Download as pdf or txt

You might also like

- Financial Analysis ReportDocument6 pagesFinancial Analysis ReportDistingNo ratings yet

- Investment Banking Chapter 1Document27 pagesInvestment Banking Chapter 1ravindergudikandulaNo ratings yet

- Financial Ratio AnalysisDocument3 pagesFinancial Ratio Analysisijaz bokhariNo ratings yet

- Ratio AnalysisDocument12 pagesRatio AnalysisSachinNo ratings yet

- IM-Chapter 7 Portfolio TheoryDocument32 pagesIM-Chapter 7 Portfolio TheoryVirali Jadeja100% (1)

- Profitability Ratios: and Allowances) Minus Cost of SalesDocument2 pagesProfitability Ratios: and Allowances) Minus Cost of Salesrachel anne belangelNo ratings yet

- Ratio Analysis of Three Different IndustriesDocument142 pagesRatio Analysis of Three Different IndustriesAbdullah Al-RafiNo ratings yet

- Concept of Financial AnalysisDocument20 pagesConcept of Financial AnalysisJonathan 24No ratings yet

- Cashflow StatementDocument14 pagesCashflow StatementVivek RanjanNo ratings yet

- Financial AnalysisDocument44 pagesFinancial AnalysisPravin NimbalkarNo ratings yet

- Financial Analysis 1Document38 pagesFinancial Analysis 1Crestine Joyce Mirabel DelaCruzNo ratings yet

- Analisis RatioDocument5 pagesAnalisis RatioKata AssalamualaikumNo ratings yet

- About Basic BudgetingDocument44 pagesAbout Basic BudgetingatifhassansiddiquiNo ratings yet

- Company Accounts: - in Law, Company' Is Termed As An Entity Which Is Formed andDocument9 pagesCompany Accounts: - in Law, Company' Is Termed As An Entity Which Is Formed andAnshul BajpaiNo ratings yet

- Weighted Average Cost of Capital: Banikanta MishraDocument21 pagesWeighted Average Cost of Capital: Banikanta MishraManu ThomasNo ratings yet

- C.A IPCC Ratio AnalysisDocument6 pagesC.A IPCC Ratio AnalysisAkash Gupta100% (2)

- CH 6-Beta Estimation and Cost of EquityDocument26 pagesCH 6-Beta Estimation and Cost of EquityJyoti Bansal100% (1)

- Financial LeverageDocument21 pagesFinancial LeverageSarab Gurpreet BatraNo ratings yet

- Corporate Finance PDFDocument56 pagesCorporate Finance PDFdevNo ratings yet

- Taxation in PakistanDocument22 pagesTaxation in PakistanAdnan AkramNo ratings yet

- Financial Ratios - Formula SheetDocument4 pagesFinancial Ratios - Formula SheetAira Dela CruzNo ratings yet

- Gordon Model For Intrinsic ValueDocument2 pagesGordon Model For Intrinsic ValueImran Ansari100% (1)

- Capital AllowancesDocument32 pagesCapital AllowancesMakoni CharityNo ratings yet

- Advanced Taxation CH - 1Document9 pagesAdvanced Taxation CH - 1Mekuriaw MezgebuNo ratings yet

- NPV, Irr, ArrDocument9 pagesNPV, Irr, ArrAhsan MubeenNo ratings yet

- Financial Statement AnalysisDocument55 pagesFinancial Statement AnalysisPravin UntooNo ratings yet

- 0452 w03 QP 1Document11 pages0452 w03 QP 1MahmozNo ratings yet

- F 3 Financial StrategyDocument3 pagesF 3 Financial StrategyOlalekan PopoolaNo ratings yet

- CH 3-Valuation of Bond and SharesDocument40 pagesCH 3-Valuation of Bond and SharesJyoti Bansal67% (3)

- DCF ValuationDocument3 pagesDCF ValuationDurga ShankarNo ratings yet

- Financial RatiosDocument4 pagesFinancial Ratiossarahbabe94No ratings yet

- Ratio Analysis: Important FormulaDocument4 pagesRatio Analysis: Important FormulaHarsh Vardhan KatnaNo ratings yet

