swap Dealers and Major Swap Participants (RIN 3038 - AC95)MarketsWikiNo ratings yet

- Chandan Sharma Project11Document92 pagesChandan Sharma Project11Chandan SharmaNo ratings yet

- Jocelyn Tan Hui Ying 18Wbr09382 IndividualDocument6 pagesJocelyn Tan Hui Ying 18Wbr09382 IndividualYChoonChuahNo ratings yet

- Vanguard Global Stock Index FundDocument4 pagesVanguard Global Stock Index FundjorgeperezsidecarshotmailomNo ratings yet

- Monthly Portfolio April 2021Document37 pagesMonthly Portfolio April 2021Visnu SankarNo ratings yet

- IAS 39 MacrohedgingDocument64 pagesIAS 39 MacrohedgingMariana MirelaNo ratings yet

- On The Goldman Sachs Investment - Warren BuffettDocument12 pagesOn The Goldman Sachs Investment - Warren BuffettRommel AcostaNo ratings yet

- BF2207 Chapter 05 - Blades Case - Use of Currency Derivative InstrumentsDocument3 pagesBF2207 Chapter 05 - Blades Case - Use of Currency Derivative InstrumentsAaron CheongNo ratings yet

- Master in Trading BrochureDocument17 pagesMaster in Trading Brochureace187No ratings yet