- Case Study Ratio AnalysisDocument6 pagesCase Study Ratio Analysisash867240% (1)

- UNIT-3 Financial Planning and ForecastingDocument33 pagesUNIT-3 Financial Planning and ForecastingAssfaw KebedeNo ratings yet

- What Is Comparable Company Analysis?: Valuation Methodology Intrinsic Form of ValuationDocument4 pagesWhat Is Comparable Company Analysis?: Valuation Methodology Intrinsic Form of ValuationElla FuenteNo ratings yet

- IntroductionDocument83 pagesIntroductionnatiNo ratings yet

- Auditing and Corporate GovernanceDocument10 pagesAuditing and Corporate GovernancealexandraNo ratings yet

- United Bank Limited (Ubl) Complete Ratio Analysis For Internship Report YEAR 2008, 2009, 2010Document0 pagesUnited Bank Limited (Ubl) Complete Ratio Analysis For Internship Report YEAR 2008, 2009, 2010Elegant EmeraldNo ratings yet

- Revision Notes Group Accounts PDFDocument11 pagesRevision Notes Group Accounts PDFEhsanulNo ratings yet

- Financial Ratio Summary SheetDocument1 pageFinancial Ratio Summary SheetKeith Tomasson100% (1)

- LN01 Rejda99500X 12 Principles LN04Document40 pagesLN01 Rejda99500X 12 Principles LN04Abdirahman M. SalahNo ratings yet

- Preparation of Financial-StatementsDocument32 pagesPreparation of Financial-StatementsRajesh GuptaNo ratings yet

- Accounting StandardsDocument22 pagesAccounting Standardsdodiyavijay25691No ratings yet

- Unit 1 Introduction To Financial ManagementDocument12 pagesUnit 1 Introduction To Financial ManagementPRIYA KUMARINo ratings yet

- Unit 3 Financial Statement Analysis BBS Notes eduNEPAL - Info - PDFDocument3 pagesUnit 3 Financial Statement Analysis BBS Notes eduNEPAL - Info - PDFGrethel Tarun MalenabNo ratings yet

- Lecture No.2 Financial Statements AnalysisDocument17 pagesLecture No.2 Financial Statements AnalysisSokoine Hamad Denis100% (1)

- Sources of FinanceDocument26 pagesSources of Financevyasgautam28No ratings yet

- Projected Balance SheetDocument1 pageProjected Balance Sheetr.jeyashankar9550100% (1)

- Methods of Stock ValuationDocument3 pagesMethods of Stock ValuationQuartz KrystalNo ratings yet

- Financial Management - PPT - 2011Document134 pagesFinancial Management - PPT - 2011Bhanu Prakash100% (1)

- Chapter-9, Capital StructureDocument21 pagesChapter-9, Capital StructurePooja SheoranNo ratings yet

- Valuation of GoodwillDocument16 pagesValuation of GoodwillManas Maheshwari100% (1)

- Couresot LineDocument2 pagesCouresot LineSeifu BekeleNo ratings yet

- Valuation Measurement and Value CreationDocument44 pagesValuation Measurement and Value CreationalijordanNo ratings yet

- 4405 Principles of AccountingDocument25 pages4405 Principles of AccountingDapheny100% (1)

- Assignment Ratio AnalysisDocument7 pagesAssignment Ratio AnalysisMrinal Kanti DasNo ratings yet

- Stock ValuationDocument71 pagesStock ValuationLee ChiaNo ratings yet

- Bav Unit 4th DCFDocument57 pagesBav Unit 4th DCFRahul GuptaNo ratings yet

- Understanding IFRS Fundamentals: International Financial Reporting StandardsFrom EverandUnderstanding IFRS Fundamentals: International Financial Reporting StandardsNo ratings yet

- Parcor Proj (Version 1)Document33 pagesParcor Proj (Version 1)Jwhll MaeNo ratings yet

- Chapter 6 Tutorial QuestionsDocument3 pagesChapter 6 Tutorial QuestionsAlefosio FonotiNo ratings yet

- Past Paper Analysis CAF-08 CMACDocument1 pagePast Paper Analysis CAF-08 CMACMuneer DhamaniNo ratings yet

- 11 Oct 2022Document3 pages11 Oct 2022Maestro ProsperNo ratings yet

- Us Interim Operating Model PovDocument12 pagesUs Interim Operating Model Povdnghainam133No ratings yet

- Accounting Formula Cheat SheetDocument1 pageAccounting Formula Cheat SheetMarta Fdez-FournierNo ratings yet

- BFIB 234 Corporate Accounting CP 2022-23Document14 pagesBFIB 234 Corporate Accounting CP 2022-23harshit119No ratings yet

- CARAJACLASSDocument22 pagesCARAJACLASSBavya MohanNo ratings yet

- For Tuesday, Mar 21 : Venture Capital Problem SetDocument3 pagesFor Tuesday, Mar 21 : Venture Capital Problem SetJerry Chang0% (1)

- Costing UG v2022EEDocument96 pagesCosting UG v2022EEKumarNo ratings yet

- Perhitungan Ben and JerryDocument14 pagesPerhitungan Ben and JerryHady LieNo ratings yet

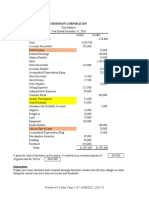

- Thompson Corporation: InstructionsDocument7 pagesThompson Corporation: InstructionsrahmawNo ratings yet

- Yes BankDocument4 pagesYes BankgetaNo ratings yet

- FMR Oct 2023Document39 pagesFMR Oct 2023Qamber RazaNo ratings yet

- Lopez, Ella Marie - Quiz 2 FinanarepDocument4 pagesLopez, Ella Marie - Quiz 2 FinanarepElla Marie Lopez0% (1)

- Week Six Top Schools RatiosDocument7 pagesWeek Six Top Schools Ratiossurfbum2006No ratings yet

- BDC224 FD ADV Financial Statement A4Document1 pageBDC224 FD ADV Financial Statement A4bscjjwNo ratings yet

- e-StatementBRImo 018201035263506 Apr2023 20230703 143056Document2 pagese-StatementBRImo 018201035263506 Apr2023 20230703 143056NONO MULYANANo ratings yet

- Samyak Jain - IIM RanchiDocument2 pagesSamyak Jain - IIM RanchiNeha GuptaNo ratings yet

- Corporate Financial Statements - IDocument11 pagesCorporate Financial Statements - ISoumya Ranjan PradhanNo ratings yet

- Chapter 12 Exercise SolutionDocument95 pagesChapter 12 Exercise SolutionKai FaggornNo ratings yet

- ACI Limited Submitted To:: ULAB School of Business Bachelor of Business Administration (B.B.A.) Term Paper OnDocument13 pagesACI Limited Submitted To:: ULAB School of Business Bachelor of Business Administration (B.B.A.) Term Paper OnashikNo ratings yet

- Analisis Investasi Tambang - 3Document21 pagesAnalisis Investasi Tambang - 3adrian nurhadiNo ratings yet

- Overhead Analysis QuestionsDocument9 pagesOverhead Analysis QuestionsKiri chrisNo ratings yet

- Process and Operating CostingDocument20 pagesProcess and Operating CostingBHANU PRATAP SINGHNo ratings yet

- Lesson 15 The Stock Market 15.1. Warm-Up QuestionsDocument1 pageLesson 15 The Stock Market 15.1. Warm-Up QuestionsÖmer Faruk EserNo ratings yet

- CFAS Millan CHAPTERS 20-22Document16 pagesCFAS Millan CHAPTERS 20-22Maria Mikaela ReyesNo ratings yet

- COGM Dan Income StatementDocument3 pagesCOGM Dan Income StatementABDUL KHALIQ BRUTUNo ratings yet

- BIMB Vs BSN PDFDocument10 pagesBIMB Vs BSN PDFIelts TutorNo ratings yet

- RAS - GEC Elec 2 - Activity #5Document2 pagesRAS - GEC Elec 2 - Activity #5George Blaire Ras100% (1)